syahrir maulana

syahrir maulana

I recently (January 18) recommended buying the Vanguard Small-Cap Value Index Fund ETF Shares (NYSEARCA:VBR), basically as a catch-up trade.

The VBR buy recommendation was initiated in January when the Fed was expected to aggressively cut interest rates possibly 6-7 times in 2024, and this monetary policy easing was designed to cancel the lagged effects of the prior monetary policy tightening - and thus, to avoid a recession. The aggressive monetary policy tightening was deemed possible due to the unfolding disinflationary process, and seemingly a sustainable return to the 2% inflation target.

Here is the initial bullish thesis:

This investment thesis heavily depends on the Fed's aggressive removal of the monetary policy restriction.

The Fed is likely to start cutting interest rates, probably in May, even though the market wants to see the cut at the March meeting. So, the timing of interest rate cuts is causing some volatility. The disinflationary process is likely to continue, as the leading indicator (the New Tenant Rent) for the shelter inflation has returned to the pre-pandemic levels, and this is important given that shelter inflation is responsible 60-70% of total inflationary spike.

Thus, assuming that the Fed follows through on the signaled interest rate normalization policy, small stocks should outperform over the near term.

Furthermore, the small cap value stocks were deeply undervalued, relative to large cap stocks, and also relative to growth stocks. The S&P Small Cap 600 Index was trading at 13.6 forward PE ratio for 2024, while the S&P 500 (SP500) was trading at forward PE ratio 22.

In addition, the earnings for the S&P Small Cap 600 Index were expected to grow at 28% in 2024, much higher relative to the S&P 500 earnings growth expectations at 10.4% for 2024.

Thus, back in January the economy was expected to avoid a recession due to the Fed's aggressive dovish turn, and the small cap value stocks were cheap with significant earnings growth expectations. Given that the small cap value stocks underperformed the S&P 500 in 2023, it seemed like the small cap catch-up trade was appropriate.

First, the expectations for the monetary policy easing were significantly reduced from 6-7 cuts for 2024 in January to currently only 2-3 cuts.

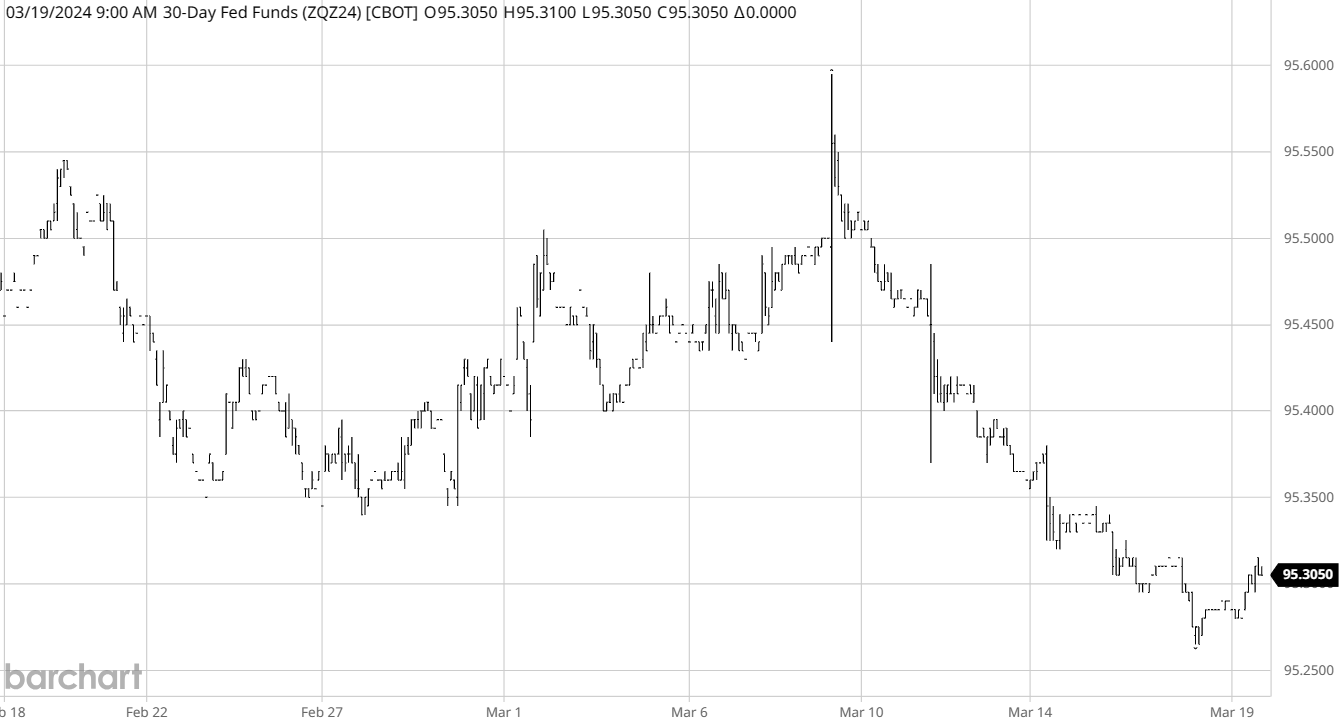

Here is the chart of the December 2024 Federal Funds futures, showing a gradual decline from January, which means higher interest rate expectations for December 2024, currently at 4.7% (above the Fed's 4.6% December dot-plot target).

December FF (Barchart)

Apparently, the Fed's dovish pivot in December was premature. As a result, the financial conditions eased significantly, which boosted the inflationary pressures. The core CPI increased by 0.4% in January and February, and while the annual core CPI has continued to fall, the quarterly annualized core CPI has been rising, currently above the 4% level at 4.16%.

As a result, the Fed is unlikely to cut interest rates in May or June, and there is a strong possibility that if the Fed does not cut in June, the first cut could be delayed to November after the US election.

The delayed "normalization" is increasing the probability of a recession - as those lagging effects of the prior monetary policy tightening are more likely to affect consumption and investment. Thus, the first Fed cut could be in response to rising unemployment - and a recession.

As a result, the initial bullish outlook for small cap stocks based on the macro environment has changed to a more negative outlook - as the probability of recession has increased.

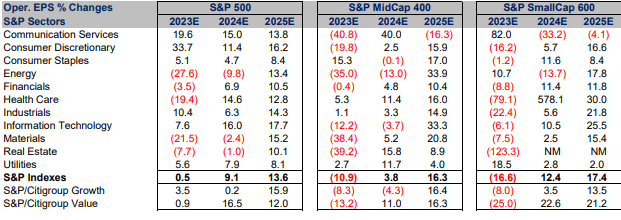

Furthermore, the earnings expectations have been downgraded significantly over the last two months. The earnings expectations for small cap value stocks have been downgraded from 28% in 2024 to 22%, while the earnings expectations for the S&P 500 have been downgraded to 9.1% from 10.4%. These earnings expectations downgrades still don't assume a recession in 2024/2025, thus, further earnings growth downgrades are likely as the economy slows down on a path to a possible recession.

Earnings expectations (CFRA)

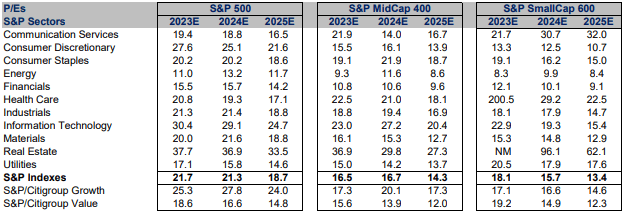

In addition, the PE ratio for the S&P Small Cap Value Index has increased from 13.6 to 14.9, so the value proposition is now less compelling.

PE ratios (CFRA)

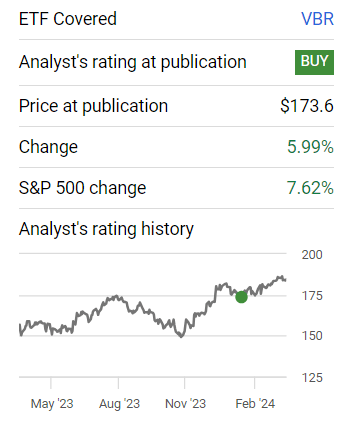

Since the initial recommendation, the small cap value ETF VBR is up by 5.99%, but the S&P 500 is up by 7.62%. Thus, the small cap value catch-up trade remains elusive - the large cap stocks dominated by the Mag 7 (or whatever is left, possibly only Nvidia (NVDA) and Meta (META)) continue to outperform small cap stocks.

Since Jan 18th (Seeking Alpha)

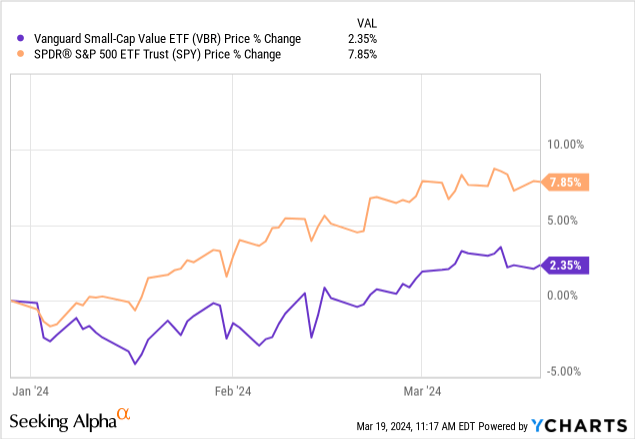

Looking at YTD performance in 2024, small cap value stocks are barely up by 2.35%, while the S&P 500 is up by 7.85%. Thus, the catch-up trade is not really happening.

Thus, based on the developments over the last two months I no longer recommend buying the small cap value ETF VBR and I'm downgrading it now from Buy to Hold.

More important for small cap stocks (IWM) in general is the fact that the there is an approaching maturity wall. Small cap stocks in general are less profitable, (most are unprofitable), and overleveraged. Many of these small cap companies will have to refinance their debt in 2025 at much higher interest rates. As a result, I expect a wave of defaults and bankruptcies as the maturity wall approaches. Thus, I am actually leaning to a Sell rating for VBR, as the macro situation unfolds.

The small cap value ETF VBR is cyclical, thus, it underperforms if the market expects an imminent US recession. Industrials and financials account for around 20%, consumer cyclicals for around 14%, real estate for around 10% of the index. Technology is only around 7% of the total holdings.

The earlier expectations of the aggressive Fed easing opened up the possibility of a "soft-landing" which would favor a rotation to value and cyclical small cap stocks. However, the macro environment changed, sticky inflation may not allow the Fed to engineer a soft-landing, thus a recession is more likely, which does not favor a rotation to value or small cap stocks.

The risk to the outlook is the possibility that the Fed ignores the inflationary data and continues with the dovish pivot - in which case the speculative tech stocks (QQQ) would likely continue to outperform as the bubble continues to inflate - still not the case for the catch-up trade in small cap value stocks.