claffra

claffra

Gasoline is a seasonal fuel, falling in winter and rising in spring and summer when drivers put more clicks on their car’s odometers. The recent price action in crude oil, turmoil in the Middle East, the U.S. election, and the low level of the U.S. Strategic Petroleum Reserve are reasons gasoline prices could soar over the coming months.

In a December 2023 Seeking Alpha article, I concluded:

As we move toward 2024, and the 2024 driving season begins around May, buying UGA on significant dips could be the optimal approach to gasoline investing for the coming year. Crude oil and oil product markets are highly volatile. As we learned over the past years, prices can move to illogical, unreasonable, and irrational levels on the up and downsides. Therefore, leave plenty of room to add on further declines as surprises over the coming weeks and months could cause significant price variance. However, the odds favor higher gasoline prices during the 2024 driving season above the current prices on the forward curve at the end of 2023.

Nearby NYMEX gasoline was at the $2.17 per gallon wholesale level on Dec. 18, 2023, with the UGA ETF at $62.69 per share. On Feb. 27, nearby gasoline futures were higher at nearly $2.60 per gallon, and UGA was trading above $67 per share.

The price action in crude oil and gasoline futures has made rounding bottoms since late 2023.

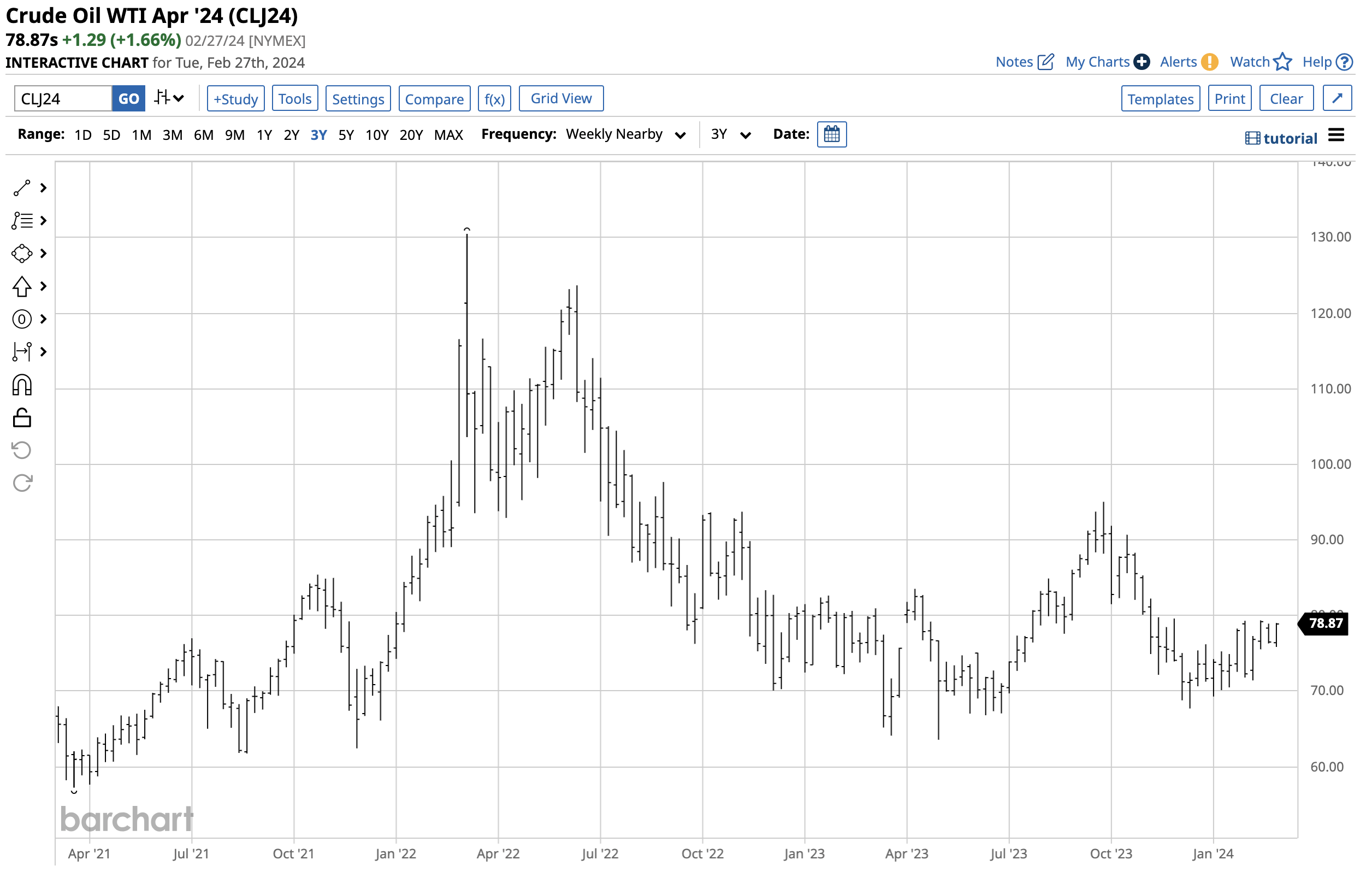

Weekly NYMEX Crude Oil Futures Chart (Barchart)

The weekly NYMEX WTI crude oil futures chart displays a higher low in mid-December 2023 at $67.71 per barrel.

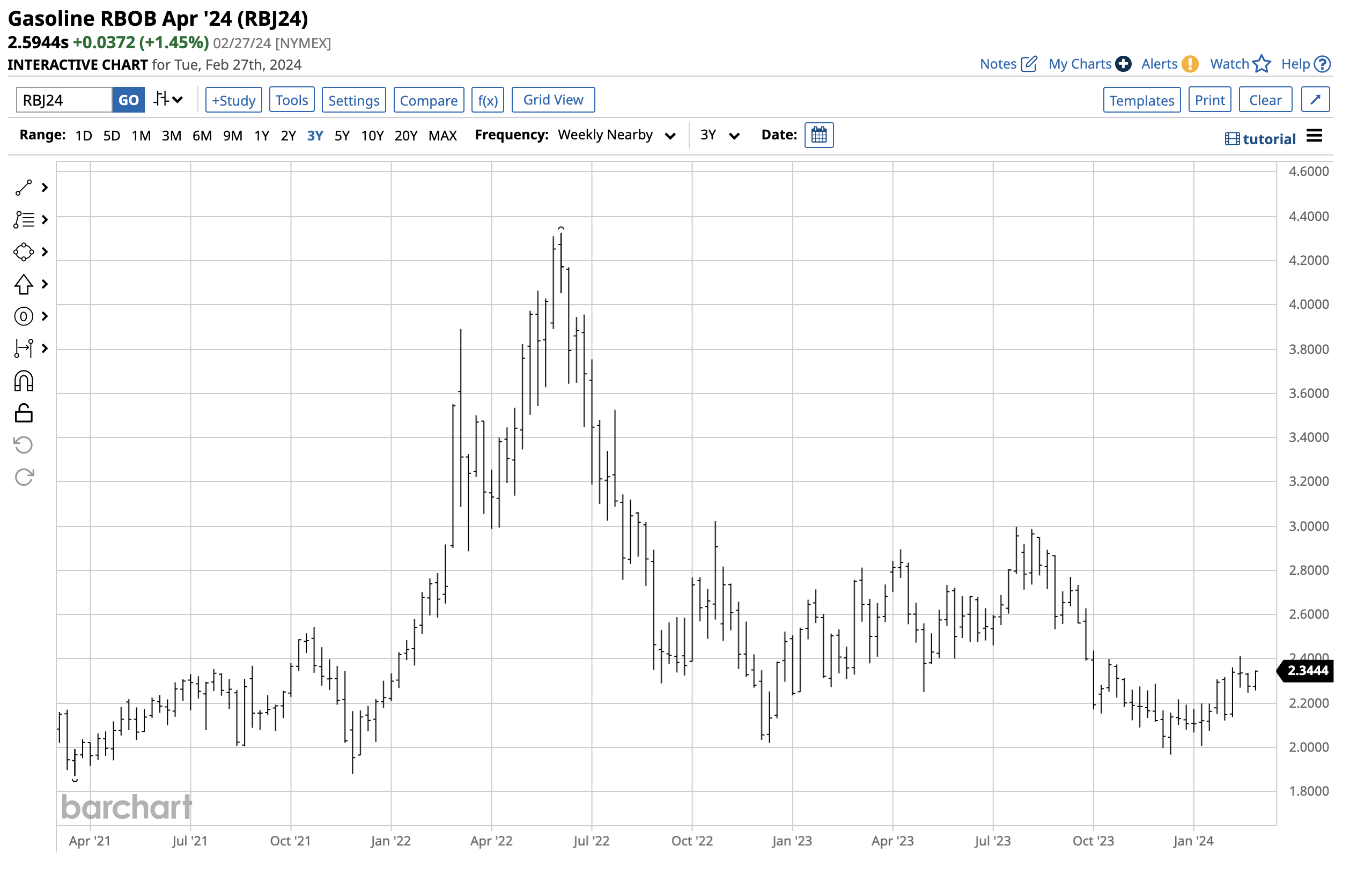

Weekly Gasoline Futures Chart (Barchart)

Gasoline futures show the same pattern as crude oil, the primary ingredient refined into the fuel. Gasoline futures traded to a $1.9672 per gallon wholesale low in mid-December 2023.

At $78.87 and $2.5944 on Feb. 29, April WTI and gasoline futures were 16.5% and 31.9% higher, respectively. Seasonality accounts for gasoline’s outperformance as the fuel tends to trade to lows during winter. The April contract reflects the price as the demand increases when the weather conditions improve.

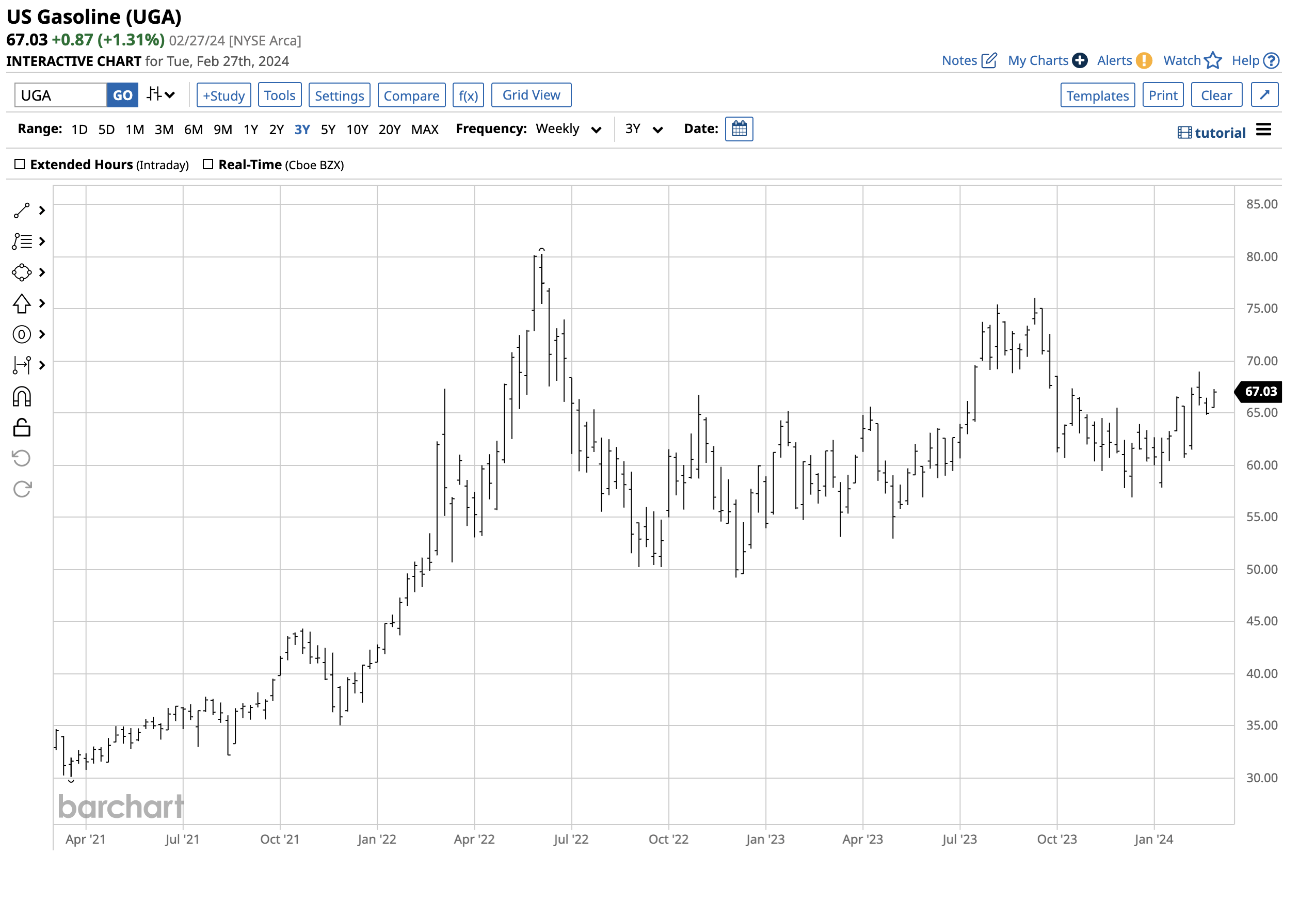

The United States Gasoline Fund, LP ETF (NYSEARCA:UGA) product has increased since mid-December but has underperformed WTI crude oil and RBOB gasoline futures.

Weekly Chart of the UGA ETF Product (Barchart)

The chart highlights UGA’s 8.8% rise from $61.63 in mid-December to $67.03 per share in late February. The ETF’s price action reflects the fuel’s seasonality. UGA’s Fund Profile describes the ETF’s structure:

Fund Profile for the UGA ETF Product (Seeking Alpha)

UGA tracks the near-month NYMEX gasoline futures contract until two weeks before expiration, when it rolls to the next contract month.

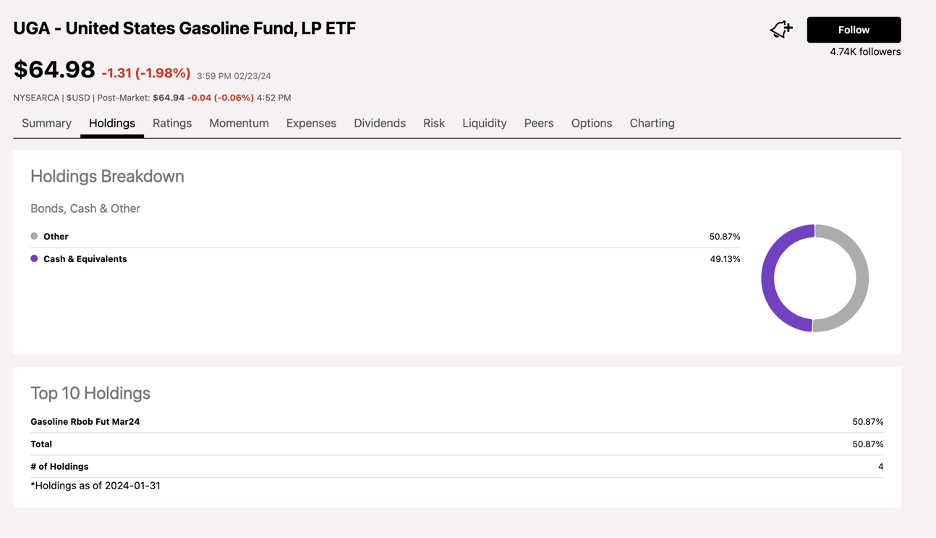

Top holdings of the UGA ETF Product (Seeking Alpha)

UGA’s top holdings as of Jan. 31 show it held the March contract that rolled to April in February. Since the price differentials between contract months can be volatile, an investment in UGA involves roll risk from nearby to the next active month contract, which can add or subtract from investment results.

Markets reflect the economic and geopolitical landscapes which offer contrasting prospects for crude oil and gasoline prices in late February 2024. While U.S. economic growth is surprisingly strong, the Chinese economy remains lethargic. Meanwhile, geopolitics are decidedly bullish.

The ongoing war in Ukraine and U.S. energy policy under the Biden administration has strengthened OPEC+’s role in determining worldwide crude oil prices. The cartel remains committed to balancing petroleum fundamentals to optimize returns for its members, causing prices for Brent and WTI crude oil futures to stay above $82 and $77 per barrel for April delivery,

Moreover, the conflict in the Middle East has increased tensions between the U.S. and Iranian-backed militias. The rising potential for hostilities has caused supply and price fears as the Persian Gulf and Straits of Hormuz are critical logistical chokepoints for petroleum. Given the U.S. administration’s commitment to addressing climate change that inhibits fossil fuel production, the Middle East plays a leading role in the path of least resistance for oil prices.

The Biden administration released unprecedented crude oil from the U.S. Strategic Petroleum Reserve after prices rose to the highest levels since 2008 at over $130 per barrel in March 2022. After peaking at over 600 million barrels in late 2021, the U.S. SPR was at the 360.3 million barrel level on Feb. 27. While recent purchases caused the U.S. strategic stocks to increase to the highest level since May 2023, they are still nearly 40% below the level in late 2021.

With nearly a quarter-of-a-billion barrels left to purchase to boost the U.S. SPR to pre-2022 levels, the administration’s plans to replenish the reserves at $67 to $72 per barrel, provides significant support for the energy commodity, which is above the top end of the administration’s target range.

Another factor supporting crude oil and gasoline prices is seasonality. Gasoline is the most ubiquitous crude oil product, and with March beginning at the end of this week, the spring is just around the corner. As the weather improves, drivers will put more mileage on cars, and gasoline demand will increase. The upcoming summer vacation period is when gasoline demand and prices reach seasonal peaks.

Gasoline prices have been trending higher since the mid-December 2023 winter low.

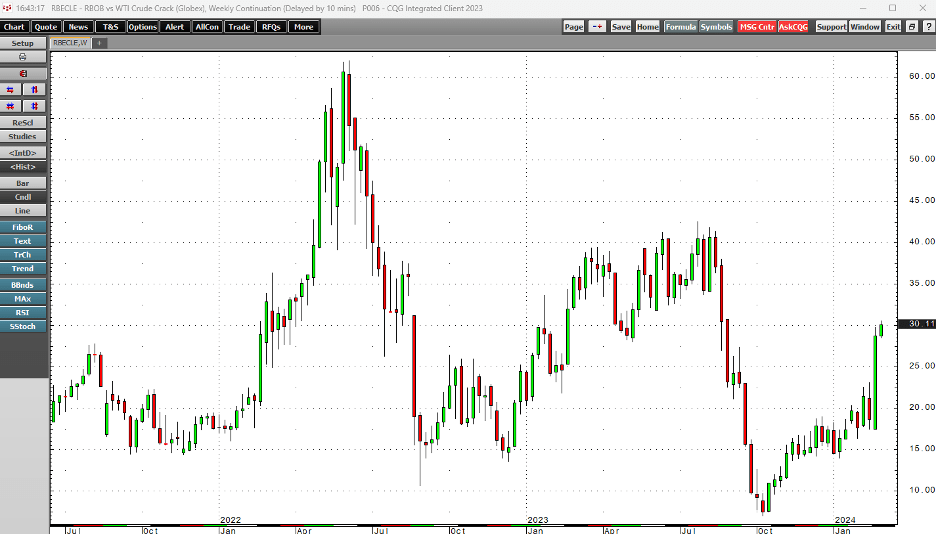

Weekly Chart of the NYMEX Gasoline Crack Spread (CQG)

The weekly chart of the gasoline crack spread highlights the rise from $7.04 in December 2023 to over $30 per barrel in late February 2024. Seasonality accounts for the rising gasoline processing spread as refineries increase gasoline output.

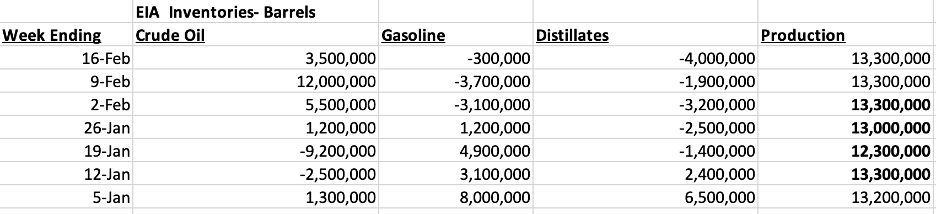

EIA Crude Oil and Oil Product Inventories in 2024 (EIA)

Source: EIA Weekly Inventories

The chart shows that EIA crude oil stockpiles rose 11.8 million barrels since the end of 2023. While gasoline stocks were up 10.1 million barrels, distillate inventories fell 4.1 million barrels. The data shows refineries are processing more oil into gasoline, preparing for the peak 2024 driving season. Refiners expect gasoline prices to rise over the coming weeks and months.

While we are likely to see higher crude oil and oil product prices over the coming months, the most significant issue for the long term will be the outcome of the 2024 U.S. election. Democrats favor addressing climate change by supporting alternative and renewable energy sources and inhibiting the production and consumption of fossil fuels. Republicans pledge to tap into vast U.S. energy reserves with a “drill-baby-drill” and “frack-baby-frack” approach to achieve energy independence and limit OPEC+’s influence on prices.

Until the election, the administration’s energy policy approach, escalating tensions in the Middle East, replenishing the SPR, and seasonality will likely increase crude oil, gasoline, and other oil product prices.

The bottom line is the trend is always your best friend in markets across all asset classes. The oil and oil product futures markets are trending higher in late February 2024, with many fundamental factors that could provide gusts of winds in the bullish sails. I favor the UGA ETF’s upside as gasoline heads toward the peak 2024 driving season.