Anodized aluminum coolers heat sinks.

Ladislav Kubeš/iStock via Getty Images

Anodized aluminum coolers heat sinks. Ladislav Kubeš/iStock via Getty Images

Massachusetts based Vicor (NASDAQ:VICR) designs, manufactures, and markets modular power components - including brick format DC-DC converters and complementary components such as AC-DC converters and AC-line rectifiers. The company also designs custom power systems solutions. Investors might think that such a line-up of products and services would put Vicor in an excellent position to capitalize on the current AI/Nvidia (NVDA) led boom in data-center build-out as companies accelerate digitization of their businesses and migration to the cloud in order to fully leverage AI/ML algorithms going forward. Yet that has not been the case, and Vicor's recent Q4 earnings report is yet more evidence that the stock is massively over-valued relative to its growth rate.

Back in September of 2021, I went bullish on Vicor after an impressive quarterly report (see Vicor's Strong Margin Expansion Has Made A Believer Out of Me). However, quarter-after-quarter of bullish talk and expectations - with very little follow through - indicated that Vicor's success always seemed to be in the future ... right over the next hill. The problem was that right over the next hill was ... just another hill. After a string of disappointing results, I went to an out-right SELL on Vicor in May of 2022 (see Vicor: Whipsawed) and have maintained that rating ever since (the stock is down 44% and has under-performed the S&P500 by 67% since that article was published). The company's most recent FY2023 earnings report is just another reason why investors should get out while they can.

Vicor's Q4 and full-year FY23 earnings report was released on February 22nd and it was another in a long-line of disappointing results. Highlights included:

The news got worse on the Q4 conference call, where CFO Jim Schmidt reported that the book-to-bill ratio, once again, came in below 1 (although the exact number was not specified ...) while the company keeps eating into its backlog:

I'll now address bookings and backlog. Q4 book-to-bill while improving sequentially, came in below 1 and with one-year backlog decreasing 8% from the prior quarter, closing at $160.8 million.

Vicor recorded a consolidated gross profit margin of 51.1%, ~ 0.7% less than the prior quarter. For full-year FY2023, gross margin rose by 5.4% to 50.6%, from 45.2% in FY22. That would have been encouraging had the company been able to actually grow the top-line at any kind of reasonable rate (i.e. 10-15% for a "growth company").

Best case, the prospects going forward appear hazy and potentially quite worrisome in the worst case:

Turning to the first quarter and the full year, 2024 is a year of uncertainty and opportunity. As of today, the year's outcome in terms of top line and bottom line is subject to a relatively wide range of scenarios. Given the wide range of possible outcomes, we are unable to provide quarterly guidance until we are further along resolving uncertainties and capitalizing on opportunities.

Phil Davies, Vicor VP of Global Sales and Marketing, gave a rather rambling explanation as to why Q4 bookings in HPC (high-performance computing) were lower than expected:

... we turned down deals inconsistent with our long-term OEM licensing strategy. The license gives OEMs access to alternate sources of supply for products covered by Vicor IP from otherwise infringing suppliers, enabling current and future-gen AI processors to achieve higher performance. The OEM license provides access to game-changing technology from a single-source innovator through multi-source supply chains. The OEM license avoids the risk of exclusion orders and the OEM license respects the IP of American innovators and manufacturers.

My question is: if Vicor's technology is truly "game-changing", then how come the company is not participating in the massive build-out of Nvidia-based data centers that is currently going on?

Davies goes on to say:

In anticipation of market needs, Vicor was the first to develop key technologies, control systems, topologies, components, and packaging for 48-volt high-current processor power delivery networks. Those market needs are clearly with us now in the advent of gen AI, machine learning, 48-volt rack power systems, and vertical power delivery. As evidenced by progress already made in forcing are IPs to NBMs, our message to the market is clear.

The "market needs are clearly with us now"? Really? Is that why the Q4 book-to-bill was below 1 and revenue "growth" actually contracted sequentially and on a yoy basis? The only thing that is "clear" to me is that Vicor is likely not a vendor selling into Super Micro Computer's (SMCI) modular high-performance computer/server product offerings - otherwise, its sales would be booming instead of contracting.

The point is, Vicor's conference calls continue to paint a seemingly bullish future, while the quarterly earnings reports continue to disappoint. In my opinion, this has been going on for years now and I doubt the company's strategy of over-promising and under-delivering will change any time soon. Indeed, the "strategy" appears to be ingrained in the management team. And, I have to say, it certainly appears to have kept the stock very highly valued relative to its fundamentals and demonstrated earnings reports. In that respect, I suppose the management team has been "successful". But, investors have to wonder, how long can Vicor maintain its "growth" valuation level when the company arguably isn't even growing?

In the 2023 Annual Report, Vicor says:

For 2023, exports to Taiwan were approximately $59,005,000, representing approximately 14.6% of total revenue and an approximately 43.9% decrease over the 2022 total of approximately $105,226,000. The decreased volume related to lower demand in Taiwan which is a contract manufacturing site for certain high performance computer OEMs.

The most meaningful "high performance compute OEM" to lower demand was quite likely Nvidia. Meantime, note that Vicor spent $52 million on marketing and sales during FY2023 - some 12.8% of total revenue. Those customer engagement efforts were, apparently, somewhat less than successful.

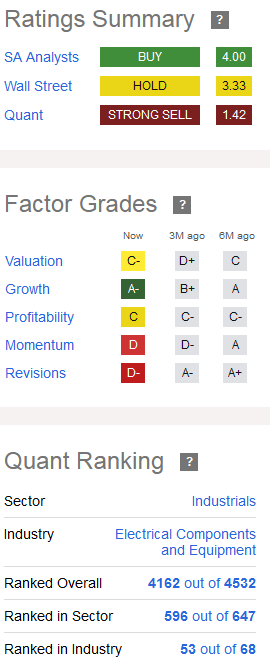

While Vicor certainly seems to have grown a bullish following on Seeking Alpha, Seeking Alpha's own investment ratings are certainly less than complimentary:

Seeking Alpha

Specifically, note the extreme under-performance of Vicor in its own industry (the Electrical Components & Equipment Group).

Indeed, on a valuation basis Vicor currently has a TTM P/E of 31.4x, which is a premium as compared to the S&P500's 27.7x. And that despite the fact that revenue in FY23 was relatively flat and the most recent quarterly results actually showed revenue is declining.

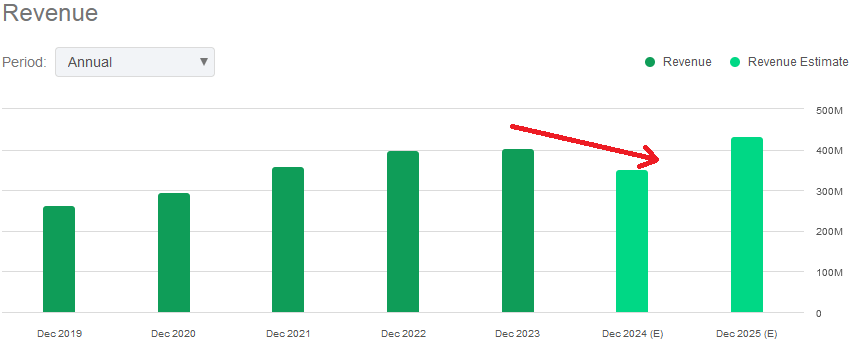

Going forward, the picture isn't any better. Seeking Alpha gives Vicor a forward P/E of 116x based on EPS estimates of $0.32/share. Indeed, revenue for FY2024 is expected to be lower by more than $50 million (13%) on a yoy basis before an expected recovery takes place in 2025 (but don't hold your breath ...):

Seeking Alpha

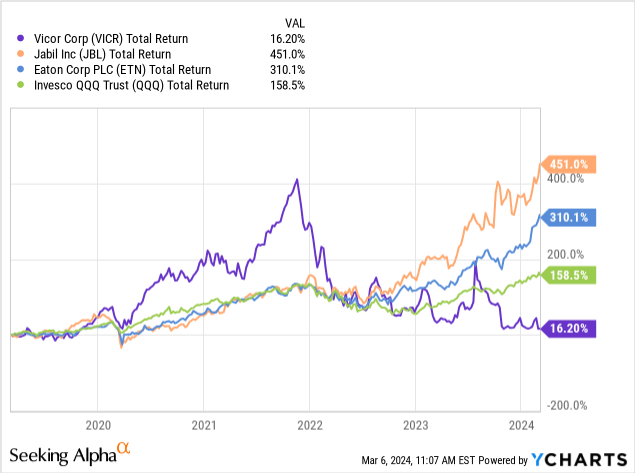

For investors looking for much better growth vehicles in the Electrical Components & Equipment related group, consider either Jabil (JBL) or Eaton (ETN), both of which I have covered on Seeking Alpha (see Jabil: Dissecting Buybacks on FY24 $1 Billion FCF Estimate and Eaton: Bullish On This Electrical Equipment Superpower). Both companies have significantly out-performed Vicor (and the Nasdaq-100 (QQQ) for that matter) over the past 5-years:

As the chart above clearly shows, there have obviously been huge opportunity costs for investors who have been waiting for Vicor's "future" to actually come to fruition ... especially compared to companies whose "future" is "now". Another observation: both Jabil and Eaton have management teams that do the exact opposite of Vicor's: they consistently under-promise and over-deliver.

Vicor ended FY2023 with net-cash of $234 million, or an estimated $5.25/share. I mention that because the company will obviously be a going concern for some time to come and - just perhaps - long enough for its "game changing" future to actually arrive.

In Q4, Vicor accrued ~$13 million in investment tax-credits related to the Biden administration's CHIPS & Science Act for equipment installed in the company's vertically integrated ChiP fab. That's not a huge amount relative to the company's annual revenue, but it is positive for investors considering Vicor's revenue actually fell in Q4 on both a sequential and yoy basis. That said, the tax credits were likely a one-off short-term boost to GAAP earnings, which is likely one reason that GAAP estimates for this year are currently $0.48/share - which would be down more than 50% yoy. Not a good trend for company that sports a high "growth company" valuation.

Vicor continues to sport a remarkably high valuation level despite its long history of delivering relatively lackluster earnings reports. Indeed, in the most recent quarter, revenue was actually down on a both a sequential and yoy basis. For the current year, Seeking Alpha reports consensus revenue estimates will be down ~13% on a yoy basis. Still, Vicor trades with a forward P/E of 116x. That's too rich for my blood. Especially given that companies like Jabil and Eaton are delivering alpha-rich returns for investors while trading at significantly lower multiples (forward P/E ratios of 16.8x and 28.5x, respectively).

That being the case, I reiterate my SELL rating on Vicor and advise investors to put the proceeds into Jabil, Eaton, or the QQQ's - all of which, in my opinion, will continue to have superior prospects as compared to Vicor going forward.