choi dongsu/iStock via Getty Images

choi dongsu/iStock via Getty Images

As I sit down to write this evening, investors may have burning questions concerning Pagaya Technologies Ltd.'s (NASDAQ:PGY) long-term path to profitability. Is the investment still viable?

There's much to consider amidst recent gargantuan losses and sky-high volatility. In the previous week (March 8-15, 2024), Pagaya's shares suffered a -40% loss in 5 days, precipitated by a reverse 12/1 split. Three days following the split, there was an unexpected secondary offering that went badly (and got worse) by the hour, bringing the shares down to $10.78.

This mini-crash has left the question of why such a debacle took place, and the reason for the surprise secondary offering in the first place.

This article is an attempt to answer these two questions.

First of all, 2023 featured a large volume of BUY and STRONG BUY articles touting the progress and success of Pagaya as an ABS (Asset-backed Security) securitizer. Today Pagaya is the number one issuer of personal loan ABS transactions in the U.S. The company has never lost a large client. Once onboarded, they have stayed.

As reported in the company's recent Fourth Quarter and Full Year 2023 Results, there have been steady increases in network volume, customers, securitizations "ABS" (15 in 2023), record revenue from fees less production costs ("FRLPC"), and quarterly-losses are diminishing.

In Pagaya's 4Q'23 Shareholder Letter (2/21/24), the company states,

We are reaching a point of sustainable profitability, setting us on a path to deliver expected adjusted EBITDA in the range of $150 million to $190 million in 2024, and positive net cash flow by early 2025." (Page 5)

Consensus from analysts is that "Pagaya Technologies is on the verge of breakeven. They expect the company to post a final loss in 2023, before turning a profit of US$28m in 2024. The company is therefore projected to breakeven around 12 months from now or less."

On March 12, 2024, Zach's upgraded Pagaya to Strong Buy, citing the recent earnings revisions "as a reflection of an upward trend in earnings estimates -- one of the most powerful forces impacting stock prices."

So there is A LOT to like.

I think the crux of Pagaya's current problem is its rapid growth in ABS securitization, juxtaposed with its required compliance with the Dodd-Frank Risk Retention Rules for those Securitizations.

Section 15G of the Exchange Act imposes risk retention requirements on any "securitizer" of ABS, approximately 5% (some say it's actually closer to 2-3% in practice) of the ABS that is securitized.

In 2024, Pagaya estimates it will securitize $9 billion to $10 billion in ABS, which would require a risk-retention investment of $450 million to $500 million in those ABS.

The question on investors' minds is, "Do they have the money for this risk-retention investment?" Hence the likely reason for the recent $280 million credit facility, and the secondary offering and capital raise (Approximately $90 million).

Currently, the company has:

Investors are uncertain. Is Pagaya Technologies Ltd. (PGY) experiencing a temporary ceiling of capital constraint, just before the company predicts it will turn fully profitable? In a sense, it's a race towards a moving target, with the goal of profitability in a year's time.

Here is how the company's business plan plays out:

Pagaya's detailed explanation of the process

When we onboard a new partner, the first year - the integration year - is focused on expanding across the lender's network of branches, dealers, or merchants, ensuring our product is live and operating successfully at each point of sale.

In year two - the ramp-up year - we are focused on growing volumes with the lender as our models learn from the new flow, enabling an increasing conversion rate, all else being equal.

By year 3 - the expansion year - most partnerships are fully ramped up and the focus turns to further expansion and product innovation to drive consistent growth in volumes.

To put it into context, the partners and channels we onboarded in 2022 delivered an additional $800 million to our network volume in the first 9 months of 2023, and we expect this figure to grow to approximately $1 billion in full-year 2023.

We expect that our recently announced cohort of 2023 integrations (Westlake Financial, top 5 bank (U.S. Bank), and top 4 auto (Exeter), which are much larger in total size and volume potential compared to our 2022 cohort, has the potential to generate significantly more incremental network volume over the next 12-18 months.

For our 2024 plan, we expect that all of our network volumes will be sourced from partners that are already part of our network as of today.

As each new customer is onboarded, a virtuous circle is created in their data, increasing conversions.

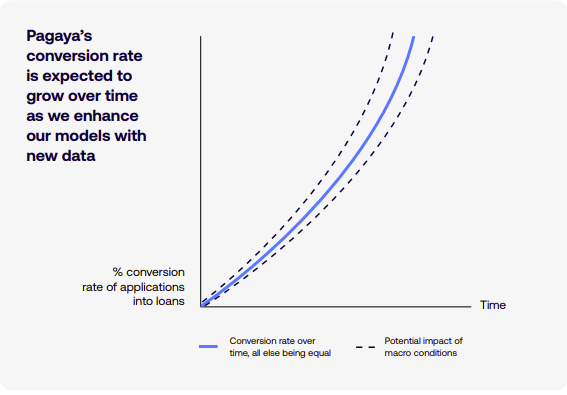

Pagaya Conversion Rate

...As we receive higher application flow, we can enhance our credit decisioning capabilities through increased proprietary data, which can lead to both an improved conversion rate of applications and better returns for investors.

Our models get smarter over time as we see more data - we can detect behavioral patterns, better predict the impact of macro trends on the ability of consumers to repay or detect instances of fraud. With time, as the predictive power of our AI models improves, we can increase our conversion rate by approving more loans at similar or higher expected returns. Higher conversion rates also lead to a strengthened competitive moat with our lenders.

When we first plug into a new lender, our conversion rate tends to be lower than average as our models start to train on a new dataset. Over time, as shown in the illustration below, we expect the conversion rate for each lending partner, all else being equal, to steadily improve over time as our models learn about the incoming data flow.

If Pagaya is pushing up against a ceiling of available resources needed for their 5% investment in new securitizations (2024), they must resolve this quandary, and with some urgency.

The only way to do this is:

When the company reaches core profitability by early 2025 (a very likely outcome), the forward-funding agreement (or portions thereof) would no longer be necessary, and future ABS could likely be self-funded.

In a sense, it is a race both against time and with time, because the company needs to get through 2024's onboarding of new clients - and the fuller integration of 2023's clients ($) on Pagaya's platform - before achieving profitability.

The company remains a Buy, with a one-year road to profitability, as previously stated by the company and the analysts which cover the company.

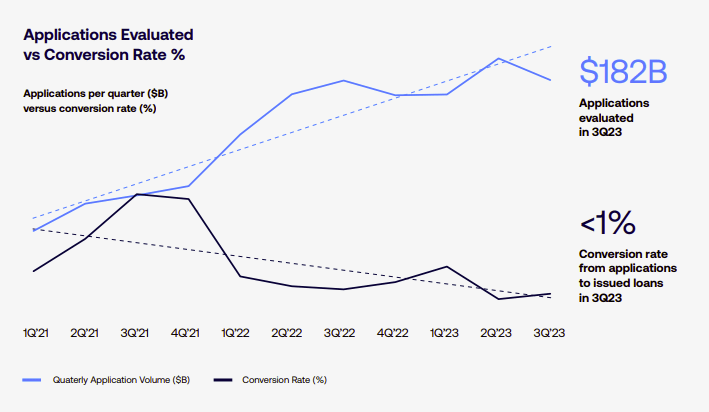

Pagaya conversion rate comparison

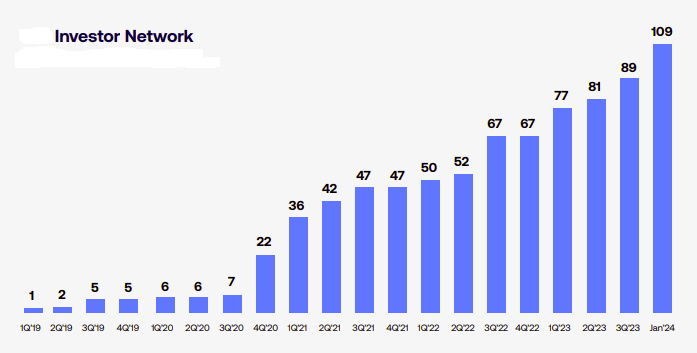

Growth in Pagaya Investor Network (Company shareholder report (2.21.24))

There are several downside risks:

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.