Kativ

Kativ

Now is arguably the best time so far in this bear market to buy REITs (VNQ).

I am saying that because we can now see the light at the end of the tunnel.

Yes, REIT share prices are today a bit higher than they were back in October last year, but you need to remember that back then, the world was convinced that we would remain in a "higher for longer" interest rate environment.

Jamie Dimon was predicting that we would face 7% interest rates!

If that was the case, then the lower share prices would have warranted. We never bought into this narrative, but it still created significant uncertainty, which justified lower valuations.

But since then, the narrative has flipped completely.

We are not talking anymore about a "higher for longer" environment. We are now just debating when the first rate cut will take place. Will it be in May? Or June? Or in the Fall?

We don't know.

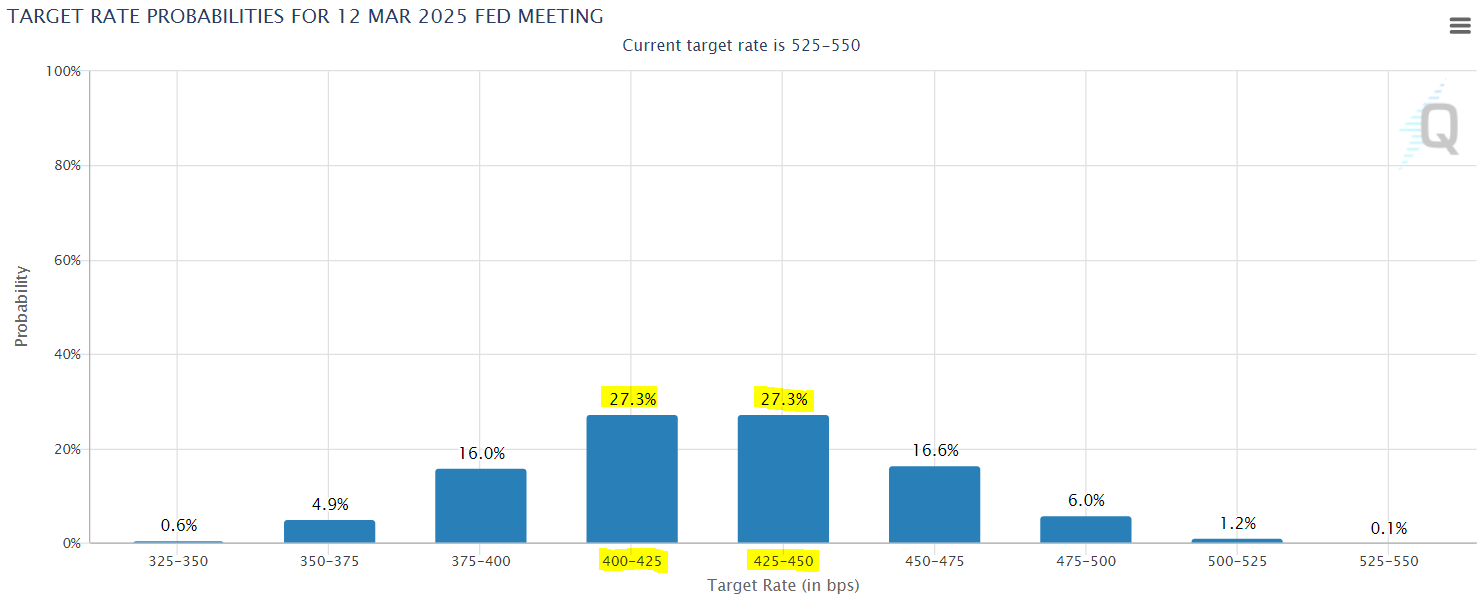

But we now have much greater certainty on the future outlook and it is much more favorable for REITs. We appear to have avoided the worst-case scenario and now have a strong catalyst already in the near term. The FedWatch tool is predicting a 99.9% chance of easing over the next year and pricing >100 lower interest rates within a year from now:

FedWatch

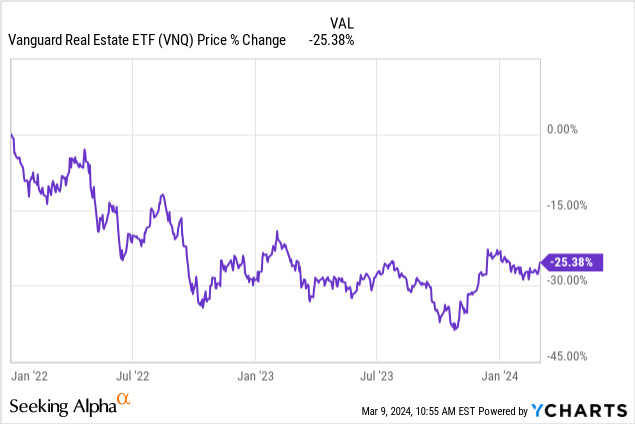

Despite that, REITs are still down over 25% on average as if we were still facing a "higher for longer" environment. Remember that most REITs have grown their cash flow by 5-10% and/or created value by deleveraging so valuations are even lower than they may seem:

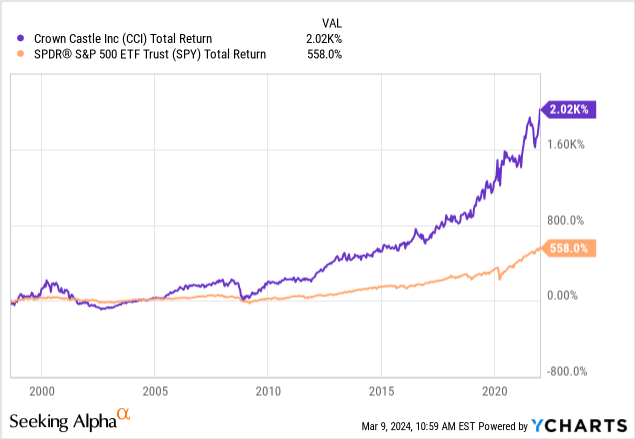

CCI is a cell tower REIT that has historically traded at ~25x FFO and a low 2-3% dividend yield during most times.

Crown Castle

It has generally been priced at such a high valuation because it is a mega-cap investment grade-rated REIT with a blue-chip reputation, rapid growth prospects, and an exceptional track record:

But all of this changed in recent years.

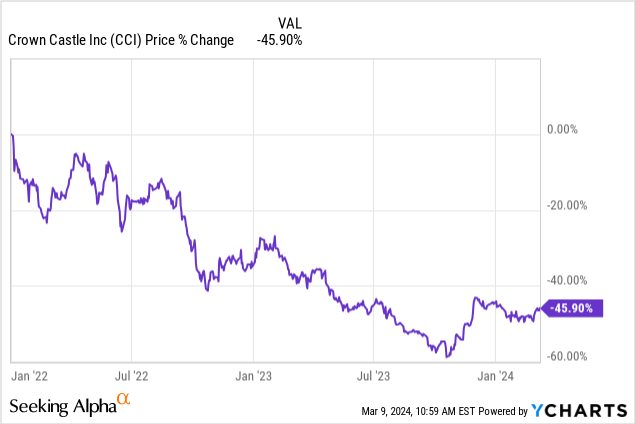

The surge in interest rates coupled with a temporary tenant issue caused its share price to crash and as a result, it is today priced at just 14x FFO and a near 6% dividend yield, which is exceptional for a REIT of this quality:

We think that this is a great buying opportunity because the reasons why the REIT is so heavily discounted are only temporary.

Firstly, as we noted in the introduction, interest rates are now expected to return to lower levels already in the near term and this should make CCI and other high-yielding REITs a lot more attractive. Suddenly investors will realize that the 5% yield that they expected to earn from money-market funds was just a mirage and as the forward yield dips to 3-4%, I expect a lot of that capital to come back to the REIT sector.

Secondly, the tenant issue is also temporary. T-Mobile's (TMUS) acquisition of Sprint meant that CCI lost a tenant and it hurt its growth due to lease cancellations.

But the impact of these lease cancellations is temporary, and the management has previously said that they expect to return to their historic 7-8% growth rate by 2026.

I believe that this will serve as a strong catalyst for the stock.

Today, CCI is heavily discounted because most investors only care about the next quarter, but as growth accelerates and interest rates return to lower levels, I expect CCI to reprice at a much higher valuation and lower yield.

If CCI repriced at a 4% dividend yield, it would unlock 40% upside from today's share price and it would still be historically cheap. While you wait, you earn a near 6% dividend yield.

In case CCI fails to reprice where it should be, it will likely end up pursuing strategic alternatives, including selling some divisions of its business to unlock value. That's what Elliott, a major activist investor, is pushing the management to do. I like that they are part of the story because they will hold the management accountable and put additional pressure on them to unlock value for shareholders.

Blackstone (BX) recently bought out Tricon Residential (TCN) in a multi-billion dollar transaction and later noted that they expect to be a lot more active in 2024, hinting at more buyouts.

As a reminder, Blackstone bought out about $30 billion worth of REITs in recent years, often paying large premiums to take them private.

It is targeting REITs so heavily because they are often priced at a large discount relative to the fair value of the real estate they own. As such, buying REITs essentially allows them to buy real estate at a discount, and with interest rates expected to return to lower levels in the near term, they seem to have a sense of urgency since the window of opportunity could be closing.

Their favorite property sectors are residential and industrial.

Today, most industrial REITs are priced fairly close to their net asset values, but residential REITs remain heavily discounted.

UDR, as an example, is today priced at an estimated 35% discount to its net asset value. Its implied cap rate is in the high 6s, but you would be happy to get its assets in the low 5s in the private market.

UDR

Apartment REITs are priced so cheaply because of two main reasons, both of which are temporary.

For one, the surge in interest rates.

For two, they are facing oversupply at the moment and it is causing their rents to stagnate. But this is temporary. The surge in construction costs and interest rates has significantly slowed down new construction activity and this should lead to an acceleration in rent growth in the coming years. New starts are today at the lowest level since the great financial crisis.

Blackstone knows this and this is why they are buying residential REITs. The best time to invest is when prices are low due to near-term uncertainty and that's precisely today.

UDR

I think that UDR could be next in line given how cheap it has gotten. In a future buyout, it could unlock ~30% upside for shareholders, and while you wait, you also earn a near 5% dividend yield and the company keeps creating value by acquiring new communities.