z1b

z1b

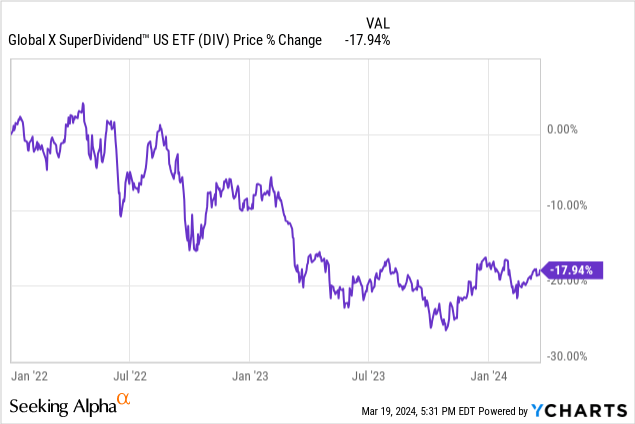

High-yield stocks (DIV) have been taking a beating in recent years due to soaring interest rates:

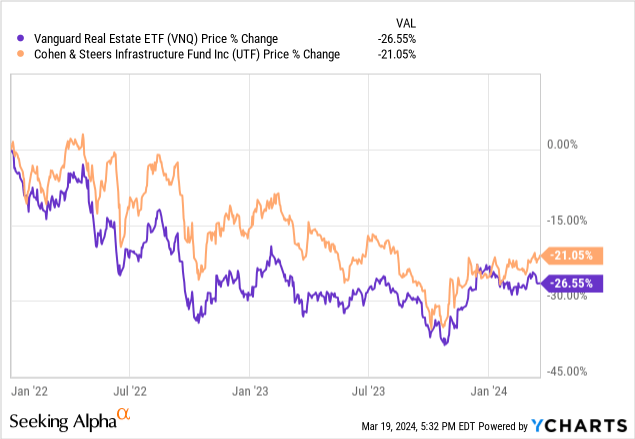

This pullback has been particularly pronounced in sectors like REITs (VNQ) and utilities and infrastructure (UTF):

That being said, there are numerous opportunities in these sectors that offer lucrative 6-10% yields. Not only that, but these yields are well-covered by cash flows, are growing year after year, and have very defensive business models, investment-grade balance sheets, and solid management teams underpinning them. As a result, they offer compelling opportunities for retirees to load up on these relatively low-risk income-generating machines to boost their passive income stream.

In this article, we will take a look at two REITs and two infrastructure businesses that we think are very attractive buys on the dip:

As we laid out in a recent article on REITs, the sector is very opportunistic right now as they generally trade at very deep discounts to NAV, are attracting significant interest from leading asset managers like Blackstone (BX) who are buying REITs very aggressively and view them as being a "generational opportunity," and are likely to benefit from the significant capital that is currently on the sidelines in money market funds and waiting for interest rates to drop before re-entering yield assets like REITs.

Two REITs that currently trade at discounts to NAV, have strong credit ratings, own high quality and well-diversified portfolios of real estate, are very defensively positioned, have solid management teams and good long-term track records, while offering 6%+ dividend yields are Realty Income (O) and W.P. Carey (WPC).

O has been facing challenges with keeping its growth momentum going given how large they have become and therefore have had to invest heavily in very large acquisitions and even move into additional property areas where they lack expertise. That being said, they still have a very strong balance sheet, their portfolio is exceptionally well-diversified, and - with a 6% dividend yield and a 7% discount to NAV - they do not need to grow by more than 2-4% per year to still generate a low-risk double-digit annualized total return moving forward. Moreover, for retirees simply looking for reliable and attractive passive income that keeps pace with inflation over the long-term, a 6% current yield backed by broadly diversified and professionally managed triple net lease real estate that will likely grow at around a 3% CAGR over the long-term is a great deal.

WPC, meanwhile, offers a similarly attractive proposition as O, only with a little bit more spice. First of all, it has substantial exposure to Europe along with the U.S. This brings with it likely a bit more geopolitical risk given the war in Ukraine at the moment as well as the weaker overall economic environment in Europe right now. At the same time, it gives WPC more markets to invest in as well as access to both Euro and USD debt markets in order to optimize its cost of capital.

Furthermore, WPC - while it has a little bit lower of a credit rating than O - has significantly greater exposure to industrial real estate, which tends to grow and also tends to command a valuation premium to the retail real estate that O focuses on. Despite that, WPC trades at the same discount to NAV as O does and offers a 20 basis point higher dividend yield than O does.

Last, but not least, WPC has significant exposure to CPI-linked rent escalators, which make it a more resistant REIT to the threat of periods of runaway inflation. As a result, retirees who want to sleep well at night over fear of inflation re-escalating and eating up their retirement income stream's purchasing power, yet still want the cash flow stability provided by triple net lease real estate may want to consider WPC over O, despite O having a more impressive long-term dividend growth track record than WPC.

Infrastructure is another sector that is very opportunistically priced at the moment and is attracting significant interest from billionaire investors and leading alternative asset managers like BX, BlackRock (BLK), and Brookfield (BAM)(BN). A big reason for this is that the sector is expected to have tens of trillions of investment dollars pouring into it in the coming decades as give major macro trends (aging demographics in developed economies, rapid economic development and redevelopment needed across the globe, digitalization in the wake of the fourth industrial revolution, deglobalization due to the rising tensions between the US and China, and the decarbonization of the global energy supply chain)

Two infrastructure picks that we think have been unfairly beaten down by Mr. Market recently that offer very lucrative yields are Brookfield Infrastructure Partners (BIP)(BIPC) and Atlantica Sustainable Infrastructure (AY).

BIP has a BBB+ credit rating, a very impressive dividend growth track record, and has delivered market-crushing total returns over the long term. Moreover, its global scale, support from the world's second-largest alternative asset manager (Brookfield), and investment themes are deliberately positioned to benefit from the aforementioned five major macro trends.

While Mr. Market has beaten down its stock price mercilessly over the past year due to concerns about rising interest rates, the company has continued to deliver robust growth numbers. In 2023, FFO per unit grew by 9%, it grew its distribution for the 15th consecutive year with a 6% hike, and its balance sheet remained in excellent shape, with 90% fixed rate debt, an average term to maturity of seven years, only 5% of debt maturing over the next 12 months, and $2.8 billion of available liquidity.

With an expected next twelve-month distribution yield of nearly 6%, expected distribution growth of about the same amount, underlying FFO per unit growth expected to come in the high-single digits, and some of the world's most skilled infrastructure investors and operators running the business and allocating its capital, BIP is one of the most compelling dividend growth stocks available in the market right now.

Meanwhile, AY is a conservatively run renewable power infrastructure business that has a solid balance sheet with relatively low corporate-level debt, regular project-level amortization with all project-level debt scheduled to be paid off by the end of its power purchase agreements, a 13-year weighted average life remaining on its power purchase agreements (mostly to investment grade counterparties), and a robust growth pipeline.

The most compelling aspect of AY, however, is its valuation. Its next twelve-month dividend yield is a whopping 10.4% and is fully covered by cash available for distribution. Meanwhile, its EV/EBITDA multiple of 8.8x is well below that of its peers (for example, NextEra Energy Partners (NEP) which is also a very beaten-down stock trades at a 9.6x EV/EBITDA multiple and Clearway Energy (CWEN) trades at an 11.4x EV/EBITDA).

On top of that, AY is likely to continue growing its CAFD per share at a low to mid-single-digit CAGR under its current growth strategy and could also extract additional value for shareholders depending on the outcome of its current strategic review. Its largest shareholder - Algonquin Power & Utilities (AQN) - holds several board seats at AY and is currently focused on working with AY to maximize the value of its holding in the company. As a result, a partial or complete sale of AY in the near future is entirely possible and would very likely lead to material upside in the share price from current levels.

While the market continues to beat down high-yield stocks like REITs and infrastructure businesses, these companies continue to increase their cash flow and dividends per share while maintaining strong balance sheets and long-term growth prospects.

As a result, income-focused investors now have a compelling opportunity to buy the dip and increase their income streams while also locking in very attractive long-term total return potential. That is why the more these stocks drop, the more I buy them.