peakSTOCK/iStock via Getty Images

peakSTOCK/iStock via Getty Images

Vir Biotechnology (NASDAQ:VIR) is developing treatments for patients with Hepatitis B (HB), Hepatitis delta (HD), Human Immunodeficiency Virus (HIV), Influenza and COVID. I wrote about the name in November 2023, rating it a buy based on an expectation of positive results from the company's ongoing work in HB and HD patients. The company also looked very cheap, with an enterprise value of over -$400M.

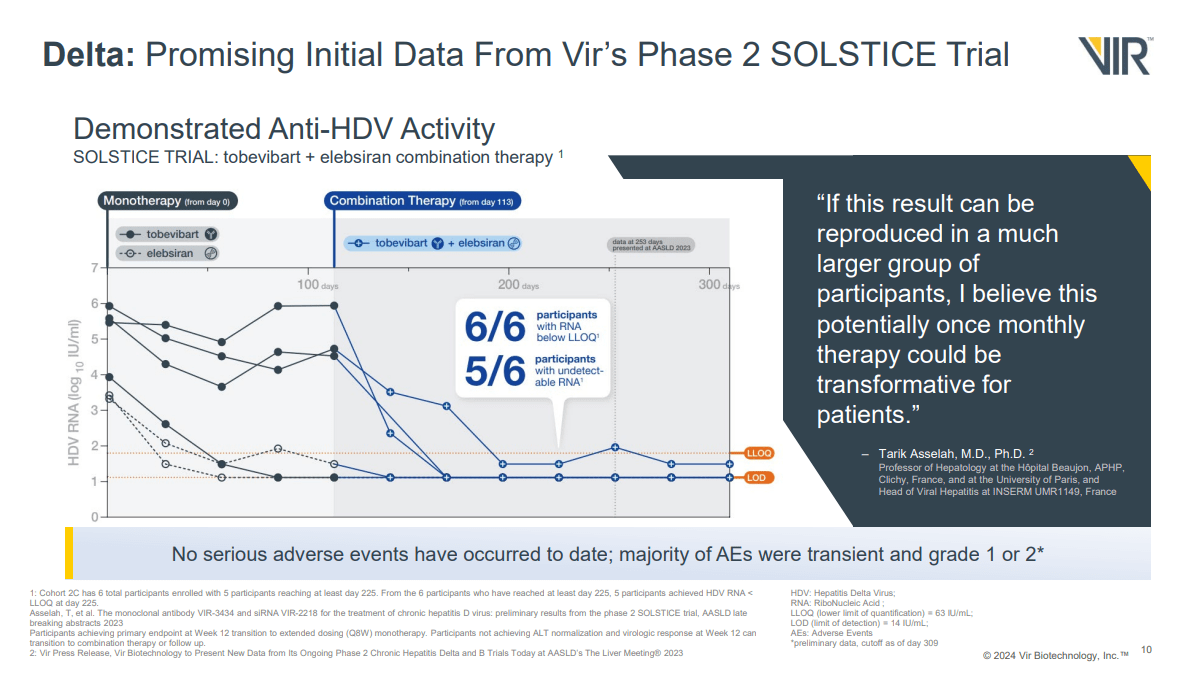

In November 2023, VIR reported the first data from its SOLSTICE trial of the siRNA elebsiran (VIR-2218) and the antibody tobevibart (VIR-3434) in patients with hepatitis delta virus (HDV). There were only data from five of six patients treated with the combination at the time of the release, but of those 5 patients, all had HDV RNA levels below the LLOQ (lower limit of quantitation). Four of five even had RNA levels below the LOD (limit of detection). Since that time, data from the sixth patient came in with that patient also achieving HDV RNA levels below the LLOQ.

Figure 1: Slide showing change in HDV RNA levels in HD patients treat with tobevibart and elebsiran. (Corporate Overview, February 2024.)

The company was planning to report additional data from the SOLSTICE trial in Q2'24 and has confirmed that timeline with recent Q4'23 earnings.

Phase 2 SOLSTICE trial on track to complete enrollment ahead of schedule with initial data expected in the second quarter; greater than 90% of participants dosed

Statement from VIR's Q4'23 earnings press release, February 22, 2024.

I see the company as very unlikely to miss the Q2'24 timing for a readout from that study then, which locks in a catalyst for next quarter. A faster than expected enrollment could be due to enthusiasm generated by the initial data of the combination therapy in six patients.

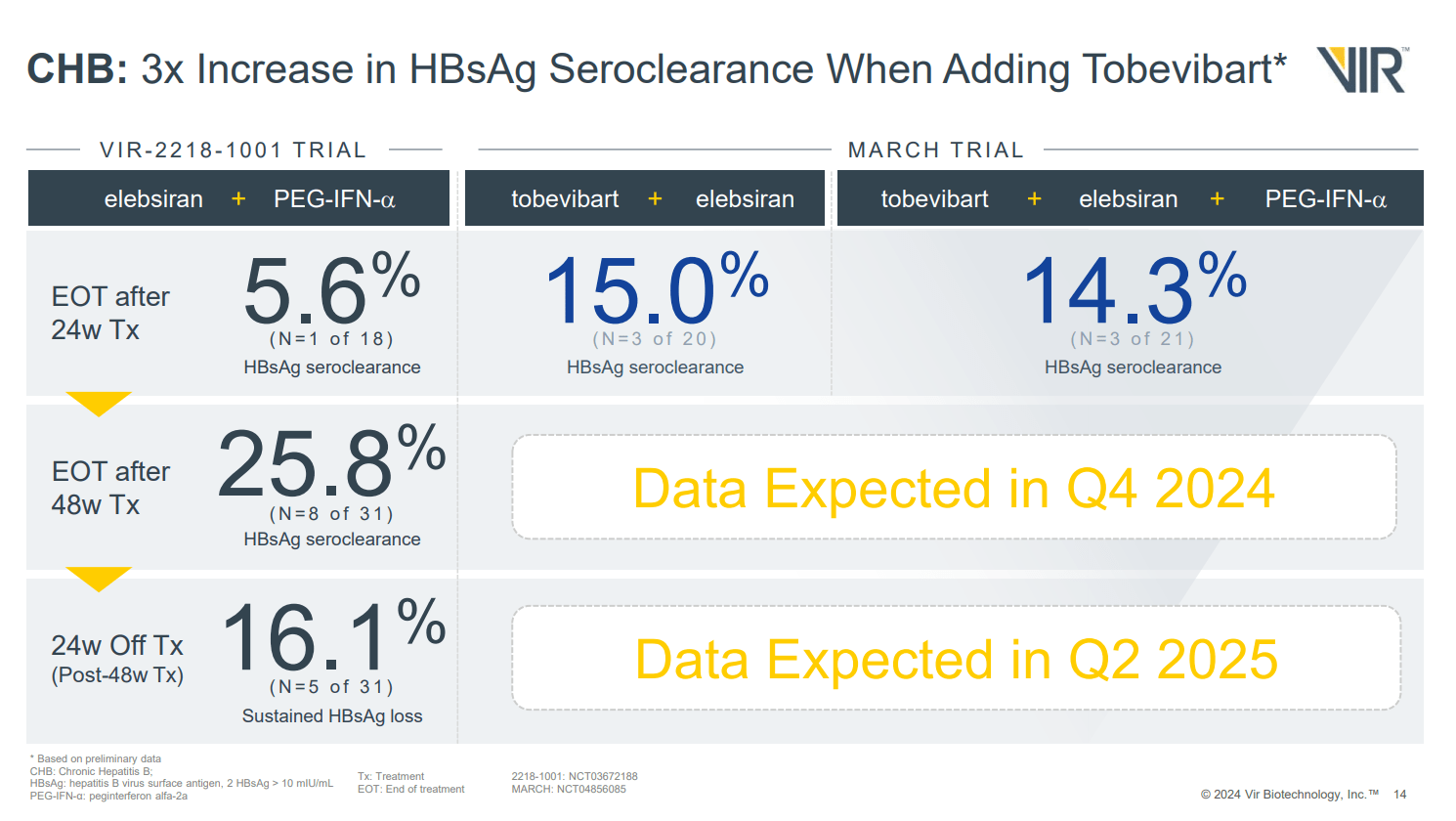

With regards to data from MARCH in patients with chronic HB, 24 weeks of treatment with the combination of elebsiran and tobevibart was similar whether administered with or without a third drug, interferon-alpha. That's good news, as an interferon-free regime could reduce side effects and simplify therapy (fewer drugs to administer). The problem is, at 24 weeks, the rate of HBsAg (Hepatitis B surface antigen) seroclearance was just 15%. On the one hand, that represents an improvement of what might be seen with elebsiran and interferon (without tobevibart) at 24 weeks, where just 5.6% patients (1/18) saw loss of HBsAg. On the other hand, it's less than was seen with 48 weeks of treatment with elebsiran and interferon, which produced a 25.8% rate of HBsAg seroclearance.

Figure 2: Slide summarizing results from the MARCH trial, and the 1001 trial. (Corporate Overview, February 2024.)

It looks like 48 weeks of treatment with tobevibart and elebsiran will be necessary. VIR is already treating HB patients with the combination for 48 weeks, but we'll have to wait until Q4'24 for data from that cohort.

A phase 1 trial of VIR's T-cell vaccine, VIR-1388, for the prevention of HIV is underway, but we won't see data until H2'24, and that data is only initial immunogenicity data. That data won't tell us if that immunogenicity actually converts to meaningful rates of HIV prevention, or how sustained that prevention would be. VIR has to start somewhere, but near-term, there will likely be more focus on the HB and HD trials.

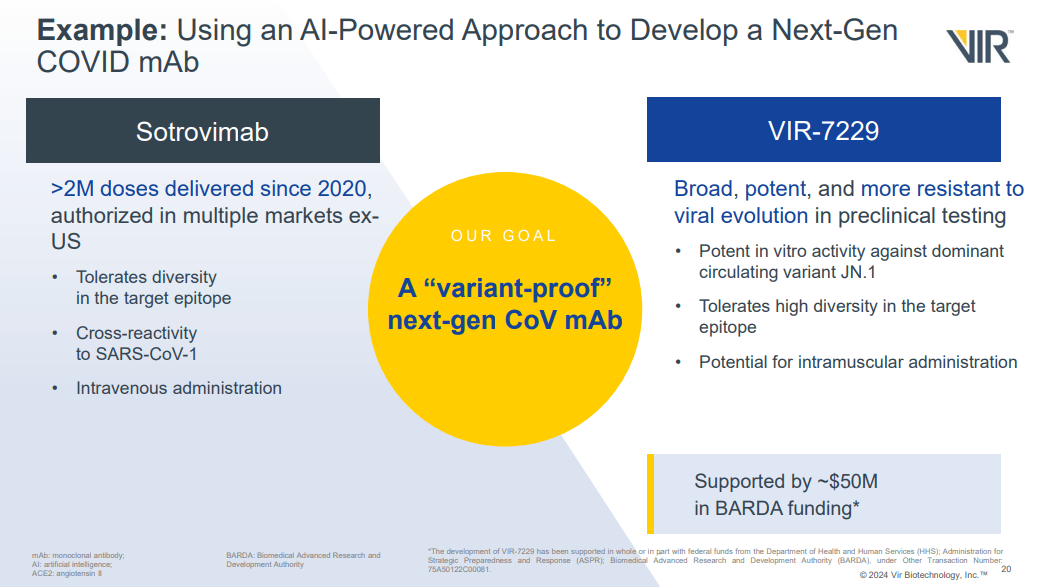

As for COVID, the company's development of a broadly neutralizing antibody for COVID remains exciting to me. As mentioned in my previous article, there was little reaction in the share price when the company secured a grant in part for the development of that antibody. I don't think VIR's attempts should be ignored, given the revenues it brought in with sotrovimab in the past. For example, VIR recognized $1.5B in sotrovimab collaboration revenue in 2022.

Figure 3: Comparison of sotrovimab and VIR-7229. Note sotrovimab was used for treatment, but VIR's pipeline slide notes VIR-7229 as prophylactic. (Corporate Overview, February 2024.)

VIR plans to file an application to run a phase 1 trial of VIR-7229 "later this year" according to the company's Q4'23 earnings press release. Whether or not the drug would actually start that trial in 2024, or early 2025, is another question.

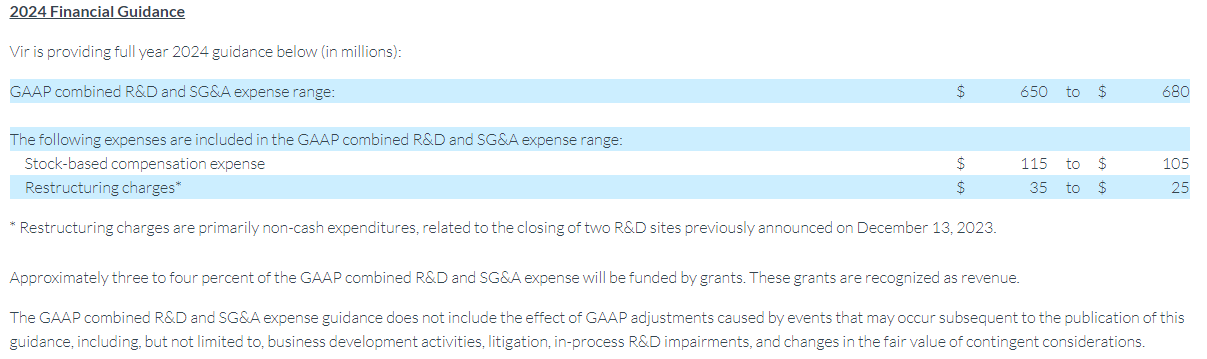

VIR had cash, cash equivalents and investments of $1.63B as of December 31, 2023. Total revenues were $16.8M in Q4'23, with $8.9M of that from collaboration revenue and $7.2M from grant revenue. SG&A expenses were $43.1M in Q4'23. R&D expenses were $111.9M in Q4'23 of which $2.6M was severance charges ($16.5M of that was non-cash compensation expense). VIR announced the company was taking steps to reduce operating expenses on December 13, 2023, so the severance charges make sense.

Looking further into that December 13, 2023, press release, the company notes it would reduce its workforce by 12% and close R&D facilities in St Louis, Missouri and Portland, Oregon in 2024. The planned steps are supposed to produce annual savings of $40M+. Even if that is true, and I have no reason to doubt that, VIR's Q4'23 earnings have come with guidance for R&D and SG&A expense that would still see the company with cash expense from R&D and SG&A at about $500M on the low end. That is, $650M guidance, minus $115M stock-based compensation expense and minus $35M in restructuring charges (which are mostly non-cash).

Figure 4: Screenshot of table on guidance from VIR's Q4'23 earnings. (VIR press release, February 22.)

It should be noted the effect of some of those cash expenses on VIR's cash balance, about 3-4% according to the footnote, would be offset by grant funding recognized as revenue. To provide a comparison, R&D expense ($589.7M) and SG&A expense ($178M) totaled $767.7M in 2023, so bringing that down to $650M-$680M does mean that VIR is serious about reducing its expenses.

Net cash used in operating activities was $778.8M in 2023, although the conclusion of VIR's studies in influenza, the workforce reduction, and the closing of two R&D sites certainly make a much lower usage of cash possible in 2023. Even at the 2023 rate of burn, VIR would have over two years of cash remaining. All things considered, VIR isn't going to run out of cash in 2024 and does have plenty of time to produce more data with its pipeline candidates.

As of February 16, 2024, there were 135,032,268 shares of VIR's common stock outstanding, giving it a market cap of $1.61B ($11.90 per share).

Since my last article, VIR stock has rallied over 35% and the enterprise value isn't negative anymore with the company trading at about cash. That being said, the company's cash will continue to run down even with a workforce reduction as the company has several programs ongoing, both clinically and preclinically. Still, the data from SOLSTICE in HD patients was genuinely good news, and further data from that trial is actually the near-term catalyst.

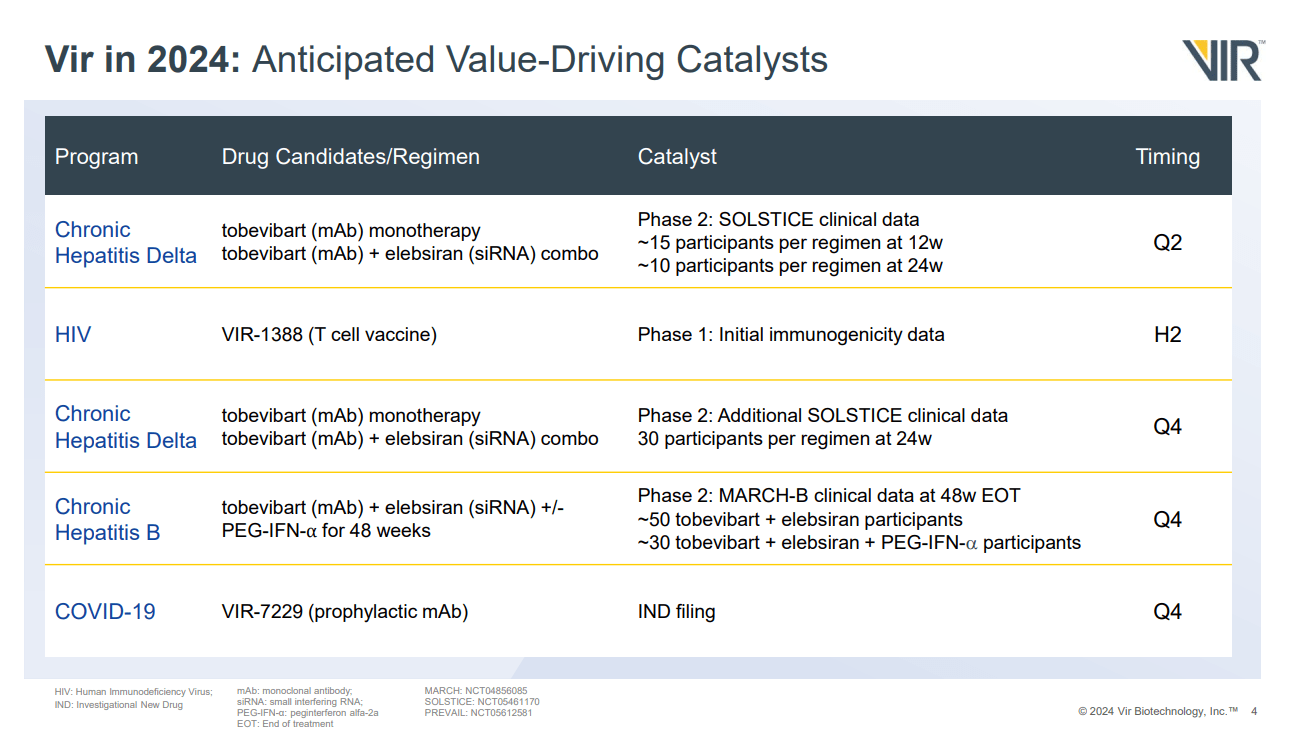

Figure 5: VIR's anticipated value-driving catalysts. Note SOLSTICE data is the near-term catalyst. (Corporate Overview, February 2024.)

As for the data in HB patients in the MARCH trial, while extending treatment from 24 to 48 weeks isn't ideal, when it came to elebsiran with interferon, this resulted in an over four-fold increase in HBsAg seroclearance rates (5.6% vs 25.8%). As such, it is tempting to suggest that doubling the length of treatment with elebsiran and tobevibart could also result in quite an increase in seroclearance rates, which could see VIR having a very impressive looking HB therapy. Overall, based on the fact that I expect more positive data from SOLSTICE in Q2'24, likely positive data from MARCH in Q4'24, and the fact that VIR has cash to last at least a couple of years, I rate the company a buy.

One of the risks of any long position in VIR is a disappointing result from one of the company's trials. While the SOLSTICE trial is apparently enrolling ahead of schedule, that doesn't guarantee the initial data seen in November will followed by strong data in Q2'24.

A further risk relates to delays in the company's clinical trials. Delays will see VIR's cash run down waiting for a result, and traders can exit to put their funds into another company with a more imminent readout.

Lastly, VIR is open to competition in the treatment of HB and HD patients. For example, GSK plc (GSK) is developing the anti-sense oligonucleotide bepirovirsen in HB. VIR's competitors reporting data could cause VIR to trade down if that data suggests their drugs pose a threat to VIR's potential revenues.