DNY59

DNY59

We previously covered Uber Technologies, Inc. (NYSE:UBER) in December 2023, discussing its highly promising FQ4'23 forward guidance and the consensus forward estimates, implying its ability to defy the uncertain macroeconomic outlook.

Then again, these developments had triggered the stock's overly premium valuations and aggressive rallies, resulting in a minimal margin of safety. As a result of the potential near-term volatility, we had cautiously downgraded our rating to Hold then.

In this article, we shall discuss why UBER has been upgraded to a Buy, with the company's market dominance and profitable growth trend unlikely to ever come cheap. Combined with the promising FQ1'24 guidance, it is apparent that we may have missed the boat since our previous coverage.

As a result of the attractive long-term risk/ reward ratio, the stock is a Buy after a moderate retracement to its previous support levels for an improved upside potential.

For now, UBER has reported an FQ4'23 earnings call on February 07, 2024, with Gross Bookings of $37.57B (+6.4% QoQ/ +22% YoY), adj EBITDA of $1.28B (+17.4% QoQ/ +92.9% YoY), and adj EPS of $0.66 (+560% QoQ/ +127.5% YoY).

Otherwise, FY2023 has also brought forth impressive numbers at $137.86B (+19.4% YoY), $4.05B (+136.8% YoY), and $0.87 (+174.3% YoY), respectively.

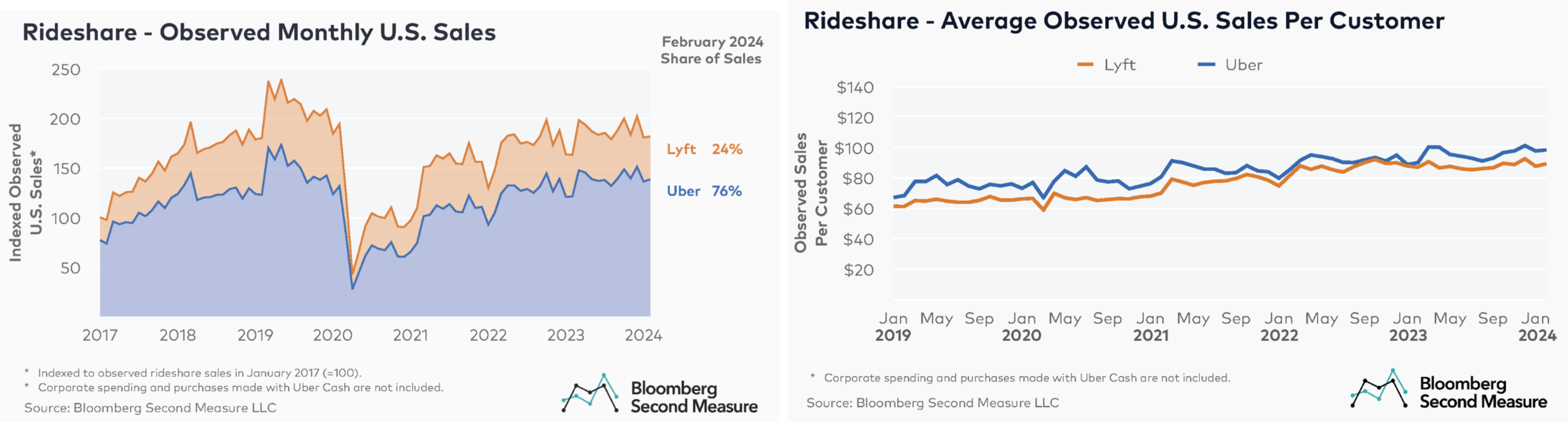

UBER's Leading Market Share

Bloomberg Second Measure

From these numbers, it is understandable why UBER continues to command the market leading share in the US rideshare at 76% by February 2024 (+2 points from August 2023 levels), compared to Lyft, Inc. (LYFT) at 24% (-2 points from August 2023 levels), based on the latest data from Bloomberg Second Measure.

UBER also commands a higher average monthly customer sales at $98 in the February 2024 month (+9% YoY), compared to LYFT at $89 (+3% YoY), suggesting the former's leading mindshare.

These have led to UBER's growing Mobility Gross Bookings of $19.3B (+7.8% QoQ/ +29% YoY) and Delivery Gross Bookings of $17B (+10.5% QoQ/ +18% YoY), with growing quarterly trips of 2.6B (+0.16B QoQ/ +0.5B YoY) and Monthly Active Platform Consumers of 150M (+8M QoQ/ +19M YoY).

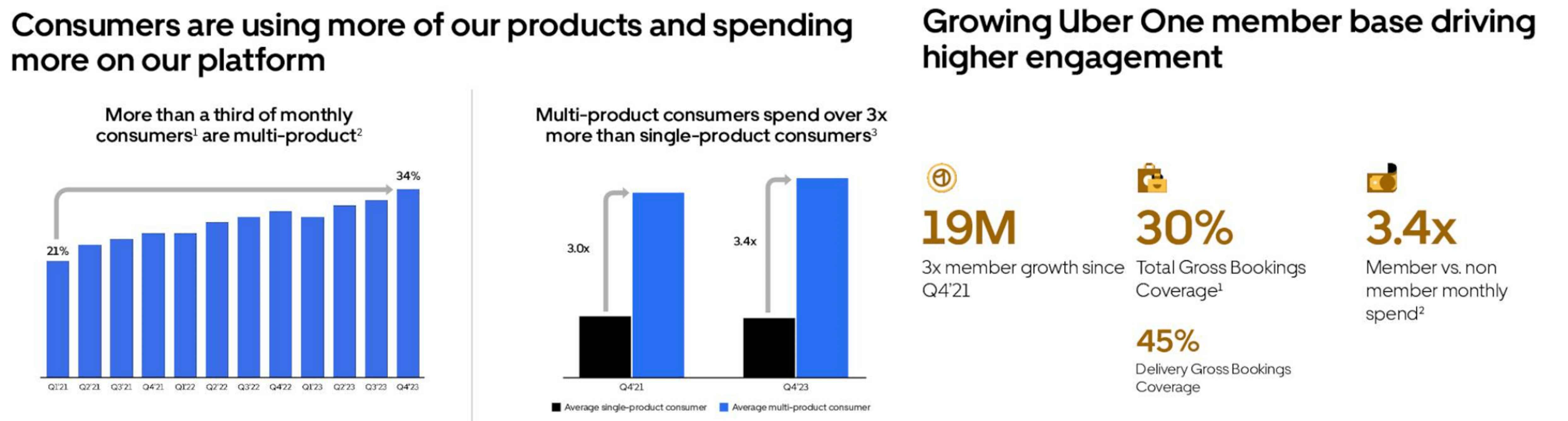

UBER's Expanding Cross-Selling & Growing Engagement

Seeking Alpha

The platform's growing stickiness and ability to attract new users are impressive indeed, with the expanding cross-selling naturally leading to its improved bottom lines, as discussed above, and healthier balance sheet with a robust cash of $5.4B on the balance sheet (+4.4% QoQ/ +25.2% YoY).

The same is observed in its moderating debt-to-EBITDA ratio of 2.33x by the latest quarter, down drastically from 5.41x in FQ4'22.

Furthermore, UBER's surprising announcement of $7B in share repurchases exemplifies the management's conviction about its ability to consistently deliver profitable growth ahead.

This naturally well balances the elevated share based compensation of $1.93B (+7.8% YoY) and consistent dilution to 2.12B in share count (+0.02B QoQ/ +0.06B YoY/ +0.88B since FY2019 levels of 1.24B) in FY2023.

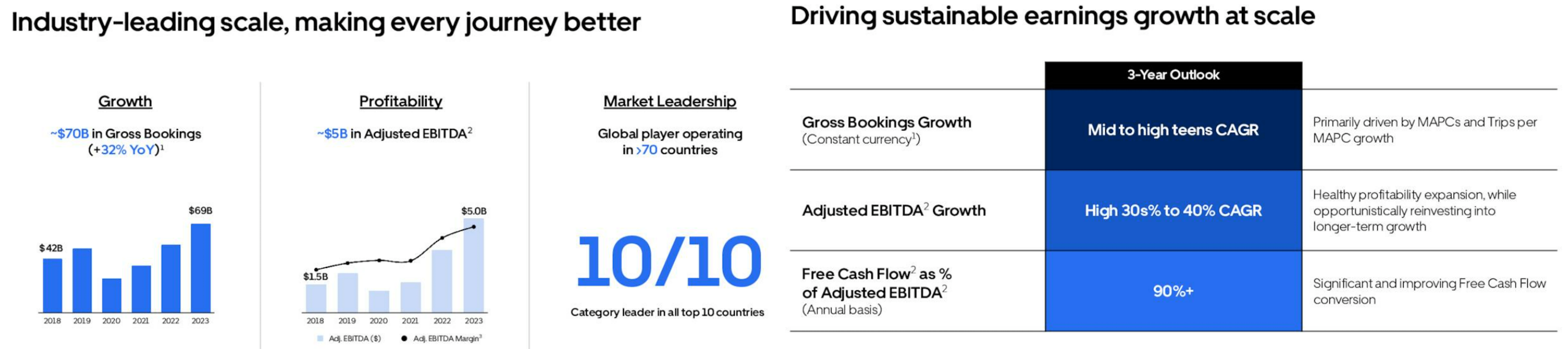

UBER's Profitable Growth Trend & 3Y Outlook

Seeking Alpha

Lastly, UBER has offered an optimistic FQ1'24 guidance, with gross booking of $37.75B (+0.3% QoQ/ +20.2% YoY) and adj EBITDA of $1.3B (+1.5 QoQ/ +70.8% YoY) at the midpoint, as the management also aims to deliver double digit top/ bottom line expansion over the next three years.

This further highlights its accelerating profitability as the adj EBITDA margin relative to gross booking rise to approximately 3.4% (inline QoQ/ +1 point YoY) in FQ1'24, with us believing that this guidance is not overly ambitious as the management continues to execute its high growth and high margin advertising segment brilliantly.

For example, UBER's advertising segment already reports $900M in annualized revenues by FQ4'23 (+80% YoY), building upon the $500M reported in FQ4'22 (+122.2% YoY).

With the management likely to exceed the $1B in advertising revenue run rate by FQ1'24, as opposed to the original target of sometime in 2024, we believe that the management may be able to consistently deliver double digit growth ahead, while building upon the historical top-line growth of +27% between FY2018 and FY2023.

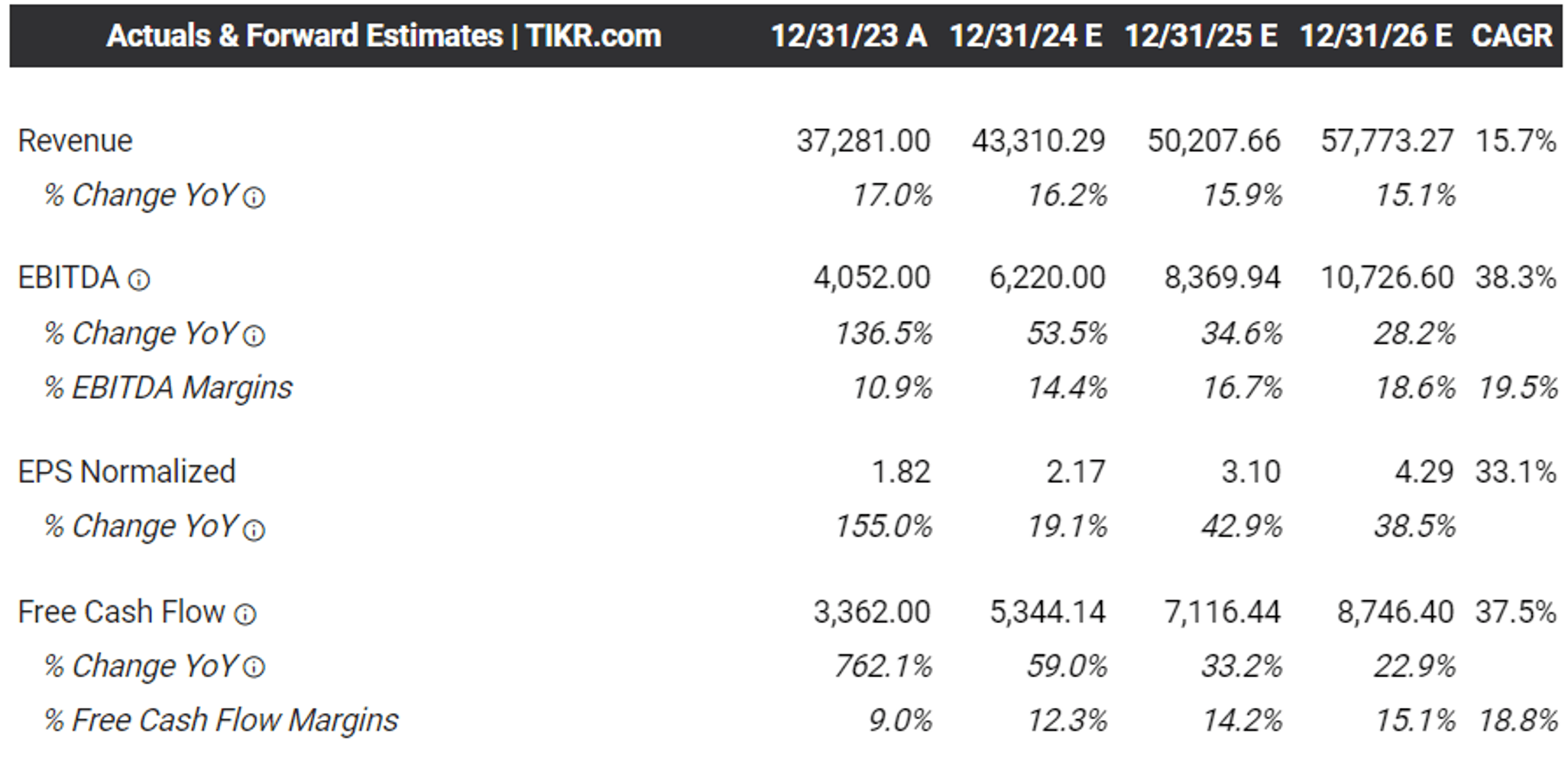

The Consensus Forward Estimates

Tikr Terminal

The same has been reflected by the consensus forward estimates, with UBER expected to generate an accelerated bottom line growth at a CAGR of +33.1% through FY2026, compared to the previous estimates of +16.1%/ +19.2%.

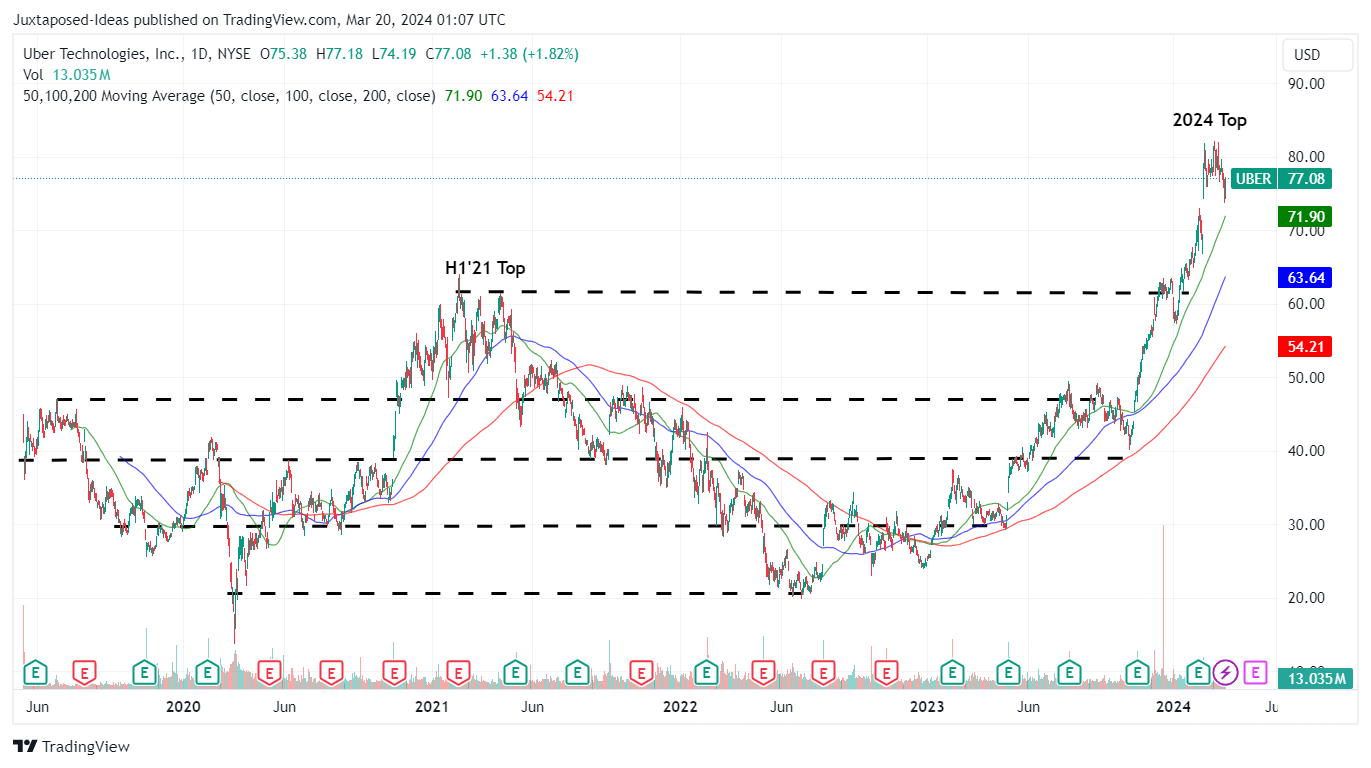

UBER 5Y Stock Price

Trading View

As a result, we can understand why UBER has rapidly broken out of its 50/ 100/ 200 day moving averages while charting new heights beyond the H1'21 tops.

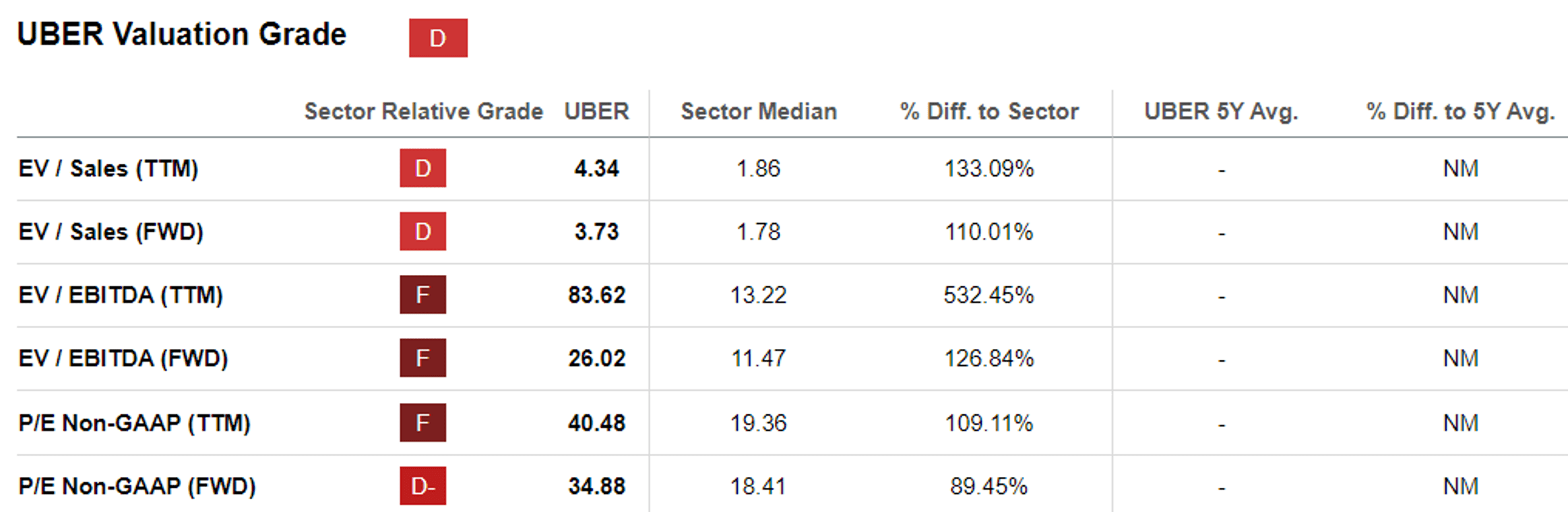

UBER Valuations

Seeking Alpha

It is apparent by now, that market leaders may never come cheap after all, with UBER trading at FWD EV/ EBITDA of 26.02x and FWD P/E of 34.88x, moderated from our previous article of 32.94x/ 46.96x in December 2023, though recovering immensely from the October 2023 bottom of 18.42x/ 27.61x.

Most importantly, with UBER trading near to its 1Y mean of 22.69x/ 33.57x, and direct peers, such as LYFT at 22.49x/ 32.50x and Grab Holdings Limited (GRAB) at 38.53x/ NA, we believe that the former is fairly valued here, especially due to the profitable growth trend as the stock grows into its premium valuations.

On the one hand, based on the FY2023 adj EPS of $0.87 (+174.3% YoY) and the FWD P/E of 34.88x, it is apparent that the stock is trading way above our estimated fair value of $30.30.

On the other hand, based on the FY2026 adj EPS estimates of $4.29 (expanding at a CAGR of over +30% as guided by the management), there appears to be an excellent near doubling potential to our long-term price target of $149.60.

Naturally, this is assuming that UBER is able to sustain its premium growth valuations, with the market likely to closely monitor its quarterly performance against the 3Y growth target.

It goes without saying that with elevated P/E valuations come great expectations, with any earning misses and/ or underwhelming forward guidance likely to bring forth painful corrections.

Only time may tell.

Here comes the most difficult question indeed.

Is UBER a buy after the impressive YTD rally of +25.19%, well outperforming the SPY at +8.50% and QQQ at +6.83%?

Yes, though with multiple caveats.

On the one hand, UBER continues to face drivers' pay headwinds in multiple US states, potentially impacting its profit margins and operations if a resolution is not achieved.

This builds upon the ongoing discussion in many EU states, where it remains to be seen if its ride-share drivers may be eventually classified as gig workers or employees, with the latter likely to trigger further adjustments in its local operations to mirror its current arrangements in Spain and Germany.

Since UBER boasts global presence, readers may want to pay attention to these ongoing developments, since there may be more regulatory changes in the near future.

On the other hand, with UBER seemingly pulling back from the recent heights at the time of writing, it appears that the previous resistance levels of $60s may very well be its new support levels.

Naturally this is assuming that the management is able to deliver its FQ1'24 growth targets and sustain the positive Free Cash Flow generation, to successfully execute its multi-year $7B share repurchase program.

With only $2.65B of its debts due through 2026, we believe that there are minimal liquidity headwinds ahead, with UBER likely to continue outperforming expectations.

As a result of the relatively attractive long-term risk/ reward ratio, interested investors may want to Buy upon a moderate retracement to its previous trading ranges of between $60s and $70s for an improved margin of safety.

With UBER continuing to generate alpha for its shareholders, we believe that the stock is one that is highly suitable for growth-oriented investors at every dips.