whyframestudio

whyframestudio

Intuitive Surgical (NASDAQ:ISRG) has enjoyed a massive run since the start of the year. It all started with the pre-release of ISRG's full year FY23 earnings, which was followed up with some game-changing forward-looking commentary that came out from the J.P. Morgan Healthcare Conference at the start of the year. The actual earnings release of ISRG's full year FY23 earnings report, a couple of weeks after the healthcare conference, didn't throw any major surprises since the cat was already out of the bag. Management did try to temper optimism during the FY23 earnings call by adding the dimension of uncertainty to their outlook.

I will admit that I initially factored in management's expectations word for word when doing an initial analysis. However, as we near the end of the earnings season, I had the benefit of combing through the earnings reports of some medical care facilities and healthcare systems, and I am now convinced that the outlook for ISRG is not as uncertain as its management previously revealed.

At the moment, ISRG is already up ~20% for the year, easily beating all major benchmark indices and richly trading at ~60+ times forward earnings. I will assign a Hold for now, but the macro certainly looks better, and the stock looks set for a banner year.

Intuitive Surgical is a market leader in the world of robotic surgery equipment. Its da Vinci product line is the breadwinner for the company. The da Vinci product is a robotic surgery system used by leading hospitals in the U.S. and the world over to assist surgeons in a range of complex surgical procedures, including colorectal, gynecological, and urological procedures. Most of these procedures are performed in an inpatient setting at hospitals and Integrated Delivery Networks (IDNs) such as Mayo Clinic, Cleveland Clinic, etc. Per its FY23 earnings report, the company has over 8,600 da Vinci systems installed in medical care facilities across the world. The U.S. accounts for ~60% of the company's da Vinci installed base.

Intuitive Surgical's da Vinci product line, Intuitive Surgical website

ISRG's robotic surgery systems are generally expensive to procure. For example, its da Vinci systems sell for between $0.7 million and $2.5 million per unit, as revealed in the recently filed FY23 10-K. The purchases made by ISRG's customers are generally recorded as capital expenses by the company's clients.

The company's revenue model is primarily based on upfront sales of its robotic systems, which also include its Ion endoluminal robotic systems in addition to the da Vinci systems. Per the presentation at the conference I mentioned at the start of this research note, ~83% of its revenue is generated from recurring revenue. The company earns recurring revenue from every surgical procedure done on its installed robotic systems. It estimates that for every surgical procedure done, it will earn between $700 and $3600 worth of instruments sold to the institution per procedure. Hence, procedures are an important forward metric for the company.

On Thursday last week, Universal Health Services (UHS), one of ISRG's clients, provided some positive updates, which added favorable context to the macro outlook for ISRG. UHS reported their full year FY23 earnings report last week and is projecting to raise their capex spend in FY24 by ~24% to just under a billion dollars. This represents a substantial jump from the ~1% increase in capex that the healthcare services company recorded in FY23. UHS had recently launched ISRG's Ion robotic surgery program for lung care in November last year. In FY23, ISRG reported a monster-sized 129% growth in Ion procedures.

On the call, UHS's management mentioned that they are also seeing their competitors expand capital deployment when asked to comment about general capital deployment trends in this space. One of UHS's competitors, HCA Healthcare (HCA) was bullish about its outlook for inpatient surgeries on the back of the 2% growth in patient surgical volumes it saw last year. HCA's management is forecasting their capex to grow by ~10% this year, up from the ~6% annual increase in capex last year.

To see industry-wide inpatient surgical procedures rising is a positive sign for ISRG. This change in the dynamic for inpatient surgical procedures, combined with the increase in capital spending that medical care facilities are committing to, elevates the prospects of higher equipment sales and recurring sales for ISRG. I had mentioned in the previous section that with every surgical procedure, ISRG earns between $700 and $3600 worth of sales in surgical instruments. Moreover, higher projections for capital spending in the healthcare industry translate to the possibility of higher sales of ISRG's robotic surgery systems and equipment.

Hospitals and healthcare facilities have mostly subdued their capital spending cycles in the last two years, but I suspect things are about to change with surgical procedure volumes improving in the industry.

In FY23, ISRG reported a solid growth in surgical procedures, growing 22% y/y with surgical procedures related to general surgery and gynecology outpacing the growth of urological procedures, as seen below.

Procedure growth by procedure volume, company sources

This surge in procedures is a boon for ISRG because capital sales are ultimately driven by procedure demand, catalyzing hospitals to establish or expand robotic system capacity. Although ISRG's management is guiding for a far lower 13-16% growth in surgical procedures this year, citing uncertainty in the macroeconomy, I suspect management used this guidance as a tool to temper expectations. Also, note that management cited similar macroeconomic uncertainty reasons when guiding their FY23 projections last year. But with the ISRG's clients starting to give much better bullish outlooks in their respective capex plans as well as their inpatient surgical volume outlook that I had noted in the earlier section, I am confident that the company is positioned to significantly beat their FY24 procedure growth.

On the revenue front, the strength in ISRG's surgical volume metric is trickling down to the company's top line as well, with total revenues rising 13% in FY23 to $7.1 billion.

Revenue growth, company sources

The company saw meaningful growth in its top line, but the company is continuing to see a huge boost from its recurring revenue model. One part of ISRG's recurring revenue model equation is the revenue it earns from sales of surgical instruments per robotic surgery procedure, which grew 22% y/y, faster than the company's total revenue growth pace. The other side of the recurring revenue model equation is also its operating lease revenue, which grew 33% y/y in FY23. Since the cost of the company's surgical systems is in excess of half a million, as reported earlier, part of the company's strategy is to structure its sales agreements with its clients in the form of operating leases, spreading out the cost of its systems over time.

In addition to being financially obligated to ISRG, its healthcare clients that enter into such operating lease agreements also have to agree to commercially competitive clauses that are structured to favor Intuitive Surgical over its competitors. These strategies help create a huge moat and drive up switching costs for its clients, which is why I continue to expect ISRG to maintain its dominant market share in robotic surgical equipment.

This report suggests that the robotic surgery market is expected to grow at a CAGR of 11% through FY26. While reviewing data from the report and from ISRG's earnings report, the company currently has ~70% market share in the robotic surgery space. I expect ISRG to continue to grow faster than the market, driven by the significant ramp in its product line and an elevated business strategy. This means ISRG will continue to penetrate the market as a result.

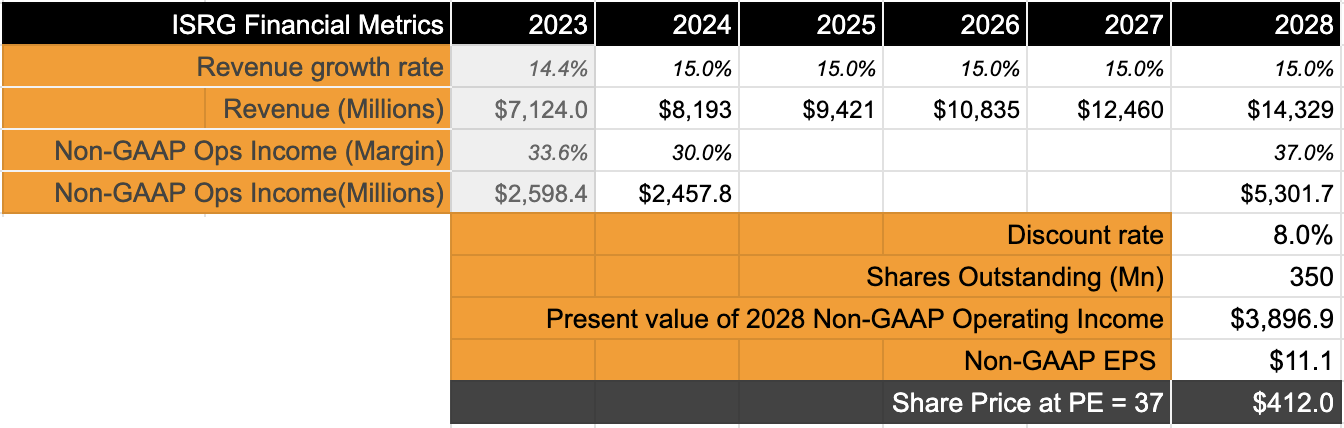

I have updated my projections for revenue estimates below, slightly higher than consensus estimates. I feel encouraged to upgrade my projections after viewing the favorable macro-conditions return in ISRG's favor. Per these estimates below, ISRG's revenue will grow at a CAGR of 15%, higher than the 13.3% compounded growth per consensus estimate over the same period.

Author's model

I expect a contraction in operating margins this year due to the launch of ISRG's da Vinci 5, which I expect will secure the necessary FDA approval later this year. Over a 5 year period, I expect operating income to grow by a compounded growth rate of 21.2%. This would imply a forward P/E of 35-37, given such impressive growth rates.

However, my model shows that ISRG is currency trading in a range that implies the stock is fairly priced with minimal upside.

Competition is always a risk, even in the case of a dominant force like ISRG. The likes of Stryker (SYK) and Medtronic (MDT) pose some threat to ISRG's market share, along with Johnson & Johnson's (JNJ) pre-pandemic acquisition of Verb Surgical. Medtronic launched its own robotic surgery system called Hugo in 2022 to address the cost and utilization barriers posed by ISRG's robotic surgery products. But I do not expect it to make a meaningful impact on ISRG's market share due to the pace of innovation demonstrated by ISRG.

However, risks such as macroeconomic slowdowns or a sudden shock recession may pose severe threats to ISRG's growth prospects. In addition, if there is a shift from inpatient to outpatient medical care, ISRG could be impacted by pricing pressure as well as a drop in robotic surgical procedures, leading to lower recurring revenue.

Intuitive Surgical continues to impress me with an impressive show of strength in its earnings report for FY23. As discussed in the note, macrotrends in hospitalization and inpatient care are turning into tailwinds for the robotic surgery company. Still, ISRG's 20% run-up through the first two months of the year has significantly expanded forward valuation multiples, leaving little room for upside. I will rate this as a Hold for now, but I am encouraged by the long-term prospects of this stock.