Stock photo and footage

Stock photo and footage

AppLovin's (NASDAQ:APP) Software Platform continues to demonstrate strength, and the App segment appears to be stabilizing. With competitors struggling, AppLovin's recent outperformance should persist. There is also potential for growth in the OEM & Carrier and CTV segments, as AppLovin leverages its capabilities in new areas.

I previously suggested that the market was underestimating AppLovin's prospects, with overly conservative analyst projections and unfounded concerns around executive turnover and insider sales. AppLovin's momentum has persisted since then, with the stock up close to 70%. My view of the company hasn't changed significantly in that time, although it has become clear that competitors are trailing by a wide margin and are unlikely to close the gap in the near term.

The combination of strong growth, high margins and a reasonable valuation should see AppLovin's stock continue to perform well going forward. A lot of the easy gains have already been made though, meaning share price appreciation is likely to moderate going forward.

AppLovin continues to record strong Software Platform growth despite market conditions remaining challenging. There is growing evidence that digital advertising markets have turned a corner though. AppLovin has suggested that user engagement began to increase and that technological advancements are driving higher CPMs. User numbers are up more than 7% YoY and users are also engaging with ads more than ever, with the average number of ad impressions per user increasing by 7%. As a result, average revenue per user increased by an average of 7% YoY in November.

AppLovin's business is also being supported by the ongoing shift towards in-app bidding. 60% of revenue on MAX is now transacted via in-app bidding, up from 40% last year.

Google previously announced its intent to shift to predominantly real time bidding in mobile mediated auctions by January. This is a shift that has been underway for a while and has potentially been a tailwind for AppLovin's business. MAX has a large share of mediation in gaming, meaning that AppLovin can extend Google's demand to most game publishers in an efficient manner. This is not exclusive access, as Google also has third-party integrations with Chartboost Mediation, Digital Turbine (APPS), and Unity (U).

Real time bidding compares prices from all buyers simultaneously, which should create a more efficient auction and maximize the value of inventory. AppLovin also believes that larger publisher profits will mean increased investment in user acquisition, further benefiting its business. AppLovin only charges its 5% take rate for real time bidding, meaning the shift should be a tailwind. Real time bidding also clears an auction faster than the waterfall method, resulting in less infrastructure usage.

Despite these positives, digital advertising markets could be in for another period of turbulence, with the Digital Markets Act now coming into effect, the deprecation of the Google Android ID and the release of iOS 17.4. AppLovin doesn’t seem fazed by this though, which could be due to the fact that it runs a more contextual behavioral model than many other adtech companies.

AppLovin's recent performance stands in stark contrast to companies like Digital Turbine and Unity. Digital Turbine's App Growth Platform business has been fairly flat in recent quarters and is down significantly from its peak in late 2021. Digital Turbine's business was built through a number of acquisitions and the company's commentary suggests that this is causing problems. Digital Turbine is currently incurring large expenses as it consolidates its ad exchange, migrates its cloud hosting platform and invests in machine learning.

Unity has pointed to increased competition as one of the issues facing its Grow business. The company is now increasing its investments in machine learning to try and improve its monetization capabilities and close the gap with AppLovin.

Whatever AppLovin is doing at the moment is clearly working in its core business, and there remains an enormous opportunity to extend this into adjacent verticals like Carrier & OEM and CTV. Digital Turbine estimates that its Carrier & OEM opportunity is worth approximately 25 billion USD. CTV ad spend in the US is expected to be around 30 billion USD in 2024, with double-digit growth projected going forward.

AppLovin's CPMs have historically been low relative to social media networks, search engines and video apps. The company believes its technology is now allowing it to more effectively monetize users though, providing a long growth runway from a low starting point. AppLovin expects its technology to continue improving as well, which should lead to further growth in the core business.

The important question for AppLovin at this point is whether it has a sustainable competitive advantage, or if competitors can catch up, and whether this advantage can be extended into new areas. AppLovin, Unity and Digital Turbine have similar scale in terms of access to devices. For example, MAX sits on top of over 1 billion daily active users, providing it with a treasure trove of data. AppLovin's Ignite has an on-device footprint of around 750 million. At the end of 2020, Unity had approximately 2.7 billion monthly active end users who consumed content created or operated with its solutions.

MoPub could be an important contributor to AppLovin's recent success. AppLovin acquired MoPub in January 2022 for roughly 1 billion USD cash. MoPub is a mobile SSP and ad exchange and was previously the biggest independent monetization solution for developers. The acquisition was all about scale, with AppLovin trying to aggregate as much supply as possible to build a data advantage. The aggregation of supply provides pricing insights that are more valuable in a privacy-focused era where it is more difficult to obtain user level data. SSPs have visibility of all submitted bids, information that is unavailable to demand partners and advertisers.

AppLovin also believes that its core AI technology is amongst the most advanced in the market, and the company plans on leveraging this as it expands into adjacent markets like CTV and Carrier & OEM. Non-gaming is growing faster, although it is smaller, with AppLovin specifically highlighting contribution from its Array business (on-device) in the fourth quarter.

AppLovin’s expansion into CTV is still nascent, but the opportunity is large. AppLovin claims that it is the only one enabling performance advertising for CTV. Given the current size of AppLovin’s software business, it will likely be several years before CTV is a material contributor though.

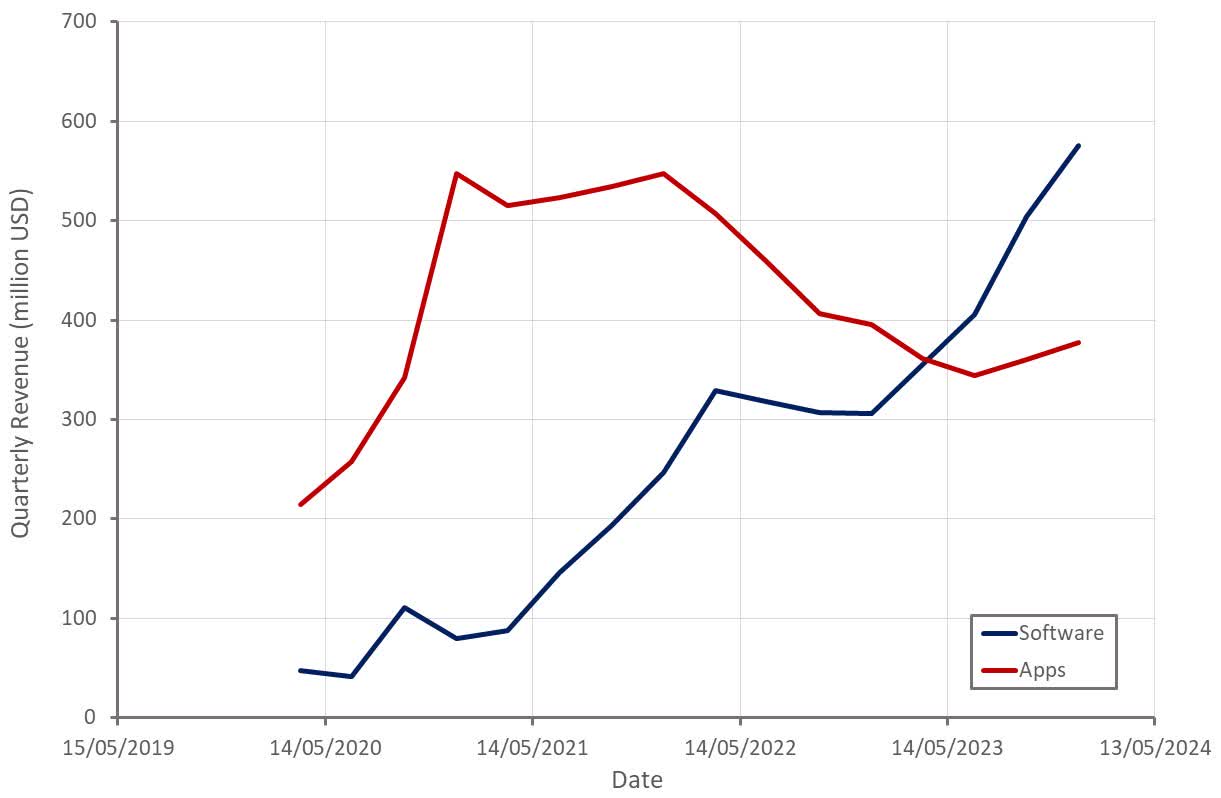

AppLovin’s revenue was up 36% YoY in the fourth quarter, to 953 million USD. The App business has returned to sequential growth after optimization efforts had reduced revenues over the past few years. AppLovin’s Software Platform continues to drive growth though, reaching 576 million USD revenue in the fourth quarter, up almost 90% YoY. Within the Software Platform, AppDiscovery is the growth engine at the moment. AppLovin has also suggested that mobile advertising market growth, a shift to real-time bidding, the Array business and AXON are contributing to growth.

AppLovin expects 955-975 million USD revenue in the first quarter of 2024, representing 35% YoY growth at the midpoint.

Figure 1: AppLovin Revenue (source: Created by author using data from AppLovin)

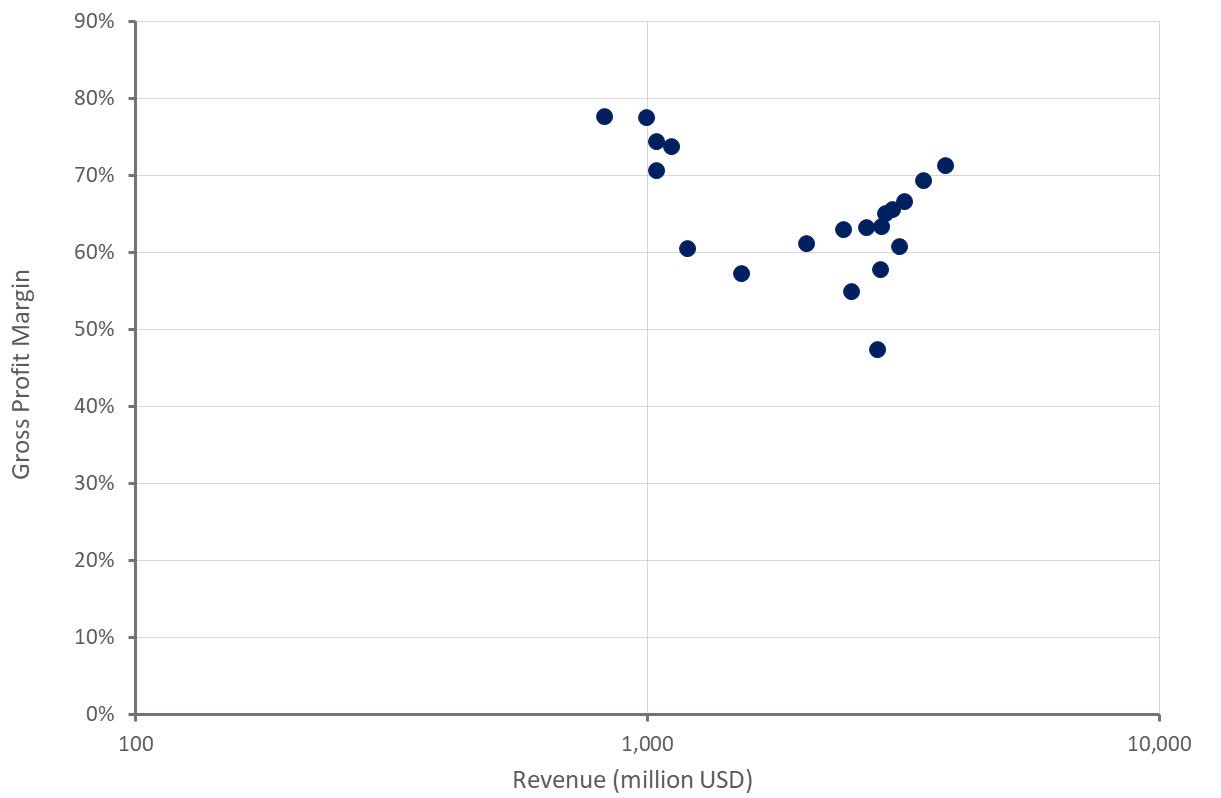

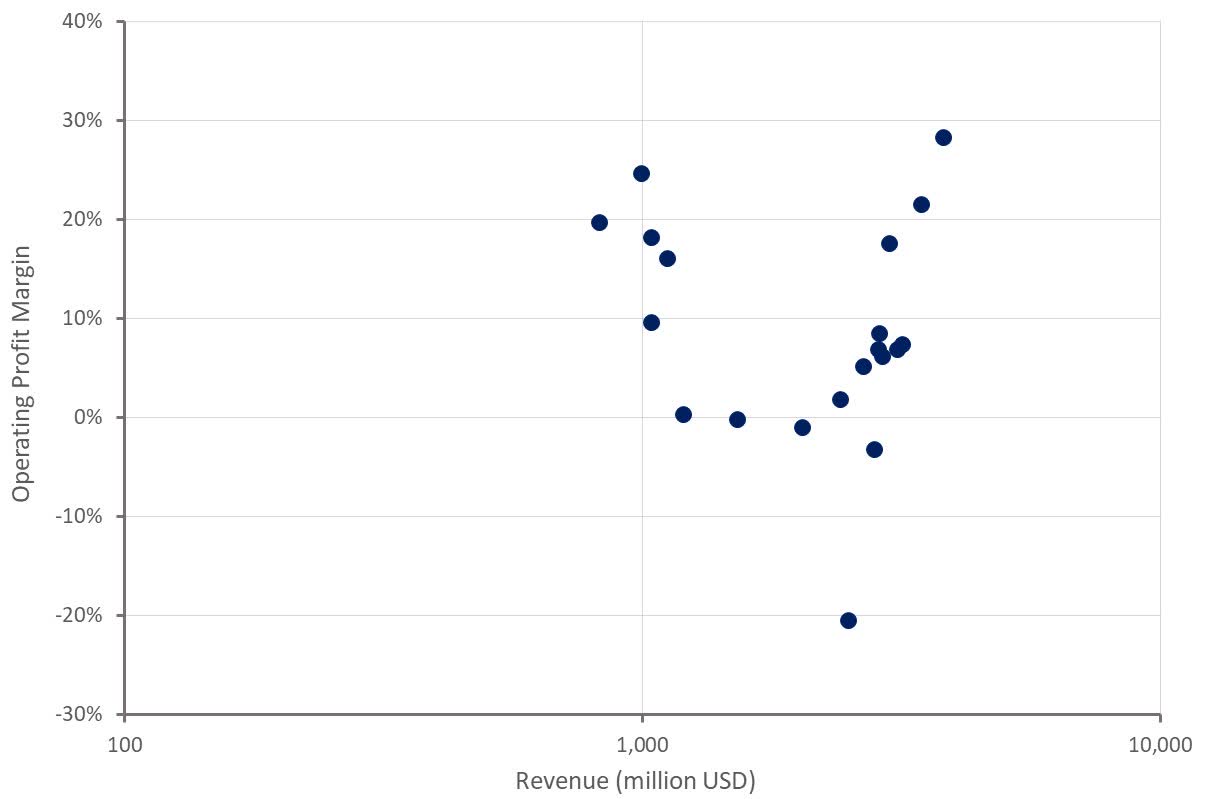

The App business currently has a 15% adjusted EBITDA margin, while the Software Platform had a 73% adjusted EBITDA margin in the fourth quarter. AppLovin has also stated that around of 80% of incremental revenue is currently flowing through to adjusted EBITDA. This means that AppLovin's margins will continue to rapidly expand as the Software business grows.

Adjusted EBITDA is expected to be 475-495 million USD in the first quarter, representing an adjusted EBITDA margin of between 50% and 51%.

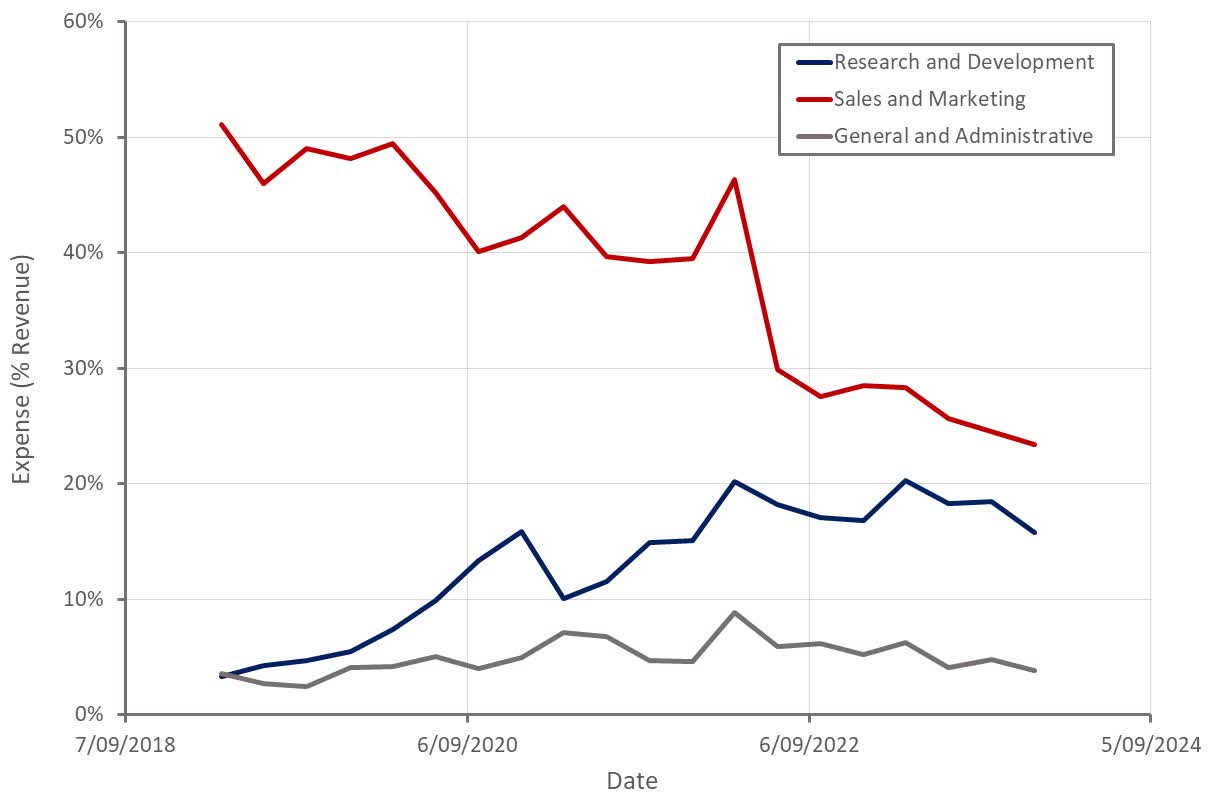

Figure 2: AppLovin Gross Profit Margin (source: Created by author using data from AppLovin) Figure 3: AppLovin Operating Profit Margin (source: Created by author using data from AppLovin) Figure 4: AppLovin Operating Expenses (source: Created by author using data from AppLovin)

The benefit of share repurchases are often wildly overstated, but it is an important consideration in AppLovin's case because of the company's ability to generate free cash flow and reasonable valuation. For example, the company reduced its share count by close to 10% in 2023. With cash flows set to continue increasing rapidly, this should provide the share price with a considerable tailwind.

AppLovin also has a relatively large debt position, with interest significantly cutting into the company's profits. For example, interest expense was approximately 106 million USD in the fourth quarter, compared to an operating profit of 270 million USD. AppLovin has extended the maturity of its term loan to 2030, which will reduce its interest rate going forward. Regardless, the company has the cash flow to easily support the current debt load, making the choice to repurchase debt or equity a question of capital structure optimization.

Despite its strong performance in 2023, AppLovin's share price still looks too low given the company's growth potential and ability to generate free cash flow. The strength of AppLovin's Software Platform was masked by the App business in 2023. With the App business returning to growth and profitability, I would expect AppLovin's revenue multiple to continue expanding in 2024, particularly if AppLovin's Array and Wurl businesses can demonstrate traction.

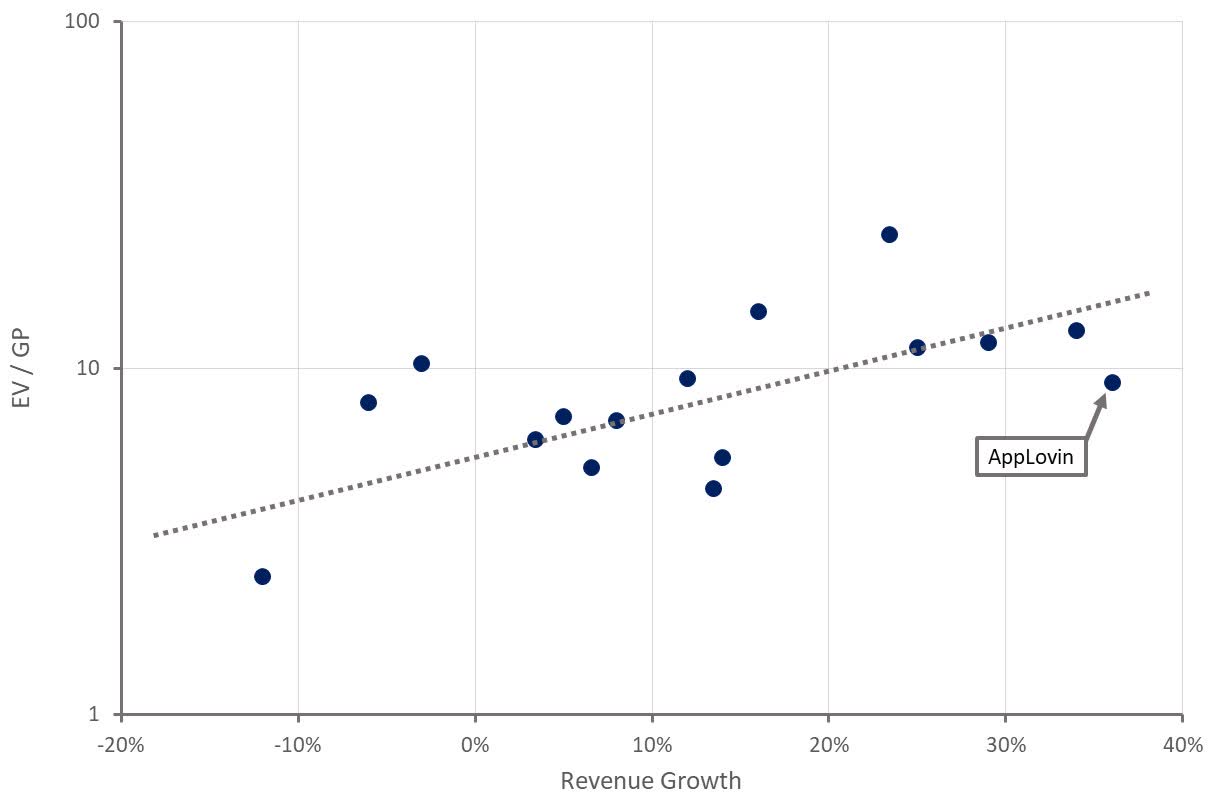

Figure 5: AppLovin Relative Valuation (source: Created by author using data from Seeking Alpha)