A UPS driver delivers packages on a route.

Joe Raedle/Getty Images News

A UPS driver delivers packages on a route. Joe Raedle/Getty Images News

As a dividend growth investor, I highly value businesses that value their shareholders. What I mean is companies that are committed to returning capital to shareholders via share repurchases and dividends in both the good times and the bad times.

This is because both the willingness and ability to do this are a somewhat rare combination in investing. A company can try to deliver value to shareholders all it wants, but if the cash isn't there, that desire is all for nothing.

On the flip side, a company can have the ability to return value to shareholders, yet choose not to do so.

One company that I believe is putting shareholders first and simultaneously navigating a difficult operating environment is United Parcel Service (NYSE:UPS). When I last covered UPS in January, I noted that I liked the generous dividend, the A-rated balance sheet, and the valuation.

In that time, shares have dipped another 1% as the S&P 500 (SP500) has gained 11%.

There have been a couple of developments since I last highlighted the company. On Jan. 30, UPS announced a 0.6% bump in its quarterly dividend per share to $1.63. According to its Q4 2023 Earnings Press Release, this marked the 15th consecutive year that it upped its payout. That same day, the company shared its financial results for the fourth quarter ended Dec. 31, 2023.

Today, I will be taking an updated look at UPS to explain why I'm maintaining my buy rating.

Dividend Kings Zen Research Terminal

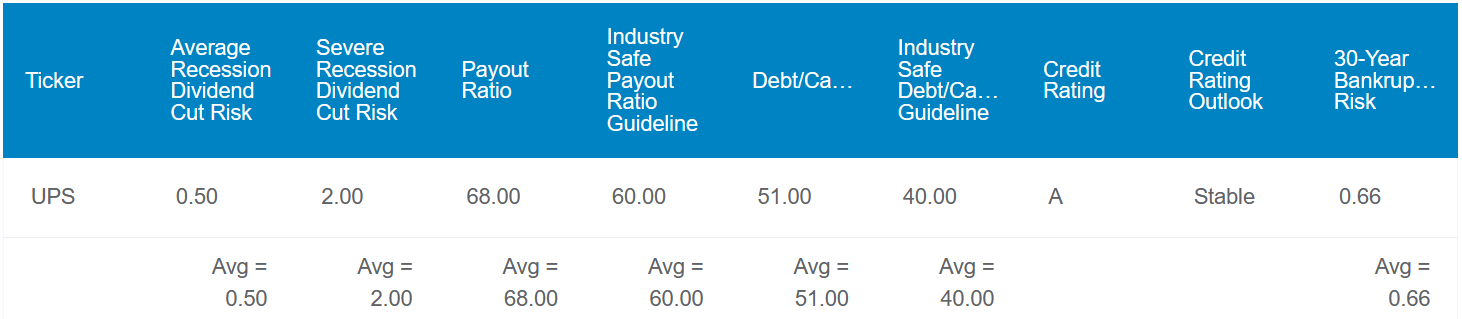

UPS's 4.2% forward dividend yield is markedly higher than the 1.4% forward yield of the industrials sector. That is enough to earn an A grade on forward dividend yield from Seeking Alpha's Quant System. The dividend also appears to be relatively safe, which is why UPS enjoys a B grade for dividend safety from the Quant System.

The company's 68% EPS payout ratio is above the 60% EPS payout ratio that rating agencies prefer to see from the industry. However, as I'll discuss in the dividend section of this article, that's not as much of a concern as it may initially seem.

UPS's 51% debt-to-capital ratio is also moderately higher than the 40% debt-to-capital ratio that rating agencies have as the industry-safe guideline. Another examination of the company demonstrates it to be in better financial health than the debt-to-capital ratio alone can convey.

For these reasons, S&P has the confidence to award an A credit rating to UPS on a stable outlook. This places the probability of the company going to zero in the next 30 years (e.g., bankrupt) at 0.66%. That implies UPS would remain a going concern in 151 out of 152 30-year simulations.

Thanks to these elements, the Zen Research Terminal projects the chance of a dividend cut in the next average recession from the company at 0.5%. If the next recession is severe, the possibility increases to 2%. For perspective, these are both the lowest likelihoods allowed in the Zen Research Terminal.

Dividend Kings Zen Research Terminal

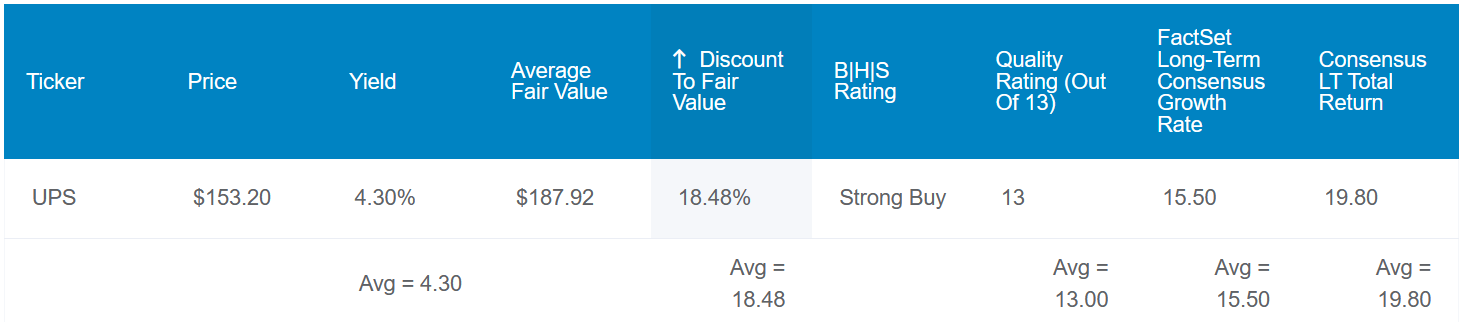

The appeal to UPS doesn't end at its fundamentals, either. The stock's five-year average dividend yield of 3.3% could signal shares to be worth $196 each.

UPS's historical P/E ratio (dating back to 2003) is nearly 20, which could indicate shares are worth $176 apiece. As the company's fundamentals improve, I believe a reversion to such a valuation could be a realistic assumption.

Using the following inputs into the dividend discount model, I arrive at a fair value of $186 a share: A $6.52 annualized dividend per share, a 10% discount rate, and a 6.5% annual dividend growth rate. As I'll touch on later, I think such a dividend growth rate could again be supported by the fundamentals within a couple of years.

Averaging out the Zen Research Terminal's fair value with my fair value, shares of UPS could be worth $187 each. This would represent a 17% discount to fair value from the current $156 share price (as of March 21, 2024).

If UPS returned to fair value and could grow at half of the current consensus, here are the total returns that it could deliver to shareholders in the coming decade:

UPS Q4 2023 Earnings Press Release

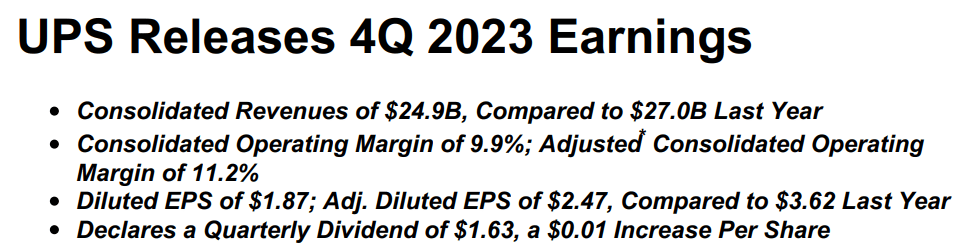

Considering the macroenvironment in which UPS operated during the fourth quarter ended Dec. 31, 2023, its results were fine in my view. The company's consolidated revenue dipped 7.8% year-over-year to $24.9 billion in the fourth quarter. For context, that was $510 million short of the analyst consensus per Seeking Alpha.

What factors were at play that make me believe UPS's fourth quarter results were satisfactory?

According to CFO Brian Newman's opening remarks during the Q4 2023 Earnings Call, the transportation and logistics sector remained pressured both in the U.S. and internationally. Newman pointed to soft demand and overcapacity within these markets as headwinds that explained these results. This is what led UPS's average daily volume to drop 7.4% year-over-year in the U.S. domestic segment and international average daily volume to decrease 8.3% over the year-ago period.

Following the five-year labor deal last summer, UPS worked diligently to recapture its lost volumes. Domestic average daily volumes were up 30% sequentially, which Newman pointed out was the company's highest sequential volume ramp in its history. Additionally, through the end of December, the company won back 60% of the volume that was diverted during labor negotiations.

UPS generated $2.47 in adjusted diluted EPS for the fourth quarter, which was down year-over-year by 31.8%. However, this did come in $0.01 ahead of the analyst consensus according to Seeking Alpha. Lower revenue coupled with higher labor costs resulted in a 320 basis point contraction in non-GAAP net profit margin to 8.5% during the fourth quarter. That's why adjusted diluted EPS fell at a much faster rate than consolidated revenue in the quarter.

Looking forward, UPS's Project Brown initiative should be a catalyst to help the business continue to recover. CEO Carol Tome indicated that the company is leveraging artificial intelligence via Deal Manager to improve response time to customers.

That has resulted in an improvement from an international response time of 22 days to six days and now down to a best-in-class two days. This takes the guesswork out of the jobs of salespeople to determine whether to accept a customer deal by providing a real-time score for a deal. That has expedited the process and improved win rates to 79% when using this tool per Tome.

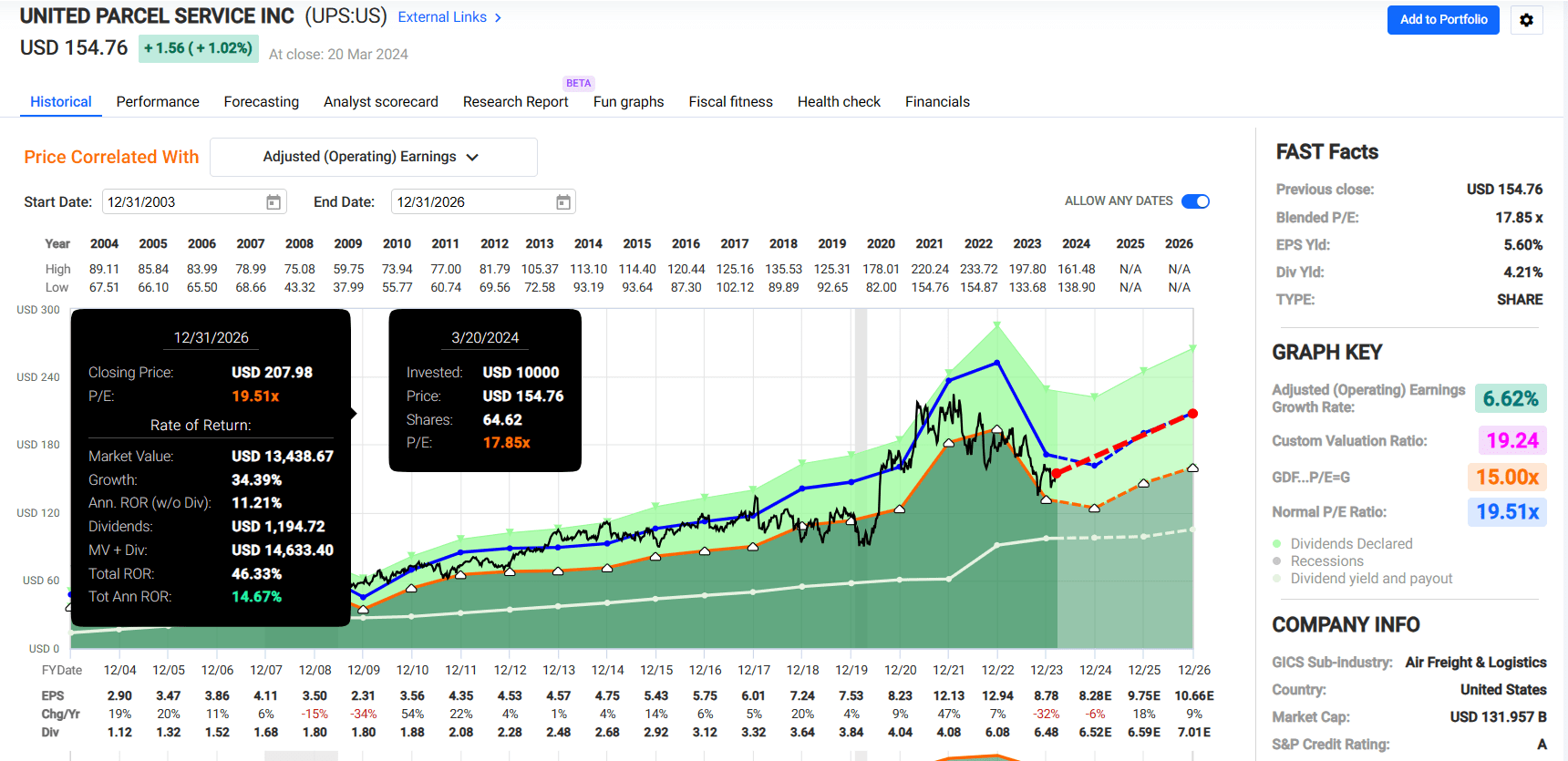

The FAST Graphs analyst consensus anticipates that adjusted diluted EPS will fall another 5.7% to $8.28 in 2024. But as UPS keeps recapturing diverted volume and macroeconomics improve, adjusted diluted EPS could rebound 17.8% to $9.75 in 2025 and another 9.3% to $10.66 in 2026.

The company's financial position also remained relatively strong for a down year. UPS's interest coverage ratio was 11.9 in 2023, which suggests it is firmly solvent. The company's adjusted debt to adjusted EBITDA ratio was also manageable at just under 2.2 (unless otherwise noted or hyperlinked, all details were sourced from UPS's Q4 2023 Earnings Press Release and UPS's Q4 2022 Earnings Press Release).

UPS's quarterly dividend per share has surged 69.8% higher in the past five years to the current rate of $1.63. This equates to an 11.2% compound annual growth rate.

The company posted $5.3 billion in free cash flow in 2023. Against the $5.4 billion in dividends paid during that time, this is a 101.8% free cash flow payout ratio. At first glance, that is alarming.

More context shows that the dividend should be fine, though. UPS's headwinds from the strike and ensuing loss of volume caused operating cash flow to crater 27.4% from 2022 to $10.2 billion in 2023. Along with an uptick in capex ($4.8 billion in 2022 to $5.2 billion in 2023) to improve the business for the long haul, this is responsible for the elevated free cash flow payout ratio (info in the previous two paragraphs according to page 67 of 169 of UPS's 10-K filing).

As UPS's free cash flow recovers and restores the payout ratio to a more sustainable level, I would expect another couple of years of token dividend raises. Once that's accomplished, though, I think mid- to upper-single-digit annual dividend growth can resume.

UPS is a business that looks poised to rebound, but there are risks to the investment thesis.

As I outlined above, UPS is winning back diverted volumes. The risk is that this doesn't continue as analysts currently are forecasting. If the company can't fully recover to 2022 levels of free cash flow, the dividend could be in jeopardy. I view this as an unlikely outcome, but it is worth monitoring this each quarter over the next couple of years just to be on the safe side.

I would also reiterate the risk that I alluded to in my previous article surrounding Amazon (AMZN). The e-commerce juggernaut accounted for 11.8% of the company's consolidated revenue in 2023 (page 8 of 169 of UPS's 10-K filing). As Amazon builds out its delivery network for its needs, this could lead to lost business for UPS.

FAST Graphs, FactSet

Even with its challenges, UPS is a business with characteristics that I like (it's 0.7% of my 99 stock portfolio). After a downward trajectory in 2023 and some residual headwinds in 2024, the company seems set to turn the corner in the next few quarters. UPS also yields 4%+ which should be safe as long as the recovery is completed. In the meantime, the balance sheet is strong enough that it can absorb a temporary shortfall between free cash flow and dividend obligations/share repurchases.

As a turnaround play, the valuation appears to be opportune. Shares are priced at a blended P/E ratio of 17.9, which is below the normal P/E ratio of 19.5 per FAST Graphs. If UPS grows as expected (fulfilling its turnaround potential) and returns to its normal P/E ratio, it could generate 46% cumulative total returns through 2026. That's why I'm keeping my buy rating.