Evelyn Fogleman

Evelyn Fogleman

This article explains why I have decided to downgrade the Avantis US Small Cap Value ETF (NYSEARCA:AVUV) to a hold. AVUV's sales and earnings growth rates have declined since my last review in November 2023, yet its forward P/E has increased, and its constituents are already up 25% over the previous year. To be clear, AVUV is an excellent small-cap value ETF, and there aren't many better options. However, I don't recommend adding to your position at this point, and I look forward to explaining why in further detail below.

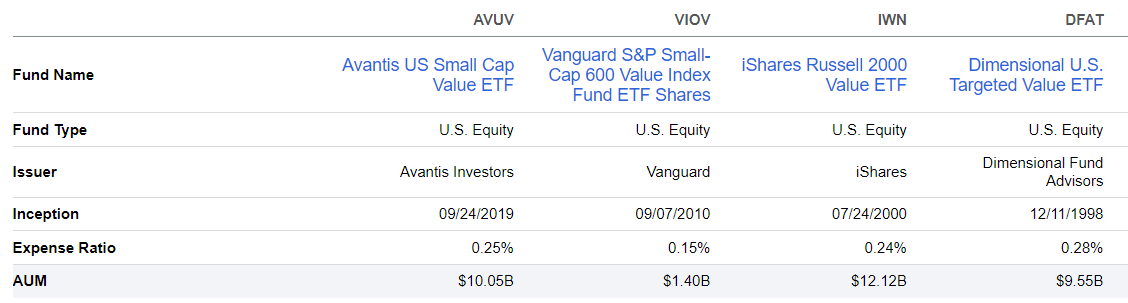

AVUV uses a proprietary approach to select highly profitable small-cap stocks trading at low valuations. The primary measure used is adjusted cash from operations to book value, which considers a company's reported and estimated book values. When creating the portfolio, AVUV's managers also consider a stock's past performance, liquidity, float, tax, governance, and diversification. Turnover is typically in the 20-25% range, so while it's technically an actively managed fund, trading activity is not much more than low-cost Index funds like the Vanguard Small Cap 600 Value ETF (VIOV). Other peers analyzed today include the iShares Russell 2000 Value ETF (IWN) and the Dimensional U.S. Targeted Value ETF (DFAT), contrasted below.

Seeking Alpha

AVUV launched less than five years ago but already has $10.05 billion in assets under management, significantly more than VIOV and about the same as IWN and DFAT. Its 0.25% expense ratio is competitive, so that's not a big consideration. Deciding which is superior comes down to each fund's performance track record and fundamentals.

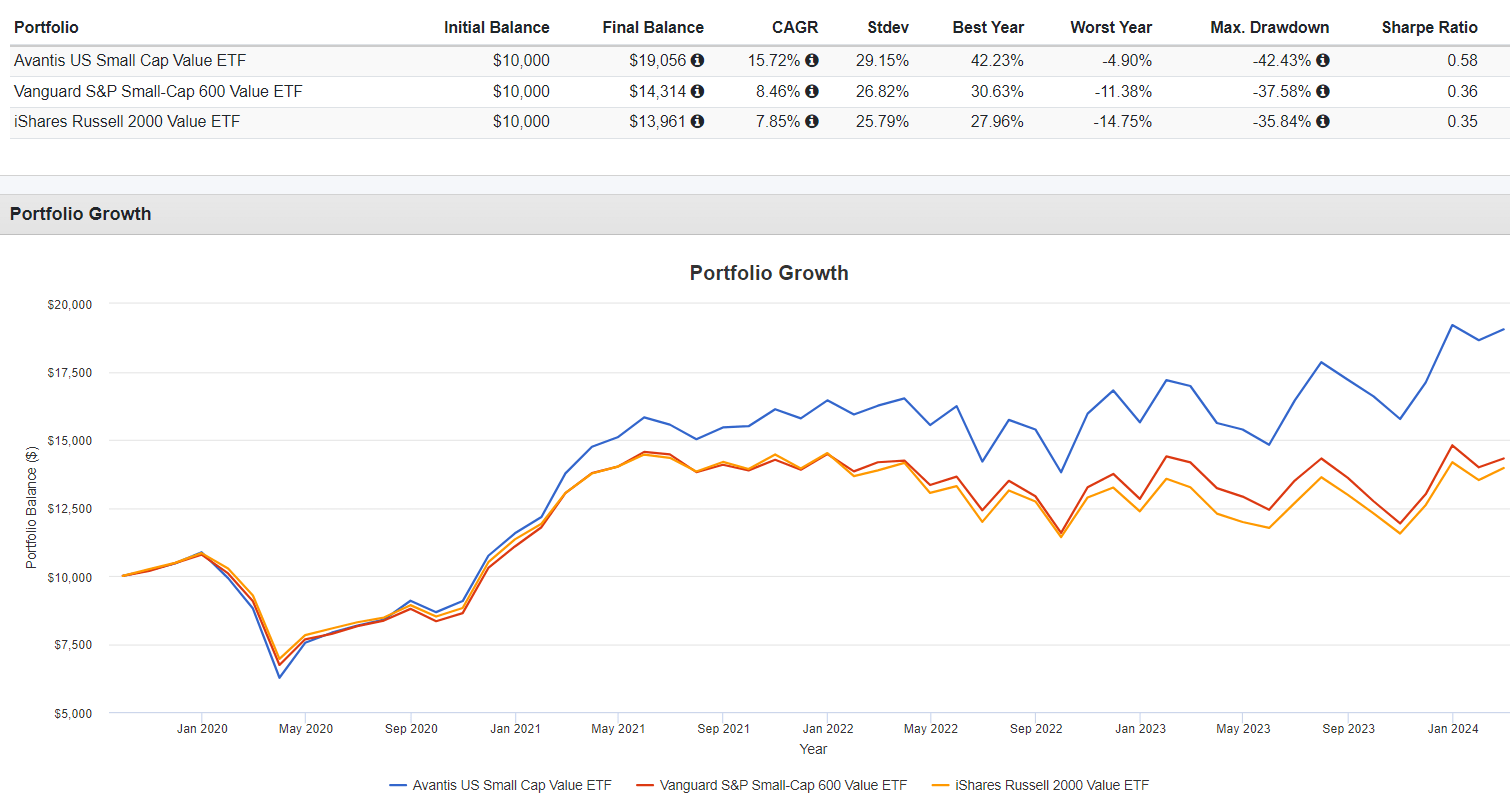

The following table illustrates how AVUV has substantially outperformed VIOV and IWN since February 2019. The 15.72% annualized return rate is 7.26% and 7.87% better, which was more than enough to offset the fund's higher standard deviation. AVUV's 29.15% figure is on the high side, and as I will touch on below, its 1.38 five-year beta driven by several Oil & Gas and Homebuilding securities might prove detrimental in a market downturn. AVUV's low portfolio turnover rate suggests managers would not act quickly, as they operate with a high-conviction mindset.

Portfolio Visualizer

We don't have much drawdown activity to examine, but AVUV did lose 42.43% in Q1 2020 compared to 37.58% and 35.84% for VIOV and IWN. AVUV ended 2020 with a 6.39% gain, better than DFAT's 2.28% return, discussed here. Portfolio Visualizer does not provide this information, as the DFAT only converted from a mutual fund on June 14, 2021.

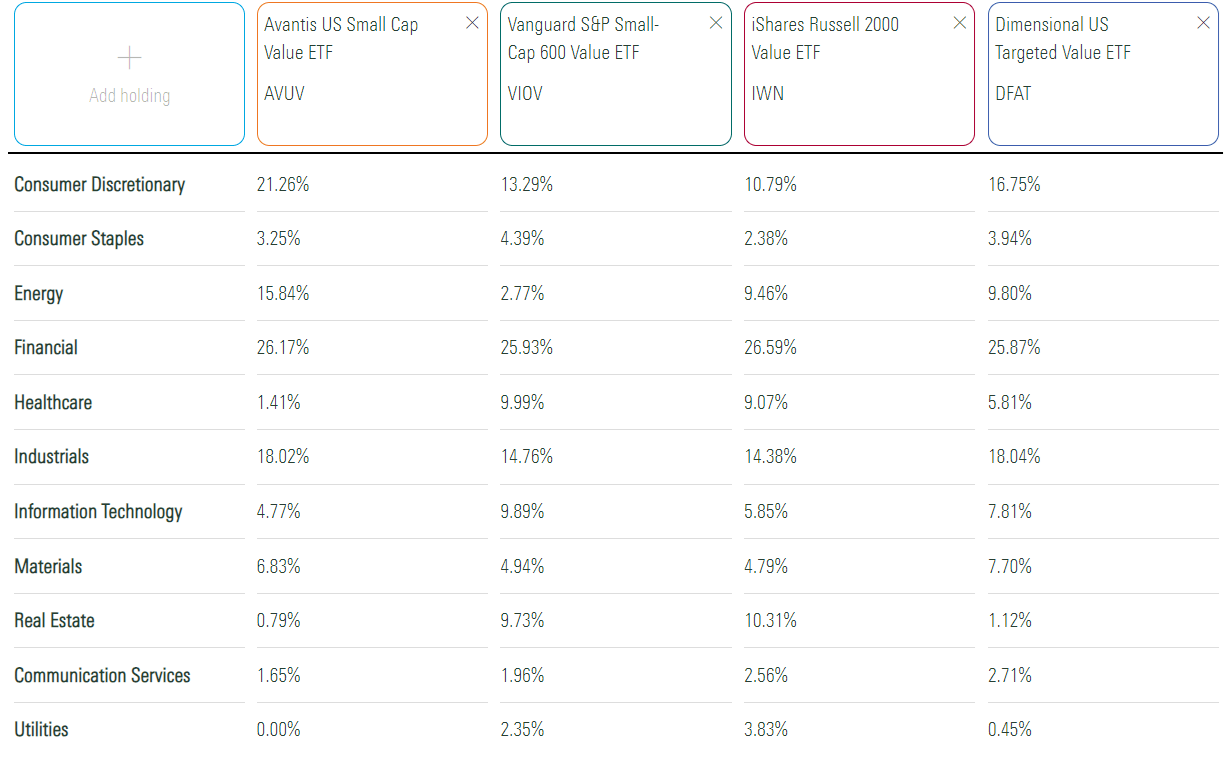

AVUV's sector exposures are listed below, alongside VIOV, IWN, and DFAT. All four ETFs overweight the Financials sector at approximately 26%, but AVUV differentiates with a 16% allocation to Energy stocks.

Morningstar

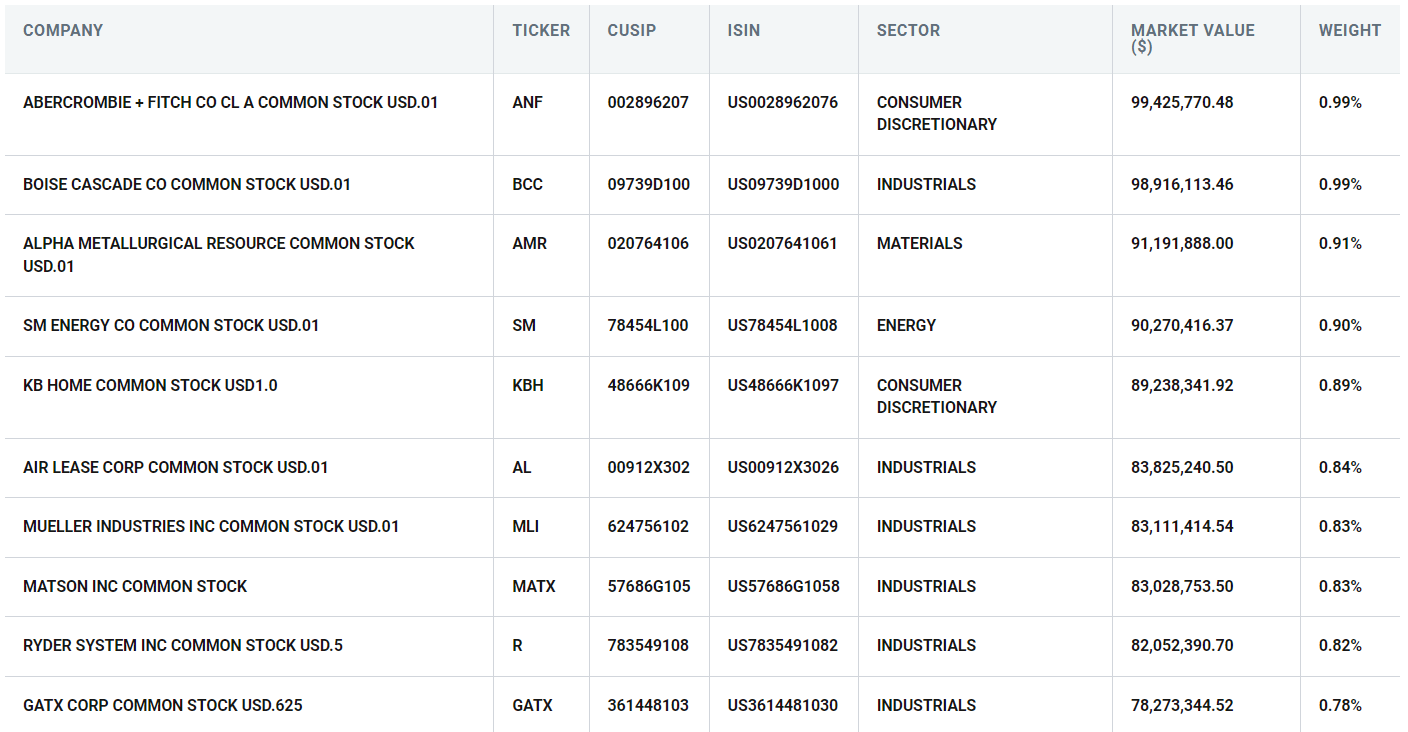

AVUV's top ten holdings, totaling 9% of the portfolio, are listed below. There are approximately 750 holdings, so even Abercrombie & Fitch (ANF), the largest holding, has a weight of less than 1%. The difference in average market cap and weighted average market cap ($1.67 billion vs. $3.20 billion) is worth noting, indicating larger companies tend to receive a higher weight. This likely results from managers' preference for profitability, which correlates positively with size.

Avantis

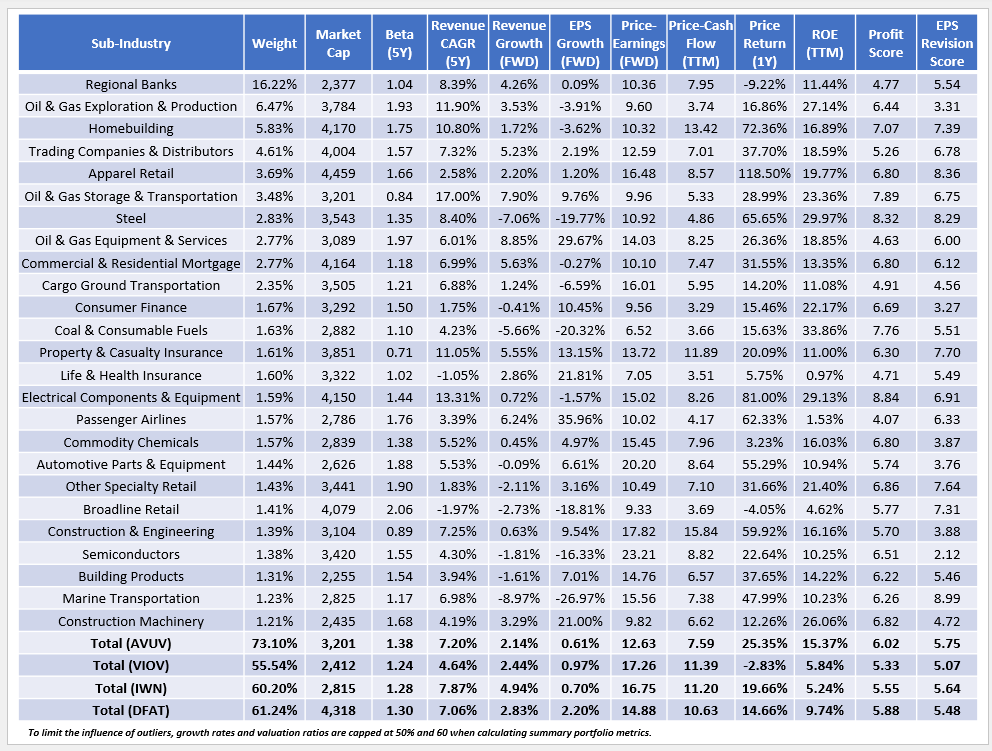

The following table highlights selected fundamental metrics for AVUV's top 25 sub-industries, totaling 73.10%. This figure reveals that despite the portfolio being well-diversified by company, it's much less diversified than its peers.

The Sunday Investor

I have four observations:

1. AVUV has 16.22% allocated to 209 Regional Banks, which might concern some readers. Still, AVUV's selections are on slightly better footing than its passive peers, evidenced by a 1.12% ROA compared to 0.79% and 0.99% for VIOV and IWN. Remember that Regional Banks are volatile and dragged down AVUV over the last year, with constituents delivering a -9.22% price return. Furthermore, these selections are only up 10.10%, including dividends, over the previous three years, and while that's what makes them potentially good value stocks, 16.22% is a lot of exposure.

2. Four months ago, AVUV featured 6.01% and 3.05% estimated one-year sales and earnings per share growth. These figures are now 2.14% and 0.61%, so growth is decelerating. In addition, AVUV trades at a slightly higher forward earnings valuation (12.63x vs. 11.23x), and it's difficult to reconcile these changes with the fund's excellent returns since my November review, shown below.

Portfolio Visualizer

AVUV is not unique in this respect. Earnings growth rates for VIOV, IWN, and DFAT are down 2-4% and forward P/E's up 1-2 points. These changes warrant caution for the entire small-cap value segment, and current shareholders might want to consider taking profits or pause building a position.

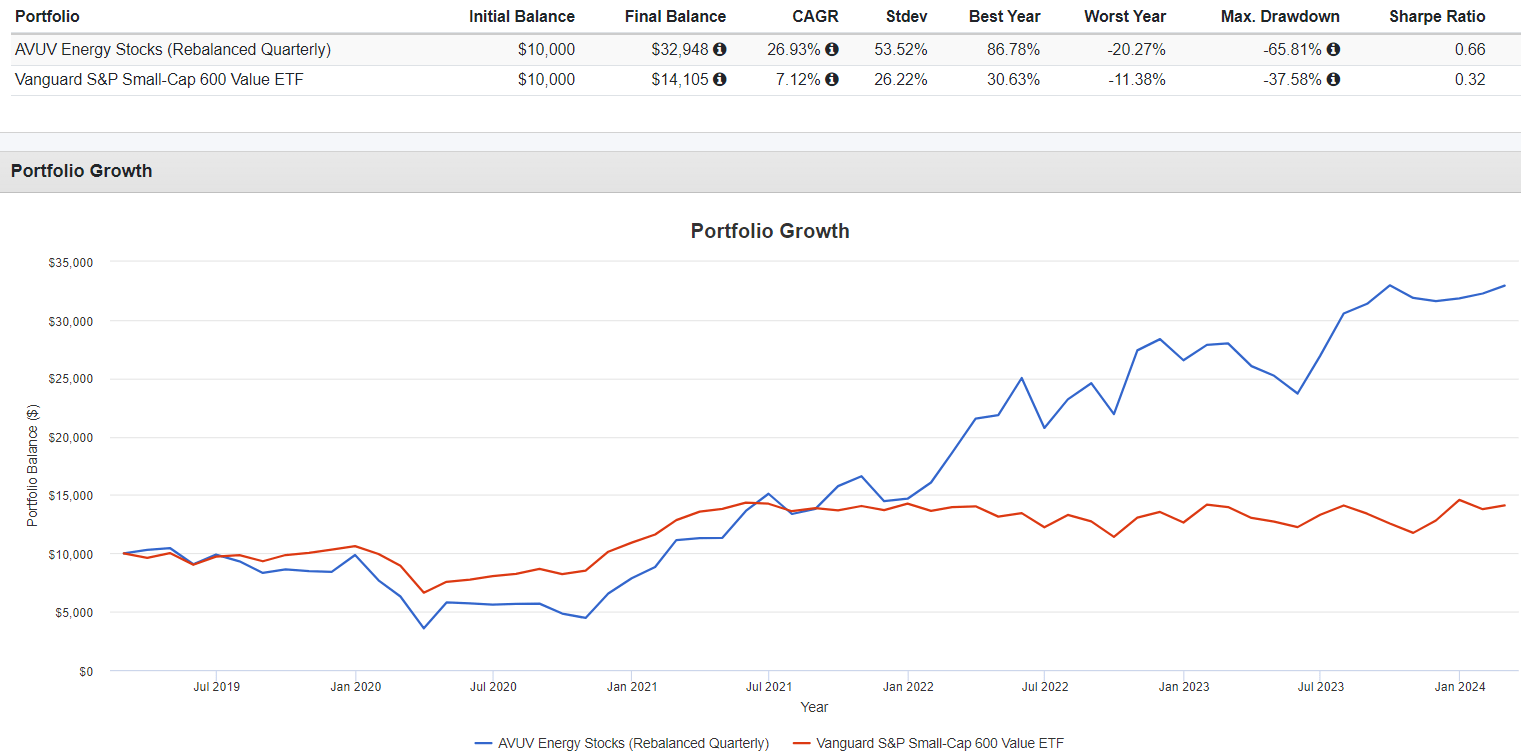

3. AVUV maintains a slight advantage over DFAT on profitability, evidenced by a 6.09/10 profit score that I calculated using Seeking Alpha Factor Grades. Regional Banks are a significant drag (4.77/10), but so are several Energy sub-industries. To gain insight into AVUV's selection process, I backtested AVUV's Energy stocks over the last five years and found they declined by 65.81% from May 2019 to March 2020 before sharply recovering.

Portfolio Visualizer

This chart suggests AVUV managers mainly consider the last few years of data and don't evaluate how its selections performed during periods of high market stress. Furthermore, since energy prices typically drive inflation and it's difficult to see inflation spiking again like in 2022, AVUV's 16% exposure to Energy stocks could be too much.

4. Despite the worsening fundamentals, AVUV still looks relatively strong compared to its peers, mainly because of its 12.63x forward P/E. I've also calculated a 10.23x harmonic weighted average P/E, consistent with Morningstar's approach, so the deep discount helps offset weak sales and earnings growth prospects.

After careful consideration, I have decided to downgrade my rating on AVUV to a "hold." The ETF had a great run over the last four months, but the fundamentals are now worse, and the risk remains high, particularly with significant exposures to Regional Banks and Energy. Since AVUV's portfolio turnover rate is typically low and its managers operate with high conviction, its composition should remain largely unchanged.

AVUV is not a "sell" because many other small-cap value peers present similar problems, and although not as cheap as before, its 12.63x forward P/E is one of the best in the segment. Assuming you still want small-cap value exposure, Avantis US Small Cap Value ETF remains a good choice, but I don't support adding to it now. Thank you for reading, and I look forward to your comments below.