cagkansayin

cagkansayin

By Gene Tannuzzo, CFA, Global Head of Fixed Income

The Fed is going lower, and that’s almost all you need to know about bonds.

For many investors, the top-of-mind questions in the current market are: What is the Fed going to do about rates? And when? We already know the answer to the first question, and we think the answer to the second is mostly irrelevant.

Here’s why.

First, we know the path of rates will be lower because that’s what the Fed has told - and keeps telling - us. Despite better-than-expected growth, a healthy labor market, and thus far resilient capital markets, we need to remember that guidance and trust the Fed’s intention. Rates are going lower. The direction of travel is most important, not every twist and turn along the way. The level of rates also matters, especially as compared to what the Fed views as neutral — which is 2.5%. With the fed funds rate currently above 5%, there is ample cushion to move lower.

Second, the reason for the Fed likely cutting rates will be different from in the past. Historically, the central bank has loosened in response to a demand shock - the global financial crisis and pandemic being prime examples. This time, it's not about demand. It’s about inflation, which has quickly decelerated back toward the Fed’s 2% target. The last year has taught us that we can have lower inflation with growth. We don't have to be bearish on the market or economy to expect lower rates. We just have to know that inflation is going lower.

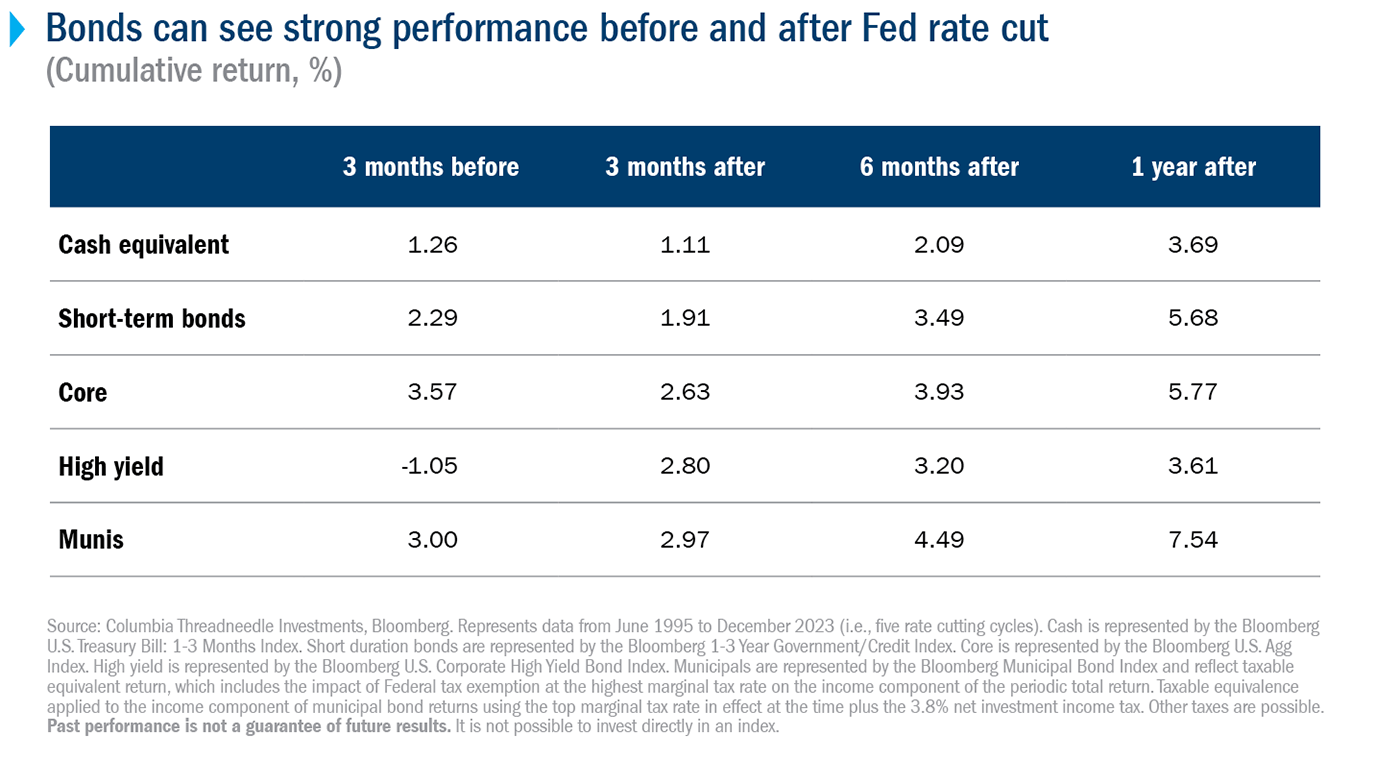

We know that the next move from the Fed is most likely to be a cut. But does the timing matter? History suggests not. Because the market is forward-looking, Treasury yields have historically peaked and begun to move lower ahead of the first cut, and this dynamic has fueled bond market returns both before and well after the Fed begins to ease.

One byproduct of the rapid rise in rates and poor bond market performance over the past few years is a high percentage of cash in investor portfolios.

Cash yields appear optically attractive, but the Fed’s shift away from further hikes diminishes their long-term utility. Falling rates mean reinvestment risk, which cash investors face instantaneously with each cut.

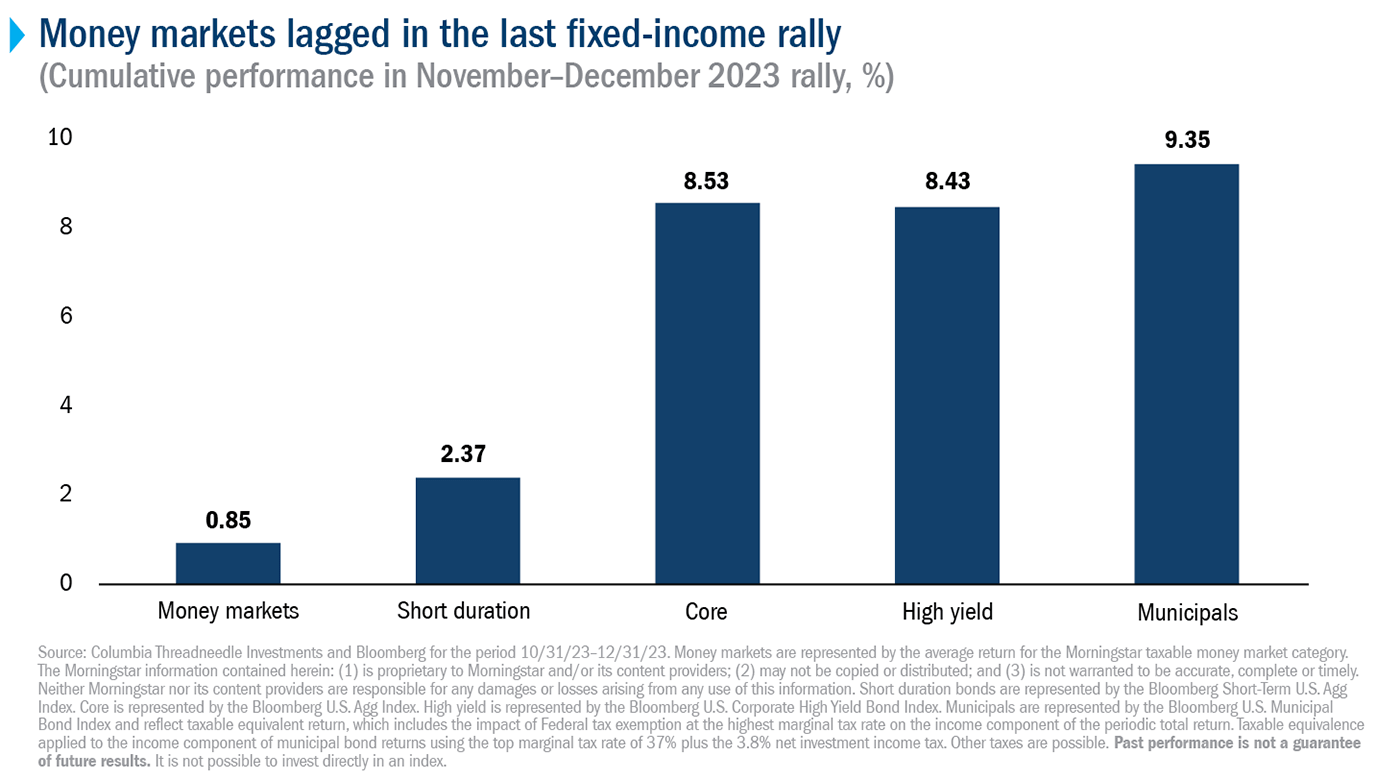

Finally, cash investments don’t offer the potential for price upside as yields decline. The 2023 year-end rally perfectly illustrated this opportunity cost. While cash generated a positive total return, it was meaningfully lower than anywhere else in the bond market.

One of the simplest and most effective ways to redeploy that cash is to move it into short-term bonds. Those investors who aren’t yet comfortable stepping further out the maturity spectrum can still benefit from generationally high yields with short-term bonds. These yields beat those on cash and provide the opportunity to participate in price upside when yields fall further.

Going forward, we think that dispersion within fixed-income sectors will emerge as a key theme. At the aggregate level, risk compensation has become less attractive.

However, notable exceptions persist. For instance, investors can earn a higher risk premium in government-guaranteed agency mortgage-backed securities than in investment-grade corporate bonds.

Within investment grade, capital-rich, high-quality banks offer relative value over cyclical industrial companies, which may underperform in the event of an economic correction.

Similarly, we think high-yield energy companies will experience very different default outcomes and cashflow generation than a leisure and hospitality company in coming years.

Identifying these examples of dispersion plays into our organization’s research capability. We think there is a significant opportunity to uncover yield-enhancing opportunities from the bottom up, with credit ideas that are agnostic to the direction of the Fed and that can work in a number of interest rate and economic scenarios.

After a dismal couple of years, the bond market rebounded dramatically in the last quarter of 2023. Investors may be worried that they missed out on the recovery, but we see a different story.

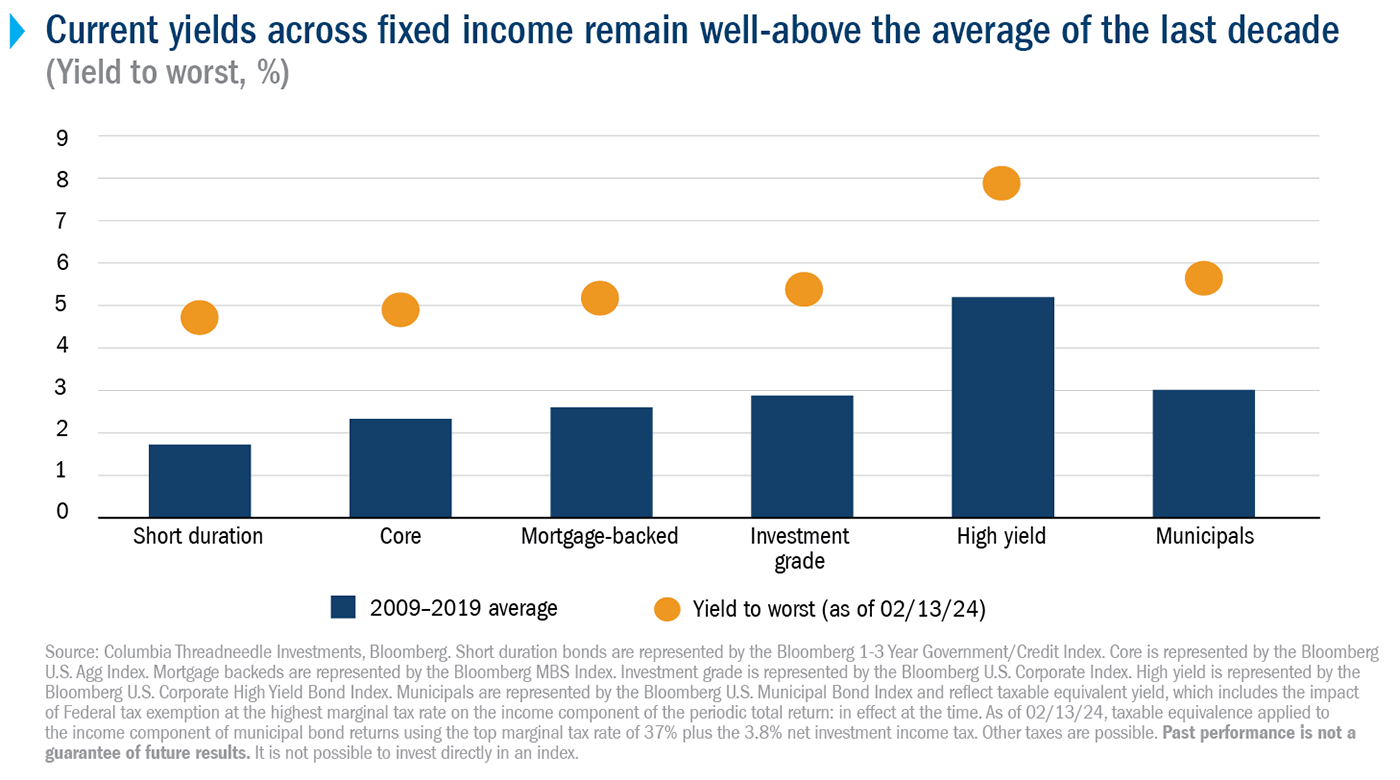

Yields across fixed-income sectors are well above their post-global financial crisis average; Treasury yields remain above 4% across the curve, representing the highest level in nearly two decades.

The Fed has consistently communicated an intention to cut rates before the end of 2024. This, along with declining inflation, should provide a tailwind for fixed-income returns.

And enough dispersion exists to create an environment for security selection to shine. The road has been painful, but today the conditions appear much more favorable for fixed-income investors. The key is getting back into the market.

Disclosure

Use of products, materials and services available through Columbia Threadneedle Investments may be subject to approval by your home office.

© 2016-2024 Columbia Management Investment Advisers, LLC. All rights reserved.

Investors should consider the investment objectives, risks, charges, and expenses of Columbia Seligman Premium Technology Growth Fund carefully before investing. To obtain the Fund's most recent periodic reports and other regulatory filings, contact your financial advisor or download reports here. These reports and other filings can also be found on the Securities and Exchange Commission's EDGAR Database. You should read these reports and other filings carefully before investing.

With respect to mutual funds, ETFs and Tri-Continental Corporation, investors should consider the investment objectives, risks, charges and expenses of a fund carefully before investing. To learn more about this and other important information about each fund, download a free prospectus. The prospectus should be read carefully before investing.

The views expressed are as of the date given, may change as market or other conditions change and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, may not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not take into consideration individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon and risk tolerance. Asset classes described may not be appropriate for all investors. Past performance does not guarantee future results, and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that any forecasts are accurate.

Columbia Funds and Columbia Acorn Funds are distributed by Columbia Management Investment Distributors, Inc., member FINRA. Columbia Funds are managed by Columbia Management Investment Advisers, LLC and Columbia Acorn Funds are managed by Columbia Wanger Asset Management, LLC, a subsidiary of Columbia Management Investment Advisers, LLC. ETFs are distributed by ALPS Distributors, Inc., member FINRA, an unaffiliated entity.

Columbia Threadneedle Investments (Columbia Threadneedle) is the global brand name of the Columbia and Threadneedle group of companies.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.