Tanja Ivanova/Moment via Getty Images

Tanja Ivanova/Moment via Getty Images

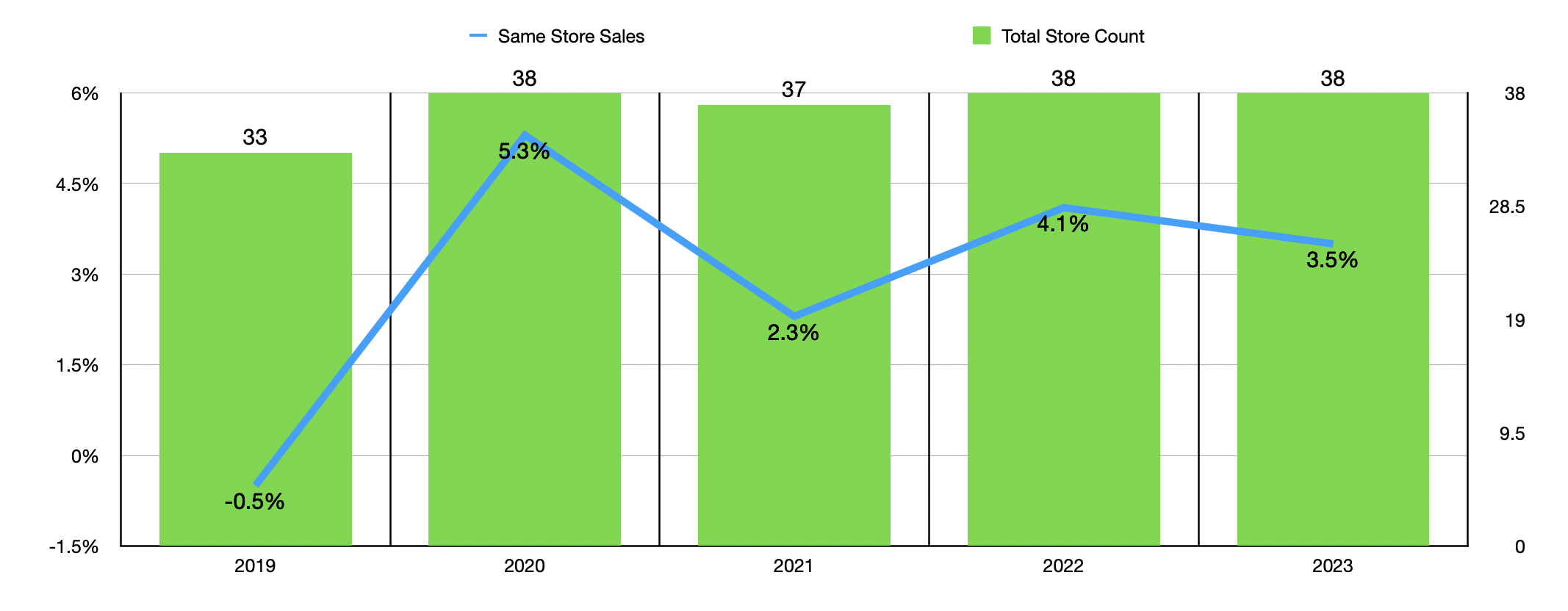

As a rule of thumb, I tend to stay away from companies in the retail space. However, every so often, I will come across a firm that makes sense making an exception for. One business in retail that focuses on groceries that I have long been a fan of is Village Super Market (NASDAQ:VLGEA). With only 37 locations in operation and a market capitalization of $370.3 million as of this writing, Village Super Market is a pretty small player in the grand scheme of things. The firm has not really achieved any physical location growth in recent years, but through a series of changes made to some of its locations, management has done well to consistently grow same store sales.

The last article that I wrote about the enterprise was published in July of 2023. In that article, I stated boldly that the market was misunderstanding Village Super Market. For some time leading up to that point, the stock had underperformed the broader market even though revenue, cash flows, and profits, were all rising nicely on a year over year basis. Add on top of this just how cheap the stock was, and I had no problem reiterating it as a ‘buy’ candidate that I believed would outperform the broader market for the foreseeable future. Since then, performance has picked up some. Shares have seen upside of 12.1% at a time when the S&P 500 is up a more modest 10.9%. But even in spite of this, the company looks woefully undervalued and, I would argue, it could very well be a fantastic buyout candidate.

Author - SEC EDGAR Data

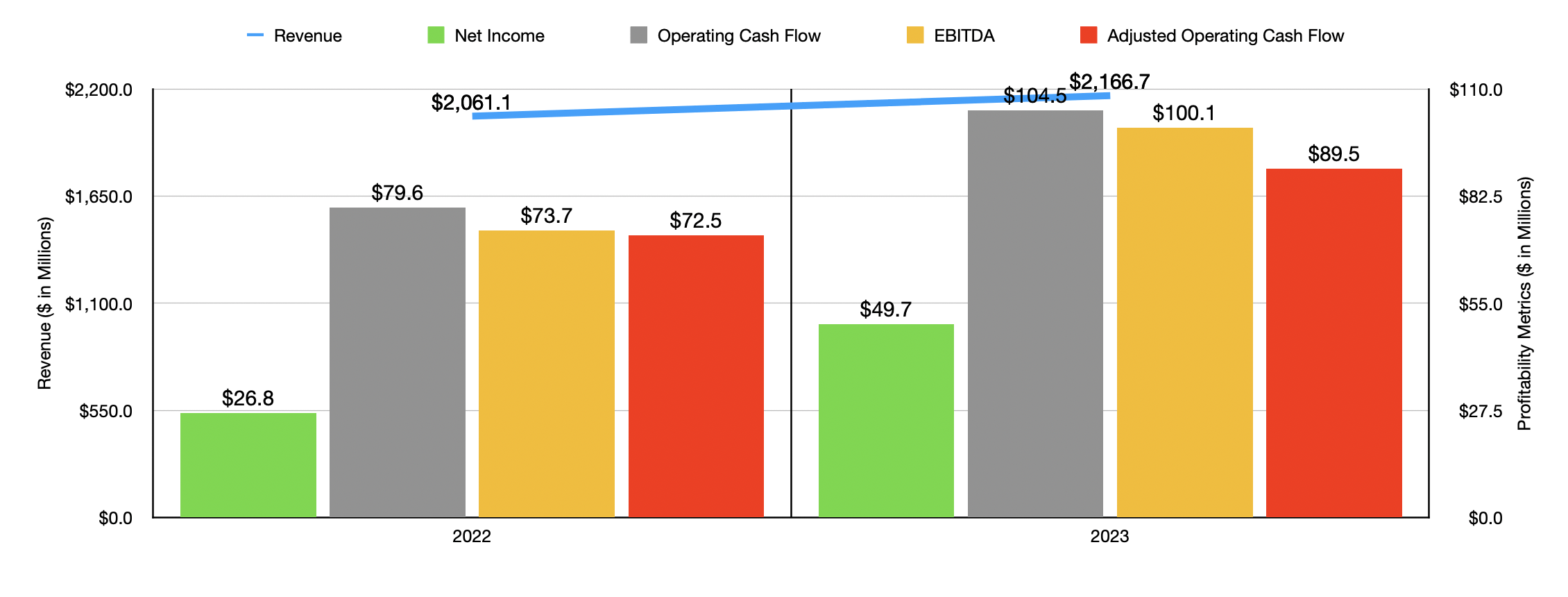

Since I wrote about Village Super Market in July of last year, we have had data come out covering not only the rest of the 2023 fiscal year, but also covering the first quarter of the 2024 fiscal year. To start with, we should touch on 2023. During that year, revenue for the business came in at $2.17 billion. That's an increase of 5.1% compared to the $2.06 billion generated one year earlier. Even though the number of locations remained unchanged during that window of time at 38, same store sales jumped by 3.5%. Management attributed this to a combination of factors, including to the remodel and conversion of one of its locations in New York. Retail price inflation played a role during this window of time as well. As the chart below illustrates, growth in same store sales has been part of what makes this a special business. The last time that it experienced a decline in same store sales was back in 2019. But in the years since then, it has seen an increase ranging between 2.3% and 5.3%.

Author - SEC EDGAR Data

With the increase in revenue also came a nice rise in profits. Net income almost doubled from $26.8 million to $49.7 million. The biggest improvement here came from a slight decline in operating and administrative costs from 24.63% of revenue to 23.86%. Lower labor costs and decreased supply spending were responsible for this improvement. Other profitability metrics also grew during this window of time. Operating cash flow went from $79.6 million to $104.5 million. If we adjust for changes in working capital, we would get a rise from $72.5 million to $89.5 million. And lastly, EBITDA for the company went from $73.7 million to $100.1 million.

Author - SEC EDGAR Data

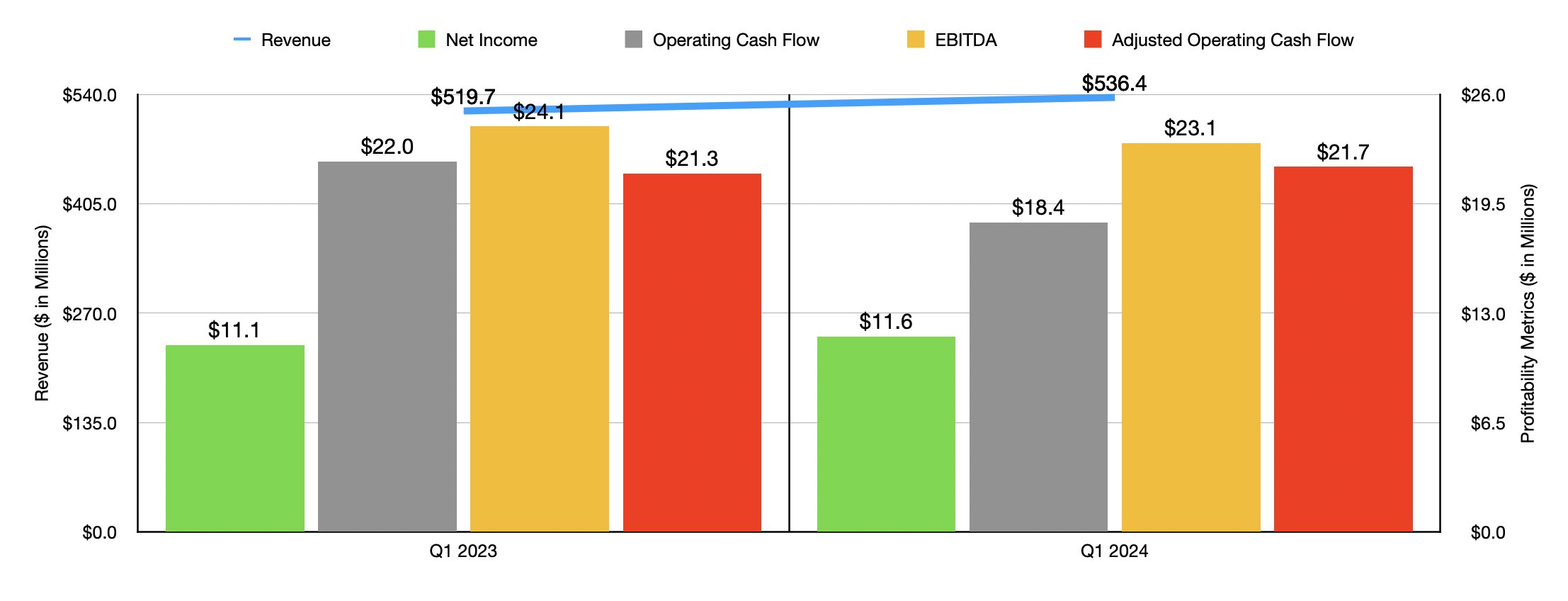

For those wondering if the small margin improvement that had a big bottom line impact was a one time event, the answer is likely no. I say this because strength on the bottom line continued into the 2024 fiscal year. During the first quarter, revenue came in at $536.4 million. That's 3.2% above the $519.7 million generated one year earlier. The largest chunk of that increase came from a 2% rise in same store sales. And it was in spite of the fact that the company closed one of its locations late last year. Net profits jumped from $11.1 million to $11.6 million. It is true that operating cash flow dipped from $22 million to $18.4 million. But once we adjust for changes in working capital, we get a modest increase from $21.3 million to $21.7 million. Although it is worth mentioning that EBITDA pulled back slightly from $24.1 million to $23.1 million.

Author - SEC EDGAR Data

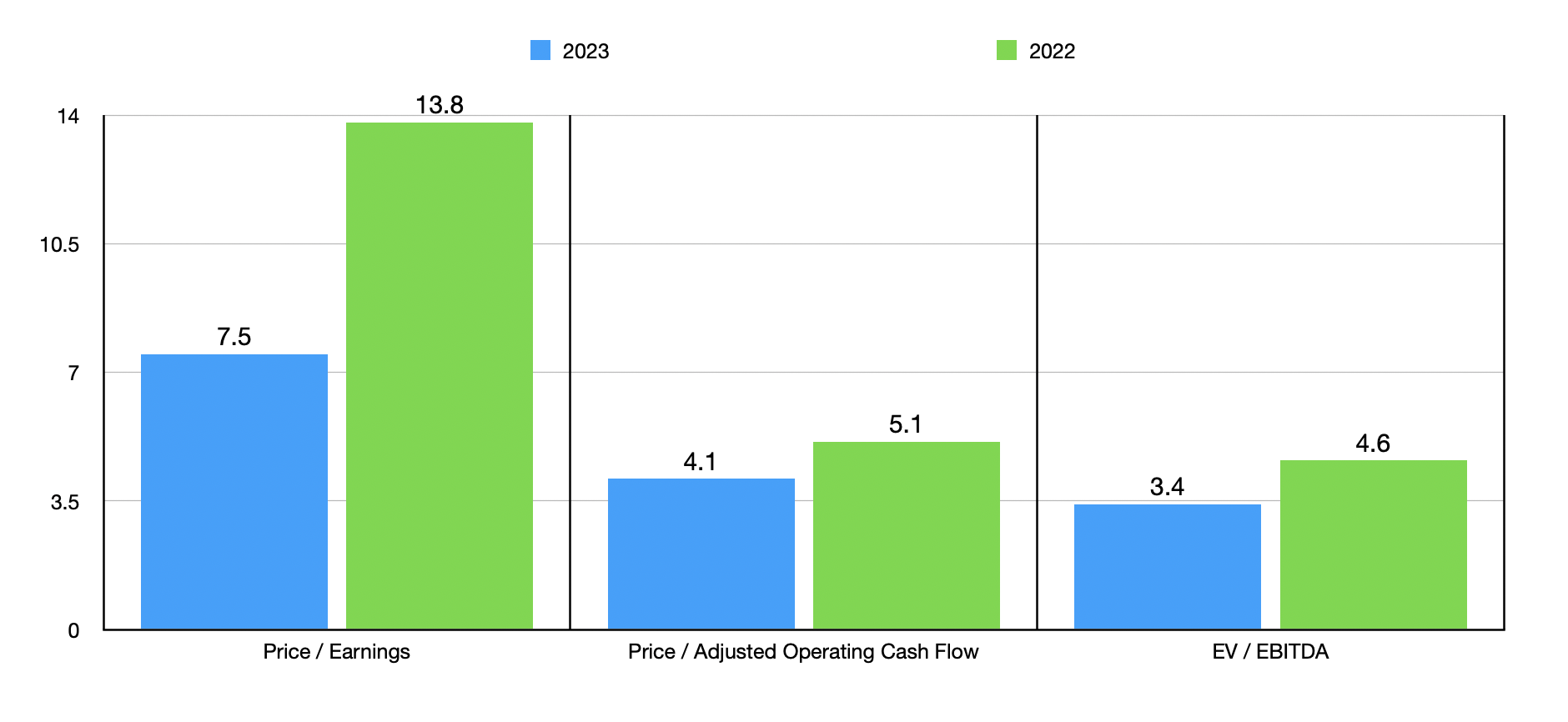

When it comes to valuing the company, the process is fairly straightforward. In the chart above, you can see how shares are priced using a price to earnings approach, a price to operating cash flow approach, and an EV to EBITDA approach. Using the 2023 results, the stock looks even cheaper than if we were to use the data from 2022. However, I would argue that shares look attractively priced in either case. In the table below, I then compared the company to five similar firms. What I found was that it ended up being the cheapest across the board.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Village Super Market | 7.5 | 4.1 | 3.4 |

| Natural Grocers by Vitamin Cottage (NGVC) | 14.6 | 5.3 | 5.3 |

| The Kroger Co (KR) | 17.7 | 5.5 | 6.0 |

| Sprouts Farmers Market (SFM) | 20.8 | 11.2 | 8.2 |

| Casey's General Stores (CASY) | 22.1 | 12.2 | 11.3 |

| Grocery Outlet Holding Corp (GO) | 31.0 | 7.9 | 12.1 |

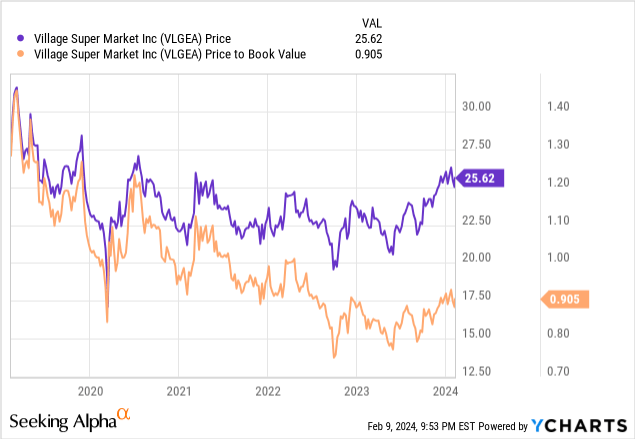

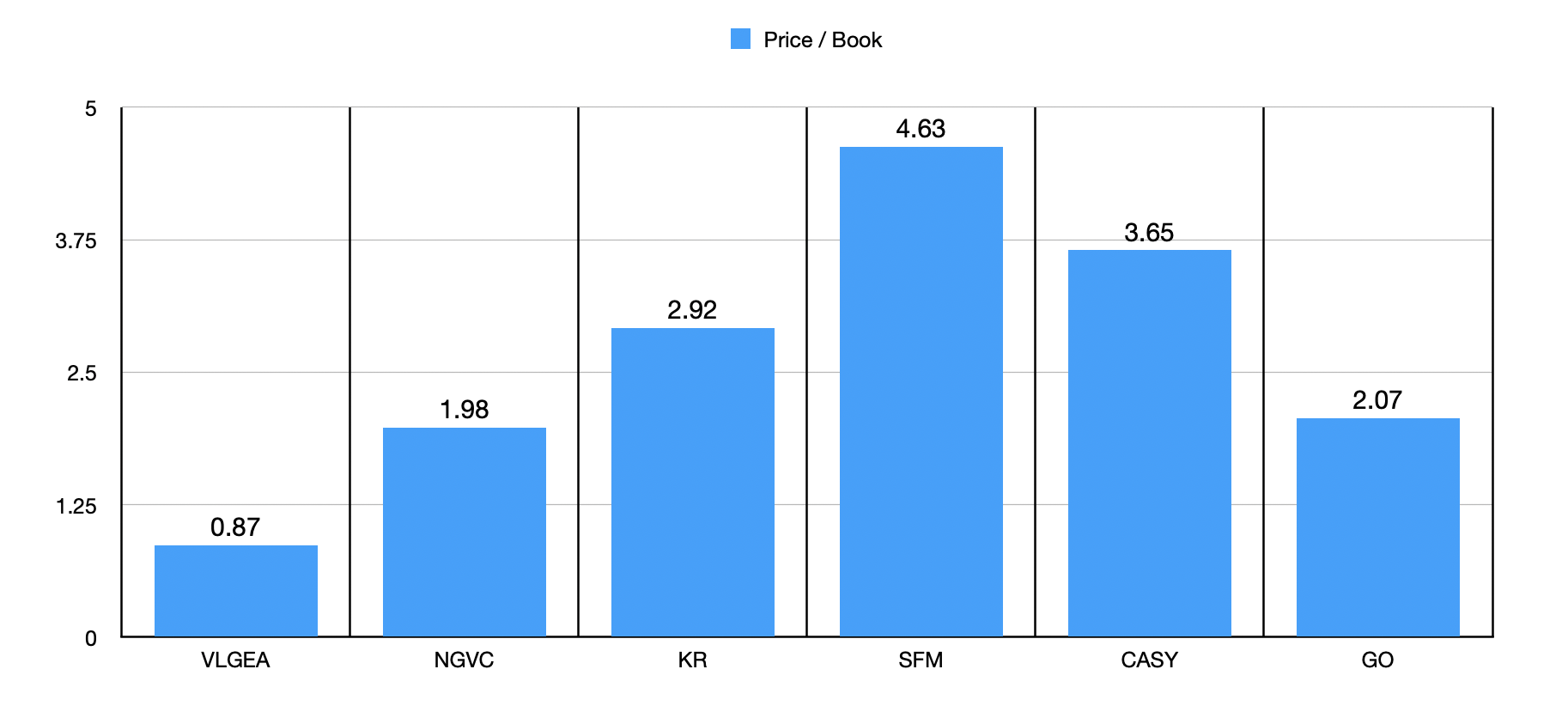

There are, of course, other ways to look at the enterprise. Another example would be through the price to book ratio. In the chart below, you can see how the price to book multiple for Village Super Market has consistently decreased over at least the past five years. The company is now trading at a real discount to its net assets. Sometimes this happens when a firm has a lot of leverage. However, cash exceeds debt to the tune of $33.5 million. So if anything, you'd expect the business to be trading at a premium to its book value. In the second chart below, you can also see how the price to book multiple stacks up against the same five firms I initially compared Village Super Market to. On a price to book basis, it was, once again, cheaper. In fact, I would take it a step further and say that it was substantially cheaper.

Author - SEC EDGAR Data Author - SEC EDGAR Data

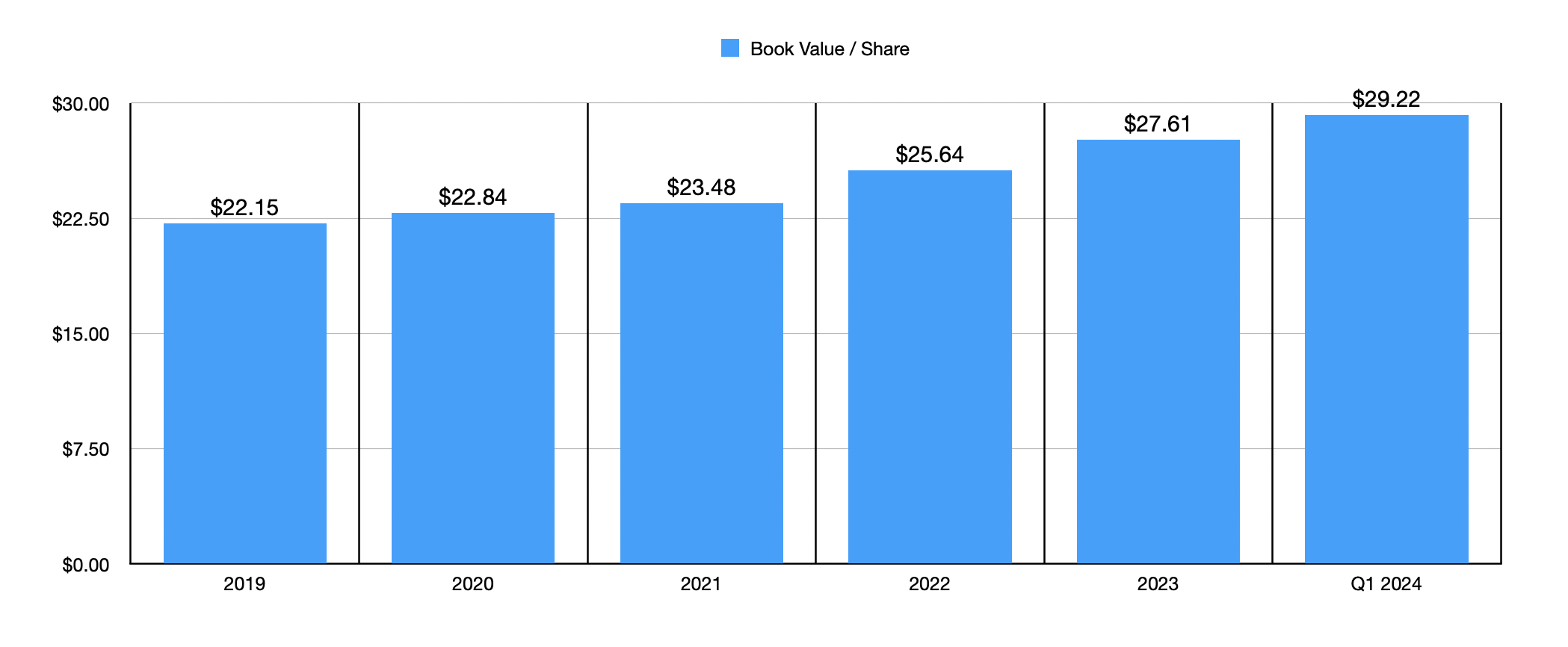

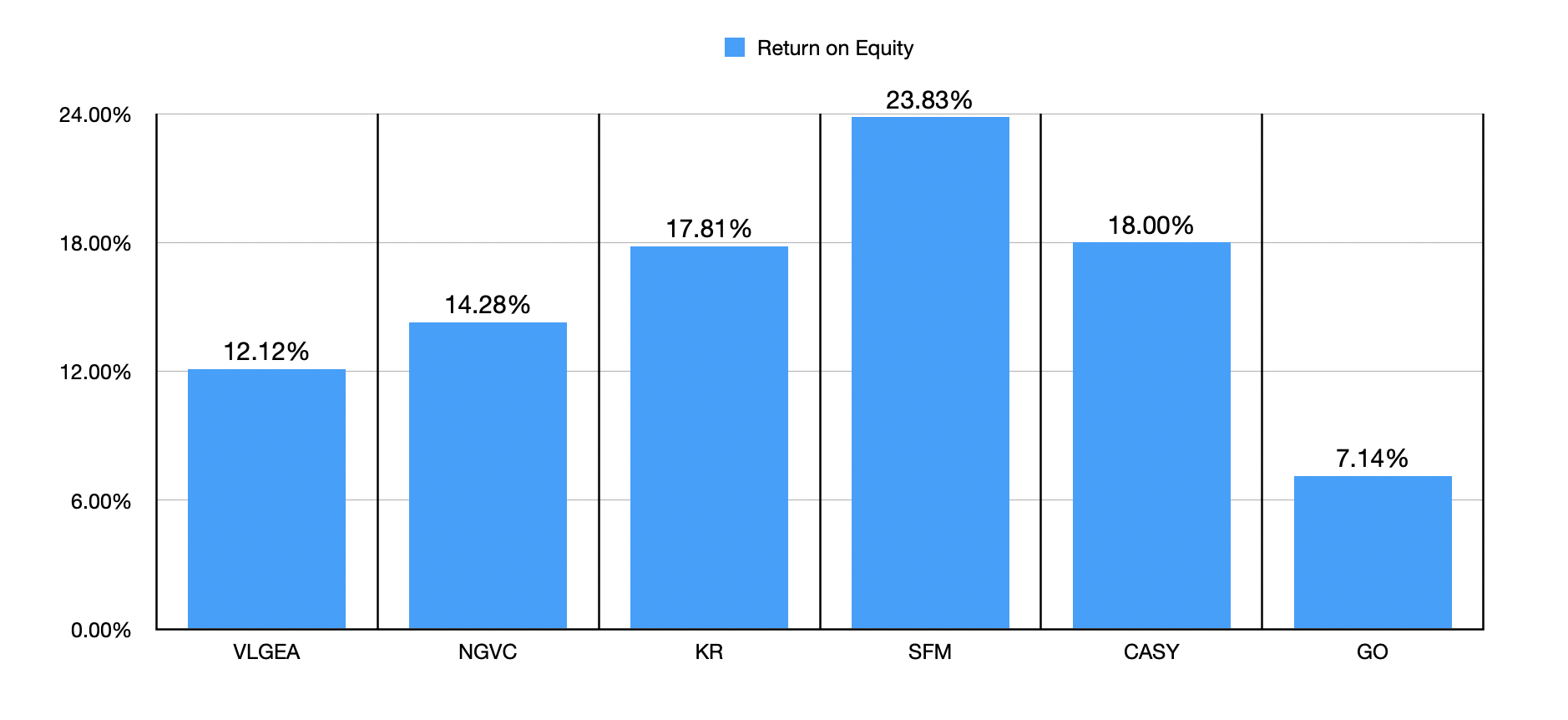

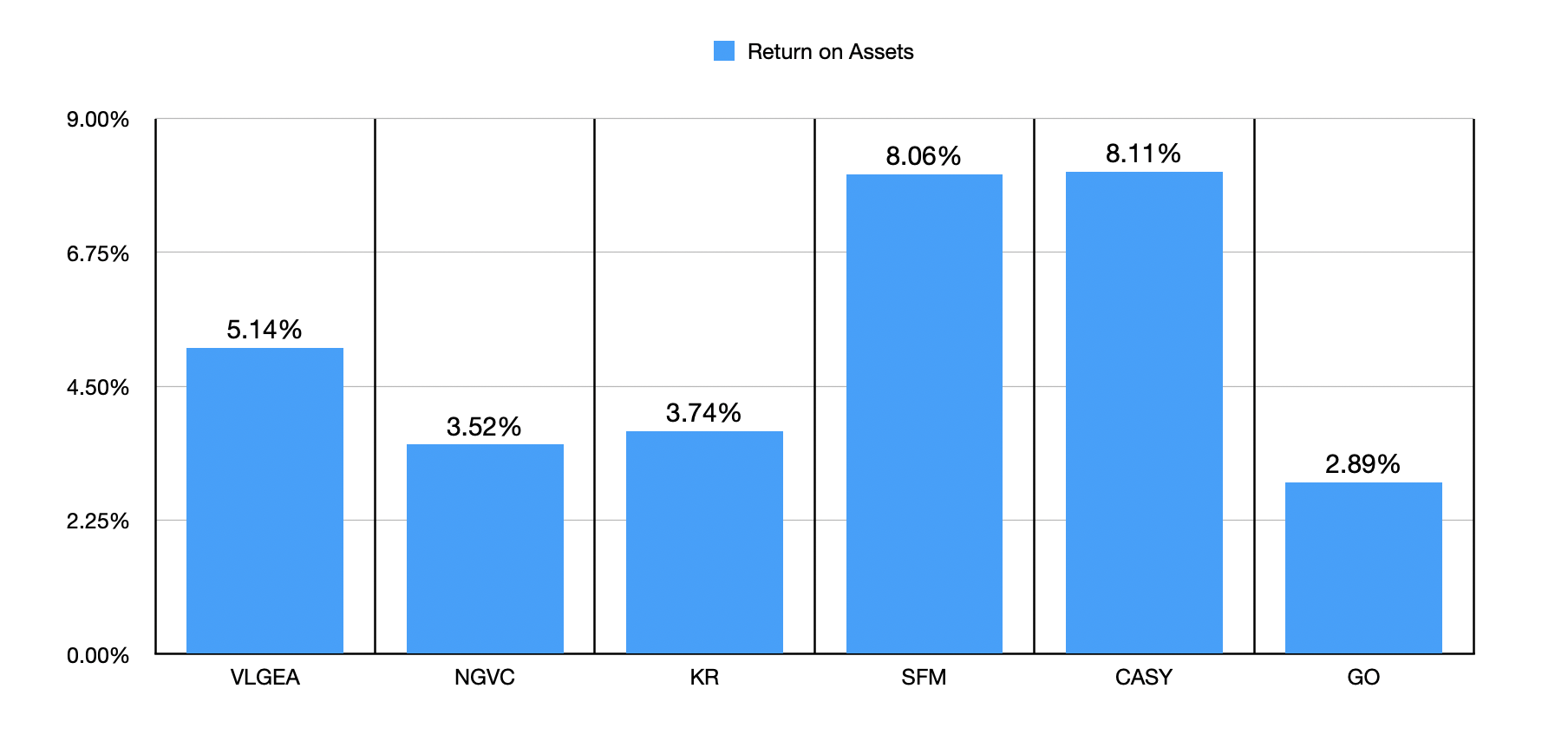

It would be one thing if Village Super Market had a history of a decline in its book value. But that is not the case. In each year between 2019 and 2023, the company has seen its book value per share increase, climbing from $22.15 to $27.61. By the first quarter of 2024, book value per share had risen further to $29.22. In the table below, I then decided to look at the picture through the lens of the return on equity for our prospect, as well as for the other five firms I compared it to. In this case, Village Super Market does fall short. Four of the five companies that I compared it to have a return on equity that is higher than what it has. But at 12.1%, it's not like Village Super Market is struggling. In the subsequent table below, I did the same thing with the return on assets. In this case, with a reading of 5.1% for 2023, Village Super Market ended up being higher than three of the five businesses.

Author - SEC EDGAR Data Author - SEC EDGAR Data

Looking at all the data that's available to me, I remain perplexed as to why the market continues to undervalue Village Super Market. Relative to book value, the picture has only gotten worse over the past few years. I know that in recent months, shares have outperformed the broader market. But that has not been enough to bring the stock even close to being fairly valued. Yes, from a return on equity perspective, there definitely are some better plays out there. But using almost any other metric that I could fathom, Village Super Market either holds its own or is superior to the competition. Given these factors, I have no problem keeping the business rated a ‘buy’ for now.