photovs/iStock via Getty Images

photovs/iStock via Getty Images

UFP Industries (NASDAQ:UFPI) is a supplier of lumber and building products to the manufactured housing industry. In its Q4 2023 results announced on Feb 20th, UFP Industries reported a miss on both revenue and EBITDA as a result of softer demand. In this article, I'll dive deeper into the latest full-year results of the company, assess the future outlook, and walk through its valuation to determine whether shares are a good buy at the current price.

UFP Industries supplies building products to fill a wide range of customer needs. With almost 16,000 employees and over 200 facilities across the United States, it primarily serves companies in the retail, packaging, and construction sectors. Principally, the company's largest segment, retail, which makes up 40% of sales, sells building material products that are used in the construction of residential products. This includes everything from fences, railings, plywood, chalkboard, and more that's used in both interior and exterior applications. In the packaging segment, which accounts for 25% of sales, UFP provides full-service, customized industrial packaging solutions to companies. These include things like pallets, skids, labels, boxes, and cut lumber. Finally, in construction, which makes up 35% of revenue, UFP essentially acts as a service-oriented, one-stop shop for service-oriented construction and building products needs mostly for commercial use as well as manufactured housing, RVs, and cargo trailers.

Investor Presentation

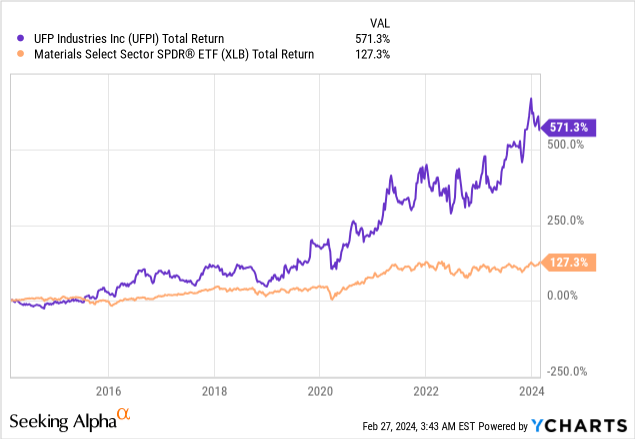

The long-term share price performance of UFP Industries has been impressive, to say the least. Over the last decade, the company's shares have returned 571.3% or a compounded annual return of 21.0%. This compares favorably to the Materials Select Sector SPDR ETF's (XLB) total return of 127.3% for a compounded annual return of 8.6%, illustrating that UFP Industries has vastly outperformed the rest of the Materials Index.

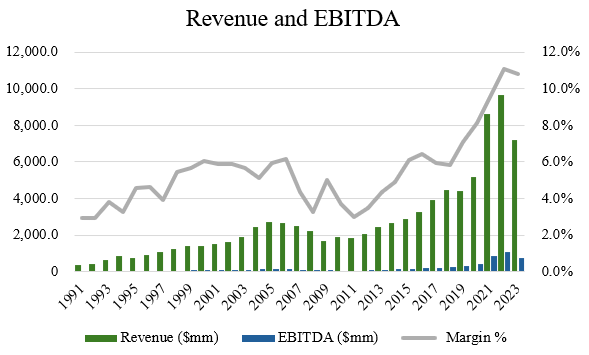

This outperformance can also be observed in the company's outstanding financial results. In the last 20 years, the company has grown revenue and EBITDA at a CAGRs of 6.9% and 10.4%, respectively. In the last decade, the results are more impressive, with revenue and EBITDA growing at CAGRs of 5.8% and 10.9%, respectively (source: S&P Capital IQ).

Author, based on data from S&P Capital IQ

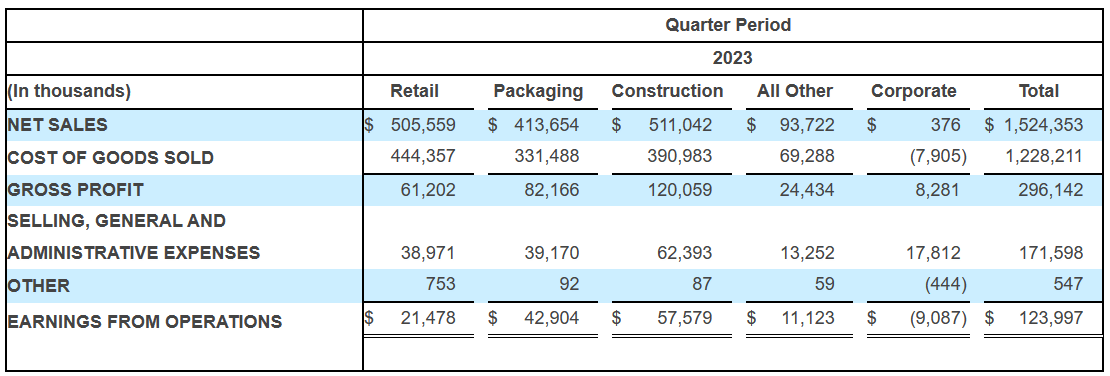

UFP Industries reported a miss on both revenues and EPS for Q4 2023. Sales for the quarter came in at $1.52 billion, which was down 20.4% from the same quarter last year (a miss on estimates by $120 million) and EPS of $1.62 fell short of consensus estimates of $1.65. On a full-year basis, revenues came in at $7.2 billion and EPS was $8.07 on a fully diluted basis.

Along with lower sales figures, this also translated over to reduced profitability and margin compression. During the quarter, adjusted EBITDA was down 22% from last year, clocking in at $166 million, which represented a 20 basis point decline to an EBITDA margin of 10.9%.

Company Filings

As a company in the Materials sector with end markets in construction and manufactured housing, UFP Industries' earnings can be relatively volatile and can swing with the economic vastitudes of the broader economy. For example, looking at the recent price action of lumber, a key material and cost input for UFP Industries, lumber is down about 28% year over year, so it's important to keep this in mind when dissecting the quarterly and full-year results for UFP Industries.

On the packaging side, this segment wasn't immune to headwinds either, down 21% (10% decline in pricing and a volume drop of 11%). Unlike consumer packaging, which held up relatively well in 2023, much of UFP Industries packaging segment is tied to lumber. These products include things like wooden pallets, skids, crates, and other protective packaging. While only 25% of revenues, the segment accounts for 30% of EBITDA, so it is a higher margin business.

Many of the company's customers in this segment have seen lower demand in their markets, which has translated to less demand for UFP Industries' packaging products. With an added steel packaging facility to add capacity and expand materials offering, the value proposition looks strong for the company long-term however and cost-cutting can already be seen in the company's results. While gross profit was down $49 million in the segment, this was somewhat mitigated by a $10 million decrease in SG&A.

Zooming out, I think it's important to reflect on the recent 5-year period that got UFP's results to where it is today. For example, for 2019, UFP Industries had total sales of $4.4 billion with EBITDA of 317.3 million. Today, those figures are 64% and 155% higher, which, as we looked at earlier in the company's long-term financial performance, suggests that UFP Industries is very much in control of its long-term future.

In my view, I think the reasons for this can be attributed to two main factors that we're a consequence of the company's operating performance and capital allocation decisions in 2023.

Firstly, despite volatile end-markets, it's important to acknowledge that UFP Industries sells a lot of value-added products compared to its competitors. With a focus on value-added products that are higher margin, have better organic growth rates, and are less cyclical, these new innovations are what's allowing UFP Industries to consistently outperform over the long-run. So even on a 5-year period where lumber prices were essentially flat, and you might have expected sales to consequently be unchanged as well, the investments the company has been making have been paying off and have been a testament to its growth.

A good example of this is the company's Deckorators product line, which is gaining both market share and reputation in the industry. While market share stats are not shared by the company, the number of specialized installers for this product line has grown to over 900 and UFP Industries has been making capex investments in the Northeastern United States to grow capacity to meet growing demand. So even with pressures in the remodeling and repair market, it's encouraging to see the company position itself for future growth.

A fair chunk of the company's products here can also be attributed to growing demand from big box retailers like Home Depot (HD) and Lowe's (LOW). A big theme here is a rebound expected in 2025 and 2026, particularly as repair and remodeling activity picks up again, and construction markets reach equilibrium.

Secondly, on capital allocation, UFP Industries continues to grow both organically and by acquisition. In my view, it's likely the sales figure wouldn't have been as low had made a few more acquisitions than it previously has done in the prior year. In 2023, the company completed only one acquisition for a company that makes wooden pallets and ceramic tiles. At a purchase price of $52 million, the acquisition was rather immaterial and inconsequential to move the needle on the sales front, with TTM revenues of $38 million. While UFP sees lots of acquisition opportunities, it noted on its conference call that it hasn't been able to close many due to elevated valuations.

To me, this isn't something to be concerned about short-term with as it demonstrates that the company is willing to wait to buy the right targets at the right price, highlighting both a focus and disciplined that's rarely seen by many companies in the space. With limited acquisition opportunities at compelling valuations, the company focused much more on organic growth initiatives, spending about $180 million in capex for the full year. Many of these investments include investments in automation, marketing, as well as technology that should improve overall margins in the future. In 2024, capex is expected to grow to $250 to $300 million.

Regarding my outlook for UFP Industries going forward, near-term, while there continues to be pressures on the macro related front surrounding higher interest rates and mortgage rates, the long-term investment thesis still remains intact. Looking out to the company's five-year plan, UFP Industries expects to achieve a compounded annual sales growth figure of between 7% to 10% with a few tuck-ins that should enable the company to meet this target. On the margin front, with 11.2% EBITDA margins for 2023, the company sees about 130 basis points of margin expansion for 2024 driven by continued value-added products, cost-cutting initiatives, and better operating capabilities.

Overall, I think the outlook for UFP Industries remains strong. With a dividend increase of 10% announced during the quarter, this highlights the company's commitment to returning excess cash to shareholders. Historically, the company has had a strong track record of maintaining a relatively low payout ratio with steady increases in the quarterly dividend year by year. Moreover, with the repurchase of 274,000 shares of outstanding shares since the announcement of the company's buyback program in July, I think this should signal to the market that the company views its shares as undervalued today. This is great for long-term shareholders as it increases their ownership stake in the company without investors having to do anything. It's a better use of capital than a dividend increase, in my opinion, because it's a non-taxable event.

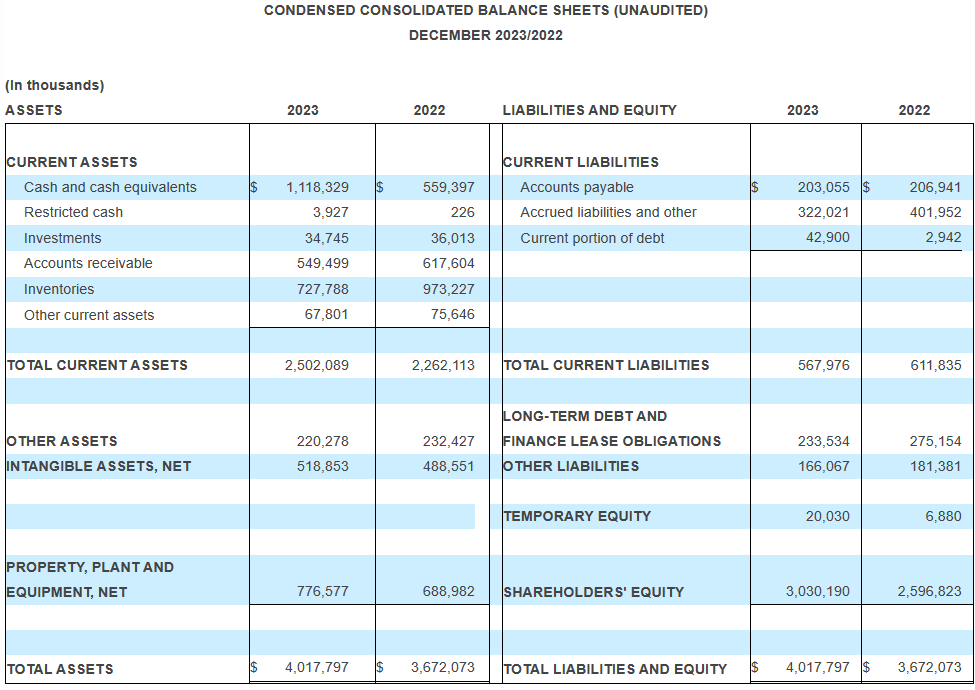

Underpinning my confidence is also UFP's relatively conservative balance sheet. At quarter end, UFP Industries had $1.15 billion of cash and $233.5 million of long-term debt. Under the company's lending agreements, it still has $1.3 billion of available room which positions it well to invest back into the business, be it organic growth initiatives or small, tuck-in acquisitions. Once valuations start to normalize to levels the company views as attractive, I think acquisitions should pick up pretty materially either later this year or into 2025.

Company Filings

Based on the 5 sell-side analysts who cover UFP Industries' stock, there are 3 'buy' ratings and 2 'hold' ratings. The average price target is $123.60, with a high estimate of $137.00 and a low estimate of $110.00 (source: TD Securities). From the current price to the average price target one year out, this implies about 10.5% upside, not including the current dividend yield of 1.2%. With a total return potential of 11.7%, this implies that analysts are moderately bullish on the near term outlook of UFP Industries' stock.

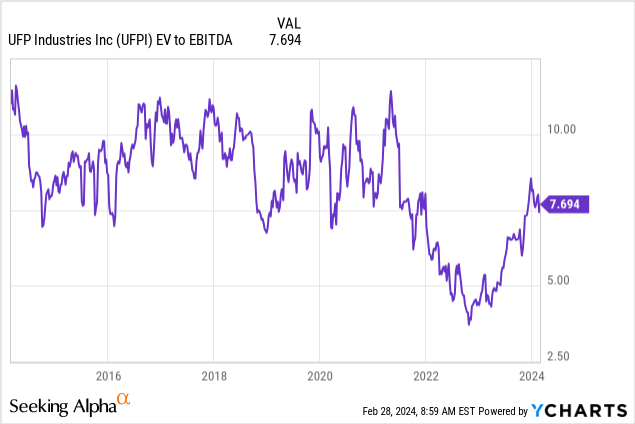

When dissecting the current valuation of UFP Industries, the company is trading at the mid-point of its historical EV/EBITDA range at about 7.7x earnings. On a P/E basis, the company is trading for around 14.1x earnings, which looks fairly reasonable for a company that's been able to grow in the high-single digits long-term.

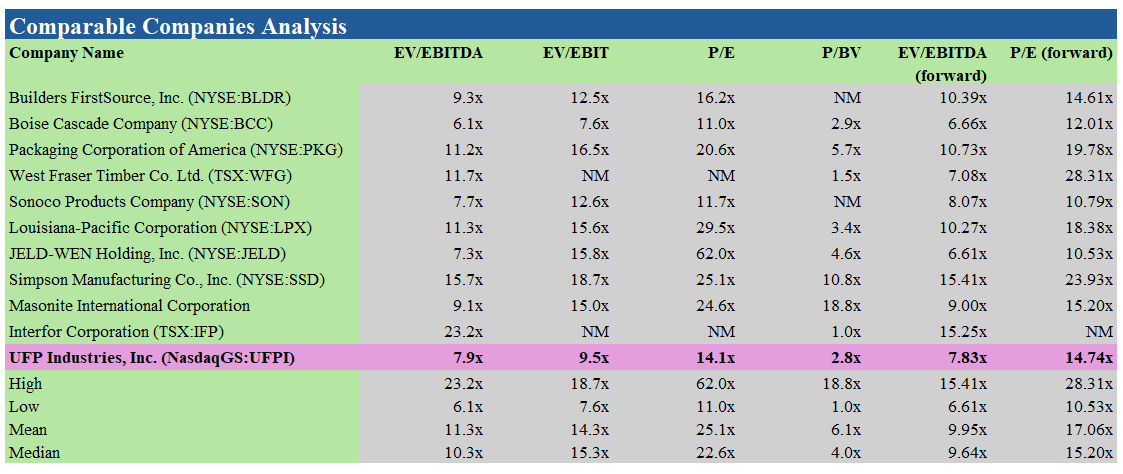

When comparing to industry peers, UFP Industries seems to be trading at a 2-turn discount on a forward EV/EBITDA basis and in line with the peer group on a forward P/E basis. Hence, trading at the mid-point of its historical valuation range and in line with the median multiple of the comps set, I would say that the valuation doesn't seem to be offering a significant margin of safety and is likely fully valued right now. For the comps set, I tried to pick companies that operate in similar end-markets to UFP Industries, have similar growth characteristics, and sell related products.

Author, based on data from S&P Capital IQ

While I believe that shares are fully valued, there's a few risk factors investors should be aware of before they make an investment in UFP Industries. Firstly, as discussed, UFP Industries is a cyclical stock. While we've seen indications that we're in a softer period in the cycle right now, it's unclear for how long the slump will last. While my expectation is that things will pick up in late 2024 and early 2025, there's no guarantee and sales could stay somewhat depressed for a while. Secondly, the company's own projections factor in some tuck-in acquisitions in the 5-year forecast. In 2023, only one acquisition was completed. So if the company isn't able to find opportunities to deploy capital efficiently, then those growth rates might be lower than expected.

In conclusion, while the full-year and quarterly results might look bad when compared to last year, I think it's important to put it into context with the results we've seen in the last 5 years as well as where the macro environment is telling us. At present, demand for repair and remodel activity is depressed, along with construction, which has put a damper on sales in 2023. Despite this, UFP Industries has been deploying capital effectively in organic growth initiatives that should pay off longer term. With an expectation for more tuck-in acquisitions in the near future, I believe the company should be able to meet its growth targets. While I'm not a buyer of the stock today due to its valuation suggesting it's likely fairly valued, I think investors who already own the stock can generate some additional yield through covered calls. As an example, the October 2024 $115 call contracts are selling for $12.00 (source: TD Securities). This represents an annualized yield of about 17.0% which looks attractive for mitigating downside risk for investors.