delihayat/E+ via Getty Images

delihayat/E+ via Getty Images

I have recently made an argument in favor of owning ProShares Ultra S&P500 (SSO), a 2x leveraged play on the major US stock index, provided that enough risk control is put in place. A potentially better approach to capturing further upside in the S&P 500 (SPY) while also protecting a portfolio against sizable losses is through the ProShares UltraPro S&P500 ETF (NYSEARCA:UPRO) — what I consider to be a misunderstood trading or investment instrument often associated with irresponsible bullish speculation.

I start below by describing UPRO at a basic level, alongside important risks to which investors should pay close attention. I wrap up the discussion by presenting how I would use UPRO strategically to continue to ride what I expect to be a lingering stock market rally while protecting my portfolio against sizable losses.

The ProShares UltraPro S&P500 ETF is, simply put, a triple-leveraged play on the S&P 500. The fund's goal is to deliver three times the daily return of the US stock index, whether it be positive or negative.

UPRO is a fairly large (roughly $3.4 billion in assets under management), very liquid (4.8 million shares traded daily for a dollar equivalent of $325 million) instrument. The ETF charges an annual fee of 92 bps that seems hefty, on the surface, until one considers that it represents the equivalent of about 30 bps on the unlevered notional.

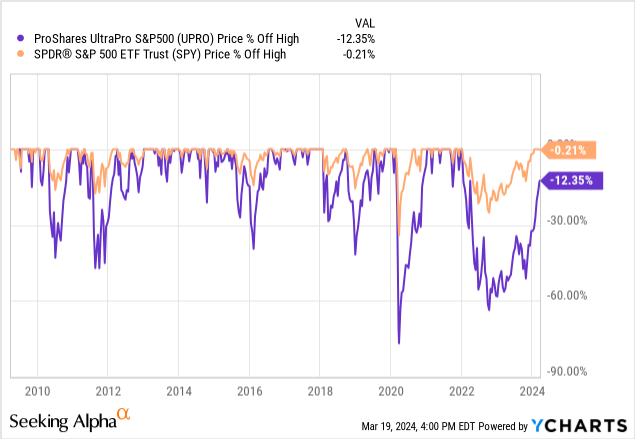

One of the main points made against owning UPRO is the dizzying volatility and gut-wrenching drawdowns. No one in their right mind should accept an annualized standard deviation of 46% and a maximum historical loss of 77% since UPRO's 2009 inception (see below). Frankly, I could not downplay these concerns. UPRO has, indeed, been extremely volatile, which makes it a terrible single ticker holding.

Also, leveraged ETFs should be handled with care, especially through a holding period any larger than one day, for two related reasons. First, there is no guarantee that UPRO's performance over time will match three times the performance of the S&P 500. Again, the 3x factor is a daily goal.

Second, UPRO "bleeds" gains through a process called volatility drag. Contrary to popular belief, this is not a flaw in leveraged ETFs, but a feature that results from the daily reset of the portfolio. Simply put, returns compound not only on the way up but also on the way down. The more daily losses UPRO incurs, the more exposed to volatility drag the ETF will be.

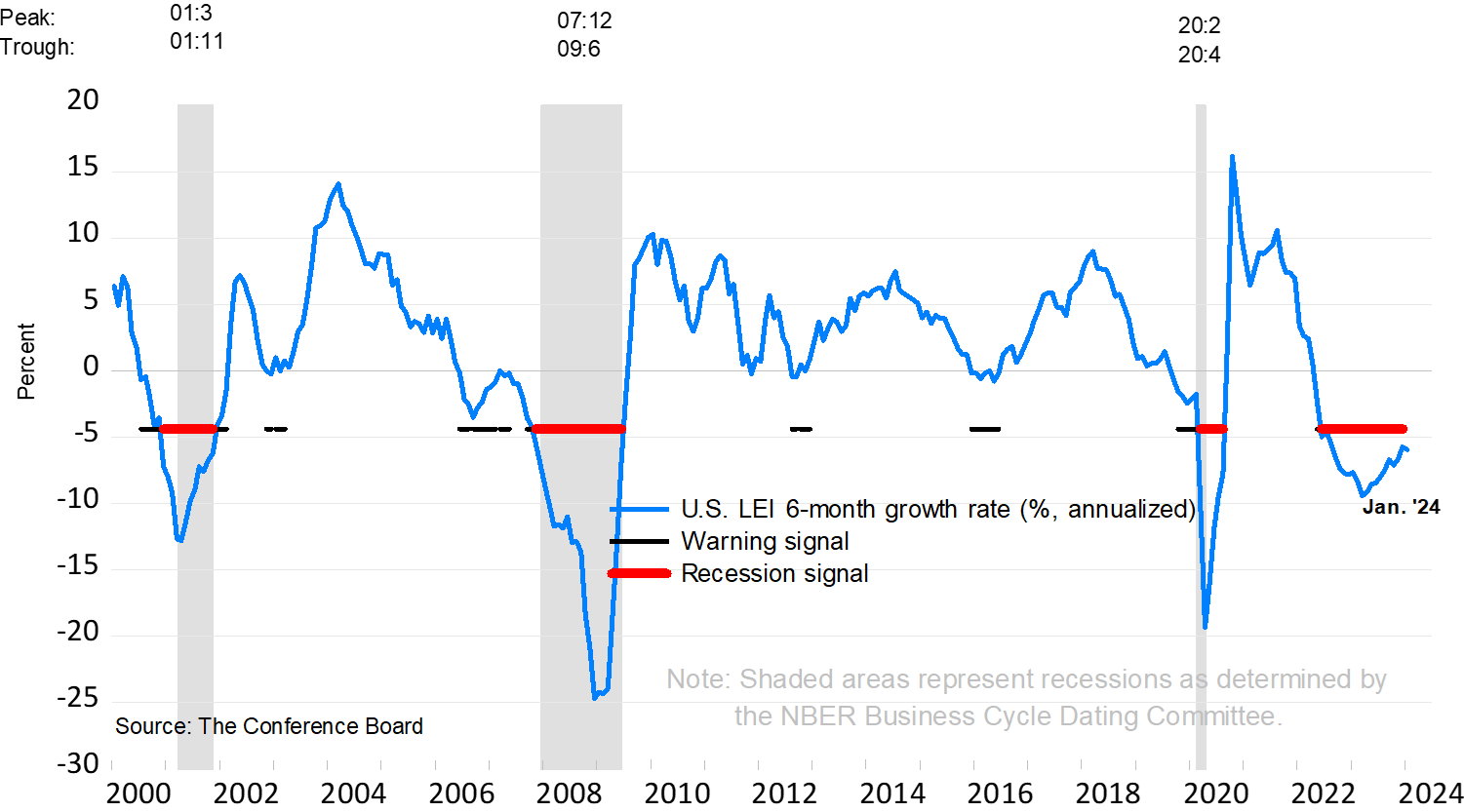

From a timing perspective, I believe that most long-term investors should be exposed to the S&P 500 (or a similar stock index) today. This is the case because the risk of an economic recession has moderated substantially lately, as suggested by an aggregate of leading indicators known as LEI (see chart below). Notice how the leading indicators flashed the red light on an upcoming recession in 2022 but have taken a turn for the better in the past few months.

The Conference Board

No, the US economy is not firing on all cylinders. But, in spite of some softness observed in business confidence and a stubbornly inverted yield curve, meaningful contraction in economic activity does not seem likely given a fairly robust job market and decent (albeit not perfect) consumer credit profile.

In any case, one does not need to be 100% sure about the health of the economy (who can ever be sure, anyway?) and the direction of stock prices to be bullish on the S&P 500. Provided that loss mitigation tactics are used, owning the stock market index makes sense most of the time, certainly for long-term investors. This is where UPRO comes in.

If I am right that the S&P 500 is likely to continue climbing for now, despite its 32% gains over the past 12 months and slowly rising valuations, the case for owning UPRO should be somewhat clear. Faced with continued stock market bullishness, the levered fund should fare well and help to provide a boost to growth portfolios.

However, one of the biggest problems with owning UPRO is the downside exposure to a crumbling stock market. Those who owned the ETF through the brief COVID-19 bear market of February and March 2020 can probably attest to this.

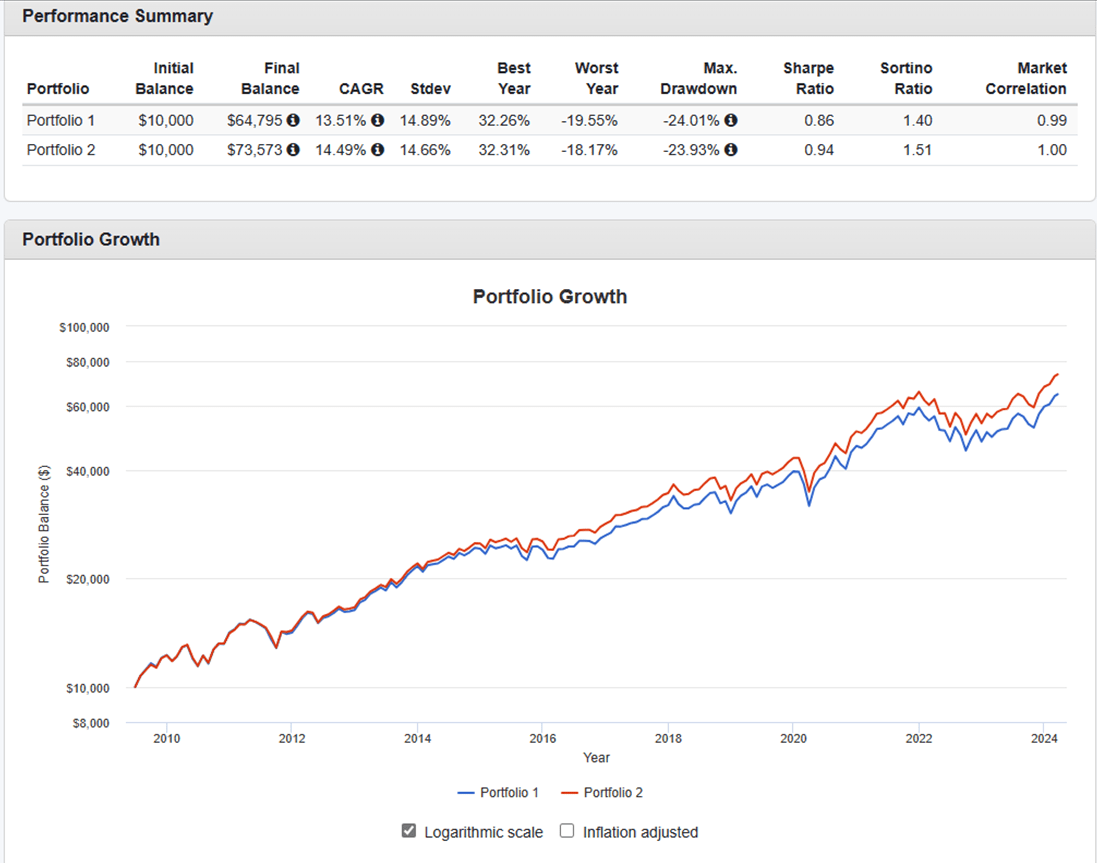

But UPRO does not need to be (and should not be, in my opinion) a majority holding. If, for example, the leveraged ETF is blended at a rate of 33% alongside a 67% allocation to cash, an investor can effectively "delever" and closely emulate the performance of the S&P 500. This is true even over long periods, as the chart below depicts.

Portfolio Visualizer

But why bother delevering a leveraged ETF? By doing so with UPRO in the 33-67 case presented above, a portfolio exposes only 33% of its assets to a declining stock market, at least until it rebalances. This is what happened during the early innings of the COVID-19 crisis.

Back then, the S&P 500 fell 34% from peak to trough in early 2020, but a 33/67 UPRO-cash portfolio fell only 25%. Had the S&P 500 continued to crater beyond March 23, 2020, the blended portfolio would have lost virtually nothing beyond that point until the positions were rebalanced.

A different way to describe the above is to say that UPRO can be used in such a way that it provides a natural hedge against fat-tail losses. Best of all, the cost associated with the hedging strategy is likely smaller than it would otherwise be through the use of negative-beta holdings, like a VIX fund, or the purchase of put options.

UPRO can be used responsibly to expose growth investors to the potential upside in the S&P 500 while protecting the portfolio against sizable, fat-tail-type losses.

In addition, allocating more (or less) to the leveraged ETF can offer investors the ability to increase (or decrease) their exposure to the S&P 500. For instance, a 40-60 portfolio in UPRO and cash would likely better match the risk appetite of a more aggressive growth investor, something that cannot be easily achieved through stock picking or unlevered ETF investing.