3 Stocks to Buy out of the Top-Rated Zacks Diversified Operations Industry

At the moment the Zacks Diversified Operations Industry is in the top 12% of over 250 Zacks industries. This collective group of stocks also represents the Zacks Multi-Sector Conglomerates which is currently the top-rated sector out of 16 Zacks sectors.

Due to their stronger operating environment, these stocks look likely to outperform the broader market over the next 3-6 months. Furthermore, conglomerates are attractive to investors because of their diversity as these companies are typically made up of several independent businesses.

With that being said, here are three Zacks Diversified Operations Industry stocks that currently hold spots on the coveted Zacks Rank #1 (Strong Buy) list.

Carlisle Companies CSL

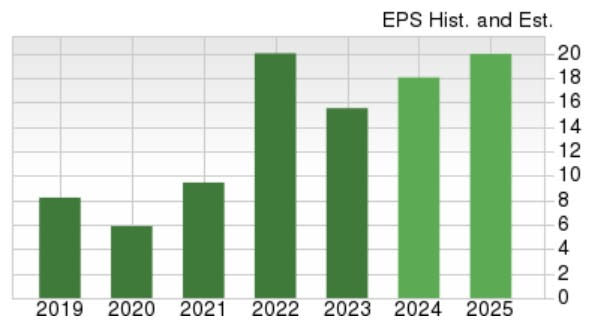

Expansive bottom line growth makes Carlisle Companies stock very attractive with a diversified global portfolio of niche brands and businesses that produce highly engineered products. Primarily used for various building solutions that enable energy efficiency along with waterproofing, Carlisle continues to have a high-profit margin on its products that extend to insulation and roofing in commercial and residential applications.

To that point, fiscal 2024 earnings are now projected to rise 16% to $18.03 per share despite sales forecasted to dip -5% to $4.85 billion. Plus, FY25 EPS is expected to expand another 11% with sales anticipated to rebound and rise 4% to $5.05 billion. Considering its bottom line expansion, Carlisle’s stock trades at a reasonable 18.9X forward earnings multiple. More importantly, over the last 30 days, FY24 and FY25 earnings estimates have risen 5% and 9% respectively.

Image Source: Zacks Investment Research

Griffon GFF

Griffon is another multi-sector conglomerate with diversified operations that extend to home-building products including garage doors and rolling steel doors. Operating primarily in North America, Griffon’s subsidiaries also manufacture branded consumer and professional tools along with residential, industrial, and commercial fans, home storage, and organization products.

Just as compelling as Griffon’s growth is the company’s valuation. Although Griffon’s stock has soared +83% over the last year GFF shares still trade at 14.1X forward earnings. This is a pleasant discount to the industry average of 20.9X forward earnings and the S&P 500’s 21X. Notably, GFF shares also trade below the optimum level of less than 2X sales.

Image Source: Zacks Investment Research

Even better, the strong price performance in Griffon’s stock looks likely to continue as annual earnings are projected to rise 6% this year and forecasted to climb another 24% in FY25 to $5.97 per share. Further alluding to more short-term upside, FY24 and FY25 earnings estimates are nicely up over the last 60 days.