Dragos Condrea

Dragos Condrea

Uranium Energy Corp. (NYSE:UEC) reports Q2 2024 results with no fanfare. Revenues were non-existent. End of story, move on? On the contrary, UEC is now months away from restarting its highly anticipated production in Wyoming. That's good news. But that doesn't even start to scratch the surface of why UEC is well-positioned, with a debt-free balance sheet, ready to move higher.

Back in December, I wrote a bullish analysis of UEC where I concluded by saying,

UEC is the best uranium miner to invest in since the business is fully unhedged with its operations ready to start mining if uranium prices stay higher than $60 per lb. Note, that uranium prices have now just crossed $80 per lbs.

Since that analysis, uranium prices moved higher only to give up some ground. And yet, uranium prices are now higher at approximately $93 per lbs.

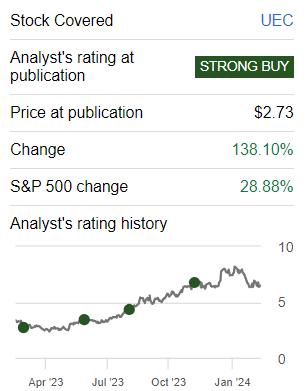

Author's work on UEC

In the past year, UEC has been a strong performer, easily outperforming the SP500. But I make the case that this investment thesis is only just getting started.

We are moving towards an energy crisis, and we are not aware of it. Two drivers of energy demand are data centers and electric vehicle batteries. While the uptick in EVs has to some extent been factored in, very few regulators have fully considered the impact of AI on our energy demand.

You mention AI, and Wall Street cheers. We all know this to be true. But AI is extremely power-hungry. Here's a quote from Bloomberg,

Electricity consumption at US data centers alone is poised to triple from 2022 levels, to as much as 390 terawatt hours by the end of the decade, according to Boston Consulting Group.

[...] "We do need way more energy in the world than we thought we needed before," Sam Altman, chief executive officer of OpenAI, "We still don’t appreciate the energy needs of this technology."

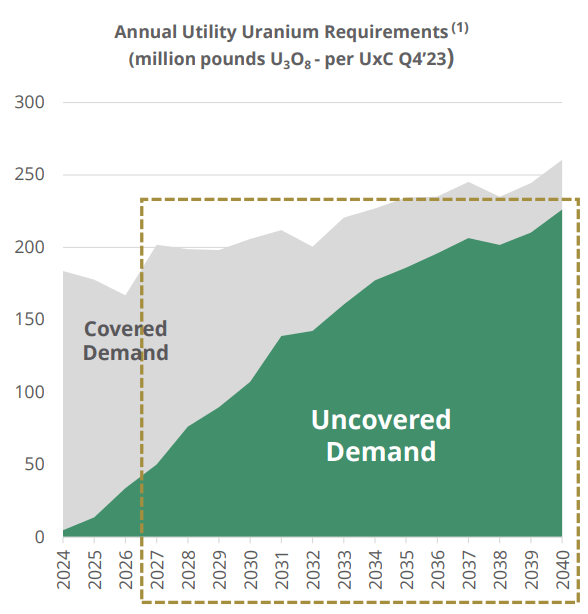

For years, uranium players have spoken about the massive shortfall in supply expected to meet uranium demand.

DNN stock presentation March 2024

That's not new news. However, the massive driving force for an uptick in energy demand driven by AI is something that very few investors are truly paying attention to. Even though there are some small groups actively discussing this element, this view is far from mainstream. At least not yet.

UEC presentation

In a few words, everything is explained. Unhedged pure-play uranium company. It's not that UEC is the only unhedged player, but it is a company, that is seriously committed to growing at scale.

Unlike many other uranium players in the sector, where the management team has very little skin in the game, CEO Amir Adnani has more than $35 million worth of capital tied up in UEC. And he is determined to 10x his investment.

UEC proxy statement

So, is UEC the best unhedged player? It's difficult to know for certain. But the fact of the matter is that Kazatomprom, the world's biggest uranium producer, which mines 20% of the world's uranium supply, has repeatedly warned that they are struggling to meet their production targets.

Similarly, let's turn our attention to discussing Cameco (CCJ).

CCJ 2023 annual report

What you see above is that when uranium prices climb higher than $80 per lb, CCJ doesn't reap the benefits as its production is hedged. This consideration is in place and will repeat itself in 2024 and beyond. Even as uranium prices stay higher than $100 per lb, CCJ is not going to benefit from this element.

Given this context, allow me to explain how I think about UEC's valuation.

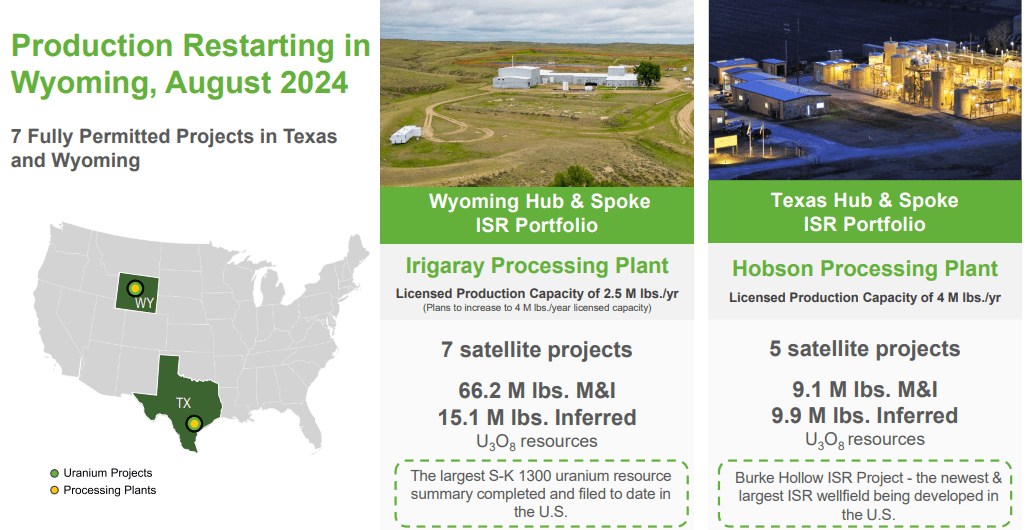

UEC operates In-Situ Recovery mining. This means that UEC is capable of extracting minerals from ore bodies without the need for conventional mining methods like open-pit or underground mining, making the process a lot cheaper.

UEC presentation

UEC is a company that has been dormant for many years, as uranium prices were too low to make it economically viable to produce uranium. But as you can see above, starting in August of this year, production will start.

So, when UEC reports that it made no revenues in Q2 2024, this insight is a distraction from where UEC is headed. It's been a long time coming, but this time next year, UEC will be up and running and busy starting to operate at scale.

I don't expect the process to start smoothly. But the fact that as of January 2024, UEC held more than $80 million of cash and no debt on its balance sheet, will allow UEC to start to roll out production.

UEC presentation

UEC has the capacity to produce about $8 million lbs of uranium per year. Assuming that it costs about $60 per lb to get the uranium out of the ground, and the price of uranium stays at north of $90 per lbs, this implies that there's roughly $30 per lb of gross profit.

Hence, this means that there's about $240 million of gross profits coming down the pipe. Of course, this is an extremely rough estimate and there are other costs too. But I believe that it's fairly easy to imagine a scenario where UEC could be making $150 million of operating profits in the next two years.

In wrapping up my analysis, I'm buying this dip in UEC.

The anticipation of restarting production in Wyoming, combined with UEC's debt-free balance sheet, paints a promising picture for future growth. As I've emphasized before, UEC's unique position as an unhedged pure-play uranium company aligns well with the increasing energy demand fueled by artificial intelligence.

CEO Amir Adnani's substantial personal investment, exceeding $35 million, reflects a strong commitment from the leadership. With the cost-effective In-Situ Recovery mining method and the upcoming production kick-off in August, UEC is poised for success. Despite the expected initial challenges, the company's solid financial standing and the potential for significant operating profits make it a compelling prospect moving forward.