Andrew Toth/FilmMagic via Getty Images

Andrew Toth/FilmMagic via Getty Images

Co-authored with "Hidden Opportunities"

Steve Eisman, the Managing Director of Neuberger Berman, rose to fame after his successful foresight into the 2007-2008 U.S. housing crisis. Steve Carell portrayed his exploits in profiting from the bubble in "The Big Short" movie. In a recent interview, Mr. Eisman said that market spectators came into 2024 with a bullish outlook and expectations of several rate cuts from the Federal Reserve.

Mr. Eisman believes that the Federal Reserve will be motivated to tread cautiously regarding rate cuts, as they would not want to make premature moves to give birth to an even more difficult-to-control comeback of inflation.

"The Fed is still petrified of making the mistake that [former Fed Chief Paul] Volcker made in the early '80s where he stopped raising rates, and inflation got out of control again. If I'm the Fed and I'm looking at the Volcker lesson, I say to myself 'What's my rush?'" - Steve Eisman

The Big Short investor is bullish on sectors benefiting big from the $1.2 trillion government dollars that will be spent over the next ten years. He expects construction firms, industrials, materials, and utilities to experience federal infrastructure spending as a major growth tailwind in the coming years.

"This is the first industrial policy in the U.S. we've seen in several decades. The money isn't spent yet-it's the government, it doesn't take a week. There has been no revenue impact at this point, and I don't think most of the spending has been embedded in any stocks." - Steve Eisman

Notably, almost 17% of Neuberger Berman's portfolio comprises materials, utilities, energy, and telecom names, among the biggest beneficiaries of the Infrastructure Law. Let us now review two time-tested CEFs to draw big monthly distributions from the historic capital infusion into the American infrastructure.

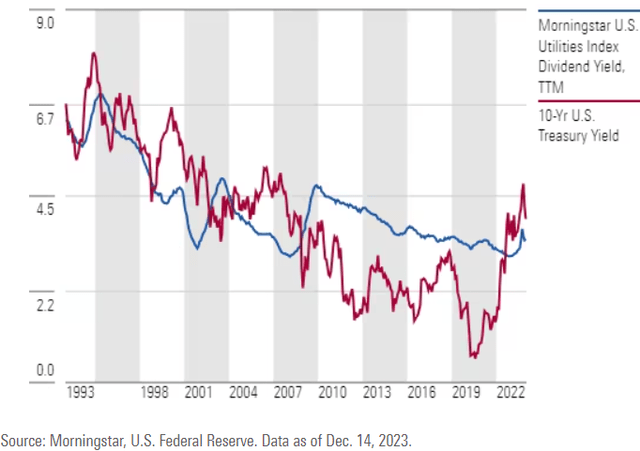

Utilities in North America often operate in regulated markets where they maintain a monopoly over the provision of essential services like water, electricity, and gas. Moreover, this is a unique industry that can, through regulatory backing, charge more for the same product without losing customers.

According to S&P Global Market Intelligence, there are currently 63 electric and 52 gas rate cases pending in 37 states. It is expected that the outcome of these decisions carry a collective $23.7 billion in consumer rate increases nationwide.

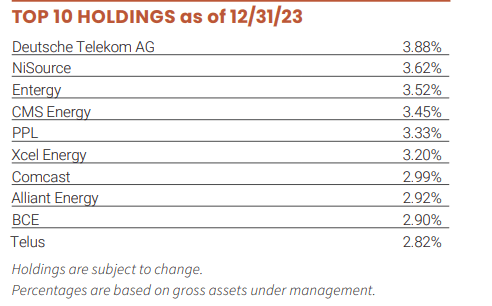

Let's take a look at the top holdings of Reaves Utility Income Fund (UTG), which constitute ~33% of the CEF assets.

UTG Fact Sheet

NiSource will be pursuing a multi-step process to spread out the changes to customer bills beginning in August 2023, with the remaining changes applied in 2024. The Indiana Utility Regulatory Commission's decision would result in a 10% increase in monthly bills for consumers.

Entergy is seeking $173 million over a three-year term beginning in September 2024, reflecting an approximate 5% increase on a typical customer's bill. This comes less than a year after the company added a $1.5 billion storm recovery fee. Entergy has been known to pass on grid hardening costs to consumers.

CMS Energy recently received approval from Michigan Public Service Commission, permitting a $95 million rate increase for natural gas customers, reflecting a 4.2% increase in monthly bills.

Public Utilities Commission approved a rate hike last year, and Rhode Island customers of PPL Corp are seeing their monthly utility bill jump by an average $32.29 (a whopping 24% YoY increase)

Xcel Energy is seeking permission from the Colorado Public Utilities Commission to hike its natural gas base rate by $171 million, reflecting a 9.5% increase for the next winter.

Alliant Energy is requesting the Iowa Utilities Board to adjust electric and natural gas rates, beginning in late 2024. The requested adjustments reflect a 7.7% (approximately $10 per month) increase to the average residential electric customer's total bill beginning in October 2024 and a second phase increase of 5.7% (approximately $7 per month) to take effect beginning in October 2025.

These are just a few notable mentions of rate hikes being pursued by UTG's top holdings. The fund comprises 60 holdings, with 73% exposure to utilities companies. Utilities currently sport decades-high yield levels amidst decade-high interest rates. Hence, the sector is well-positioned to rebound strongly with interest rate cuts. Source

Morningstar

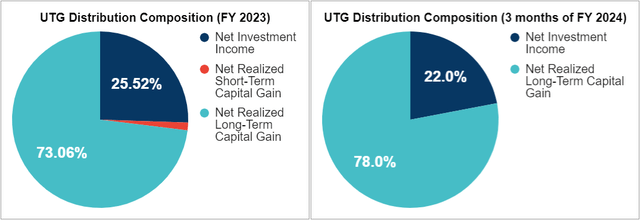

UTG is actively managed, with a high proportion of its distributions sourced from long-term capital gains.

Author's Calculations

UTG itself operates with leverage, representing ~21.4% of the fund's assets. The fund has $520 million in borrowings from its credit arrangement at an interest rate of 1-month SOFR + 0.65%. As such, we expect rate cuts to immediately reduce borrowing costs for UTG.

Utility firms are executing their growth plans and successfully passing on costs to the consumer. The fundamentals of quality companies in the industry remain strong, and UTG provides a monthly income opportunity to ride this defensive sector.

2024 marks the third year since the Infrastructure Law was enacted, and the U.S. Department of Transportation's FHWA (Federal Highway Administration) has allotted $61 billion in FY 2024 apportionments for 12 programs supporting investment in roads, bridges, and tunnels, carbon emission reduction, and safety improvements. The year also marks the year that megaprojects, like the Gateway Hudson Tunnel project, the high-speed Brightline West train, and the Brent Spence Bridge, are expected to put shovels in the ground.

Similarly, the Inflation Reduction and CHIPS Act will continue to boost domestic manufacturing and onshoring efforts, and exports project double-digit growth in multi-family housing, hotels, motels, and manufacturing facilities.

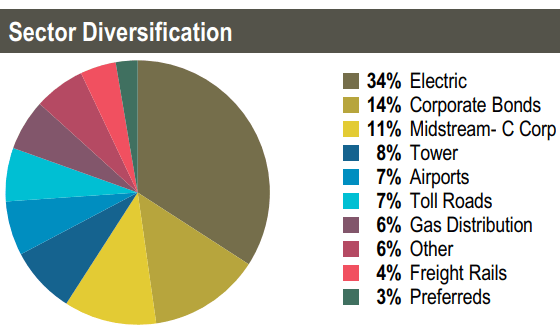

Many exciting projects are underway for 2024 and beyond, billions of dollars that will flow into the income statements of companies in the sector. Cohen & Steers Infrastructure Fund (UTF) is a CEF heavily diversified across 244 holdings, primarily in global infrastructure companies - electric utilities, midstream c-corps, airports, towers, etc., giving excellent exposure to this sector with strong cash inflows. Source

UTF Fact Sheet

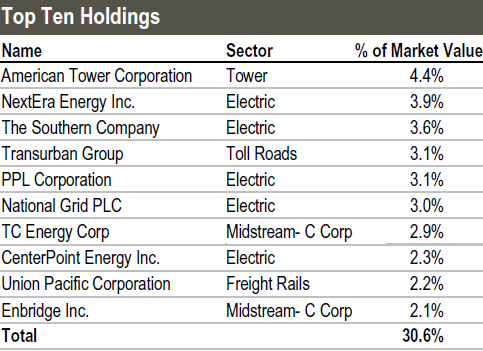

UTF's top holdings represent ~30% of the fund and are among their respective sectors' most established and defensive names. If you live in the United States, you will likely pay for recurring services, directly or indirectly, to at least one of these ten companies monthly.

UTF Fact Sheet

UTF's portfolio comprises 84% common and 16% preferred stocks, and the CEF operates with a 31% leverage, which carries a 2.5% weighted average interest rate. You will never be able to leverage your portfolio at these rates in the current market. This leverage will boost returns as billions in federal funding make their way into the holding company's income statements.

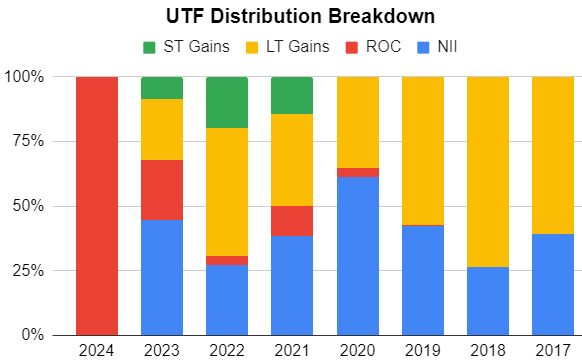

85% of UTF's leverage carries a fixed 1.8% rate with a weighted average term of 2.5 years, which is enough to ride out this rate cycle and refinance on better terms. The CEF issues a monthly distribution with a healthy mix of Net Investment Income, capital gains, and ROC, as seen from the composition in recent years.

Author's Calculations

UTF's $0.1550/share monthly distribution calculates to an 8.6% annualized yield. This CEF presents an attractive entry point as it trades almost at par with NAV, providing much-needed exposure to the critical industries for the American economy.

Our Investing Group doesn't just talk the talk; we walk the walk when it comes to prioritizing current income and navigating the unpredictable terrain of the financial markets with a rate-agnostic portfolio. We're not fearful of interest rate fluctuations; we embrace this with a strategic blend of fixed-income assets featuring high fixed or floating-rate coupons and equity positions across resilient sectors; our cash flow is positioned to thrive amidst economic uncertainty.

UTG and UTF stand tall in our arsenal of investments from resilient sectors, delivering steady monthly distributions to fuel our financial goals. Our "model portfolio" has over 45 carefully selected picks to maintain a growing income stream regardless of what the Fed decides.

So, as Steve Eisman sounds the alarm on Wall Street's unrealistic expectations around interest rates, we ask: Are you as prepared as we are?