niphon/iStock via Getty Images

niphon/iStock via Getty Images

Investment thesis: Energy Fuels (NYSE:UUUU) is emerging as a strategic mining company within the current global geopolitical situation. It is involved in uranium mining, which is set to play an increasingly pivotal role in the global energy mix since hydrocarbon energy is increasingly seen as undesirable. It also plans a significant expansion of its rare earth minerals production. China is seen as having an uncomfortably strong position of dominance in terms of global production of these materials, without which many electronics, green energy technologies, as well as EVs, cannot be built. With both segments of its mining activities looking robust for the foreseeable future, Energy Fuels is an intriguing investment opportunity, even though its recent financial reports are less than solid. I decided to pick up a small position in this stock, with the intent to add if it goes down further this year and next. I expect things will be looking up for this company within two years at most, assuming execution will match the external opportunities that global trends are offering.

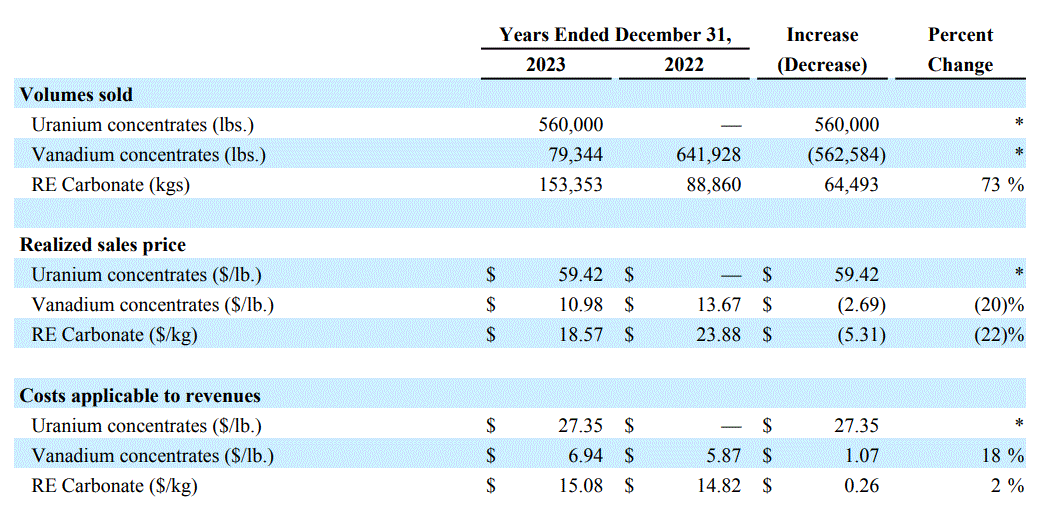

For 2023 Energy Fuels had an operating loss of $34.4 million, which was a significant improvement on the loss of just under $45 million in 2022. One of the factors that led to the improvement was the revenues realized as a result of the sale of $32.3 million worth of uranium concentrate. Energy Fuels did post net earnings of $99.8 million, thanks mostly to the sale of $119.3 million in assets for the year.

While it did start selling uranium concentrate, it also reduced its vanadium sales significantly.

Energy Fuels

It should be noted that Energy Fuels incurred standby costs associated with the care of idled mines of just under $7.5 million for 2023. As mines are brought back into production, those costs should decline while revenues increase. As this happens, operating losses should start to narrow and perhaps turn into operating profits, with some help from external factors, such as an improving market for uranium and other minerals.

Trading Economics

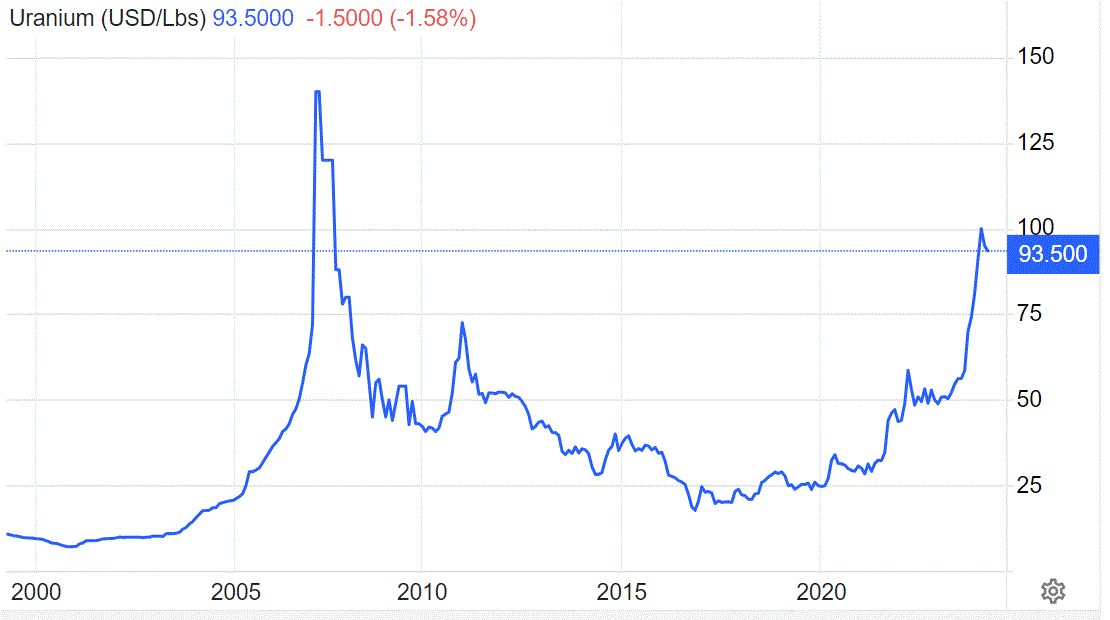

As we can see, Energy Fuels sold uranium for about 2/3 of the spot price last year. Assuming that the uranium market remains bullish this year, Energy Fuels could potentially see higher uranium sale volumes as it reopens mines, and it could also see a higher realized price on those volumes sold. It could be enough to make it profitable as early as within a few quarters.

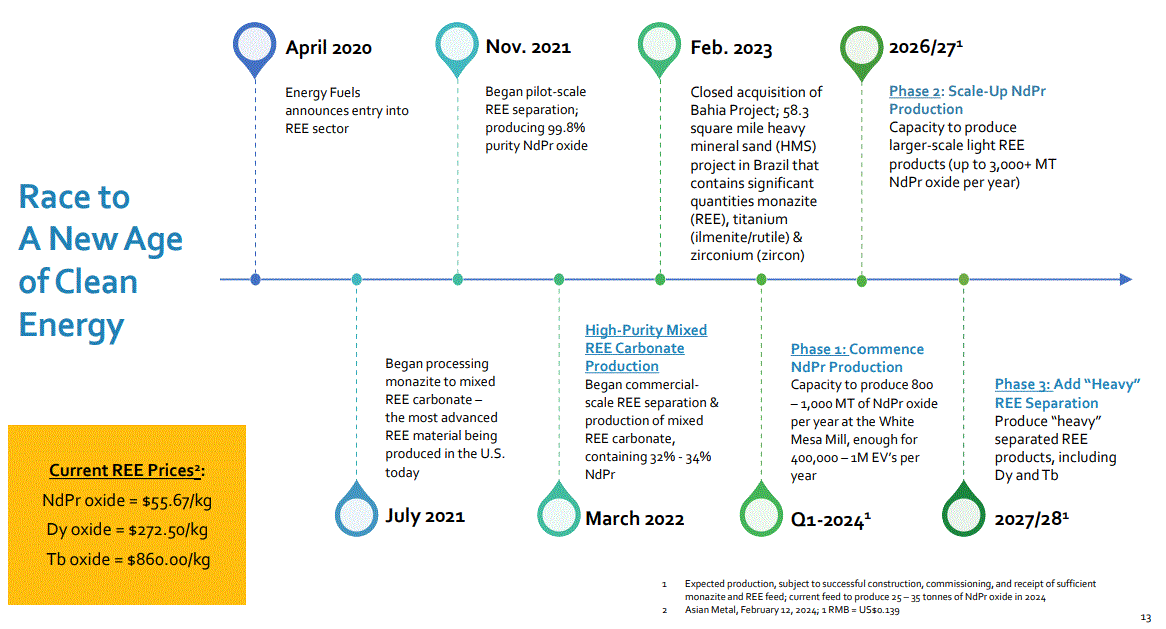

Energy Fuels is planning several production expansion initiatives in the next few years in both uranium mining as well as rare earth mining & processing. For the uranium segment, it intends to expand production volumes to a yearly output of 1.1-1.4 million pounds by the end of this year, which is double or more compared with its 2023 sales volume.

Its rare earth mineral production plans aim to move into what is likely to become a booming mining sector as a desire to reduce the world's dependence on China leads to stimulus funds for this sector. It is not yet clear how much financial or other support Energy Fuels is set to receive from government initiatives meant to secure a robust domestic supply chain for rare earth minerals. In my view, even if it does not translate into direct grants, there will be some potentially beneficial measures in place that will benefit Energy Fuels, such as mandating domestic content, as we saw with the Build Back Better plan.

Energy Fuels

The world is in the midst of a major technological shift, in terms of how we provide energy, transport as well as other related needs. Many major economies are seeking a complete phasing out of coal as an energy source while increasing renewable wind & solar energy production. With some early real-life indications in place that exposed some of the dangers associated with economies becoming over-reliant on intermittent electricity sources, nuclear power is seeing renewed interest.

The push to reduce global oil demand growth by encouraging the adoption of EVs is a strong driver for uranium since more electricity is needed to accommodate EV demand for electricity. The official reasons provided for the pro-EV policies are environmental. In this regard, I do believe that it is in part also due to fears of global oil supply growth constraints, as I pointed out in recent articles. In other words, EVs have become an integral part of the global effort to reduce oil demand growth as a means to preserve our ability to grow the global economy. This benefits Energy Fuels both on the uranium side of the business given that it drives electricity demand higher, as well as its rare earth minerals business, given that EVs use a lot of rare earth mineral inputs.

If the geopolitical situation were closer to the way things were about a decade ago, the economic developments that favor both uranium and rare earth metals might not necessarily provide Energy Fuels with a significant boost. After all, Chinese companies might be better positioned to increase rare earth production, while Kazakh or Nigerien uranium supplies would ordinarily fill excess uranium demand. Within the current trend of re-shoring industries especially industries that are deemed strategic, Energy Fuels could potentially see an outsized benefit from being positioned as one of the mining companies that can meet at least a part of the rising domestic demand for these minerals.

As is often the case in the business world, timing can be everything. Energy Fuels has the resources to expand into the right mined products at the right time. It has the resources to increase the production of uranium and sustain it for many years to come.

Energy Fuels

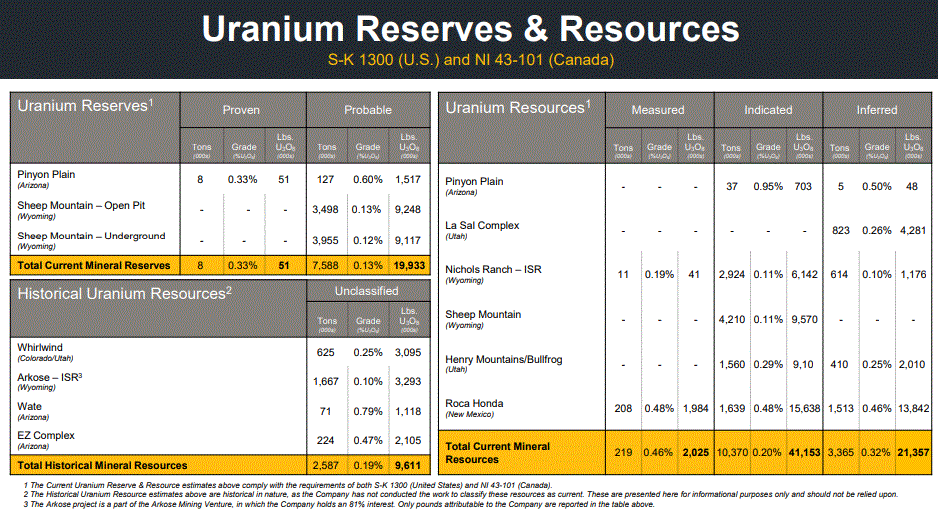

At a rate of 1.4 million pounds/year which is the current goal for production, its proven & probable resources would last about 14 years, while some of the additional resources could be upgraded. It remains to be seen however just how profitable the extraction of uranium will be for the company. Even within the context of the currently favorable market conditions, certain resources may fail to materialize as profitable assets. We will only know in hindsight once the resources are produced because in my experience prior estimates of cost do not always pan out.

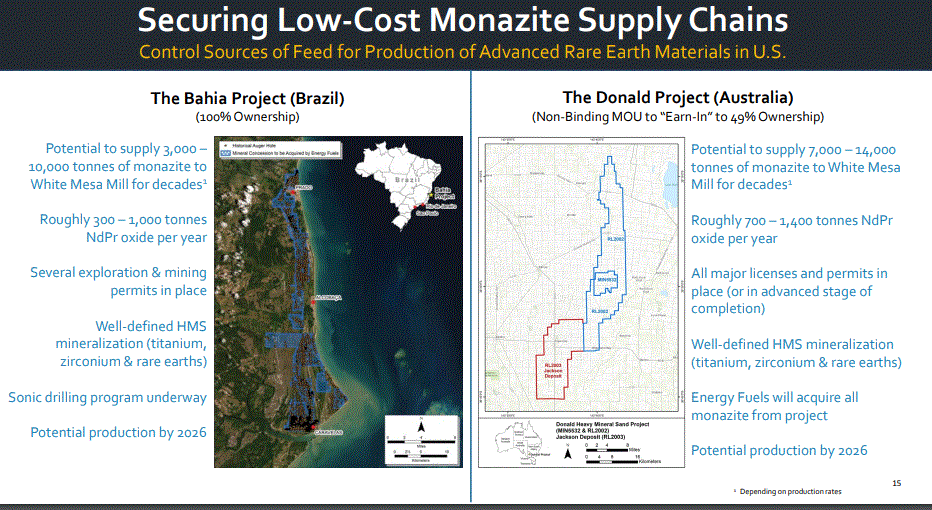

The rare earth segment of the company is likely to be an even bigger wildcard, given all the unknowns associated with how projects like the Bahia project in Brazil, or its Australian project will work out.

Energy Fuels

The target date for commencing production for both monazite projects is 2026, which may or may not happen. The expected volume of production also ranges from 10,000 tonnes/year to 24,000 tonnes/year. Just to provide some perspective in terms of probable revenues, the spot price in the past few years was reported by various sources as being anywhere between $750-$7,000/tonne depending on the quality and other factors. In other words, monazite revenues could come in at anywhere between about $7 million/year to about $170 million, depending on production volumes, the quality of those volumes as well as prevailing market prices.

Given that Energy Fuels is currently taking operating losses, there is a risk of its stock trading down significantly from current levels, especially if some bad news, such as delays to production ramp-up happens. For this reason, I am investing rather cautiously at the moment. This stock currently makes up about 0.75% of my total stock portfolio, and I am willing to increase my position if there is a further 20%-30% decline in the stock price.

My reasoning behind assuming that there is some significant potential upside to this stock is based on a comparative analysis of near-peers. For instance, Cameco (CCJ), with revenues of almost $2.6 billion for 2023, currently trades at a market cap of $17.3 billion, which is about 6.5 times its revenues. Energy Fuels could potentially increase its revenues from $38 million in 2023 to as much as about $250 million based on the production plans I highlighted and assuming the best-case scenario in terms of market pricing of its minerals. Its market cap is currently under $1 billion. Comparatively speaking, Energy Fuels could have a roughly 50% upside from current levels in terms of market cap, assuming that it will trade similarly to industry peers in terms of valuations. If its stock and market cap decline further from current levels, those valuation measures will become even more attractive in terms of potential upside for its stock, which is why I am looking to buy more on the dip.