solarseven

solarseven

As I argued a couple of times in the past few days, the US economy might not be crumbling necessarily, but it is also not quite firing on all cylinders:

Manufacturing new orders are still soft. Consumers remain skeptical of business conditions. The yield curve is still sharply inverted between the 3-month and 10-year maturities (5.5% vs. 4.3%, respectively). Average weekly manufacturing hours, at 39.9, are still near the lowest since 2010, excluding the early COVID-19 period. Plateauing inflation numbers [could] delay the Federal Reserve's move to lower interest rates in 2024.

To the above, I would add household debt that is starting to look a bit concerning. Debt service costs are increasing relative to income. In addition, credit card and auto loan delinquency has been rising.

Yet, the S&P 500 (SPY) keeps making all-time highs. At the same time, the VIX, or volatility index, dipped below 13 during the Thursday trading session and as of the writing of this paragraph, which has happened only once every five to six days since 1990, on average.

Given the current setup, I believe that going long volatility makes sense as a hedge to a potential decline in the S&P 500. One can do so by allocating small amounts to an instrument like the ProShares VIX Short-Term Futures ETF (BATS:VIXY).

VIXY is an ETF that provides its holders with exposure to volatility, allowing them to benefit from a market that turns bearish on the S&P 500. The fund does so by going long short-term VIX futures contracts. Today, the $157 million ETF parks all its assets in cash while going long the April (primarily) and May 2024 VIX futures at a notional exposure of $157 million.

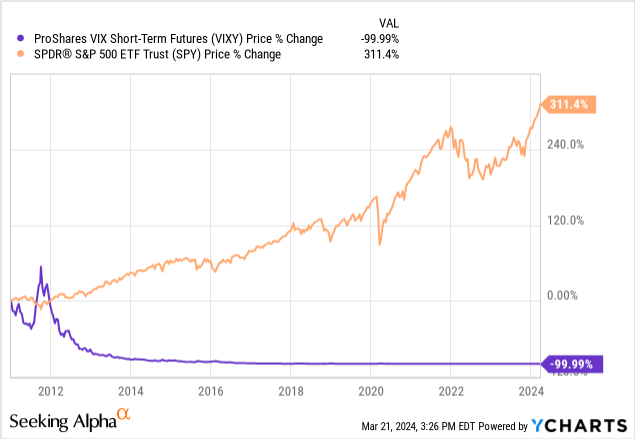

One of VIXY's main features is its track record of losing significant value over time, as the chart below displays. This is the case because of the naturally upsloping shape of the VIX futures curve (i.e., it is generally in contango, rarely in backwardation). Since VIXY buys the fear index high and sells it low consistently, it bleeds value at a fast rate.

Therefore, it is evident from the historical record that holding VIXY for a long period as a speculative bet is probably not a great idea. In my view, owning VIXY makes the most sense if (1) held in small amounts, (2) coupled with the S&P 500 as a hedge, and (3) timed properly.

As discussed above, due to the shape of the VIX futures curve, it is nearly guaranteed that a long-term bet on VIXY will eventually turn sour. On the other hand, a well-timed bet on VIXY can produce gains (or at least protection against large losses, when coupled with an S&P 500 position) because the volatility index consistently reverts to the mean. That is: when the VIX is historically low, it is safe to assume that it will eventually rise. The opposite is also true.

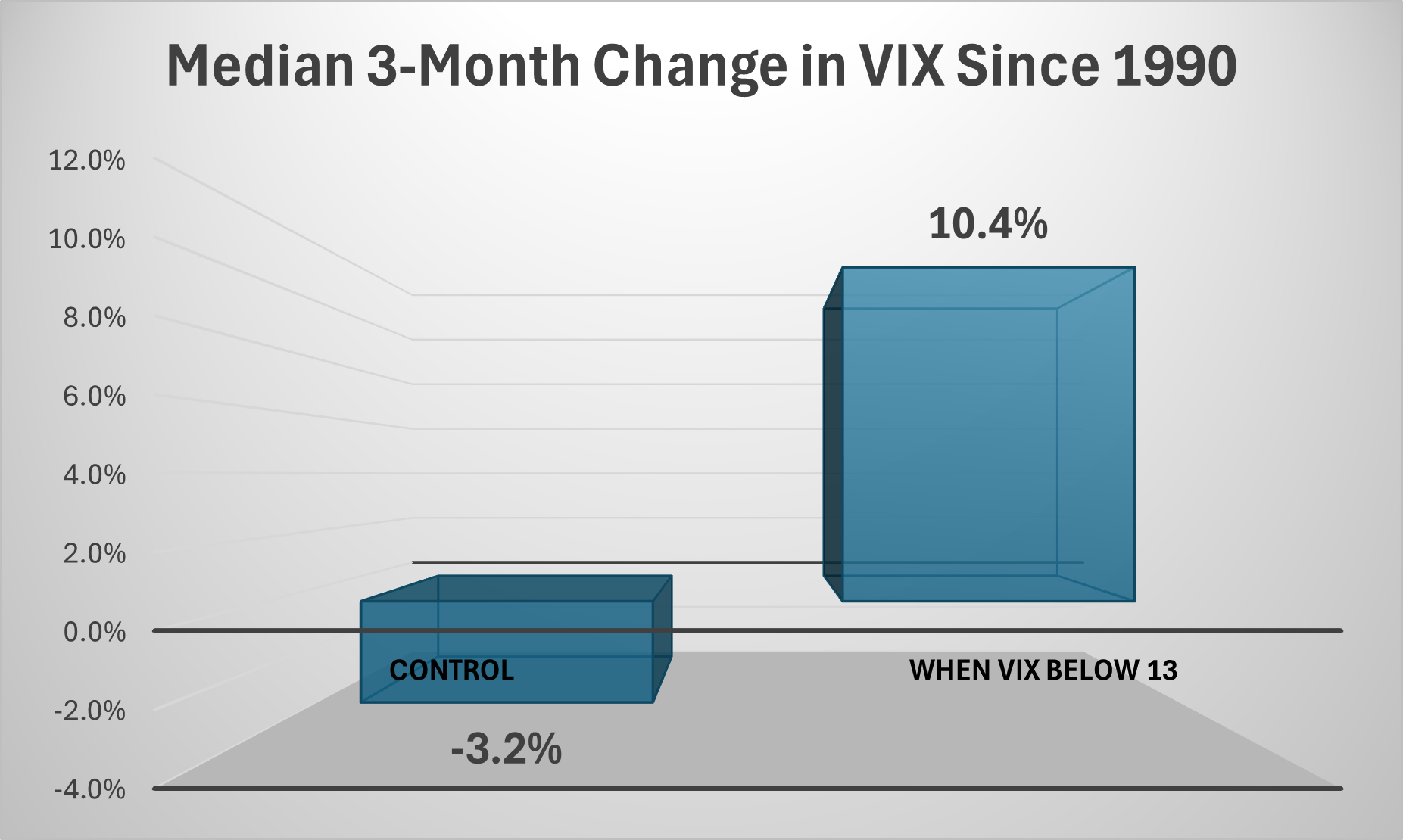

Today, the VIX breached the 13 level to the downside, reaching intraday lows of 12.6 - since 1990, the median has been 17.7. The chart below shows the inverse relationship between VIX levels and the change in the index three months later. The median three-month change in VIX on any given day since 1990 has been -3%. But when the VIX is below 13, as it is now, the median three-month (forward) change has been 10%. At the 75th percentile, the change has been a whopping 30%; and at the 25th percentile, a harmless -1%.

DM Martins Research, data from Yahoo Finance

So, should one buy the VIXY today as a speculative play, hoping that the VIX index rises over the next three months? Sure, this is one simple approach that might work for some - just don't forget that the negative roll yield would still be a headwind to gains. However, I prefer to combine VIXY and SPY at a ratio of 7% to 93%, respectively. Doing so blindly, even without caring about the right time to set up the hedged position, has historically produced better risk-adjusted returns than holding the S&P 500 alone.

Better yet, I think, is to set up the 7/93 position described above when the VIX is as cheap as it is now. Since the tendency is for the VIX index to rise from current levels over the next three months, VIXY will likely benefit in two ways: (1) from the VIX index climbing and (2) from the increase in the VIX possibly causing the futures curve to flatten, which tends to happen when the fear index moves up.