10'000 Hours

10'000 Hours

The market has been a story of haves and have-nots so far in 2024. AI plays have seen unprecedented momentum, alongside renewed optimism for cryptocurrencies. Meanwhile, non-tech stocks have lagged, and EV companies have also declined precipitously.

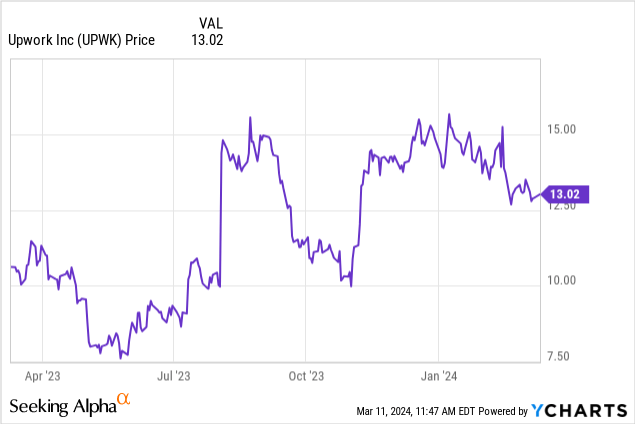

In the losers' bucket as well as Upwork Inc. (NASDAQ:UPWK), a freelance work platform that temporarily surged during the pandemic as companies sought to band-aid their workforces with temporary remote help. Upwork has languished in the years since; and so far in 2024, the stock is down ~10%. We have to ask ourselves: is there salvage value here?

I last wrote a bearish article on Upwork in December, when the stock was trading closer to $15 per share. Since then, two things have happened: first, the stock has declined by ~15%; second, the company has released Q4 earnings and an outlook for FY24 that addressed many top-line qualms. In light of the rare dual combination of favorable fundamentals plus a cheaper price, I'm upgrading my rating on Upwork to neutral.

At this juncture and at current prices, I see a relatively balanced bull and bear case for Upwork. On the positive side for this company:

At the same time, I also see a myriad of risks:

We have to consider the fact that Upwork trades at a modest valuation in an otherwise expensive market. At current share prices near $13, Upwork trades at a market cap of $1.78 billion. After we net off the $550.1 million of cash and $356.1 million of debt on the company's most recent balance sheet, Upwork's resulting enterprise value is $1.59 billion.

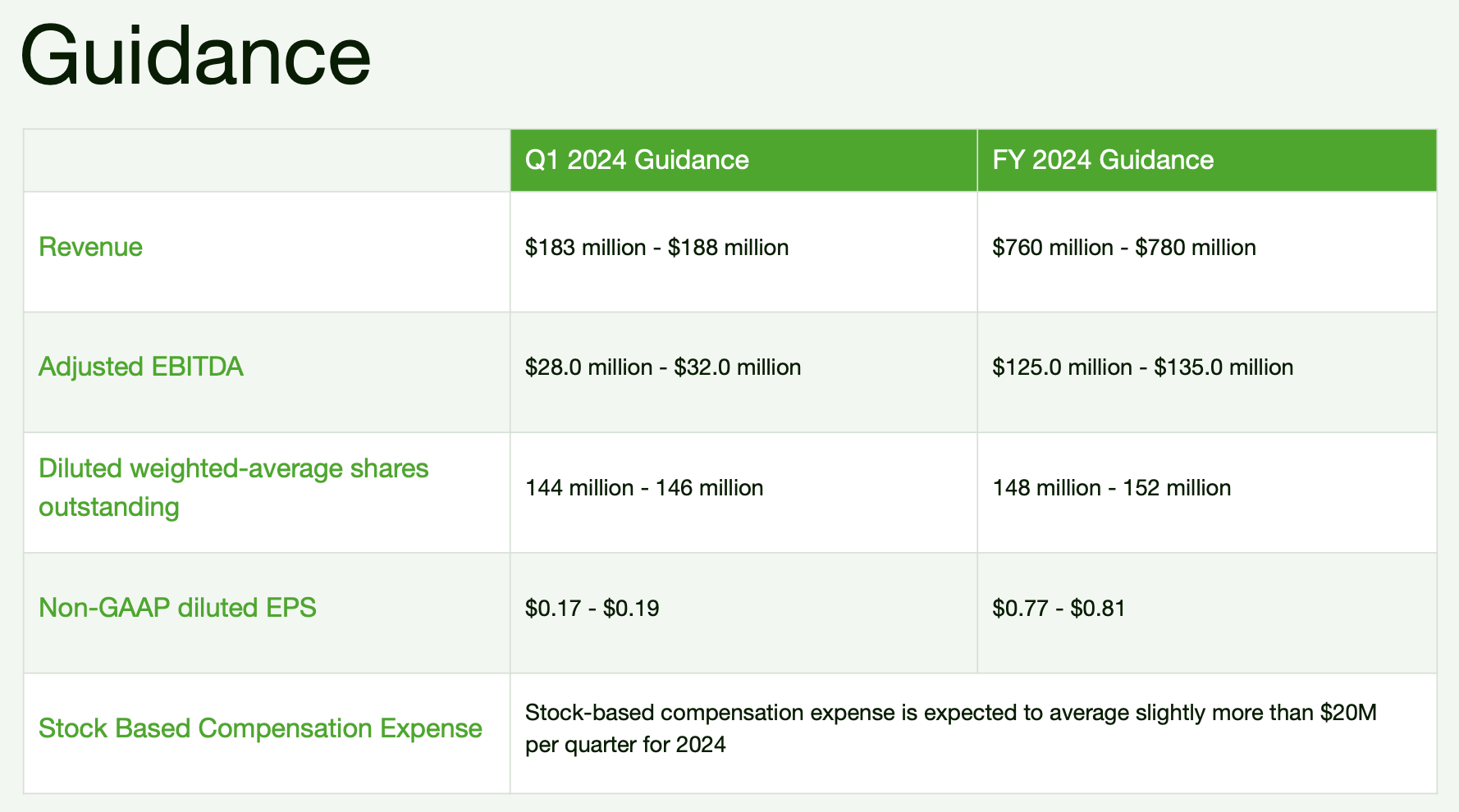

Meanwhile, for the current fiscal year, Upwork has guided to $760-$780 million in revenue (10-13% y/y growth) and $0.77-$0.81 in pro forma EPS:

Upwork outlook (Upwork Q4 earnings deck)

This puts the stock's valuation multiples at:

In my view, I'd still hold off on rushing in to buy, but I'd turn bullish on Upwork if the stock fell to ~$11.50 (representing ~14.5x P/E and ~1.8x revenue), roughly where it was trading last October before the broader market rally.

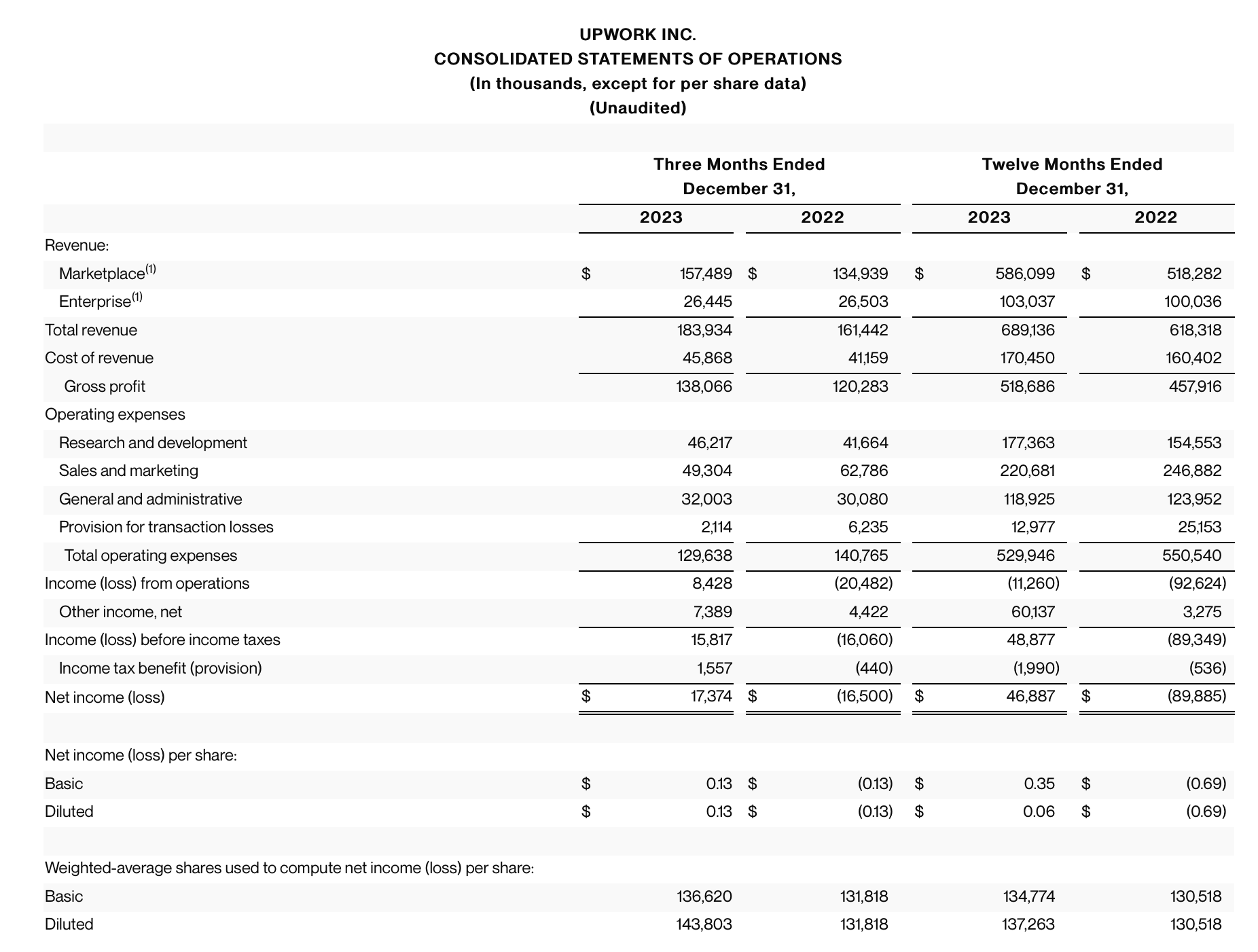

Let's now go through Upwork's latest quarterly results in greater detail. The Q4 earnings summary is shown below:

Upwork Q4 results (Upwork Q4 earnings deck)

Upwork's revenue grew 14% y/y to $183.9 million, ahead of Wall Street's expectations of $178.1 million (+10% y/y) by a sharp four-point margin. It's worth noting as well that revenue growth accelerated meaningfully versus 11% y/y growth in Q3. As a reminder, Upwork is benefiting from upward pricing actions that it took in the back half of FY23 (it's also signaling that while growth is expected to land at 10-13% y/y in FY24, the back-half growth rate in FY24 will slow down considerably due to lapping these price actions).

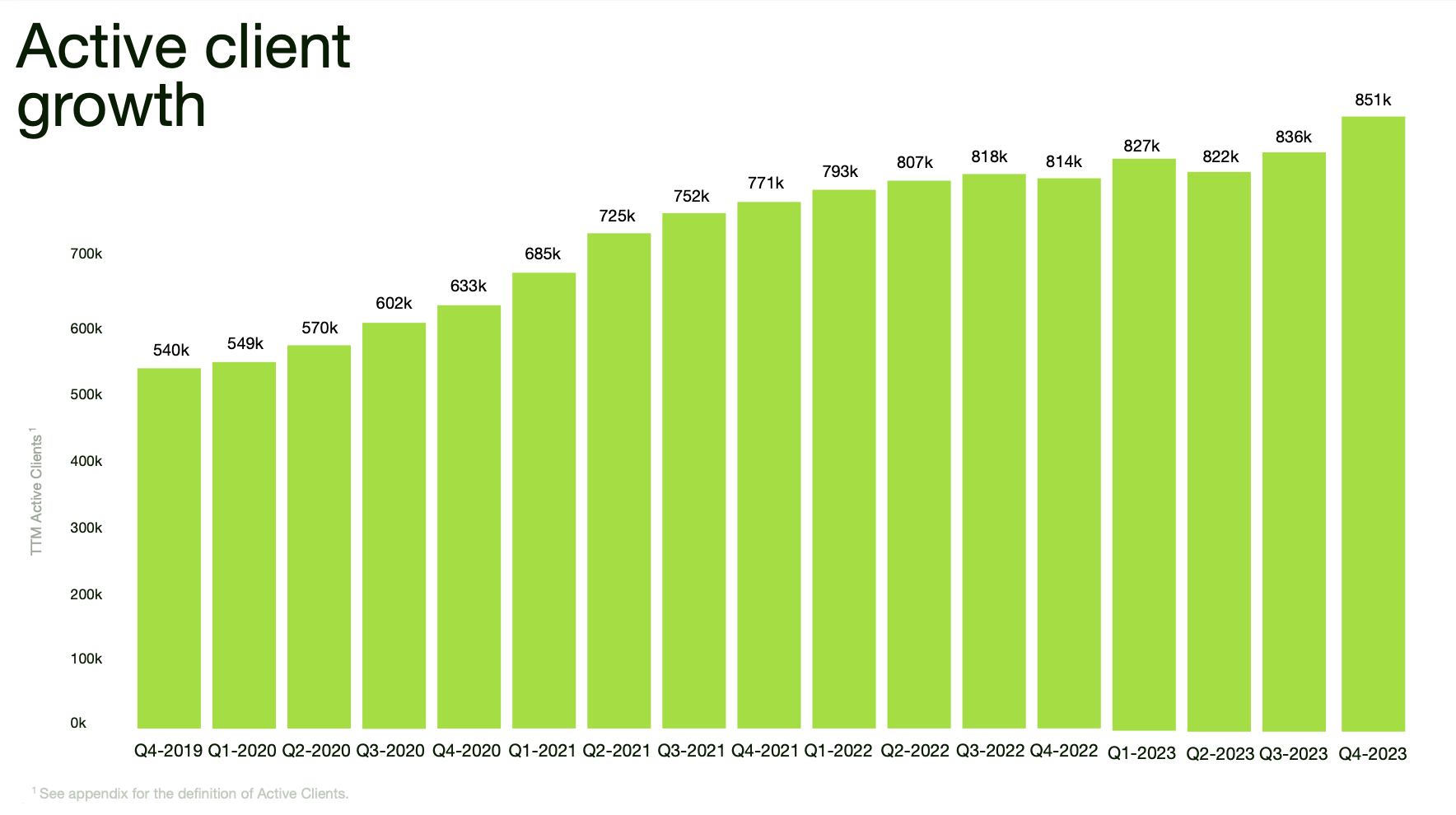

However, notably: Upwork's decision to increase prices has not dented its client acquisition rates. Active clients soared to 851k in Q4, up 17k sequentially after several rocky quarters that bounced back between net adds and net losses:

Upwork client trends (Upwork Q4 earnings deck)

Here is further anecdotal commentary from CFO Erica Gessert's remarks on the Q4 earnings call:

Our focus on greater efficiency is yielding tremendous results. Our performance marketing engine is working better than ever. In Q4, we saw 20% growth in our new client starts driven by performance marketing, while our CAC in the same period improved by 24% year-over-year. We also had excellent success with higher-value client segments, which we expect to have an outsized impact on revenue and LTV. And in enterprise sales, we were able to increase our client acquisition in Q4 even with our rationalized sales force. These positive actions helped to drive total active client growth of 5% year-over-year in the fourth quarter.

Within the dynamic market environment in 2023, we turned our business into one of steady growth. For the full year 2024, we expect to continue this progress, producing strong year-over-year growth in active clients, revenue, adjusted EBITDA, and adjusted free cash flow. Our momentum exiting 2023 and our plan for 2024 give us the conviction that we can provide strong business results and serve our customers even in uncertain economic conditions. This confidence is based on our growing business efficiency, our culture of innovation, and the pipeline of new products that we have planned for 2024 and beyond."

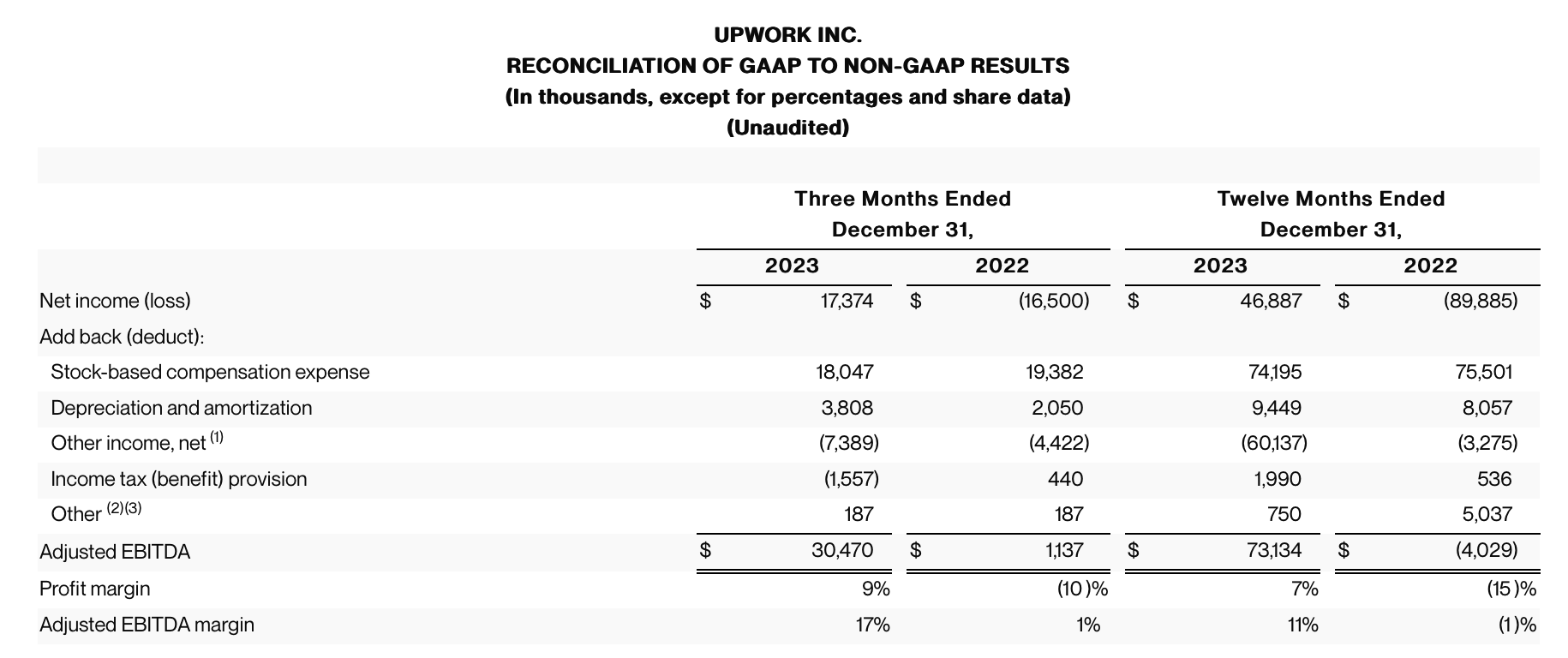

And from a profitability standpoint, note that Upwork notched a rich 17% adjusted EBITDA margin in the fourth quarter, up from just 1% in the year-ago Q4, while full-year adjusted EBITDA also leaped up 12 points:

Upwork adjusted EBITDA (Upwork Q4 earnings deck)

Upwork's guidance implies adjusted EBITDA margins growing to 17% next year, up six additional points from FY23.

With price increases driving revenue re-acceleration while not hampering new customer acquisition, there are reasons to be hopeful about Upwork going forward: especially as it looks to significantly boost its profit margins in 2024. I'd still wait for Upwork to drop to the ~$11-$12 range before buying in, but this stock merits re-inclusion in your watch list now.