M. Suhail/iStock Editorial via Getty Images

M. Suhail/iStock Editorial via Getty Images

Ulta Beauty (NASDAQ:ULTA), one of the leading beauty retailers in the U.S., ended 2023 on an underwhelming note.

Despite results that beat expectations, there were several flaws in the print, including lackluster guidance, low comparable sales, and a questionable international expansion strategy.

Let's see if Ulta is now attractive following the earnings selloff.

I started covering Ulta on Seeking Alpha back in October of 2023. Initially, I rated Ulta a Buy, as it was oversold amid increasing theft, decelerating growth, and worries about a pressured consumer.

My thesis was that the 15x P/E Ulta was trading at was extremely attractive, and made it a pure value play, although I said I don't think Ulta can return to its historical mid-twenties P/E, not until it shows it has a path to accelerate growth through international expansion.

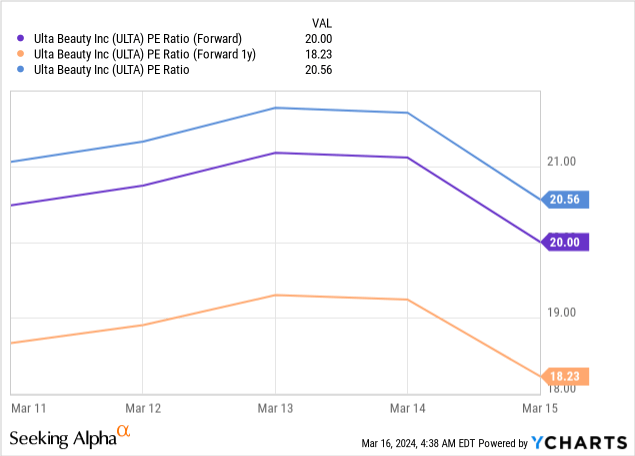

Less than three months went by, and the stock recovered all the way back to a nearly 20x P/E, despite no material improvement in its fundamentals. This has led me to downgrade the stock to a Hold.

Today, following the selloff, Ulta is trading in the 20x range, both on 2023 EPS and 2024 expectations, which stand at low-single-digit growth.

These levels are still materially below historical levels, which begs the question of what changed, and as we showed in previous articles, what changed is Ulta's growth outlook.

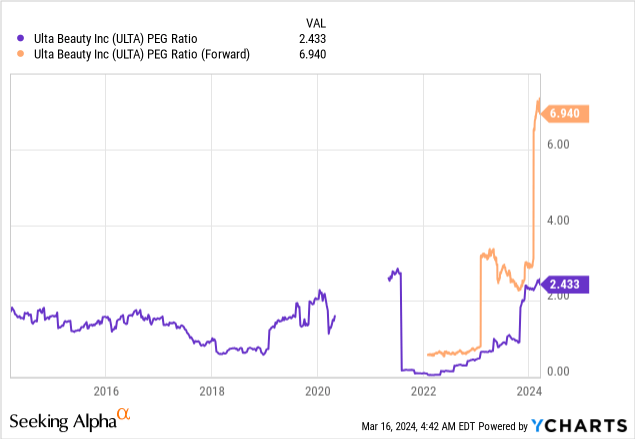

Today, Ulta might be trading at a relatively low P/E, but it's trading at a record high PEG for the company, at more than 6.9x over 2024 EPS growth expectations.

So, once again, we need to see if Ulta can flip the switch on its growth trajectory. First, let's dig into the recent quarter's results.

Ulta had revenues of $3.6 billion, up 10.2% Y/Y, primarily due to the extra week in the fiscal period, and a smaller contribution from comparable sales of 2.5%. Revenues came slightly ahead of expectations.

Gross margins were 37.7%, in line with historical discount activity in the fourth quarter due to holidays.

Operating margins were 14.5%, a 140 bps improvement over the previous quarter and a 60 bps improvement over the prior-year quarter.

Net income was $394 million, reflecting 11.1% margins, which is a 110 bps increase from Q3'23 and a 50 bps increase from Q4'22. Earnings also came better than expanded.

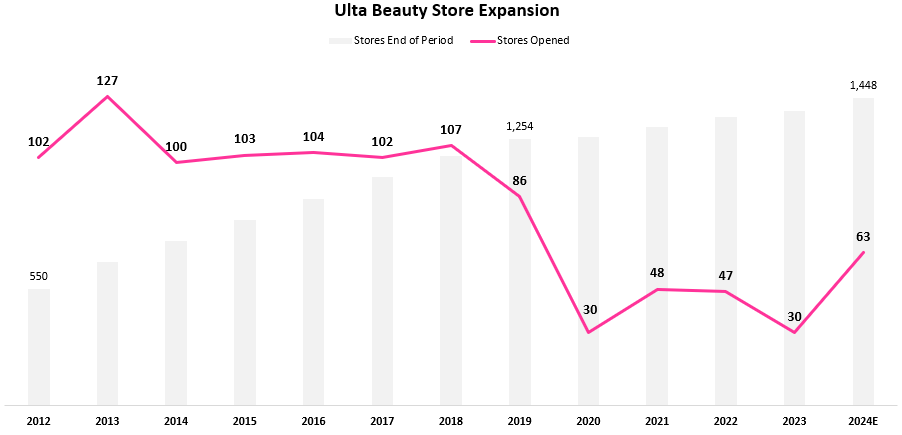

Operationally, Ulta ended the year with 43.3 million loyalty members, and 1,385 stores, with 30 net openings during the year.

One of the main themes in my previous articles was the fact that Ulta is waiting too long for an international expansion. This raised worries about the relevance of the brand worldwide, and its potential to succeed in developed markets in Europe where rivals like Sephora and Douglas already have a very significant presence.

Created by the author based on data from Ulta Beauty's financial reports.

As we can see, since 2020, Ulta has decelerated from a range of 100 store openings annually to a much smaller 30-50 pace. This of course limits the company's growth prospects, as geographic expansion remains the number one driver of growth for a mainly physical retailer.

In 2024, the company expects to accelerate to 63 openings at the mid-point of guidance, which is better, but still way below the pre-pandemic pace.

Created by the author based on data from Ulta Beauty's financial reports.

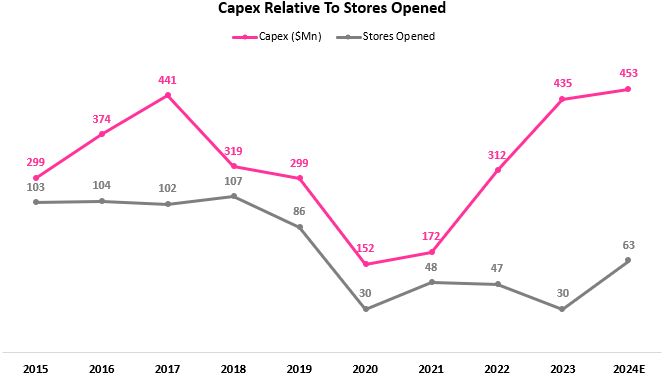

Moreover, we showed that fewer openings didn't translate into better capital spending over the past couple of years, as Ulta spent heavily on renovation, building a digital presence, and improving store security amid rising theft.

For 2024, there's a more balanced investment plan, although we can see that in 2017, a similar level of investment resulted in 102 openings, almost double what the company plans for 2024.

Despite the pickup, there's no change in plans as to their long-term target footprint in the U.S., which is slowly approaching.

With the low-end of management's footprint targets in the U.S. on the near horizon, the pressure to expand internationally continues to increase.

Finally, management announced their plans to expand outside the U.S., but I don't think this is exactly what investors anticipated. Ulta announced its plans to expand to Mexico, through a partnership with Axo, a retail operator. In other words, it seems Ulta chose to go with a franchise model, which is quite surprising.

Unfortunately, they essentially dismissed questions about the decision during the call, and analysts didn't pressure them into more information.

In management prepared remarks, they cited competitive reasons as the reason for the cloudiness:

As a result of this partnership approach, we do not expect this venture to be material to our financials in fiscal 2024. For competitive reasons, we're not sharing more details today, but we'll provide updates as appropriate.

--- Dave Kimbell, Chief Executive Officer

Then, when asked about the decision to go specifically with Mexico, they said the following:

After careful evaluation of many market opportunities, we really felt like the Mexican market is the next step for Ulta Beauty for us to have this partnership with Axo. I'm really excited about this. I know that the future is going to be really bright in this partnership. We spend a lot of time with their teams from a cultural perspective also, just even from the best-in-class performance with global partners that they've brought to the Mexico consumer, the Mexican consumer, our border stores are performing really, really well. And I just think it's the next natural step for us as we continue to expand internationally. So we are really excited about this. Again, we are planning to be operational in 2025. The cost of this is built into the guidance in ‘24, so we don't feel like it's very material, but we're super excited and feel that Axo is the right partner for us to launch in this next new territory for us.

--- Kecia Steelman, President and Chief Operating Officer

I don't see much more information here, aside maybe from the fact their border stores are performing well.

A franchise model is peculiar, in my view. If Ulta is making about 15% operating margins in the U.S., generally a more profitable region than Mexico, how is a franchisee going to make meaningful profits?

While Mexico shares a border with the U.S. and could be an easy geography to enter logistically, it really doesn't provide any hope for a significant growth acceleration in the near to mid term.

They said they plan to go operational in Mexico in 2025, and I guess we'll have to keep waiting for more news about international expansion in the future.

However, I'm becoming more and more pessimistic on that front.

UB Media, which stands for Ulta Beauty Media, is Ulta's attempt at monetizing its loyal membership base, currently amounting to 43.3 million members. Through UB Media, Ulta offers brands the opportunity to advertise to a very targeted cohort in beauty, which sounds quite appealing.

That said, we don't really know how the business is progressing, as they don't break out its numbers.

When asked about it, the CEO said the following:

We're not sharing, we haven't shared, and we don't plan to share specific on number of brands or even specific financial impact at this time. But what I will say is we're really pleased with the progress that we've made in 2023 and are confident that we'll continue to grow this part of the business. The network that we have offers advertising access via off-site display, video, social influencers, as well as on-site sponsored products. Our on-site display inventory is one of the actually new core offerings that we activated just in 2023. So we've got a full suite of ad inventory experiences, value-added services, and as I said, we're confident in its impact going forward. And the support engagement reaction from brands has been very positive. As you know, the advertising world continues to evolve. So the value that we can bring through first-party data with 43 million beauty enthusiasts is very meaningful, and we continue to work with our brand partners, and they have demonstrated to us that they see a positive return and we're continuing to grow that business.

--- Dave Kimbell, Chief Executive Officer

It's hard to gauge whether or not the initiative is successful, but considering Ulta's financials aren't materially different, and operating margins remain at low levels historically, I estimate the presumably higher-margin ad business is still relatively very small.

As investors digest no major announcements for another year and with the realization other pillars like UB media are not going to be contributors to growth in the near to mid term, management made sure to provide underwhelming guidance for 2024 as well.

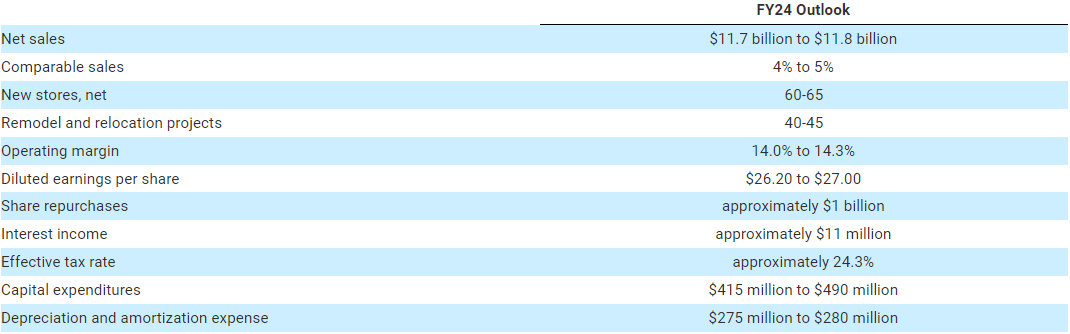

Ulta Q4'23 Earnings Release

Aside from the higher number of openings (which was anticipated), most of the guidance was either in line or below expectations.

Prior to the report, consensus estimates were for revenues of about $11.7 billion, and EPS estimates were $27.00, reflecting expectations for higher margins.

All in all, considering all that we discussed, I'd say the selloff was more than justified.

Ulta's cash conversion over the last years has been in the 60% range, as higher capital investments more than offset slightly better working capital management.

That said, I believe the right way to evaluate Ulta is using its P/E ratio, as we've clearly seen over the past year.

In previous articles, I showed Ulta used to trade much higher in the 25x-40x range during its much higher growth period, and that post-pandemic, the P/E slowly declined to below twenty, as growth deceleration became more and more a reality.

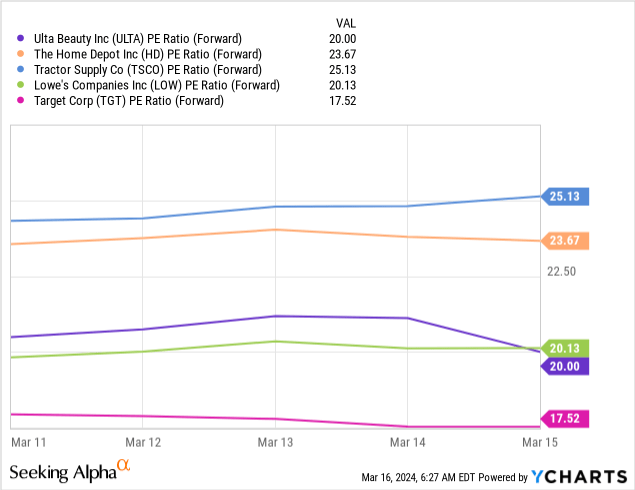

Stacking up Ulta against other specialty retailers, we can see that its valuation is somewhere in the middle of the pack, while all of the names in the list are expected to grow at a pretty similar pace in 2024.

With Ulta, we should also take into account that it operates in the resilient faster-growing beauty category, which is arguably more attractive than the rest of the names here.

Considering Ulta's questionable international expansion plans, slowing growth, and continued margin pressures, I find Ulta fairly valued.

Ulta had a decent fourth quarter, but an underwhelming guidance and a questionable franchising plan in Mexico were rightfully received badly by investors.

I don't see a catalyst on the horizon that will send the stock back toward historical valuation, as growth deceleration and margin pressures persist.

At today's valuation, I view Ulta as a Hold, although investors who bought the stock in the October trough should consider selling and allocating money into more attractive investments.