SOPA Images/LightRocket via Getty Images

SOPA Images/LightRocket via Getty Images![]()

I previously rated buy rating for Udemy (NASDAQ:UDMY) as I expected UDMY to continue growing EBITDA strongly, which support UDMY to trade at the same valuation as peers. My previous call recommendation played out well as the stock surged to $16 in mid-Dec 2023, surpassing my target price. I believe the share price decline post the result has presented another buying opportunity, as such, my recommendation for UDMY is a buy rating. I believe the issue with UDMY is a fixable one, and importantly, the long-term demand remains intact. While FY24 is going to be a soft year, I am expecting growth to recover to mid-teens percentage range in FY25 with an improved adj. EBITDA margin.

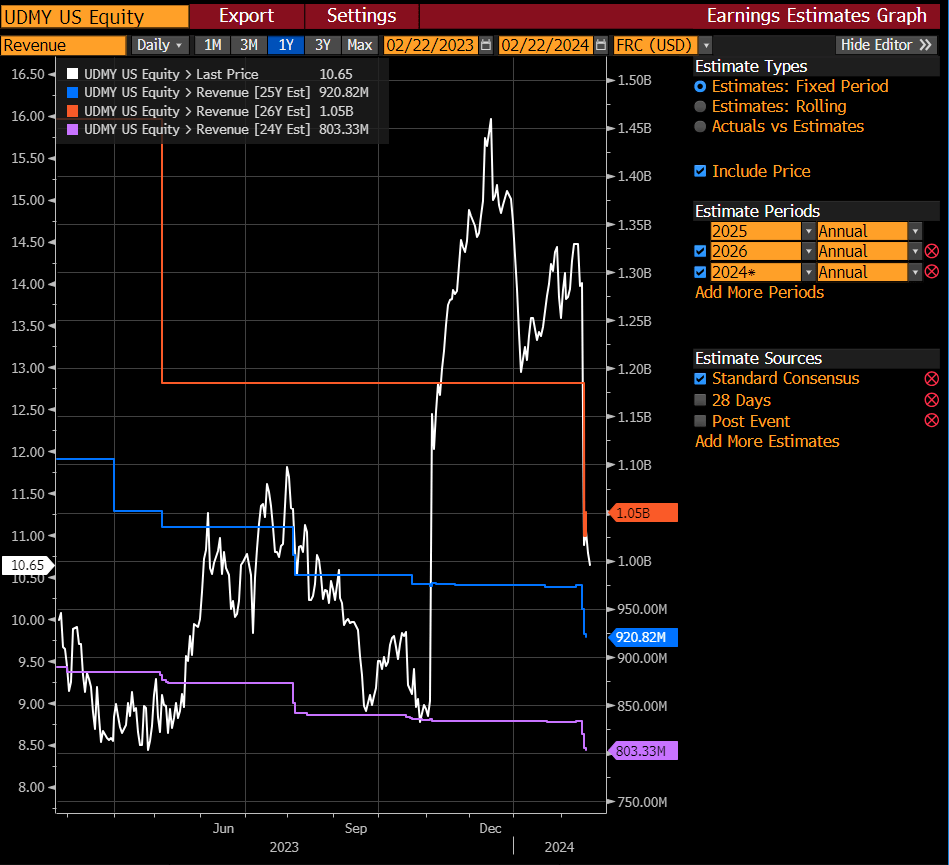

UDMY reported 4Q23 revenue of $189.5 million, modestly above street expectation for $186 million, and an adj. EBITDA margin of 2.1%, which also beat street expectation by 150bps. On a FY23 basis, UDMY reported total revenue of $730 million and positive adj. EBITDA of $7.8 million (1.1% FY23 margin).

Contrary to what I believed was a decent quarter, the stock price fell sharply back to the ~$10 range, wiping out all the gains that it had seen since my last update. In my opinion, the decline was mainly due to the FY24 guidance. Management guided FY24 revenue to range between $795 million and $810 million, or $802.5 million at the midpoint. This reflects 10% FY24 y/y growth, which is a big step down from the 15% growth seen in FY23 (note that 4Q23 growth was also ~15%). Within the guide, the assumption is that consumer revenue will decline by 4%, while UB (Udemy Business) ARR growth will see a dip in 1H24 before accelerating in 2H24. The FY24 guide was also very weak, as management guided for an adj. EBITDA margin of 1.75% at the midpoint (almost 100bps lower than the street's expectation). This weak guide led to a series of consensus downgrades, which led to the share price decline.

Bloomberg

To be fair, I think the consensus and market concerns about the near-term performance (FY24) are legitimate, as UDMY flagged execution issues that are worrisome. According to management, UDMY had poor performance in EMEA and execution problems with some of its reseller partners in Korea and Vietnam in 4Q23. The situation has not been completely resolved, as management has stated that they are still working on resolving the performance and execution issues. I believe this was a key reason for the weak guidance provided. In addition, UDMY is still facing a challenging macro environment; as previously mentioned by management, sales cycles are still quite long, and although they did not grow even longer in Q4, they are still significantly higher than in the past.

Putting all the negative points together, I can see why the stock got punished. However, I don't think we should discount positive performance and the long-term secular trend simply based on 1 quarter of weak execution and the ongoing macro situation (which is outside of UDMY's control). I point investors to the positive aspects of UDMY that suggest demand is not as bad as it seems. Firstly, UDMY did grow revenue by ~15% in 4Q23, despite all the negatives that are mentioned above. Secondly, annual recurring revenue [ARR] grew by 25% in 4Q23, which has decelerated, but on an absolute basis, it is still a very strong performance. Thirdly, the net dollar retention rate [NDR] for UB customers has stabilized at 106% after six quarters of consecutive declines, suggesting that the macro impact has not worsened. Importantly, UB grew revenue by 27% and saw 80% y/y growth in the number of deals that are worth >$10 million in ARR, which is a big indication of UDMY success in acquiring larger customers. The same stabilization can be seen in the consumer segment as well, which grew 0.3% in 4Q23, extending the streak of growth to a 2nd consecutive quarter after 9 consecutive quarters of negative growth. Lastly, and arguably one of the most important takeaways, is that UDMY sales and marketing as a percentage of revenue were sustained below the 40% level while maintaining mid-teen growth in 4Q23. This is noteworthy because it shows that UDMY's traction in acquiring larger customers is having a positive impact on unit economics.

Furthermore, I also don't see any structural impairments to the long-term growth driver for UDMY-more learners adopting digital solutions because they are more assessable and typically cheaper. What triggered the weak guidance was poor execution, something that can be fixed, and I think it would be fixed given UDMY's ability to execute so far. As for the macro situation, it impacts everyone, not just UDMY. There is practically nothing UDMY can do to revive the macroeconomy anyway. What UDMY can do is continue its strategy, which appears to be working, as it continues to see traction in acquiring larger customers. I would also argue that the weak macro situation will force further market share consolidation in the industry as the smaller players lack the financial capacity (i.e., balance sheet) to tide through this weak phase. UDMY will be there to pick up market share as it has net cash of $430 million and is becoming more profitable.

Author's valuation model

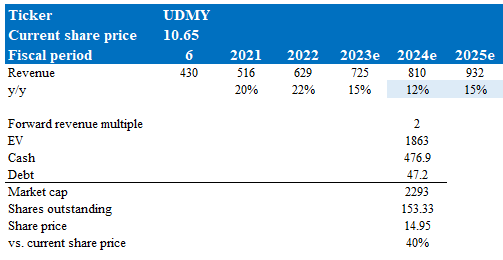

Because of the share price decline, I believe the upside has become attractive again, even if we take into account management FY24 guidance. My growth assumptions are that FY24 is going to be a soft year because of the execution issues and ongoing macro situation, and all of these will go away in FY25, where UDMY will revert back to its mid-teens revenue growth range. My valuation assumption is that UDMY should trade back to 2x forward revenue. The devaluation to 1.5x simply reflects the expected weak FY24-something that I see as temporary, as discussed above. So long as UDMY shows growth recovery with adj. EBITDA margin expansion, I expect valuation to recover as well, trading back to where it was a few months ago.

The new risk that appeared in my thesis is that UDMY misexecution in the mentioned regions could be a way bigger problem than expected. Asia and the Middle East represent a large part of UDMY's revenue base (51% as of FY23). If UDMY is not able to resolve the issue, it could drag down the entire business performance, delaying the recovery to mid-teen growth profile, which will cause further downward revisions in the street's expectation.

Despite UDMY recent challenges leading to a share price decline, I maintain a buy rating. While the FY24 guidance reflected concerns about execution issues and a challenging macro environment, I believe these are fixable, and the long-term demand for UDMY product remains strong. The recent dip in valuation presents an attractive upside, especially if Udemy can recover in FY25 with mid-teens revenue growth and improved EBITDA margin. The key risk lies in the potential impact of misexecution in certain regions, particularly Asia and the Middle East, which could hinder overall business performance and delay growth recovery.