DANIEL SLIM/AFP via Getty Images

DANIEL SLIM/AFP via Getty Images

Frontier Airlines (NASDAQ:ULCC) reported fourth quarter earnings and full year 2023 earnings on the 6th of February. It seems shareholders have liked the results and guidance provided by management as the share price increased from $5.15 to $7.32, a surge of more than 40%. In this report, I will be analyzing the results, the guidance for the upcoming quarter and full year, as well as the initial expectations for 2025.

Frontier Airlines

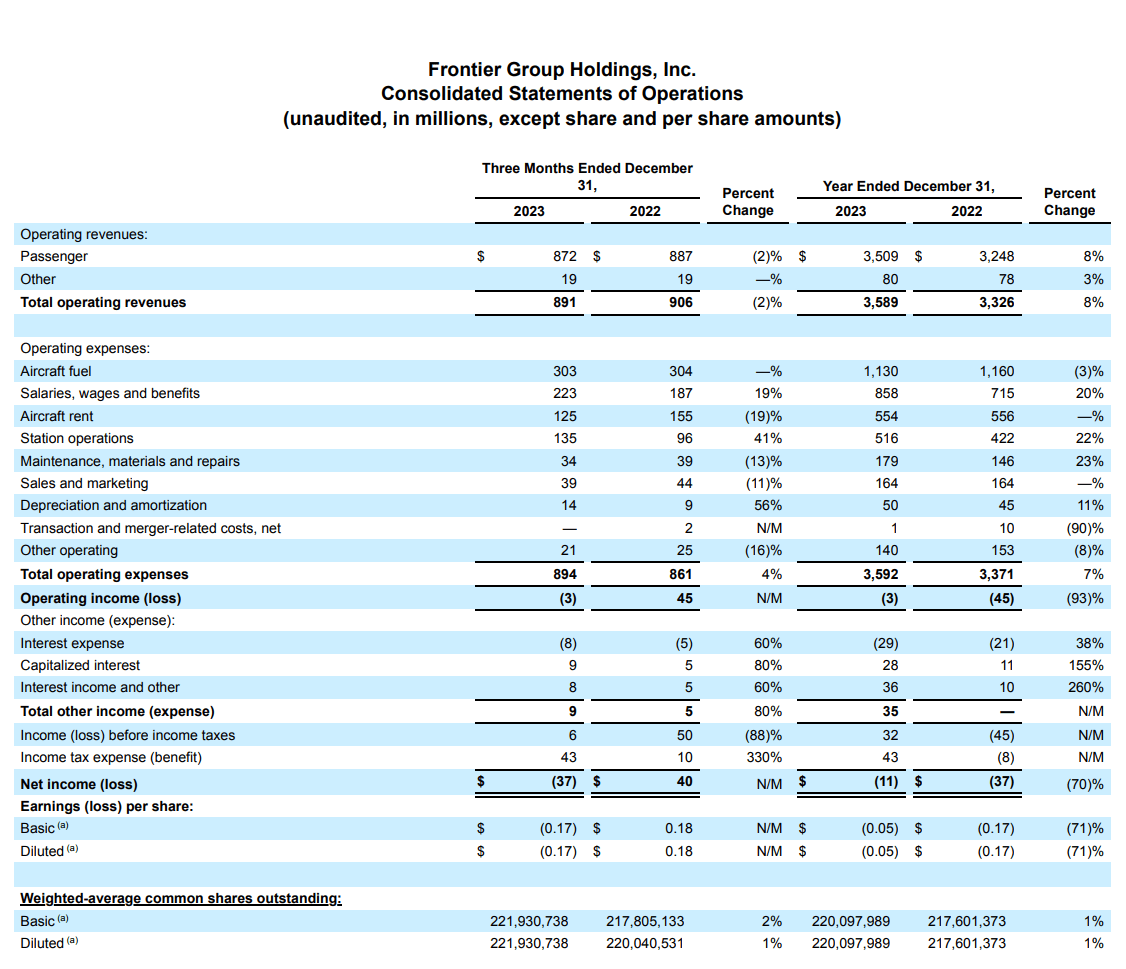

Frontier Airlines initially had guided for adjusted fourth quarter pre-tax margins of negative 6 to negative 9 percent. Adjusted pre-tax earnings, however, came in at a $7 million profit reflecting a 0.8% adjusted pre-tax margin. While it certainly is not a huge margin, it was significantly better than what the company had guided for driven by operational performance and better cost control. A look at the numbers shows that costs excluding fuel, which can be seen as controllable costs, were $591 million while the company had guided for operating expenses of $655 million to $665 million. The lower costs drove margins up by 7.5%-8.5%. So, in some way you could say that the strong cost control during the quarter resulted in the strong beat. Year-over-year, costs excluding fuel were 6% higher driven by higher salaries, wages and benefits as well as higher depreciation as the company's fleet continues to grow partially offset by lower aircraft rent, maintenance and marketing costs as well as other operating costs. While costs grew 6% capacity grew 15% resulting in an 8% reduction in unit costs excluding fuel.

Revenues declined 2% year-over-year on a 15% increase in capacity, so unit revenues were eroded and that is driven by a significant oversupply on leisure capacity.

So, the fourth quarter showed capacity increases exceeding the 12 to 14 percent guide, but pressure on unit revenues while cost control was strong.

For the full year, the unit cost pressure also radiated on the top line with an 8% increase in revenues on a 19% increase in capacity while unit costs excluding fuel declined 6% and 11% on an adjusted basis resulting in near-even operating break-even margins and a slight improvement in net income from a $37 million loss last year to a 11% loss this year.

Looking at the results, I am not quite satisfied. The demand environment for air travel is strong but overall, we are seeing that the business is failing to generate a sound profit. The company has elected to prioritize unit costs reductions over preserving strength in unit revenues and it does show quite clearly in the results.

Frontier Airlines

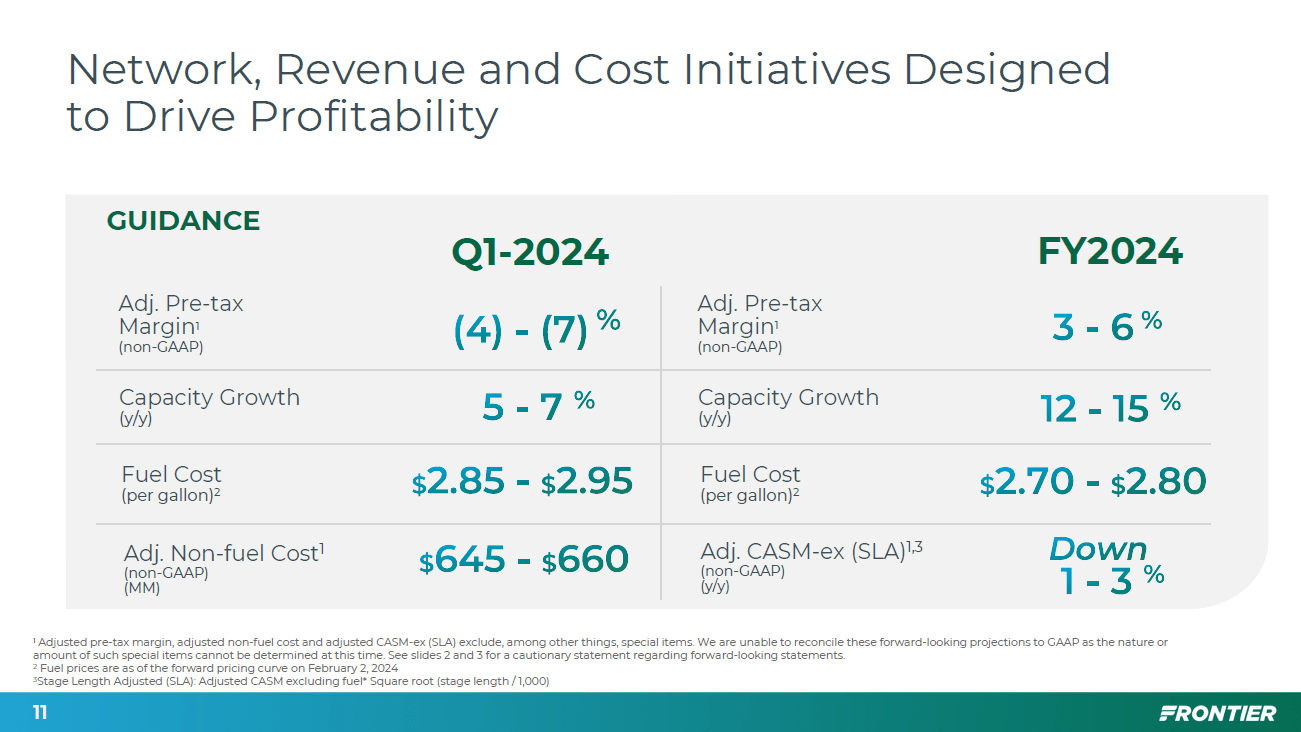

For the first quarter of 2024, Frontier Group is targeting 5 to 7 percent capacity growth 4 to 7 percent loss margins on $645 million to $660 million in non-fuel costs. The first quarter is a seasonally weak one so that is generally a quarter in which many airlines are happy with near break-even margins or to make up for the losses from Q2 onwards. Interesting is the company's guidance for non-fuel costs as it indicates that sequentially the company does expect to see higher costs again.

For the full year, the company is targeting continued capacity growth of 12 to 15 percent to bring unit costs down by 1 to 3 percent and adjusted pre-tax margins of 3 to 6 percent. Given that the company is seeing top line pressures, the continued increase in capacity could pose to be problematic. However, the company aims to reduce its capacity in some leisure market and direct them more towards visit friends and family markets as those could provide better revenue strength than the leisure market which is currently oversupplied. So, the capacity is increasing but the company also intends to shift more capacity into more premium revenue segments. Furthermore, the company is simplifying its network with airplanes returning to base overnight as much as possible. The network simplifications should have annual run rate savings of $200 million.

It seems that current analyst estimates do not yet include those targeted savings. If we would assign half of the savings to be realized in 2024 with full savings achieved in 2025, we would get to EBT margins of 2.8% for 2024 and 8.2% for 2025. For 2025, the company is targeting 10 to 14 pre-tax margins. To me it seems that even if we add the cost savings to the projections by analysts, we don't quite get to the targeted margins. So, Frontier Group's ability to increase its margins to the targeted levels is going to depend greatly on the success it has in shifting capacity away from the leisure market into the "visit friends and family" markets to a level that is beyond what analysts currently have modelled.

Frontier Airlines has shown strong cost control in the fourth quarter and for 2023 it aims to shift capacity into better yielding markets as the leisure travel market seems to be oversaturated. This seems to be a prudent decision by management. However, the company really has to perform on the top line as it capacity additions will only yield unit cost reductions of 1 to 3 percent whereas in a stable cost environment meaning no significant inflation on costs and particularly in labor costs the targeted would be 5 to 6 percent. The company is aiming to reduce costs by $200 million annually, which should be fully visible by 2025. However, whether that will be enough needs to be seen. Current analyst estimates suggest that that is not the case and unfortunately, the company provides no balance sheet data or cash flow details in its 8K filing which prevents me from updating my price target and rating at this point from fundamental perspective.

In November, I put a $7.31 price target on Frontier Airlines stock and that price target has been fully realized marking a 87.2% gain. However, I believe that given the cost reduction initiatives and capacity shifts targeted to optimize revenues there could be further upside. Hence, I am maintaining my Hold/Speculative Buy rating for Frontier Airlines stock.