fcafotodigital

fcafotodigital

Following my coverage of US Foods Holding (NYSE:USFD) in Mar'23, for which I recommended a hold rating as I wanted to monitor how USFD executes in the tough macro environment (high rates and sticky inflation), this post is to provide an update on my thoughts on the business and stock. Since my last post, USFD has showed great execution, as seen from its growth vs consensus expectations and unit economics, which led to a strong rally in share price to the current ~$51/share. I am upgrading my rating to buy as management showed that they can execute at a high level, and the underlying demand appears to be healthy as well. Notably, I expect margins to continue improving from here, which should lead to EBITDA growing faster than revenue for the near-to-medium term.

USFD 4Q23 (released on 15 Feb 24) showed that they are able to execute at a high level despite the macro conditions. 4Q23 revenue of $8.94 billion beat consensus expectations for $8.82 billion, driven by robust case growth of 4.3%. My key takeaways from the quarter that are relevant to my thesis are that: (1) The strong case growth was supported by organic growth across key areas; and (2) unit economics have trended really well, suggesting strong execution in expanding margins. Notably, gross profit per case (GP/case) outpaced operating cost per case (OPEX/case), leading to EBITDA of $388 million (beating consensus) and EPS of $0.64.

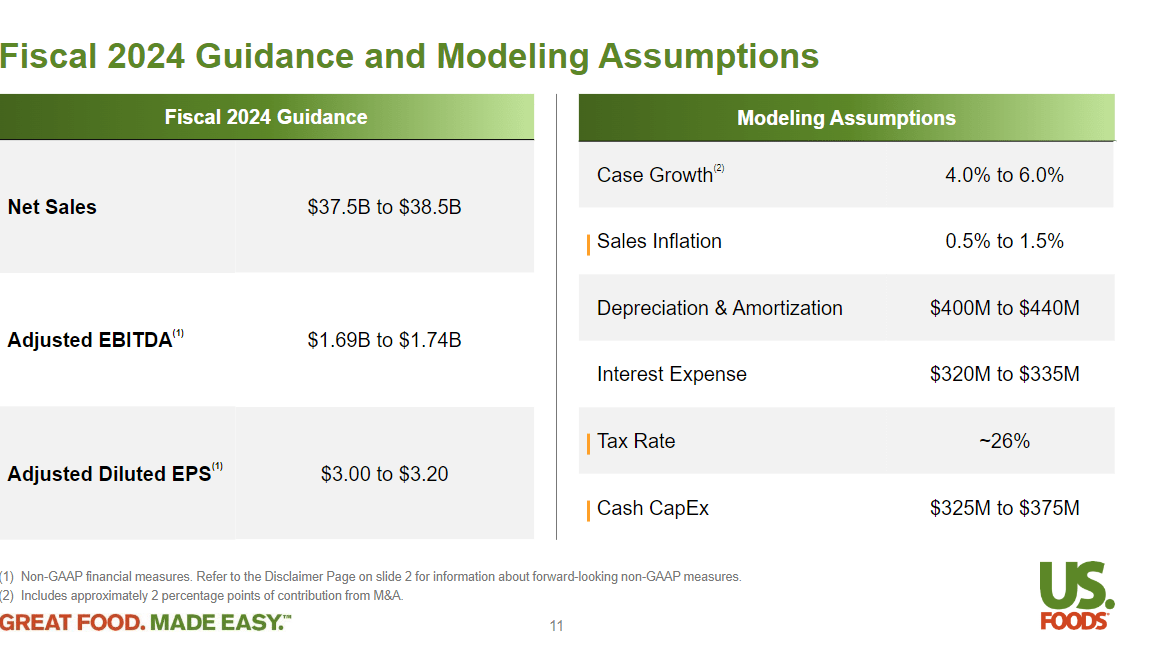

Although I have missed out on the recent rally from ~$40 (my last update) to the current $50, I believe investing today (with better evidence of strong execution) is safer, and I still see upside from the current level. I expect fundamentals to continue improving as the case growth of 5.6% was driven by strength across customer types: independent restaurant cases grew 6.3%; healthcare grew 8.1%; hospitality grew 5%; even chain volumes turned positive, coming in at 0.8% after being negative for a couple of quarters. In the near term (1Q24), volume performance will be a little weak, but it should not be a concern as it was mainly related to the union-related labor disruptions, which are now done and dusted. Importantly, volumes have trended better since January. Also, note that USFD closed Saladino's acquisition in 4Q23, which, combined with the acquisition of IWC Food Service (whose business has $200 million in annual revenue) that is expected to close in 2Q24, will further help support topline growth in FY24. These inorganic contributions are expected to be 200bps, which means management is guiding for 2 to 4% of organic growth in FY24. I believe the hurdle is not high to meet as the historical 4Q23 exited with 3.6% in organic growth (on top of 11.5% in 4Q22 organic growth), which suggests that the underlying demand strength is healthy. In addition, historically, USFD has grown organic growth on average at ~4%, so this guide is suggesting USFD will underperform historical rates, suggesting that the guide was not aggressive.

Own calculation

Moving down the P&L, management is guiding for adj. EBITDA growth of ~9%, higher than the top line, indicating margin expansion. Based on how unit economics have trended, I believe this guide is not far-fetched as well. Investments in initiatives to increase productivity, decrease the cost of goods sold, and optimize prices started to pay off in the second half of 2023 and should keep doing so all the way into 2024. Based on my read-on management comments, although supply chain productivity has improved, there appears to still be plenty of room to improve. For instance, optimizing distribution footprints to improve efficiency, which I think USFD can drive margin improvement from here, is something that they have already successfully achieved in other regions (they noted that due to supply chain initiatives, they drove a 5% improvement in both delivery and warehouse productivity).

I was pleased with the progress that we made in the back half of the year, however, I think largely that portion of our improvement has still lagged the other two areas, and so I see the greatest opportunity for productivity gains largely coming out of the supply chain.

And IWC in particular, I didn't say this on the call, but we're serving that market today, but we're coming from through two other distribution centers that are probably three hours away from the market. So we're not getting there very efficiently. 4Q23 earnings results call

If we take a step back and move up from the EBITDA line to the gross profit line, there is also plenty of room for gross margin expansion. To give a sense of the magnitude, the USFD FY23 cost of goods sold is ~$30 billion. If USFD can just save 0.5% from this, it equates to $150 million, or 10% of adj. EBITDA. As such, I am very positive about the recent strategic vendor management initiatives, which address ~60% of the COGS (potential for more gains if USFD can find a way to address the remaining 40%).

We addressed approximately 60% of COGS last year, and continue to look for additional cost savings in 2024 as we deliver on the remaining 40% of our vendor spend that has not yet been addressed. 4Q23 earnings results call

Own calculation

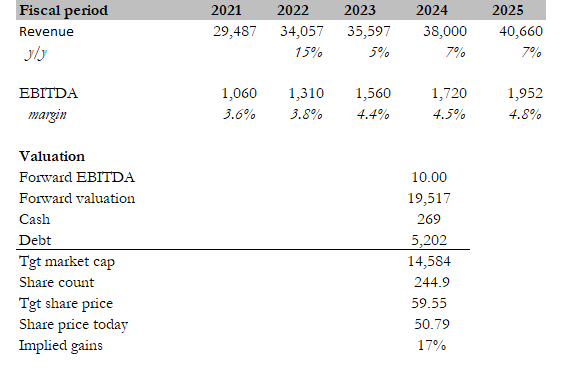

My target price for USFD, based on my model, is $61.78. My model assumptions are that USFD will grow 7% in FY24, in line with management guidance, and 7% in FY25. There should be no issues for USFD to at least sustain the 7% growth, as I expect the economy to turn better in FY25. As I said above, USFD grew organically historically at an average of 4%, which, combined with the current inflation rate of 3%, should easily give 7% growth, excluding another inorganic growth contribution. Margins should improve as well, driven by all the cost savings and productivity gains. I modeled a 4.5% margin in FY24 (guidance) and another 30 bps acceleration, in line with recent trends. In my model, I am assuming USFD will trend back to normalcy with a better margin; as such, USFD should have no issues sustaining its current multiple of 10x forward EBITDA (note that this is where USFD has historically traded on average over the past 10 years).

Although the staffing crisis is over, if it does happen again, it would definitely impact USFD performance. Not only will it impact the growth recovery, but it will also be a resource drag for USFD as they need to reallocate resources to address this situation, potentially impacting USFD's ability to execute its margin improvement and cost savings initiatives.

I am upgrading my rating on USFD to a buy. USFD's robust 4Q23 results, beating consensus expectations with strong case growth and positive unit economics, shows that they can execute well. Looking ahead, USFD's ongoing cost-saving / productivity improvement initiatives should drive margin expansion, leading to EBITDA growing faster than topline. While I may have missed the recent stock rally, I believe current evidence of robust execution makes it a safer investment, with further upside potential.