HT Ganzo

HT Ganzo

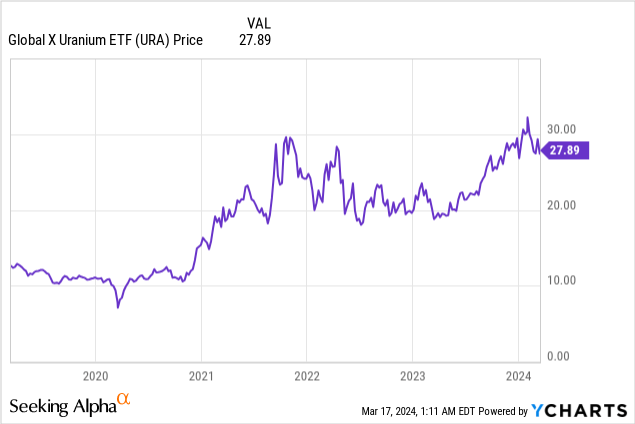

The Global X Uranium ETF (NYSEARCA:URA) includes stocks that provide exposure to the uranium value chain. Its share price has retrenched from $32.2 and is trading around $27.9 as charted below.

This thesis will show that this constitutes a buying opportunity, and, this based on the vast amounts of energy being consumed both by Nvidia’s (NVDA) AI-enabling GPUs and for Bitcoin mining. I also support my position with the seasonality factor.

Starting by putting things into perspective, according to an article published in Data Center Frontier, AI and cryptocurrency together could double global data center energy consumption to 1,000 terawatt-hours (TWh) in 2026. Tellingly, this represents a quarter of what the entire U.S. consumed in 2022 which means that a lot of power needs to be produced in just two years.

First, diving deeper into AI, while it surely offers productivity gains for enterprises, it consumes a lot of power, for example, Hugging Face consumes around 433 megawatt-hours (MWh) per day just for the training of its models. This is equivalent to the one-year energy bills of 40 average homes in the United States.

Now, due to their notoriously high computational demands, Generative AI algorithms that drive applications like ChatGPT work best when driven by Nvidia’s H100 GPUs, and one of these consumes up to 700 W, or nearly double that of processors from Intel (INTC) and Advanced Micro Devices (AMD). Now, since 1.5 million to 2 million of these chips are expected to be sold this year alone, the aggregate power consumption could rival with metropolitan cities.

Due to the high demand for its products, one could be tempted to invest in Nvidia's shares, but the problem is the relatively rich valuation at a trailing GAAP P/E of 76.18x. Even the VanEck Semiconductor ETF (SMH) which dedicates 27% of its weight to Nvidia trades at a multiple of 28.73x according to Morningstar. By comparison, URA's P/E trades at only 17.85x signifying that even if it is an indirect way to ride the AI story, it is a much cheaper one too.

Then comes the crypto industry which should digest about 160 TWh of electrical energy in 2026, representing a 40% increase since 2022. Furthermore, the approval of Bitcoin spot ETFs by the Security and Exchange Commission in January this year has led to increased demand for the asset, but, at the heart of cryptocurrency production is the power-hungry Bitcoin mining process which uses computing power to add blocks to the blockchain.

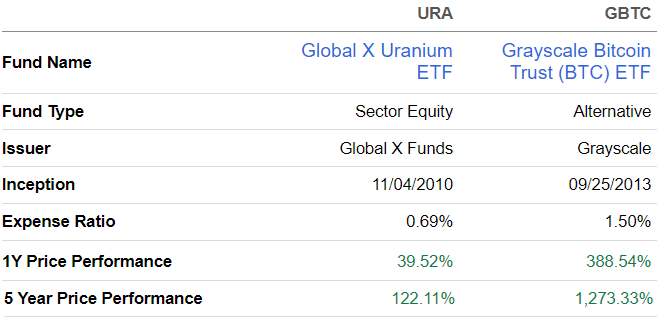

Now for those of you who have missed the Bitcoin rally or are contemplating additional investment into one of the crypto funds, like the Grayscale Bitcoin Trust ETF (GBTC), the problem is it has already gained more than 1270% during the last five years. That is more than ten times URA's upside.

Comparison of Metrics (seekingalpha.com)

Therefore, thinking laterally, it again makes sense to get indirect exposure to Bitcoin through energy, but, it is important to explain why the nuclear route is the best.

There are so many energy sources ranging from fossil fuels including natural gas, and renewables (wind and solar) which can provide power to data centers. However, because of Net Zero, or no emissions of greenhouse gases like carbon dioxide commitments, the United States' goal is to achieve 100% clean electricity by 2035. As a result, data centers where AI and other servers are housed plan to reduce their carbon footprints. At the same time, Bitcoin miners are shifting to renewables to cut down on fossil fuels.

However, during the transition phase to clean energy, nuclear power is expected to play a key role. As such, it is the second most used low-carbon energy source utilized to produce electricity after hydraulic, or using water such as in dams. Also, nuclear power plants emit almost no greenhouse gases during operation according to Global X.

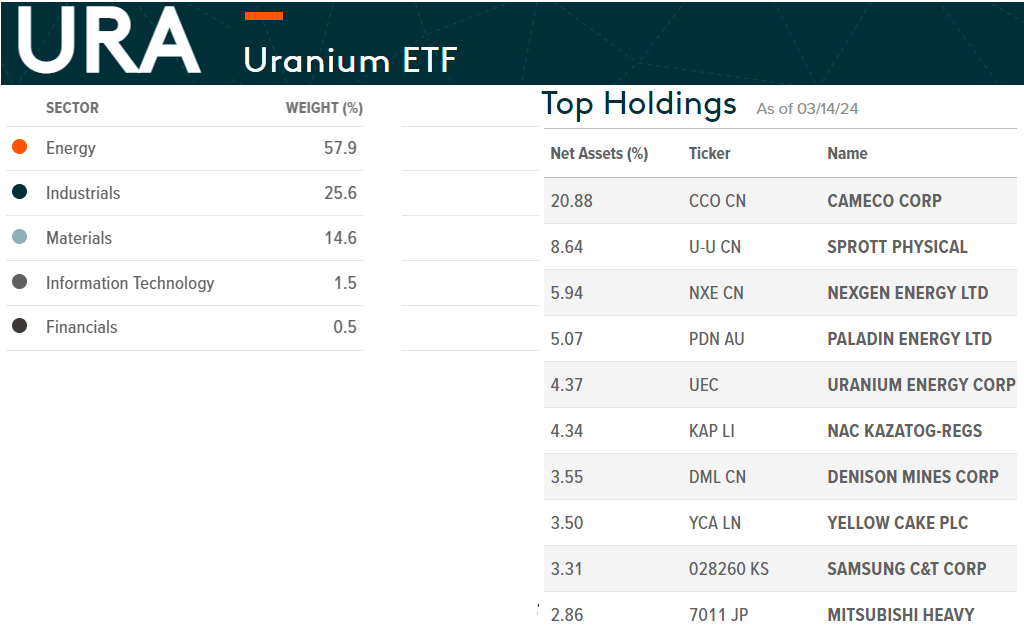

As for URA, it provides diversified exposure to uranium in the sense that its holdings operate across the entire value chain of the metal ranging from energy, to industries like mining, and those providing the technology support as shown below. In addition, about 8.64% of its assets consist of physical uranium.

www.globalxetfs.com

The top holdings is Canadian miner Cameco Corp (CCJ) which constitutes 20.88% of URA's weight and whose revenue forecasts are roughly 68% both for fiscal years 2024 and 2025. Hence, based on Cameco's weight of 20.88%, I have a growth estimate of 14.2% (68 x 0.2088) for URA. Applying this multiple to the current share price of $27.9, I have a target of $31.9. This represents a relatively modest increase given the risks.

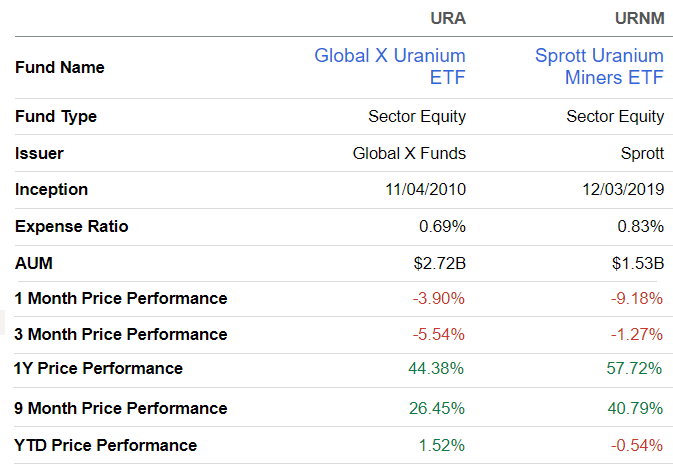

First, looking across the industry, there is the Sprott Uranium Miners ETF (URNM) which charges 0.83% compared to URA's 0.69% as illustrated below. It invests in companies involved in the actual exploration, mining, production, and holding of the radioactive metal. As such, its holding structure bears more concentration risks than URA which is more diversified across other industry verticals like energy and equipment manufacturing for the nuclear industry. This may be the reason why the Sprott ETF has suffered from a higher degree of volatility, as shown by the one-month price performance.

seekingalpha.com

Second, there are risks in investing in nuclear energy is that it is a sensitive topic, especially after the Fukushima power plant in Japan sustained damages to its cooling systems after a powerful earthquake followed by a Tsunami hit in 2011. As a result, three reactors melted down causing the release of radiation in the vicinity, and this had a profound effect on the industry since the country’s nuclear power stations had to close down for maintenance purposes with the shortfall in energy production generated mostly through LNG (light natural gas).

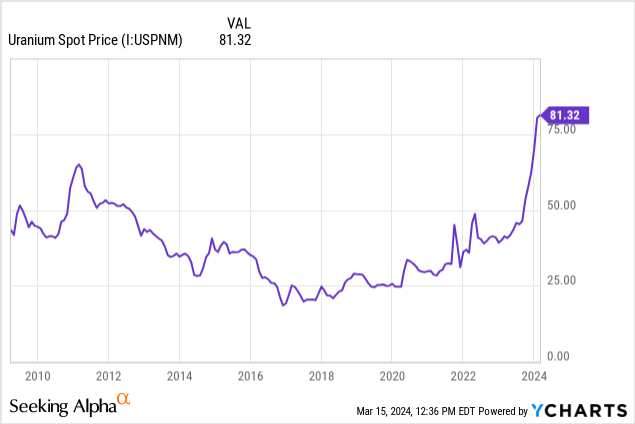

Consequently, in case there is any incident at one of the world's 440 nuclear commercial power reactors which together provide about 10% of global electricity needs, expect backlash against this energy source. Things could prove worse in case there are radioactive leaks entailing production cuts and causing demand for the radioactive metal to drop. This would in turn put pressure on commodity prices, and uranium could fall off its peak as was the case in 2011 (chart below).

However, besides the fear factor, economic realism also comes into play on the back of surging natural gas prices from 2021, without forgetting that global supply chains can easily be disrupted because of conflicts. Consequently, more than a decade after the incident, eleven out of the 25 Japanese reactors are again operational, with the authorities having approved a further six to be put online, with eight undergoing the review process. Noteworthily, public opinion has become less averse to nuclear energy with more than 50% of Japanese nationals now favorable to restarting the rest of the plants according to a recent survey compared to 30% previously.

Along the same lines, the International Atomic Energy Agency has urged development banks worldwide to provide financing for commercial nuclear projects in a bid not to delay the energy transition process. The agency's chief also exhorted international financial institutions to get rid of the post-Chornobyl mindset consisting of restraining funding for uranium-based energy projects. He emphasized the need for alignment with the realities of a changing world where conflicts like those in East Europe and the Middle East can potentially disrupt oil supply chains.

Therefore, the prospect of more financing increases the likelihood of the 110 nuclear plants currently in the planning stage being implemented and adds to the 60 reactors already under construction.

In conclusion, by going through the enormous amounts of energy required for AI computing and Bitcoin mining, this thesis has shown the additional power that will be required is only achievable through nuclear energy because governments have already pledged to reduce reliance on fossil fuel. Now, if this pledge is reviewed to one favoring fossil fuels in case of a change in the U.S. Presidential administration following the November elections, the price of uranium could be under pressure as seen in the above chart for the 2016-2020 period.

Still, to be realistic, no nuclear plant is under construction in America, and, the vast majority of those planned are in Asia which means that demand for uranium should be sustained irrespective of U.S. energy policy changes. On the contrary, with nuclear power generating 19%–20% of total annual U.S. electricity generation from 1990 through 2021, it is unlikely for them to reduce output given the energy needs for AI and Bitcoin which implies demand should not be impacted, but do expect volatility in case the nuclear energy topic comes in the limelight.

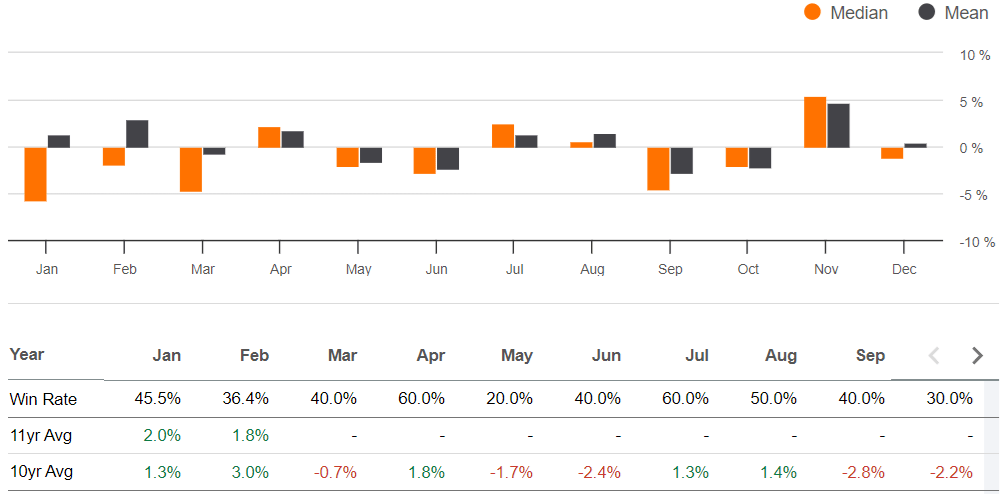

Moreover, looking at country exposure, the U.S. makes up less than 10% of URA's weight, and there is also the seasonality factor as per the chart below which builds on data from the last 10-11 years. It shows that there is a 60% chance (win rate) of an average upside of 1.8% in April. This should be followed by volatility episodes (downsides and upsides), but, there is a 70% chance of an average upside of 4.8% in November.

Seasonality (seekingalpha.com)

Finally, URA provides dividends but history shows that these tend to vary throughout the years. Thus, the yield was 6.07% at the end of 2023 but was only 0.8% one year earlier.