Ole_CNX

Ole_CNX

Uranium Royalty (NASDAQ:UROY) is a uranium royalty company focused on gaining exposure to uranium prices through a portfolio of uranium royalties and physical uranium ownership. The company is more of a bet on a higher uranium price than an investment, as it is currently priced at $100 per pound of uranium, which makes it 20% overvalued.

In August 2023, I wrote an article, Uranium Royalty: A Bet on the High Price of Uranium and the Lack of Supply. Since then, the stock has been up 25%, and I think that now, after more than 7 months, it is a good time to revisit the stock, find out what has changed since August, and evaluate where I was wrong, where I was right, and whether my thesis is still valid. If you are also interested in information about the business model and royalties owned by the company, I suggest that you check out my previous article, where I provided this type of information. Now I will focus more on the development since August 2023.

The most important developments in the company from my perspective are the following (for more detailed information please check Management's Discussion and Analysis and Interim Consolidated Financial Statements from January 31, 2024):

There are also two other significant developments in the uranium market. The single most significant is that the price of uranium has gone from $55 in August 2023 to $106 in January 2024 and is now, in March 2024, a bit lower at $85 per pound.

The second important development is that new uranium supply is coming to the market, and this new supply is expected to reach 6 million pounds of uranium in 2024. For more information regarding this supply, you may refer to my previous article "Kazatomprom: Undervalued Despite Strong Cash Flow Prospects," where I also provide links to the information sources.

There is an interview on the UROY web page with CEO Scott Melbye from PDAC 2024 in Toronto, where he explains the plans for the company in the future. In a nutshell, they plan to increase the number of royalties from 20 to 25 by March 2025. These deals should be financed by sales of existing physical uranium stockpiles.

If that's the case, the purchase of 2.5 million pounds of uranium for $54.44 per pound makes sense. My concern is that the price of new royalties will probably be higher too, and the time to bring a mine online may take 10 or more years, so in the meantime (till the royalties produce a cash flow), the shareholders will exchange uranium for the possibility of future cash flows. This may be a good move if the price of uranium goes up and the miners have an incentive to produce the metal. With this strategy, they gained some time to find and buy some new royalties, so there was nothing bad with it.

My first mistake was that I did not expect that the uranium price would almost double from $55 per pound to $106 per pound (in January 2024) without a significant supply disruption caused by existing supply going down. Well, as we now know, that did not happen, and the price has gone up anyway. As a consequence, I will use for the valuation a larger price range.

My second mistake was that I did not expect that the company would generate positive net income. For the nine months ended January 31, 2024, the company generated net income of $3.1 million from the sales of uranium inventory. Although I suggested that the company should also sell some inventory instead of issuing new shares.

I was correct that the number of shares will go up and shareholders will get diluted as the number of ordinary shares increases from 100.37 million to 120.2 million in just 8 months. However, the price increase of uranium helped the company, and it is now slightly less overvalued than it was 8 months ago.

Author

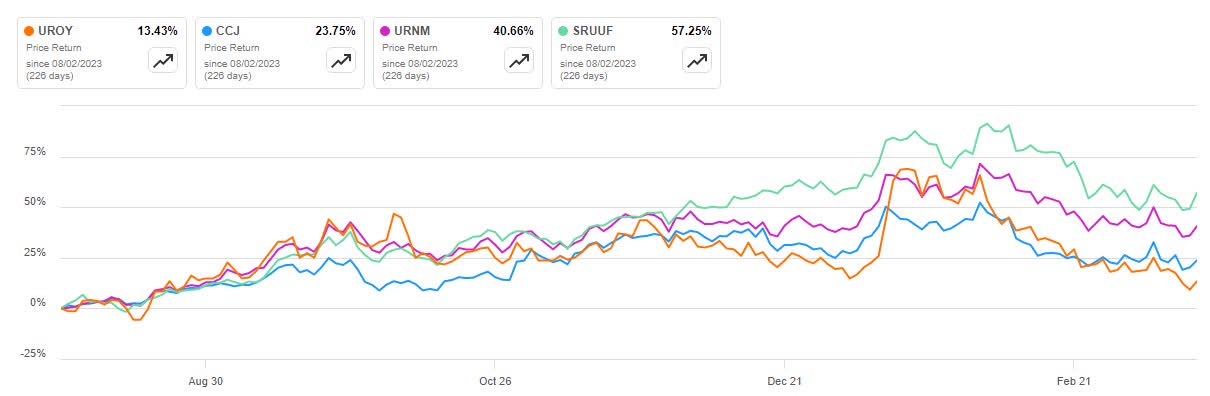

I was also right in my expectation that there are other and better ways to get exposure to uranium. I named three: Sprott Physical Uranium Trust (OTCPK:SRUUF), Sprott Uranium Miners ETF (URNM), and Cameco (CCJ). All are performing better at the current date; however, to be fair, in January, when the UROY price rose to $3.76, it was time to sell.

Seeking Alpha

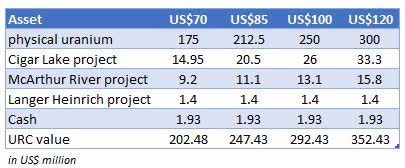

For the valuation, I have used different uranium prices, a 10% discount rate, and only those royalties that are in production or will be in production by the next year, as it makes no sense to include royalties where the planned production date is more than 2 years in the future because, as is usual with mines, anything can happen and the production may be postponed. A good example of this is the Lance Uranium Project, which was postponed in July 2023 within a month of the planned restart of production.

Table: Author

The current market cap of UROY is $296.24 million, which tells me that the company is priced at $100 per pound of uranium and is currently 20% overvalued. At the end, it all depends on the uranium price, which has been very volatile since last year.

For me, this is still more of a bet on the high uranium than an investment. However, I have to point out that the market cap of the company is low, and if enough money flows to it, the stock may double or triple. Just for comparison, the Cameco market cap is $17.83 billion, which is 60 times higher; therefore, the volatility may be higher.

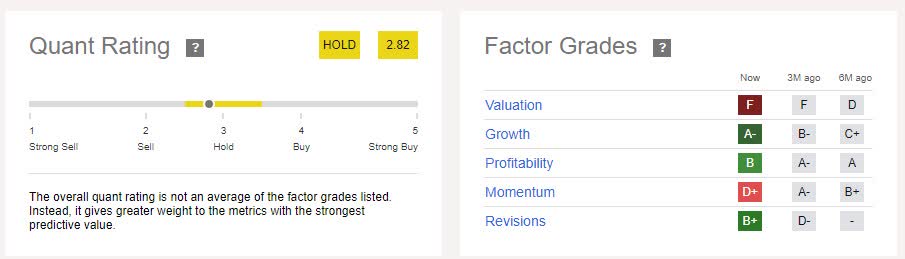

When I check the quant rating and valuation on Seeking Alpha, it is also not far from my own valuation. I tend to use this kind of information on the Seeking Alpha page as it offers me useful information, especially when I dig deeper into factor grades.

Seeking Alpha

There are also risks associated with this company and my investment thesis. Below, I'll attempt to highlight a few of them.

For me, this company is still more of a bet on a higher uranium price than a real investment. There is no real revenue except for the sale of physical uranium and one royalty from CAMECO. In my last article, 8 months ago, I made the statement that there are better ways to play the uranium market, and I think that it is still true. The Sprott Physical Uranium Trust and the Sprott Uranium Miners ETF are better ways to get exposure to uranium. At least they are safer, and there is only a 0.70% or 0.83% management fee, which is less than the 19.7% share dilution in UROY.

Finally, I want to point out that the market cap of the company is just $296.24 million, and the stock may experience high volatility depending on the flow of funds.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.