Igor Kutyaev

Igor Kutyaev

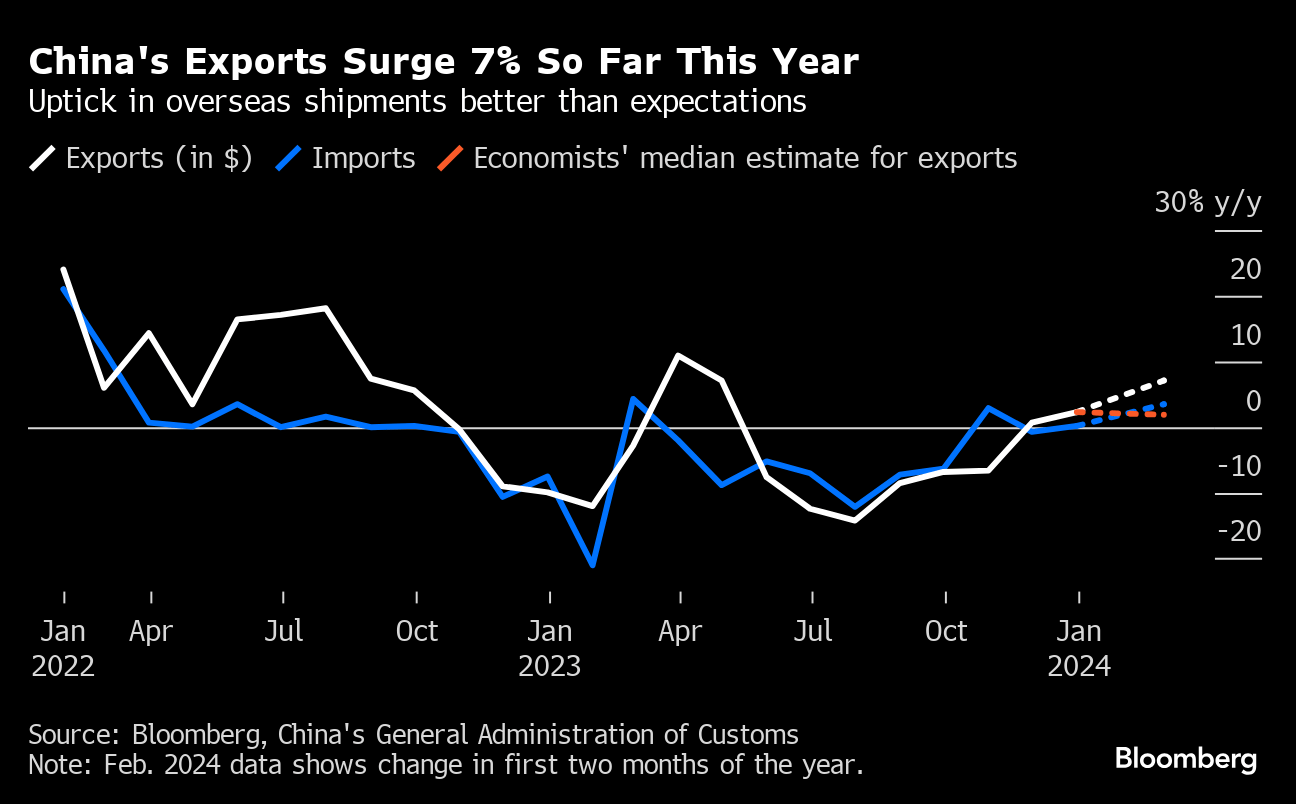

China’s economy surpassed expectations across the board in early 2024, showcased by booming exports, strong retail sales, record holiday spending, and robust industrial activity. Overseas shipments surged 7% YoY in the first two months of the year combined, well beyond economist forecasts.

Chinese Export Growth in Jan-Feb 2024 (Bloomberg)

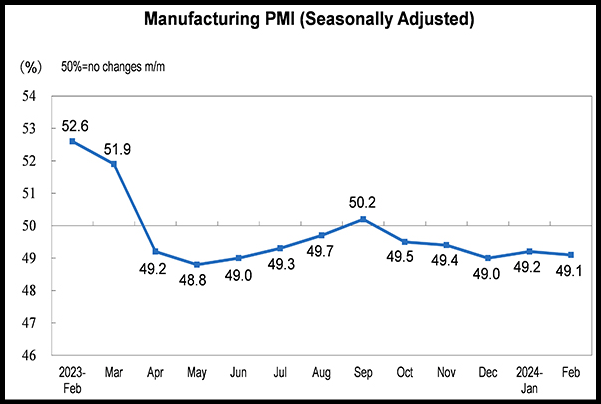

Industrial production increased 7% YoY during the same period vs. analyst predictions of 5%. China’s manufacturing PMI hit 52.6 in February, the highest factory activity level reading in almost 11 years.

China's Manufacturing PMI for February (National Bureau of Statistics of China)

China's retail sales increased by 5.5% YoY in the first two months of 2024, marking the 13th straight month of growth, while online sales of physical goods rose 14.4%. Consumer spending during the eight-day long Lunar New Year holiday (February 10-17) rose 47% YoY, topping pre-pandemic levels, and air and train travel soared. Additionally, 18 million passengers were transported by air during the spring festival, setting a new record high.

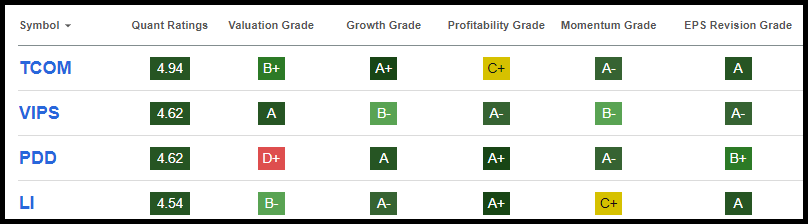

SA’s Quant Team identified four Chinese stocks that could potentially benefit from these positive economic growth trends.

The four best Chinese stock picks have Strong Buy ratings based on recommendations generated by Seeking Alpha’s quantitative stock rating system, which has a proven track record of strongly predicting future returns. SA Quant Ratings are based on over 100 underlying metrics that are systematically gathered, analyzed, and graded across five factors: Valuation, Growth, Profitability, Momentum, and EPS Revisions. All stocks on the list have strong or solid growth and EPS revision factor grades, and three have strong marks in profitability. Three possess attractive valuation metrics and all but one has decent momentum factor grades.

Top 4 Chinese Stocks (SA Premium)

The list kicks off with a company that has directly benefited from China’s travel boom, followed by two retail stocks and an EV automaker.

Market Capitalization: $28.43B

Quant Rating: Strong Buy

Quant Sector Ranking (as of 3/19/24): 6 out of 525

Quant Industry Ranking (as of 3/19/24): 1 out of 38

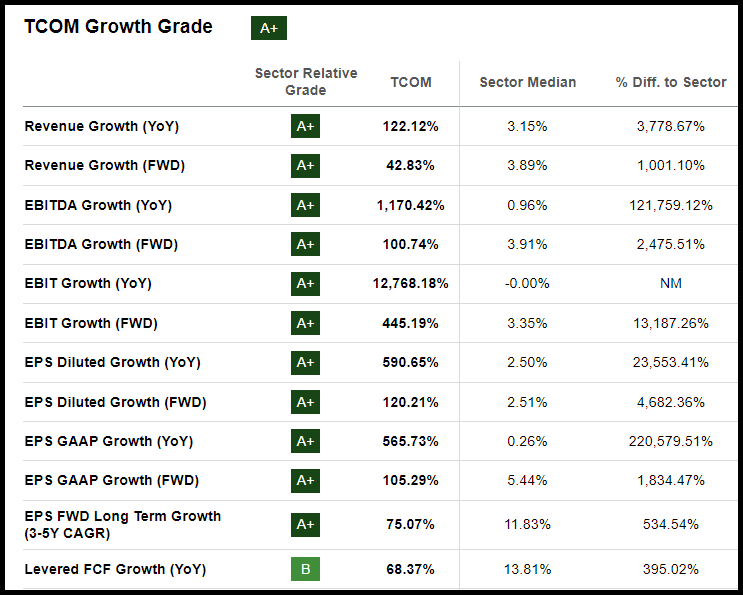

Trip.com is a Shanghai-based company, topping quant-rated stocks in the Hotels, Resorts and Cruise Lines industry, and is up around 20% in the past 12 months. CEO Jane Sun in Trip.com’s Q423 earnings call said domestic hotel and air reservations were up 60% and 50% YoY, respectively, during the Lunar New Year holiday, surpassing pre-pandemic levels. TCOM’s ‘A+’ Growth Grade is driven by sector-crushing historical and forward underlying metrics, including revenue growth YoY of 122% and revenue forward growth of 42%. EBITDA is up an astounding 1,170% YoY vs. a sector median of less than 1%, and EBITDA forward is at +100%. EBIT growth YoY was over 12,000%, and EBIT forward growth is at 445%. EPS FWD long-term growth (3-5 years), a heavily weighted metric, is 75% vs. 11% for the sector.

TCOM Growth Grade (SA Premium)

TCOM beat earnings for the seventh time in eight quarters. Q423 EPS of $0.56 beat by $0.24, and $1.44 billion in revenue (+97% YoY) beat by $15.5 million. TCOM has 20 up earnings revisions to 1 down revision in the past 90 days, with revenue projected to grow about 18% in FY24. TCOM has a C+ Profitability Grade, but gross profit margin TTM of 81%, EBIT margin of 24%, and EBITDA of 27%, are all significantly above sector peers. P/E growth forward (PEG), a crucial valuation metric, is a mere 0.22x vs. 1.5x for the sector.

Market Capitalization: $9.31B

Quant Rating: Strong Buy

Quant Sector Ranking (as of 3/19/24): 45 out of 525

Quant Industry Ranking (as of 3/19/24): 7 out of 31

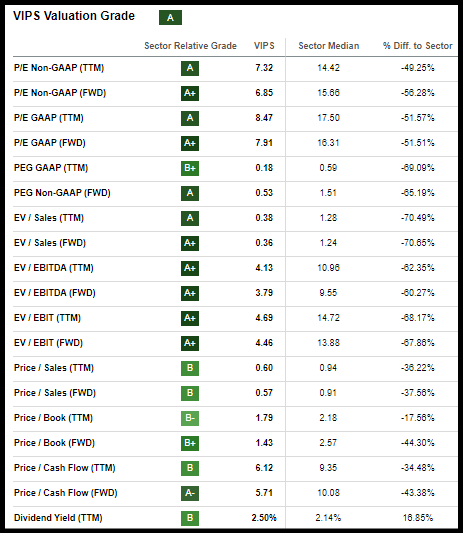

Vipshop is among the top 10 quant-rated stocks in the Broadline Retail industry and operates the VIPS online retail website where consumers can buy a wide-range of products, including clothes, cosmetics, sportswear, shoes, and supermarket products. VIPS is up ~15% in the past year and is trading at a discount relative to the sector based on most underlying valuation metrics, resulting in an ‘A’ Valuation Grade. P/E FWD of 6.8x is a 56% discount to the sector median. PEG FWD is at 0.53x, EV/EBITDA FWD 3.7x, and EV/EBIT FWD 4.4x. VIPS has an ‘A-’ Profitability Grade with ROTC at 14% and ROA at 11%.

VIPS Valuation Grade (SA Premium)

VIPS has met or surpassed earnings expectations in eleven of the past 12 quarters and has 14 earnings up revisions to 3 down revisions in the past three months. Q423 EPS of $0.80 beat by $0.09 and revenue of $4.82 billion beat by $161 million. EPS is projected to grow 7% in FY24 and sales by 5% based on consensus estimates.

Market Capitalization: $171.00B

Quant Rating: Strong Buy

Quant Sector Ranking (as of 3/19/24): 44 out of 525

Quant Industry Ranking (as of 3/19/24): 6 out of 31

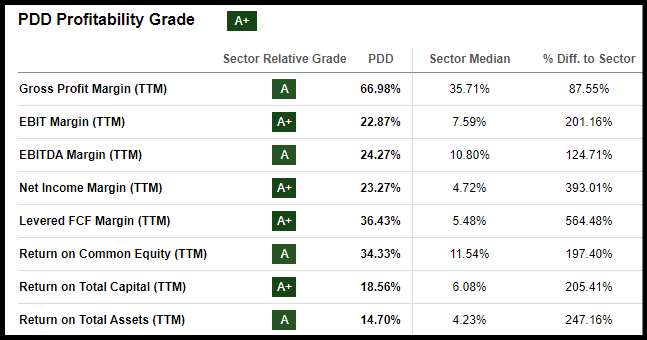

PDD operates an e-commerce platform, Pinduoduo, focused on agricultural produce and a range of product categories, including food and beverage, apparel, electronic appliances, household goods, and the Temu online marketplace. PDD has an ‘A+’ profitability quant factor grade, underpinned by an operating margin (TTM) of 22%, which is over 200% above the sector median, and levered FCF margin of 36%. PDD’s ROE (34%), ROTC (18%), and ROA (14%) metrics clearly indicate the company is outperforming significantly when it comes to effective utilization of capital and returning value to investors.

PDD Profitability Grade (SA Premium)

PDD has impressive sector-relative growth grades, with revenue YoY at 68% and revenue FWD at 45%. EPS FWD growth is a whopping 97% vs. a sector median of 5%. EPS long-term growth FWD is 27%. PDD has 10 EPS up revisions to 3 down revisions in the past three months. EPS is projected to grow 30% in FY24, while revenue is expected to rise 40%, according to the consensus estimates.

Market Capitalization: $33.22B

Quant Rating: Strong Buy

Quant Sector Ranking (as of 3/19/24): 49 out of 525

Quant Industry Ranking (as of 3/19/24): 7 out of 32

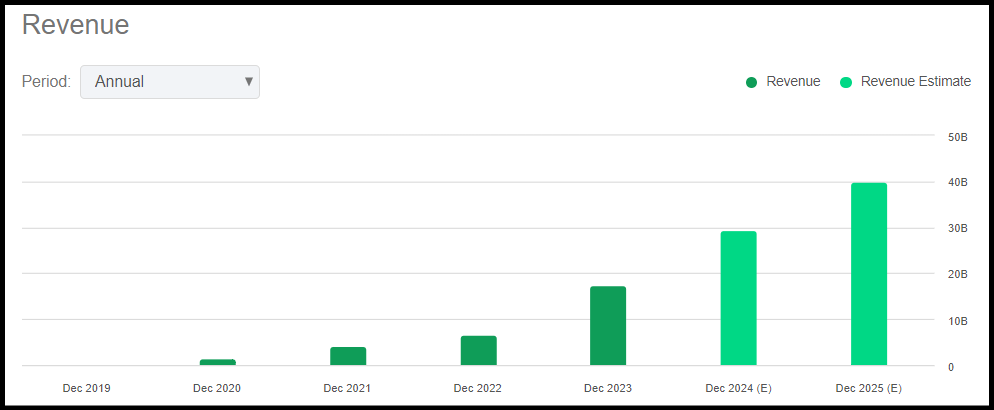

Li Auto Inc. is a premium smart electric vehicle maker based in Beijing, up about 50% in the past year, that grew by a factor of 12 from 2019-2023 to $17.45 billion. Sales is projected to grow to almost $40 billion by FY2025, according to consensus estimates. Li’s strong record of growth gives it an ‘A’ factor grade, with sales up 173% YoY, and sales growth forward at +83%. Levered free cash flow growth YoY is 817%. EPS long-term FWD is about 19%, over 60% better than the sector median.

Li Auto Sales Growth (SA Premium)

Li’s ‘A+’ in Profitability is driven by a net income margin of 9%, levered FCF margin of 35%, and ROE of 22%, all significantly above the sector, along with PEG FWD at 0.89x.

China’s economy is roaring in the first two months of 2024, setting records for holiday travel while growth in exports, retail sales, and industrial production surpassed expectations. Four Chinese stocks within industries experiencing favorable trends have been identified by the SA Quant team as attractive investments based on key quantitative metrics. The picks are at or near the top of quant-rated stocks in the automotive, broadline retail, and travel industries and have solid momentum and growth quant factor grades. In addition to top Chinese stocks, if you're seeking a limited number of monthly ideas from the hundreds of top quant Strong Buy rated stocks, the Quant Team’s best-of-the-best, consider exploring Alpha Picks.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.