Artem Zakharov/iStock via Getty Images

Artem Zakharov/iStock via Getty Images

It's always important to be mindful of how far a company's share price has gone compared to what its ultimate potential is. You may buy into shares of a company expecting a certain amount of upside. And after that upside is achieved, better opportunities abound elsewhere. However, I can speak from experience when I say that it's not always easy to sell a stock, especially one that has performed so well. But as I get more experience with investing, on top of the 15 years I already have, that process becomes easier.

A great example of when it might make time to look elsewhere for opportunities can be seen by looking at Vulcan Materials Company (NYSE:VMC), a provider of aggregates, asphalt, and ready mix concrete. Although this is not an exciting space for many investors, I find it to be fascinating. It's a simple business with simple economics that bodes well during times of economic expansion. Input costs are often tightly controlled, and cash flows have the potential to be quite robust. These factors, combined with the right price, can create a great opportunity.

Back in July of last year, as an example, I ended up rating Vulcan Materials Company (VMC) a "buy" For these reasons. And since then, things have gone really well. Shares have seen an upside of 21%, which is nearly double the 10.8% rise seen by the S&P 500 (SP500).

Unfortunately, all good things must come to an end. And the way I see it, now is a prime time to downgrade the stock to a "hold" even though it has potential in the long run.

Author - SEC EDGAR Data

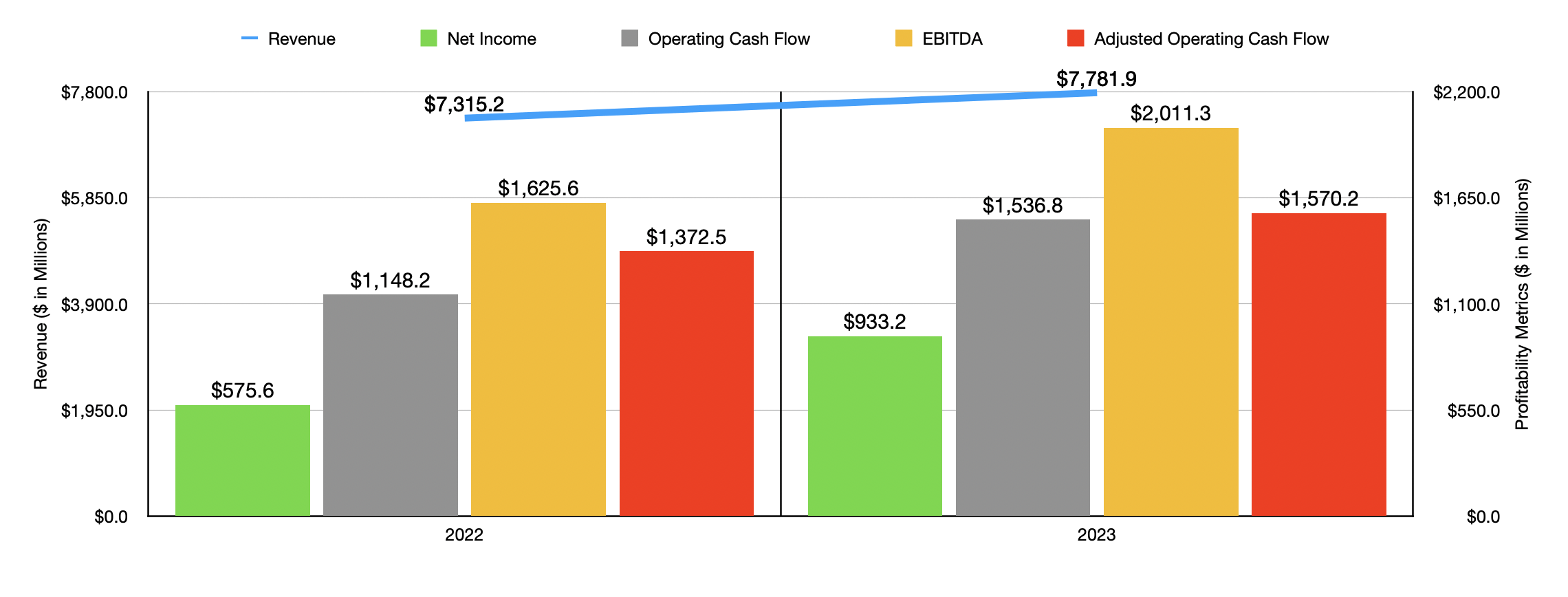

Fundamentally speaking, Vulcan Materials has been performing quite well. When I last wrote about the company, we had data extending through the first quarter of the 2023 fiscal year. Today, that data now extends through 2023 in its entirety. According to management, revenue for 2023 came in at $7.78 billion. That's 6.4% higher than the $7.32 billion generated in 2022.

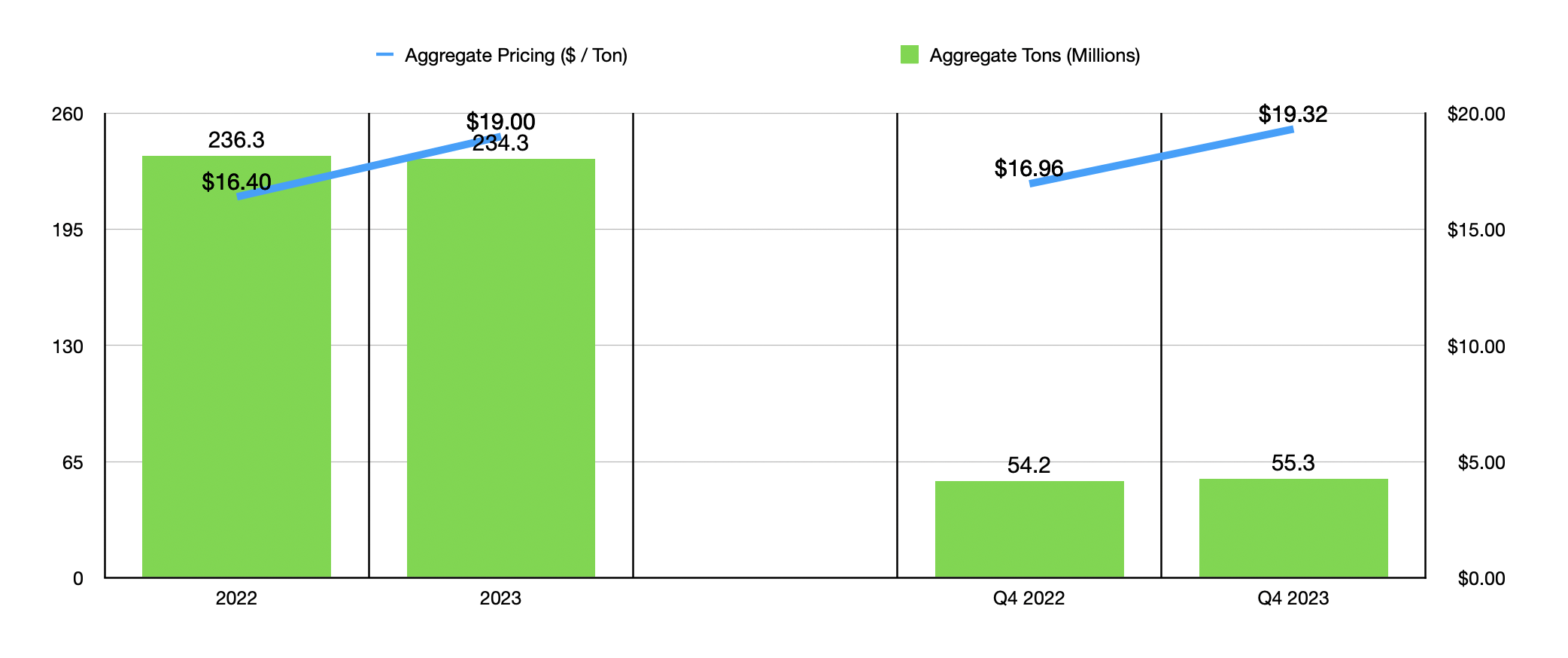

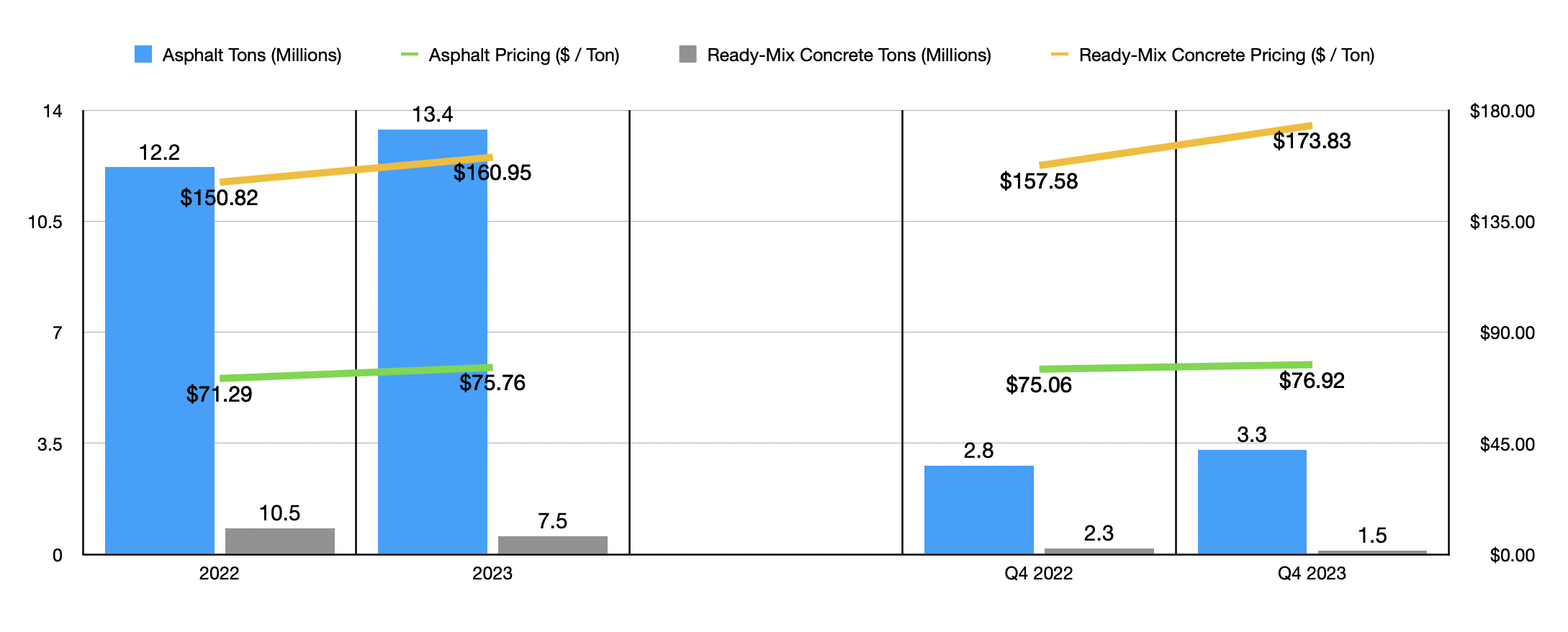

This increase in revenue was driven by a couple of different factors. For starters, the company saw the average selling price of its aggregates rise from $16.40 per ton to $19.00 per ton. Unfortunately, the number of tons sold slightly offset this, dropping from 236.3 million to 234.3 million. The company also went from selling 12.2 million tons of asphalt at $71.29 per ton to 13.4 million tons of asphalt at $75.76 per ton. And although the business went from selling 10.5 million tons of ready-mix concrete to 7.5 million tons last year, the average selling price per ton for it managed to grow from $150.82 to $160.95.

Author - SEC EDGAR Data

Higher pricing and, at least when it comes to asphalt, higher volumes, helped to push profit margins higher. In fact, net income nearly doubled, soaring from $575.6 million to $933.2 million. Other profitability metrics fared well too. Operating cash flow, as an example, grew from $1.15 billion to $1.54 billion. Though if we adjust for changes in working capital, the increase was more modest from $1.37 billion to $1.57 billion. Lastly, EBITDA for the company grew from $1.63 billion to $2.01 billion.

Author - SEC EDGAR Data

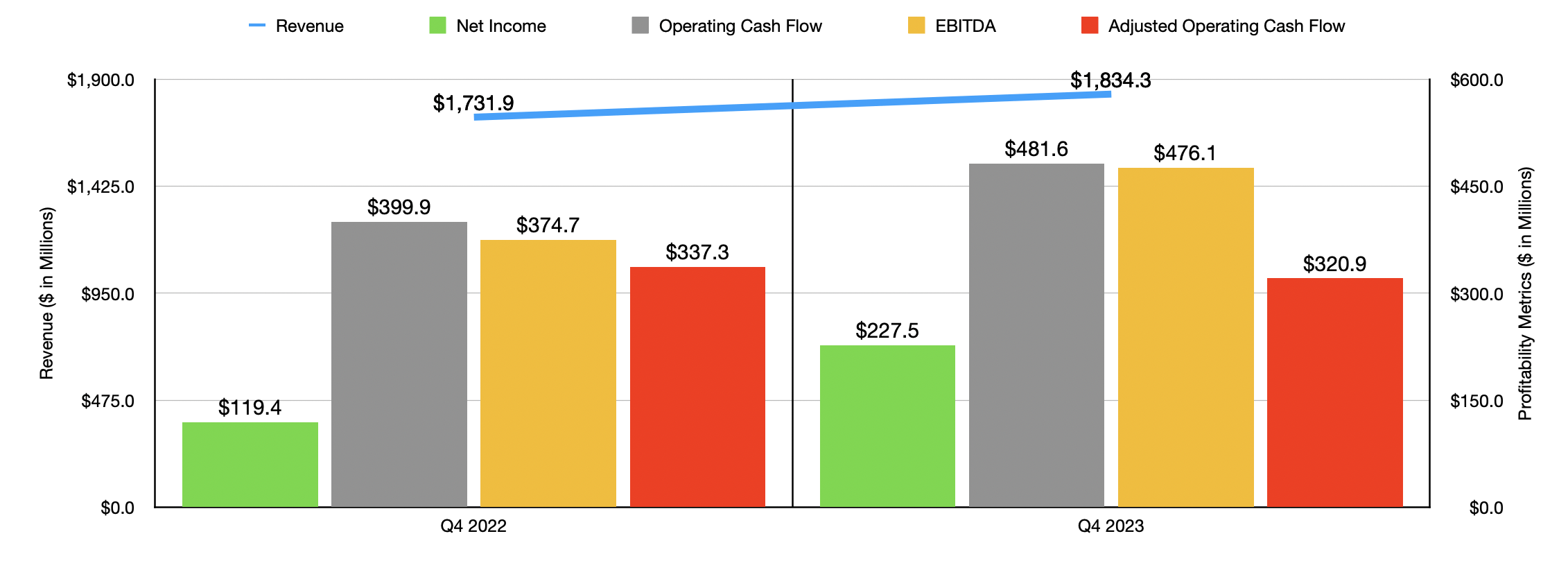

Even when you look at the most recent quarter for which data is available, the final quarter of 2023 relative to the same time one year earlier, you see that strength at the company remained intact. In fact, if anything, there were signs of progress when it came to some of the weakness that the business experienced earlier in the year. Revenue managed to spike from $1.73 billion to $1.83 billion. That's an increase of 5.9%. Even as the average selling price for asphalt expanded from $16.96 per ton to $19.32, the tons sold during that time grew from 54.2 million to 55.3 million. Asphalt tonnage went from 2.8 million to 3.3 million, with pricing inching up from $75.06 per ton to $76.92 per ton. And while ready mix concrete sales fell from 2.3 million tons to 1.5 million, average selling prices grew from $157.58 to $173.83.

Author - SEC EDGAR Data

All things considered, the picture for Vulcan Materials has been quite impressive. This year, management expects overall financial performance to improve further. While management is forecasting shipments remaining flat at best and dropping by 4% at worst, the expectation for net profits is between $1.07 billion and $1.19 billion. EBITDA has been forecasted to be between $2.15 billion and $2.30 billion, which implies adjusted operating cash flow, at the midpoint, of $1.74 billion. All of these numbers are higher than what the company achieved in 2023. More likely than not, they will end up being more or less right about this.

Vulcan Materials

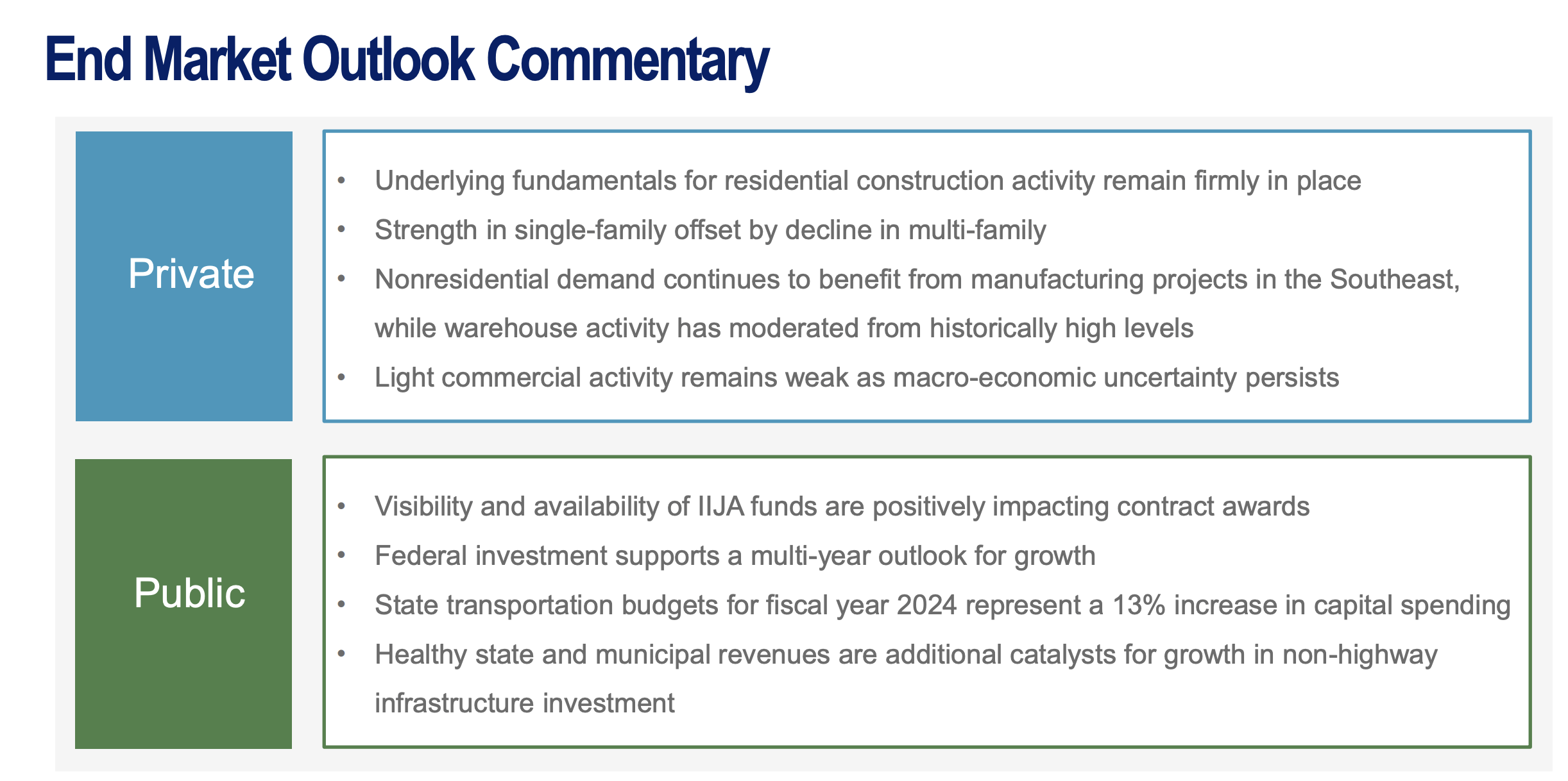

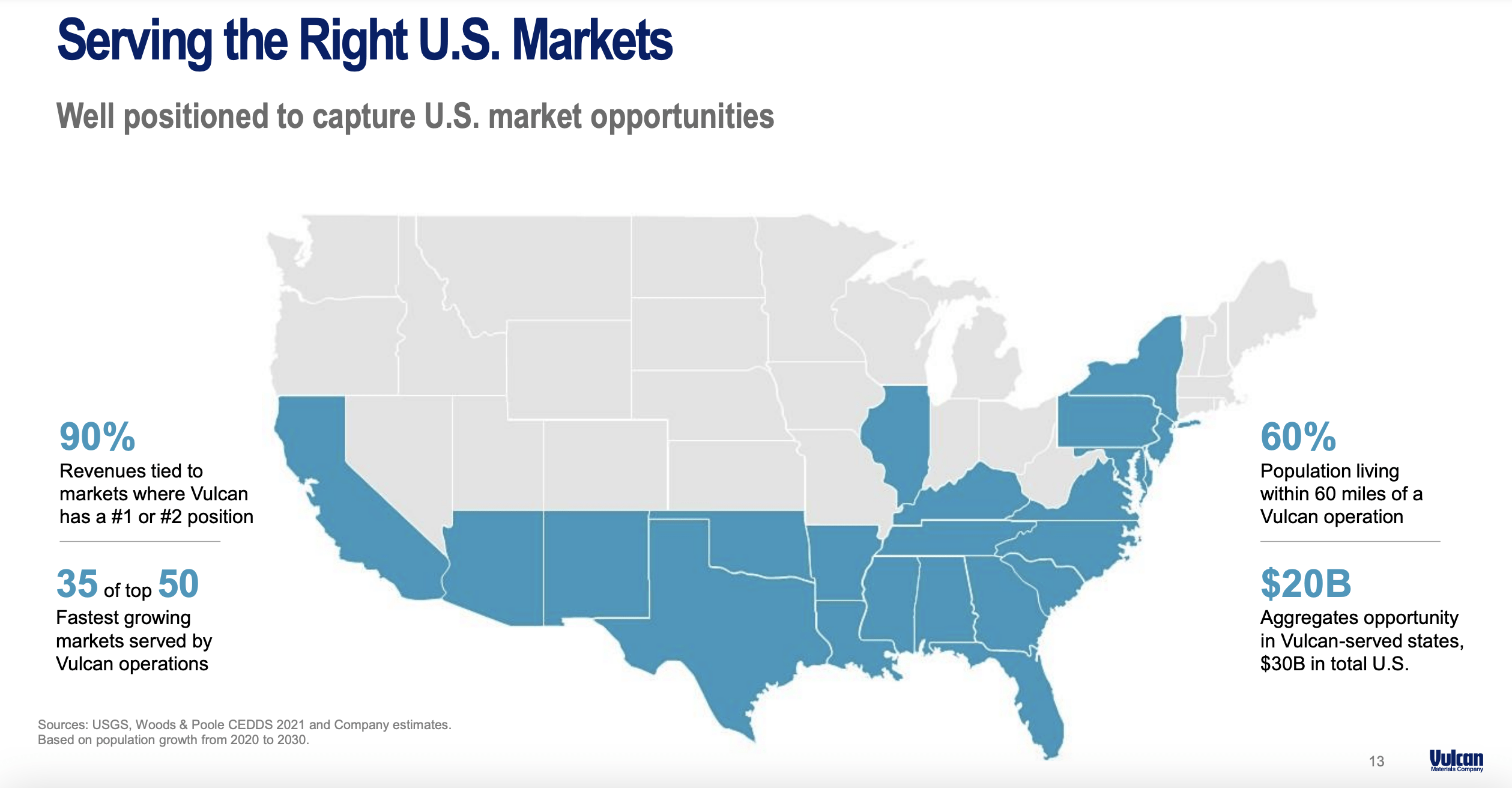

I say this because of their commentary regarding end market outlook. On the public side of things, management said that overall public spending on construction is likely to grow. Federal investment suggests multiple years of growth moving forward, while state transportation budgets for 2024 imply a 13% increase in spending over what was seen last year. But on the private side, management state of that while fundamentals for residential construction activity "remain firmly in place," there will be some weakness in multifamily demand. Nonresidential demand is expected to grow, largely in the southeast where, as the image below illustrates, Vulcan Materials has a sizable presence.

Vulcan Materials

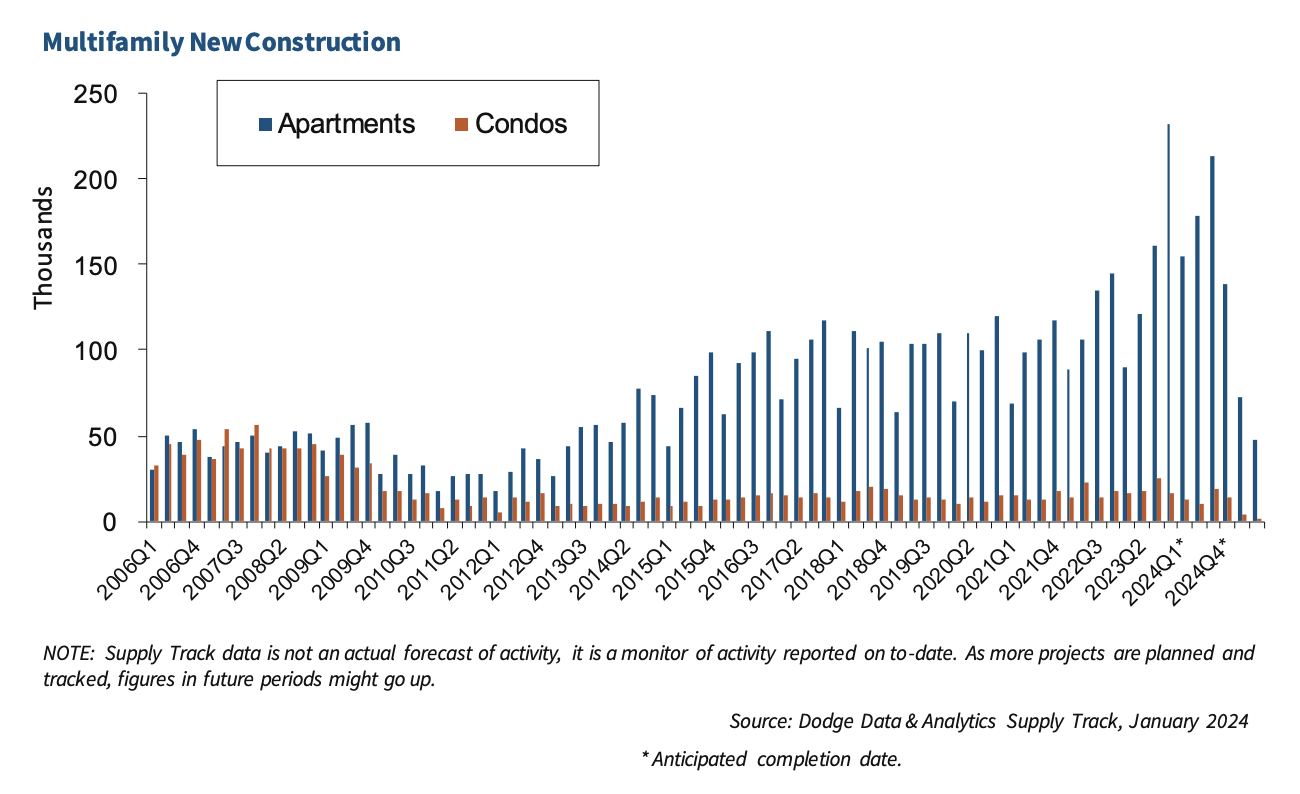

On the residential side of the equation, particularly when it comes to multifamily properties, the company is expecting some weakness. This is interesting because, after seeing 500,000 apartment units built nationwide in 2023, some data discussed by Fannie Mae sees 736,000 multifamily rental units being completed this year. Having said that, even that organization states that about 84% of respondents surveyed as part of a construction survey dedicated to multifamily housing reported construction delays because of permitting requirements or getting projects started. 79% of those said that delays were caused by construction financing concerns, with 83% stating that it was because of broader economic uncertainty.

Fannie Mae

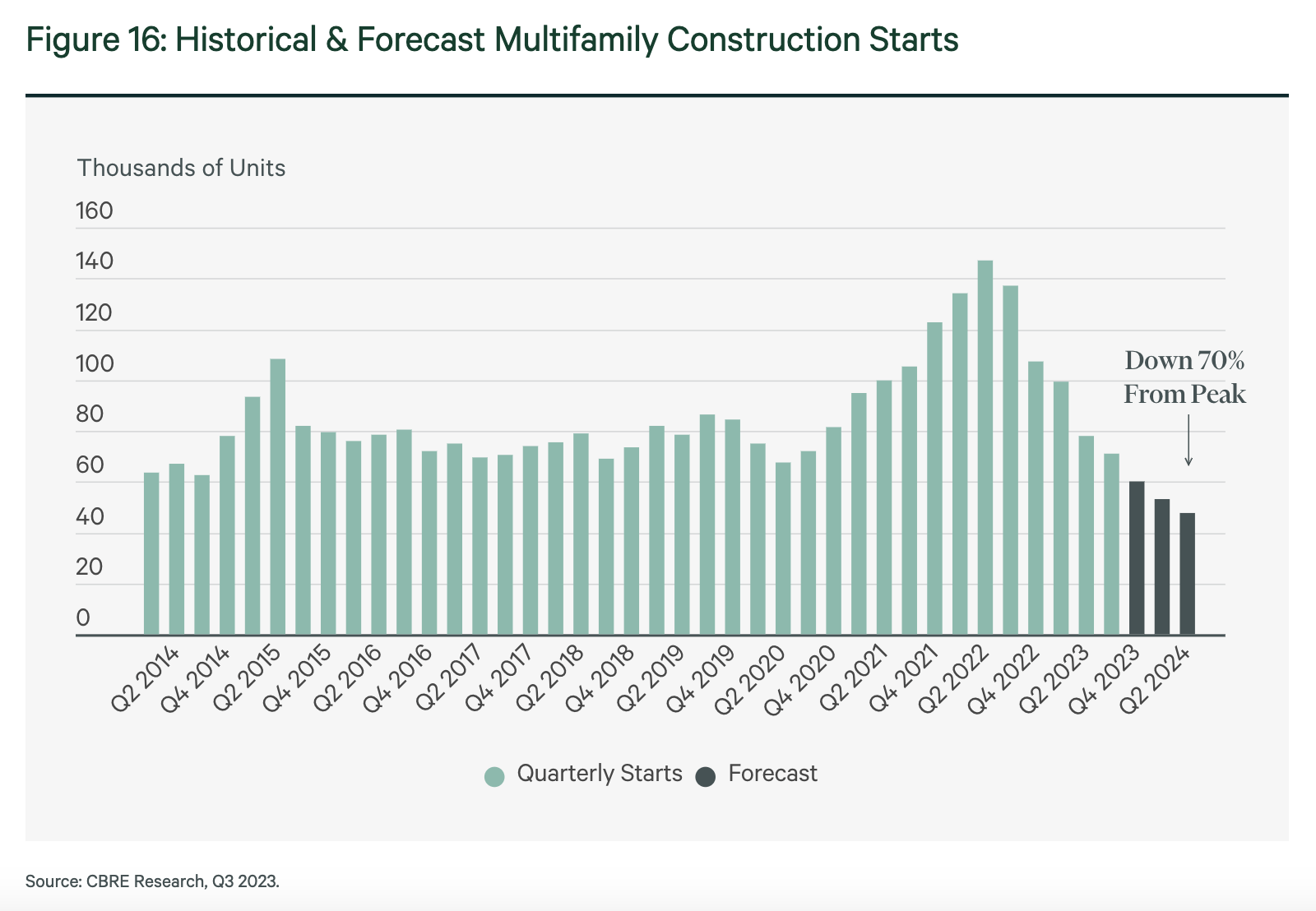

They don't give a firm estimate as to what they think the number of units built will ultimately be. But they did say that these issues, combined with labor shortages, rising material costs, and more, will likely lead to far fewer completions than anticipated. And while multifamily completions could very well peak this year, with the CBRE even going so far as to say that there are 900,000 such units under construction nationwide, that organization forecasts construction starts in that space to be down 45% compared to 2023 and down 70% compared to their peak in 2022.

What this suggests is that there could be some near-term demand for aggregates. But as the year goes on, that weakness that management is forecasting will likely rear its ugly head. As for the single-family side of things, I also think that management is spot on in their assessment. This is something that I have written about previously here.

CBRE

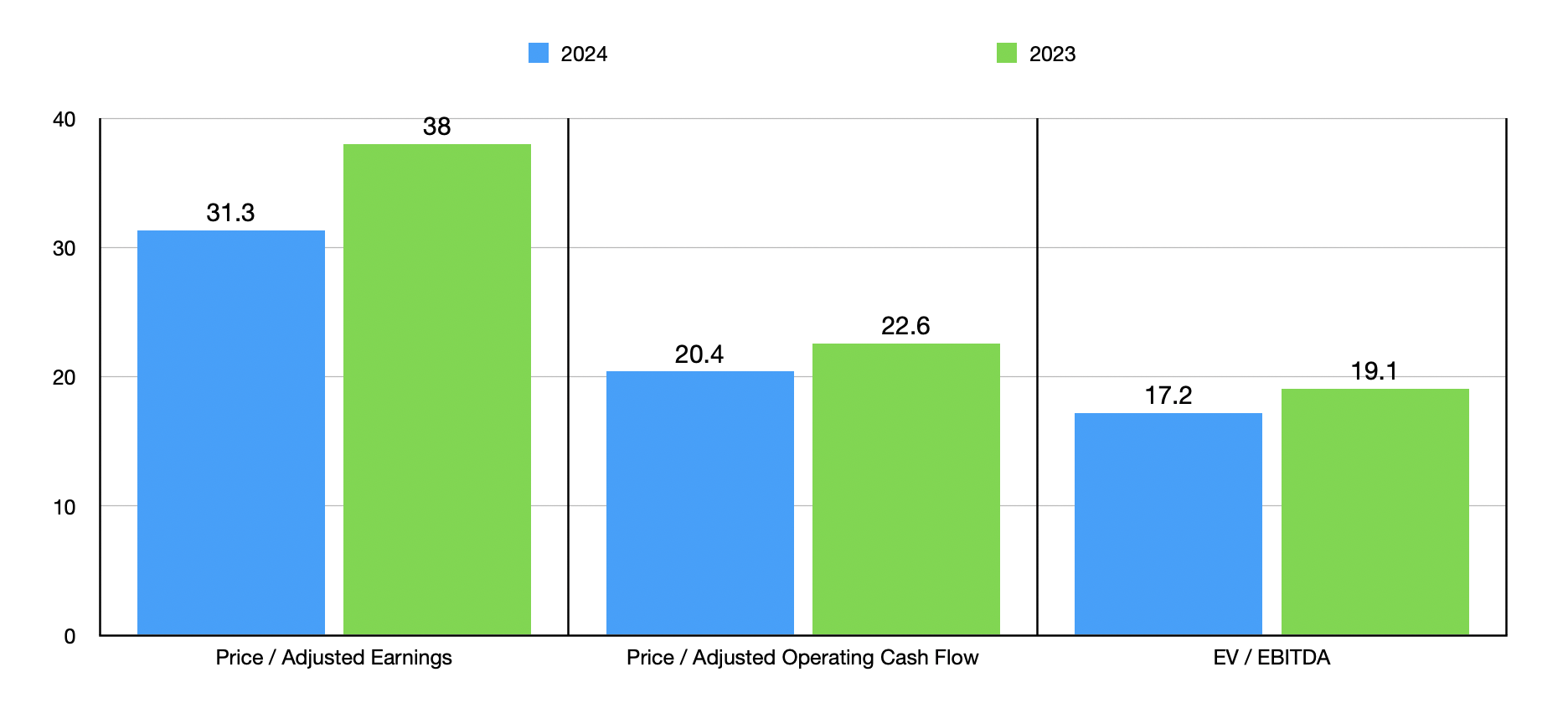

Regardless of the outcome, so long as the outcome is not worse than anticipated, my overall assessment of Vulcan Materials is unlikely to change. I say this because shares have gotten a bit pricey. In the first chart below, you can see how the stock is priced using data from 2023 and how it is priced using estimates for 2024. And in the table below that, you can see how shares are priced compared to five similar firms. On both a price to earnings basis and a price to operating cash flow basis, four of the five companies ended up being cheaper than it. And when it comes to the EV to EBITDA approach, our prospect was the most expensive of the group.

Author - SEC EDGAR Data

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Vulcan Materials Company | 38.0 | 22.6 | 19.1 |

| Martin Marietta Materials (MLM) | 32.0 | 24.5 | 18.6 |

| Summit Materials (SUM) | 18.1 | 11.8 | 13.0 |

| James Hardie Industries (JHX) | 33.0 | 19.1 | 18.1 |

| Compass Minerals (CMP) | 70.3 | 21.6 | 17.1 |

| Eagle Materials (EXP) | 18.0 | 16.1 | 11.9 |

From what I can tell, Vulcan Materials has been and will likely continue to be a high-quality player in the aggregates space. Long term, I have no doubt in the company's ability to thrive.

But this doesn't mean that it makes for an appealing prospect at this time. Lower volumes are slightly concerning, though it's nice to see revenue, profits, and cash flows all rise year over year.

Having said that, Vulcan Materials Company shares look pricey on an absolute basis, and they are quite expensive compared to similar firms. Given these factors, and the run-up that shares have experienced since I last wrote about the firm, I believe that a downgrade to a "hold" only make sense at this time.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.