Tar_Heel_Rob

Tar_Heel_Rob

This article was coproduced with Leo Nelissen.

I already admitted in at least two previous articles that I started thinking about NCAA’s March Madness weeks ago. Months, even.

But now that it’s officially begun, you’d better believe I’ve got college basketball on the brain.

The preliminary team matchups were released on Sunday. Those initial matchups were between:

For those who don’t know how March Madness works, I’ll quote Wikipedia for convenience’s sake:

“The First Four is a play-in round of the NCAA Division I men’s and women’s basketball tournaments. It consists of two games contested between the four lowest-ranked teams in the field (usually the four lowest-ranked conference champions), and two games contested between the four lowest-seeded ‘at-large’ teams in the field, which determine the last four teams to qualify for the 64-team bracket that plays the first round.”

After that, the real melee begins, with 32 single-elimination matches scheduled across four days. It’s a full-pressure experience that requires these athletes to give it all they got.

There’s plenty of ways for athletes to get inspired to do just that, from locker-room pep talks to audience enthusiasm. But I’d throw in one more suggestion: Remembering past greats who showed us all how it was done.

In which case, I have to mention the Fab Five legends of the early 1990s.

I remember the Fab Five well. What college basketball junky my age couldn’t?

But I’ll go right to “the source” to describe this dream team at none other than the Fab Five Group:

“The Fab Five (was) the 1991 University of Michigan men’s basketball team, the greatest recruiting class of all time.

The class consisted of Chicago native Juwan Howard (#25); two recruits from Texas: Plano’s Jimmy King (#24) and Austin’s Ray Jackson (#21); Detroit natives Chris Webber (#4) and Jalen Rose (#5).

The Fab Five (was) the first team in NCAA history to compete in the championship game with all-freshman starters.”

Those young men could be controversial, from the outfits they wore at pressers to their “antics on the court.” But they definitely were worth watching. People couldn’t get enough of them.

Even today, they make the headlines. The AP published this on Jan. 15: “Michigan’s Fab Five reunites to support Howard, attends 1st basketball game at Crisler in 3 decades.” Howard, for the record, was coaching Michigan at the time.

I have to say “was,” because of this March 15 update, also from the AP: “Michigan fires Juwan Howard… after five seasons coaching men’s basketball.” To quote that piece, the school let him go after:

“Howard finished with an 82-67 record with the Wolverines, reaching some highs and lows. He won a conference regular season championship and was a win away from the Final Four in 2021, when he was named The Associated Press coach of the year.”

But…

“He lost a school-record 24 games this season as Michigan plummeted to a last-place finish in the Big Ten for the first time since 1967.”

In Howard’s defense, if it’s true that “those who can’t do teach,” then perhaps the opposite applies as well.

‘Cause, man, Howard could play.

Like I said, Howard’s college basketball career was significant – more than enough to inspire those fighting it out in March Madness now. And while his pro ball and coaching career were clearly more muted, his name remains one to remember decades after his greatest playing era ended.

Of course, when it comes to investments, we want our holdings to continue performing at any age. That’s why my “Fab Five” real estate investment trusts, or REITs, are racking up points just as well today as when they began.

One of them, VICI Properties (VICI), is admittedly less than a decade old. Except that the past 10 years involved the absolute chaos of the COVID-19 pandemic.

The REIT couldn’t open its casinos and other physical properties for months. And then for months more, people were less than enthusiastic about frequenting them.

That meant its tenants were making no in-person revenue and then severely depleted in-person revenue. Yet they never missed a single rent check.

In fact, on Feb. 18, 2021, VICI reported that, for fourth quarter 2020:

It also:

And, for the record, that wasn’t a blip. The full-year results were impressive as well despite the worldwide retail meltdown.

I don’t know about you, but that’s the kind of company I’m looking to own long term. So that’s why it easily makes my Fab Five team.

It was obvious that I would start this article with VICI Properties. After all, when speaking of fabulous, what’s more fabulous than Las Vegas?

Hotels.com

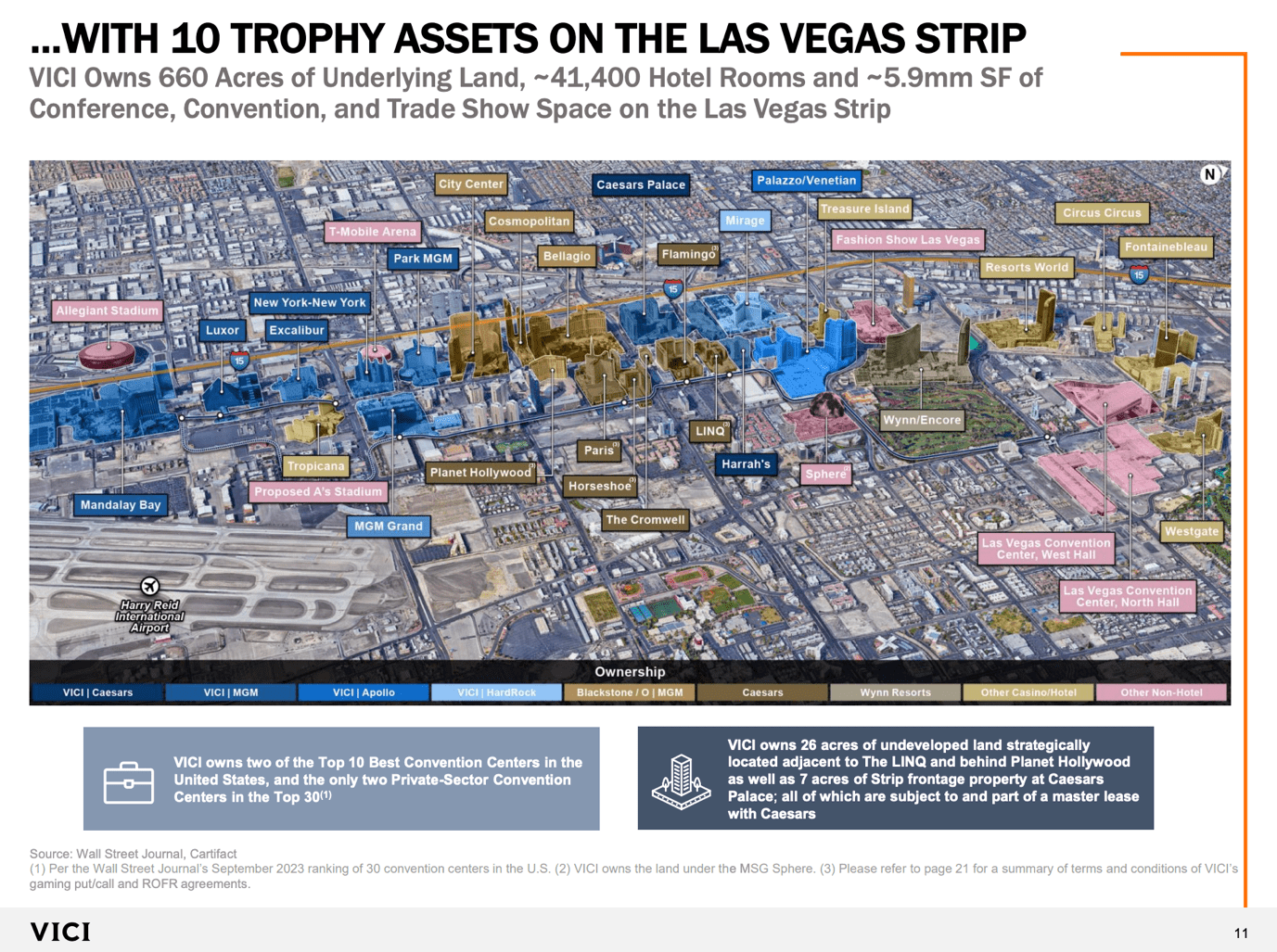

With a market cap of $30 billion, VICI Properties owns 54 gaming and 39 “other” experiential properties in 26 states and one Canadian province.

See, VICI doesn’t just buy random hotels. It buys entertainment venues that are hard to replicate.

And 46% of its footprint is in Las Vegas, where it owns some of the most iconic properties on the Strip, including but not limited to Mandalay Bay, Luxor, Excalibur, New York-New York, Park MGM, Venetian, and Caesars Palace.

VICI Properties

Its largest tenant is Caesars, which accounts for 40% of its annualized rent. This is followed by MGM Resorts, which accounts for 35% of total revenues.

The Venetian alone accounts for 9% of total rent and brings in $257.5 million each year!

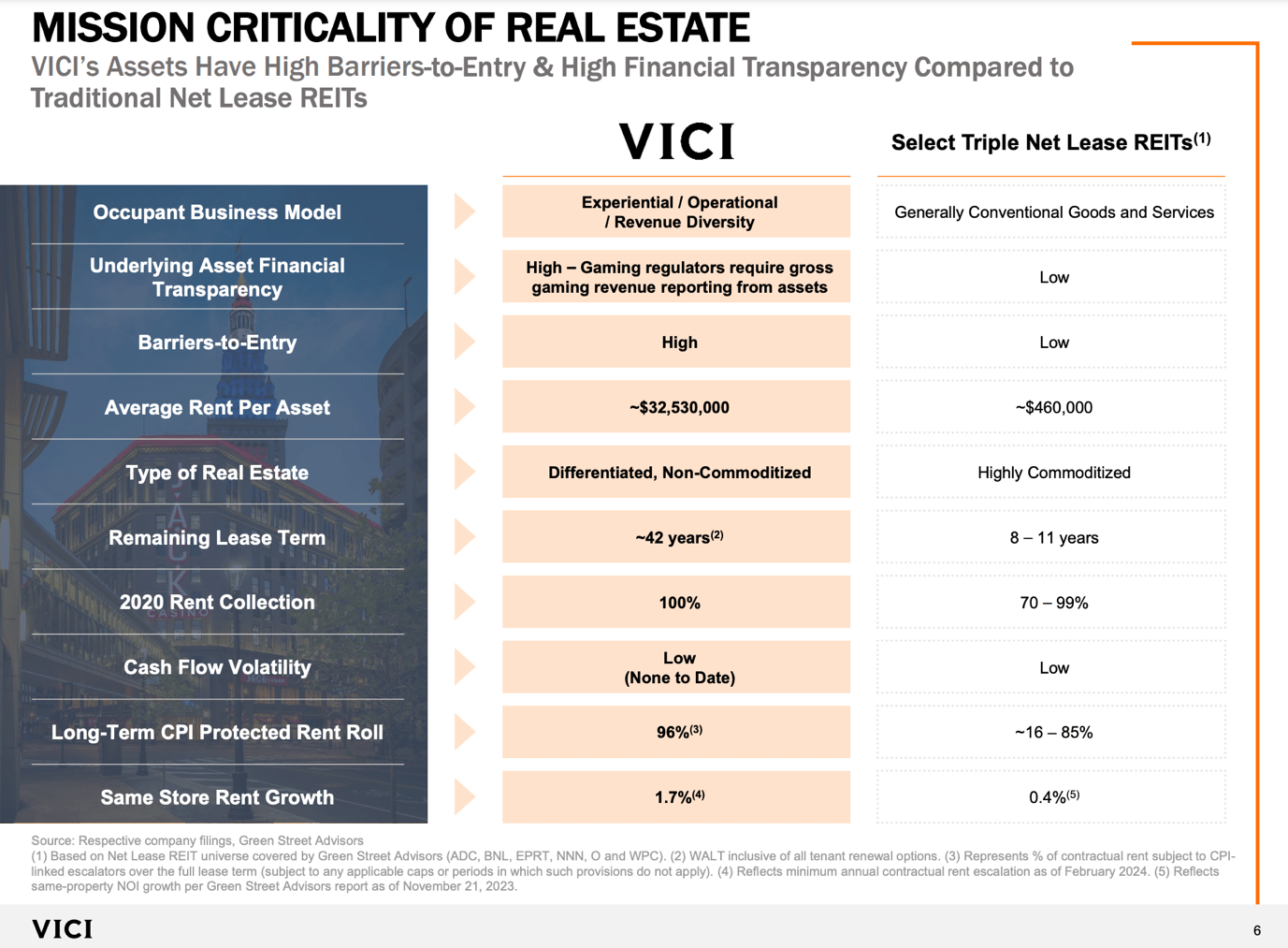

Even better, the company, which has a 100% triple net lease model, benefits from properties that are hard to replicate.

For example, its assets are highly differentiated (non-commoditized), protected by an average lease duration of 42 years, and 96% protected against inflation.

Moreover, as we can see below, during 2020, the company collected 100% of its rent, as I already briefly mentioned.

VICI Properties

It also helps that the company has a net leverage ratio of 5.7x EBITDA, which comes with an investment-grade credit rating of BBB-.

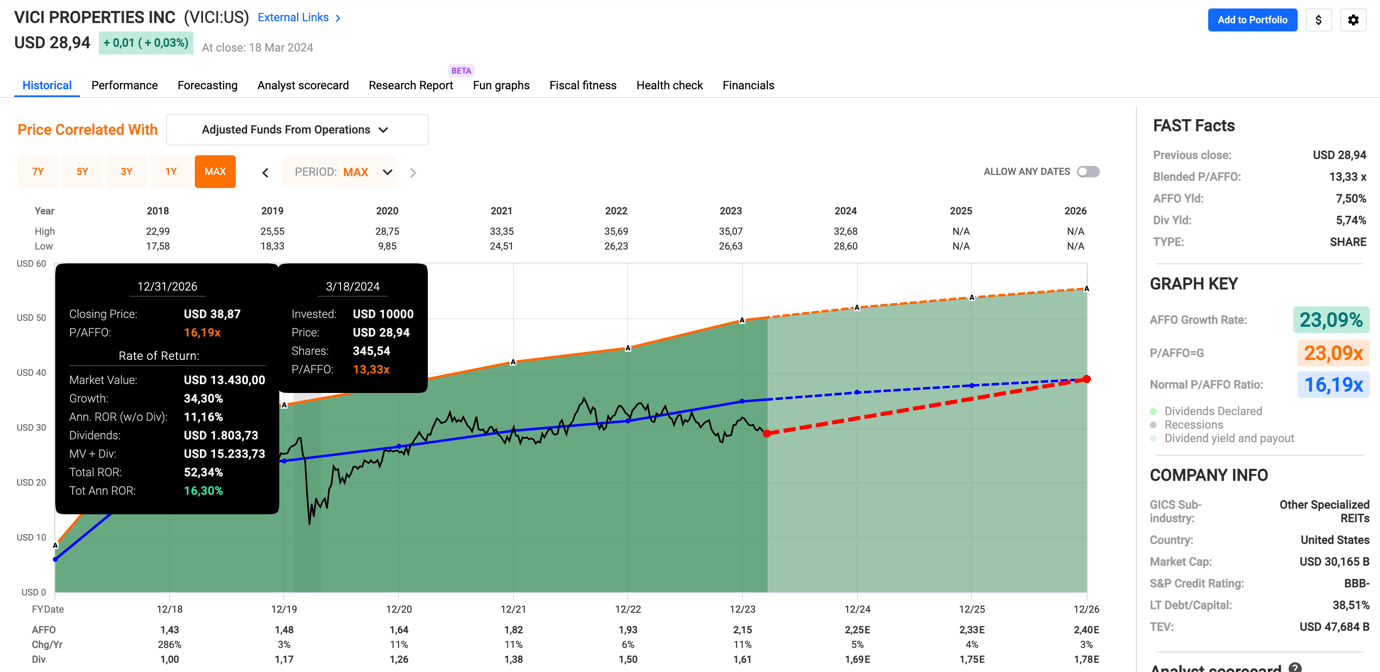

Since 2019, adjusted funds from operations (“AFFO”) growth has averaged 7.9%, which supported its dividend. The stock currently yields 5.7%. This dividend comes with a mid-60% payout ratio and a five-year CAGR of 10%.

The company also is attractively valued as it trades at a blended AFFO multiple of 13.3x, which is below its normalized AFFO multiple of 16.2x.

FAST Graphs

If we get normalizing interest rates, we could see double-digit annual returns in this name.

Investors looking for stability/safety, income, and growth shouldn’t look further than the company behind the O-ticker.

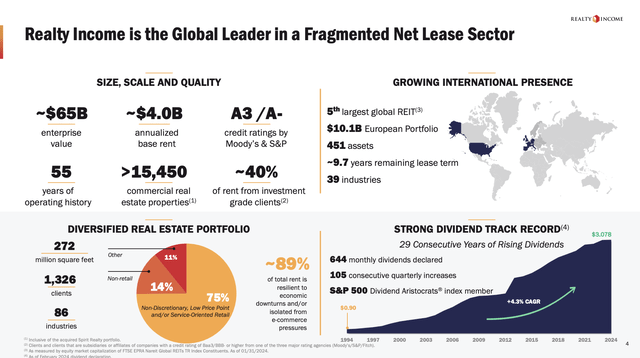

With more than 270 million square of rental space and roughly 1,300 clients, Realty Income is one of the biggest real estate operators anywhere in the world.

Founded 55 years ago, it has become the fifth largest REIT in the world, bringing in roughly $4 billion in annual rent.

Realty Income

Protected by a credit rating of A-, it has paid more than 640 monthly dividends, which includes 105 consecutive quarterly increases. It has hiked its dividend for 29 consecutive years, making it one of the few Dividend Aristocrats in the REIT space.

After all, a lot of REITs were forced to cut their dividend during the Great Financial Crisis.

On March 13, the company hiked its dividend by 0.2%. It now yields 5.9%.

This dividend is protected by its A-rated balance sheet and a mid-70% AFFO payout ratio.

The five-year dividend CAGR is 3.6%. That’s not spectacular. However, it’s decent for a company with a yield close to 6% and enough to offset the average annual rate of inflation.

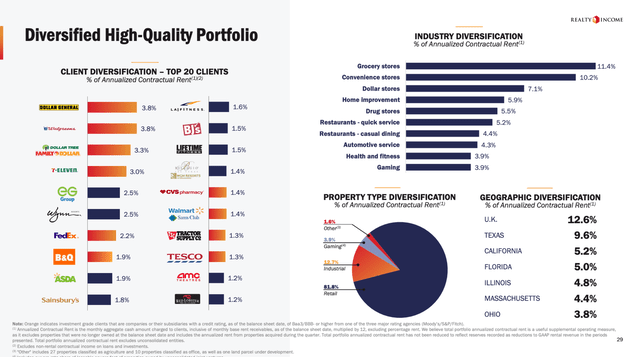

It also helps that the company has a very stellar tenant profile.

Most of its tenants operate grocery stores, convenience stores, dollar stores, and home improvement stores.

Its largest tenants are Dollar General (DG), Walgreens (WBA), and Dollar Tree (DLTR), which tend to be highly desired tenants for people trying to get into the triple net lease business, as they come with a lot of stability.

Realty Income

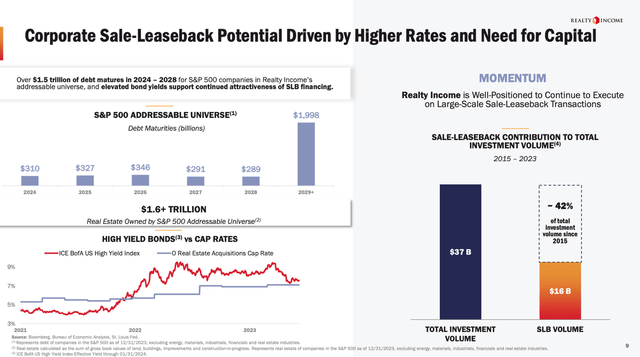

Another reason to like the company is its resilience in a tough environment of elevated rates.

While there's no denying that Realty Income would trade at a much higher price if rates and inflation were lower, the company sees an opportunity in sale-leaseback (“SLB”) operations.

SLB deals allow companies to sell their buildings to a company like Realty Income. This frees up cash. Especially in times of elevated rates, companies opt to sell their buildings to avoid high rates on new loans.

In exchange for selling their buildings, they pay monthly rent to the landlord.

As Realty Income has access to attractive funding, it’s a fantastic opportunity for growth with an addressable market of $2 trillion. That’s not a typo.

Realty Income

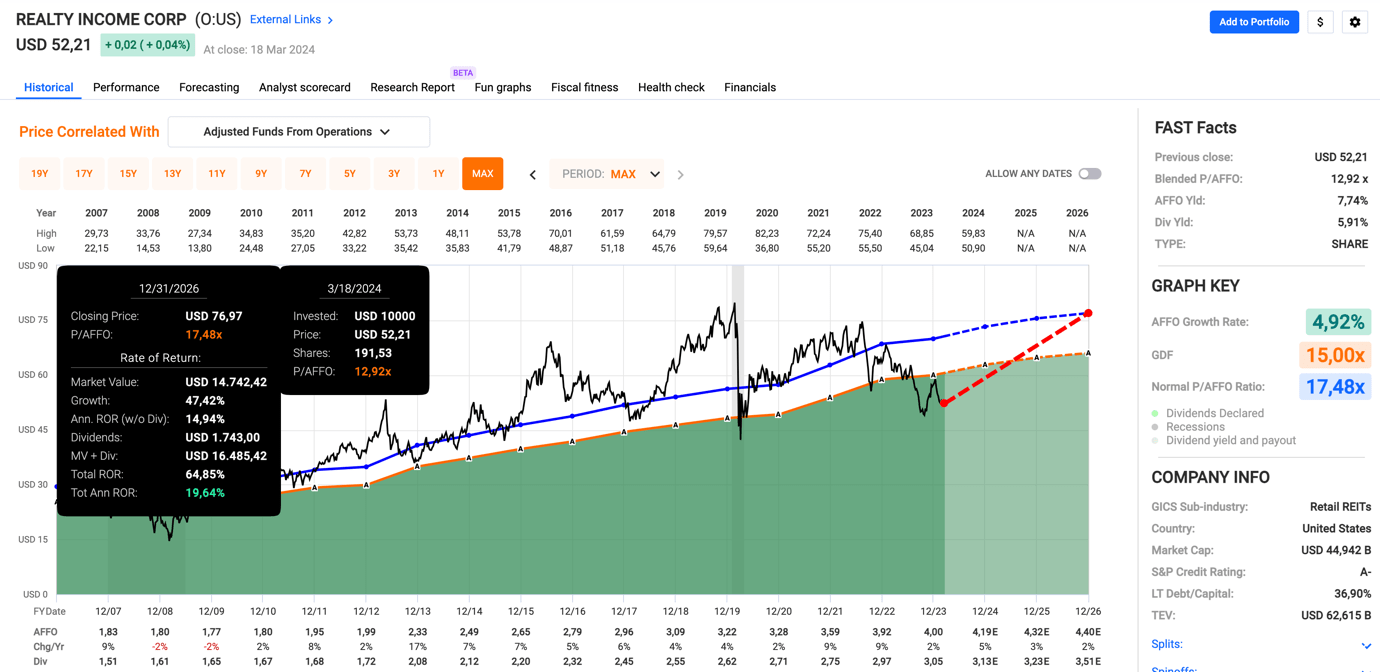

While Realty Income investors enjoy SLB benefits and a fantastic triple net lease business model, the best thing about the company may be its valuation.

Trading at a blended P/AFFO ratio of 12.9x, the company trades at a big discount to its 17.5x normalized valuation. It’s also expected to avoid AFFO contraction, with 5% expected per-share AFFO growth in 2024 and 3% growth in 2025.

FAST Graphs

Although it requires lower interest rates to unlock value, the stock is trading roughly 40%-50% below its fair value, which bodes well for longer-term returns.

Besides that, it doesn’t hurt to collect a 6% dividend while waiting for investors to apply a higher multiple to this giant.

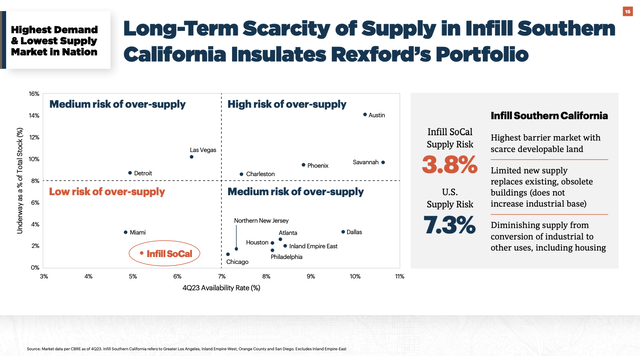

Southern California (“SoCal”) is a topic that quickly leads to political discussions.

However, regardless of one’s view on SoCal or California, in general, it’s important to be aware that it’s still the biggest consumer market anywhere in the world.

It’s also the biggest industrial market in the United States. Bigger than the Rustbelt or the emerging industrial sector in Texas.

SoCal also benefits from two major ports (Los Angeles and Long Beach) and severely constrained industrial supply growth. Unlike other markets, it’s hard to build new industrial assets in SoCal.

As we can see below, the SoCal infill market has both availability and supply benefits.

Rexford Industrial Realty

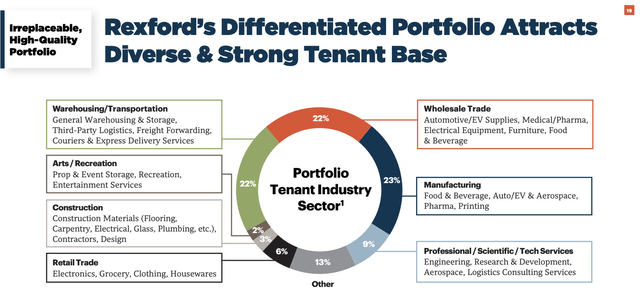

In this market, Rexford Industrial Realty shines bright.

The company has a well-diversified tenant base consisting of warehouse and transportation giants, wholesale traders, and manufacturers (among others) that are expected to protect the company against potential industrial weakness.

Currently, the company has a 97.8% occupancy rate. This year, that number is not expected to drop below 96.5%, according to company guidance.

Rexford Industrial Realty

On top of that, it has elevated growth expectations. As we can see below, AFFO per share is expected to rise by 10% this year, potentially followed by 18% growth in 2025 and 15% growth in 2026.

FAST Graphs

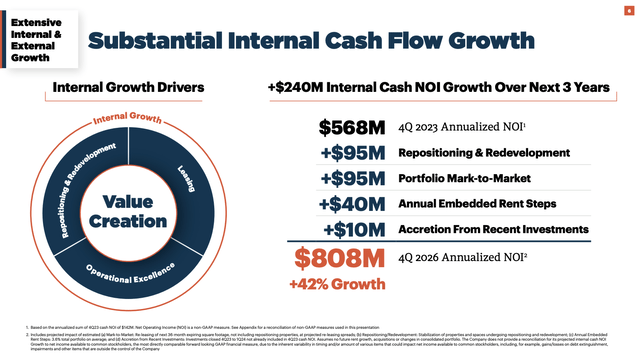

A big part of this growth is provided by internal growth.

Through 2026, the company sees more than $800 million worth of net operating income (“NOI”) growth. That’s a 42% growth rate based on redevelopments, rent adjustments, embedded rent growth, and accretion from recent investments.

Rexford Industrial Realty

It also has a fantastic balance sheet with a net leverage ratio of just 3.6x EBITDA, a BBB+ credit rating, and $1.2 billion in liquidity.

The stock currently yields 3.2%. This dividend has a five-year dividend CAGR of 18%. Since it went public roughly ten years ago, annual dividend growth has averaged 23%.

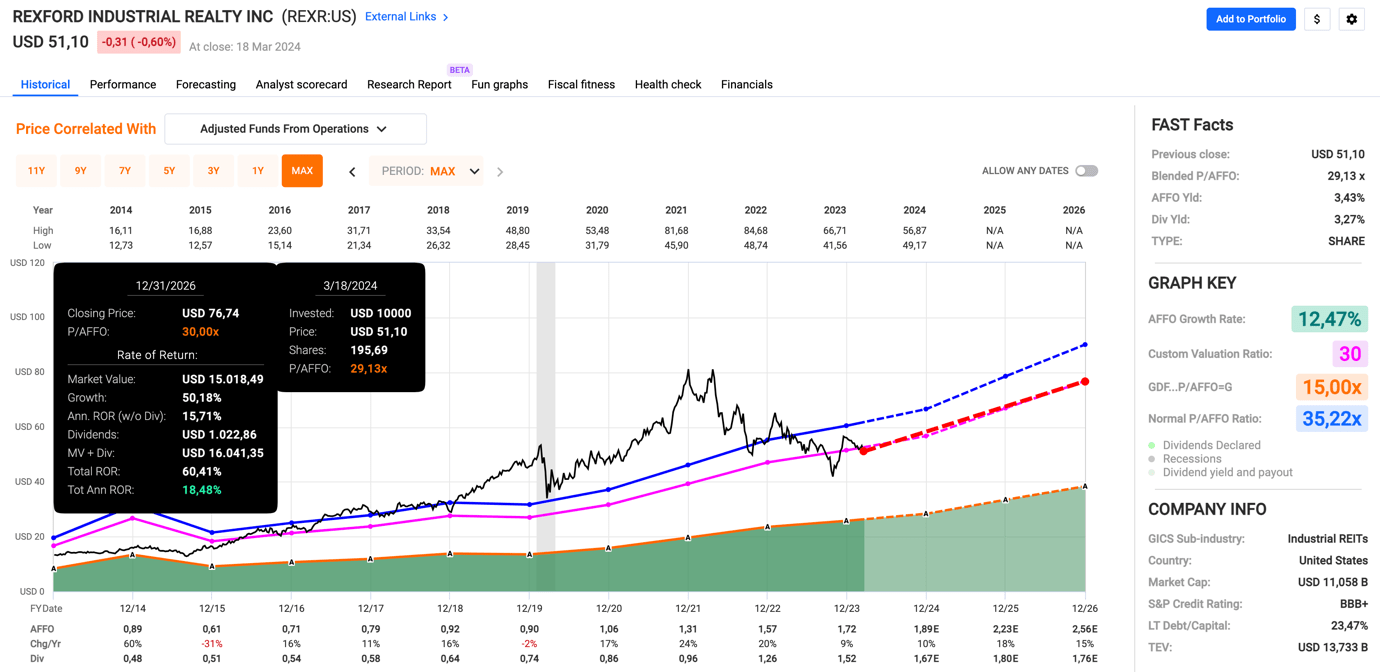

Even better, the stock is trading at just 29.1x AFFO. While that may be elevated, it has a normalized AFFO multiple of 35.2x and growth expectations that most REITs cannot compete with.

Even a 30x multiple would indicate that REXR is up to 50% undervalued.

While economic uncertainty and rate/inflation headwinds may keep a lid on the stock, the stock is definitely a fabulous addition for REIT investors seeking both yield and growth.

If you like Realty Income, odds are you’ll like Agree Realty as well.

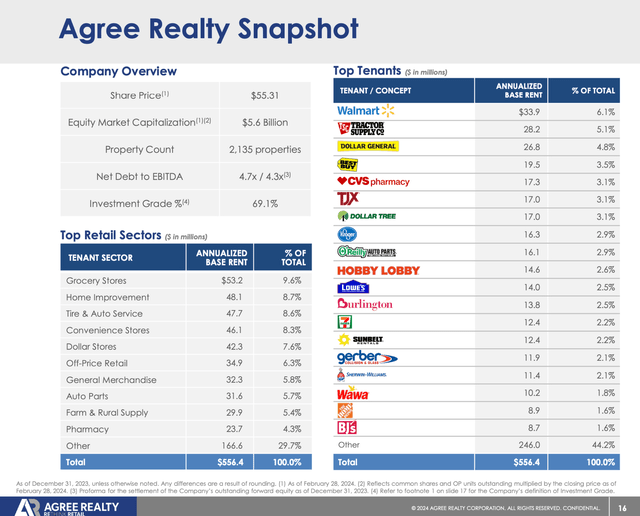

Like its bigger brother, this triple net lease company has some of the best tenants in the United States.

The company, which has more than 2,100 properties, generates most of its revenue from companies like Walmart (WMT), Tractor Supply (TSCO), Dollar General, Best Buy (BBY), CVS (CVS), and others.

Agree Realty

69% of the company’s tenants have an investment-grade balance sheet, which brings a lot of safety to the table – especially in this market environment.

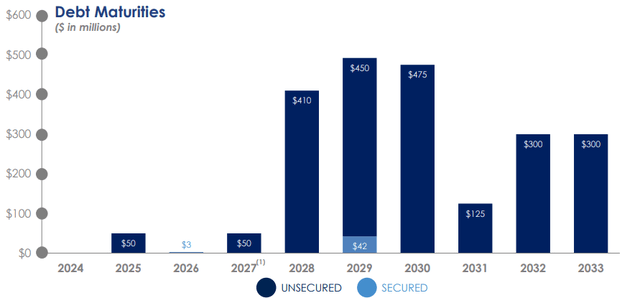

The company itself also is investment-grade rated as it has a BBB rating with a net leverage ratio of just 4.5x EBITDA.

Even better, it has barely any maturities until 2028, which buys the company a lot of time in this very unfavorable environment.

Agree Realty

This isn’t just great news in terms of financial risks but also allows the company to capitalize on weakness if we were to enter a scenario where weaker landlords are forced to sell assets to service their debt.

Moreover, it also benefits from sale-leaseback deals.

Last year, SLB deals accounted for a third of acquisitions. In 2022, that number was just 10%!

This number is likely to remain stable as ADC is not looking to take on tenants with elevated financial risks. After all, companies that require SLB deals aren’t always the safest tenants.

ADC is finding the right balance to benefit shareholders without taking on too much risk when it engages in SLB deals.

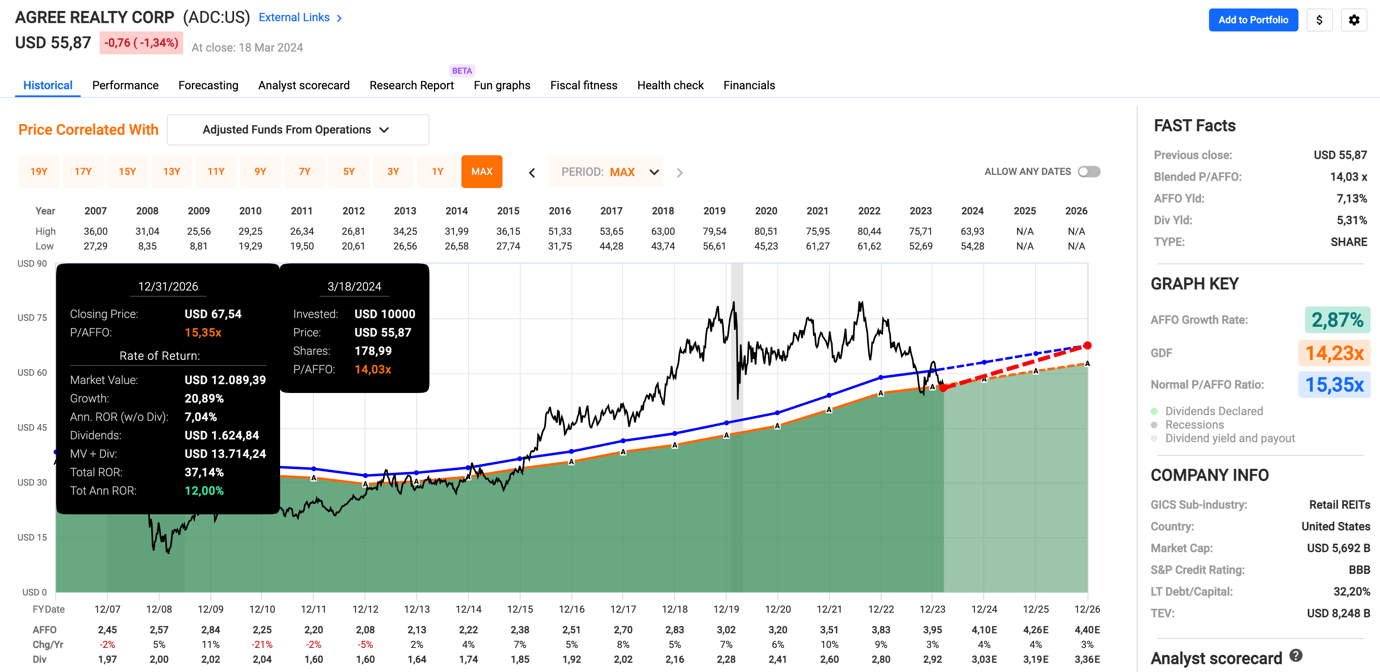

It also has an attractive valuation and a juicy yield.

The company has a dividend yield of 5.3%. This dividend is protected by a payout ratio in the 70% range and comes with a five-year CAGR of 6.4%.

In other words, it has a 60 basis points lower yield than Realty Income yet higher dividend growth.

It also trades at just 14.0x AFFO. That’s below its normalized valuation multiple of 15.4x and implies that ADC shares are roughly 20% undervalued. This number also includes the outlook of roughly 4% annual AFFO growth in 2024 and beyond.

FAST Graphs

It may not be as cheap as some other stocks on our fabulous list. However, it comes with safety, a juicy yield, consistent growth, and a tenant/asset portfolio that most peers can only dream of.

The beauty of buying REITs is that instead of doing the work ourselves, we can buy thousands of high-quality assets from the comfort of our own homes.

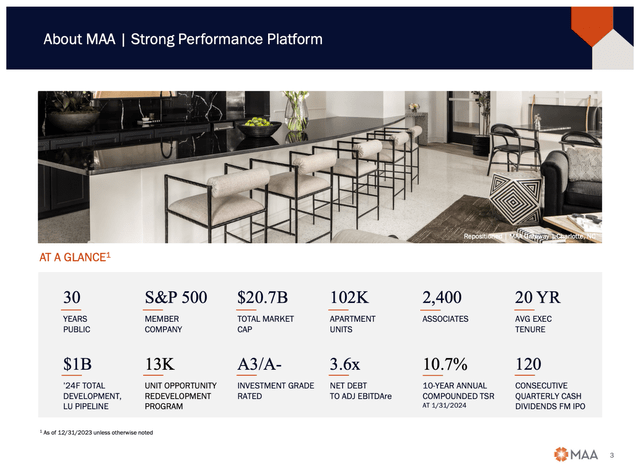

In the case of Mid-America Apartment Communities, we can buy more than 100,000 apartments.

After being in business for 30 years, MAA has become one of the largest residential landlords in the United States. This S&P 500 member is so large that its development pipeline for 2024 alone is $1 billion.

Mid-America Apartment Communities

It also enjoys a credit rating of A- and a net leverage ratio of just 3.6x EBITDA.

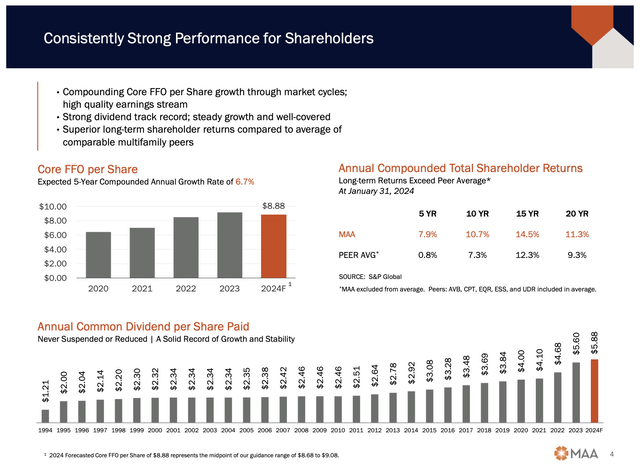

What sets MAA apart isn’t just its ability to buy a ton of apartments without damaging its balance sheet but also the fact that it has been a source of income, growth, and stability for millions of investors.

Over the past 20 years, the company has returned 11.3% per year, beating its peers by 200 basis points per year.

It also kept its dividend steady during the Great Financial Crisis when many peers (especially private companies) were forced to cut their dividends and sell assets.

Mid-America Apartment Communities

Speaking of its dividend, MAA currently yields 4.5%. This dividend has a five-year CAGR of 8.8% and a sub-66% payout ratio.

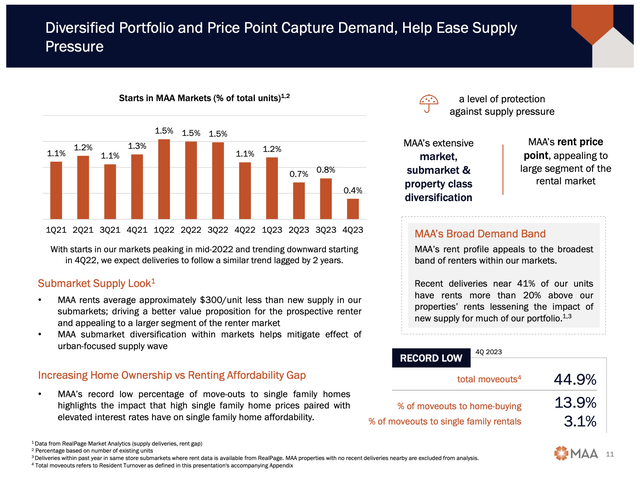

It also helps that the company is solely focused on the Sunbelt (excluding California), where it enjoys strong tenants.

80% of its tenants are single, with a median age of 34. The rent/income ratio is just 22%. That’s at least eight points below the nation’s average.

Adding to that, despite rising supply in major Sunbelt markets, the company enjoys a strong market presence and record low moveouts.

Mid-America Apartment Communities

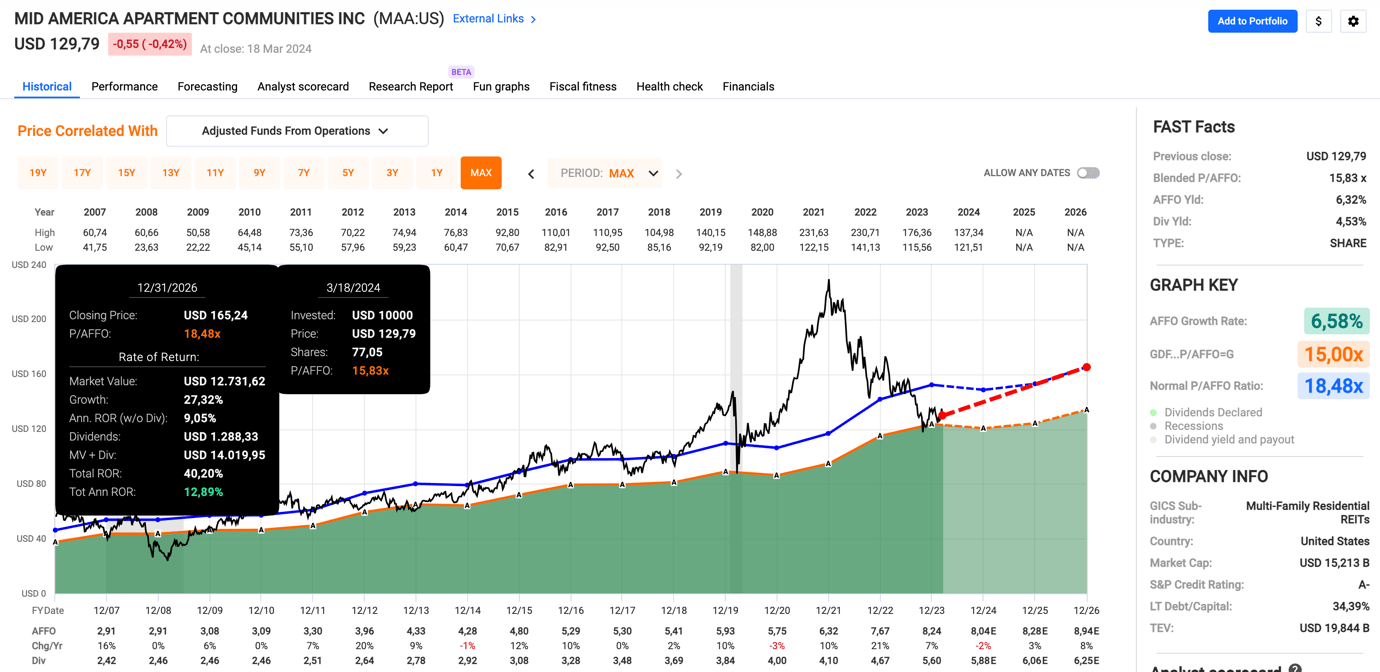

It's also attractively valued!

The company, which is expected to see a 2% per-share AFFO decline this year, is expected to see accelerating growth in 2024 and 2025, making its current blended P/AFFO ratio of 15.8x attractive.

The normalized AFFO multiple is 18.5x. A return to that number could unlock up to 27% upside – excluding its dividend.

FAST Graphs

While it will likely require lower rates, MAA is a fantastic stock to buy and hold. It has a juicy yield, an anti-cyclical tenant base, a stellar balance sheet, a good growth outlook, and a very attractive valuation.

If that doesn’t make it fabulous, I’m not sure what will.

As March Madness captivates the nation, the legacy of the Fab Five reminds us of the power of greatness in the face of controversy.

Just as these basketball legends left an indelible mark, my "Fab Five" REIT picks continue to impress with their resilience and performance.

VICI Properties dominates the Las Vegas scene with its diversified portfolio, while Realty Income's stability and consistent growth mirror its "Monthly Dividend" reputation.

Meanwhile, Rexford Industrial Realty capitalizes on SoCal's thriving market, Agree Realty balances safety and growth in the SLB market, and Mid-America Apartment Communities offers stability and income in the residential sector.

With each REIT boasting unique strengths and attractive valuations, they exemplify the enduring spirit of excellence, just like the Fab Five on the court.

Author's note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: written and distributed only to assist in research while providing a forum for second-level thinking.