abadonian

abadonian

Tortoise Energy Infrastructure Corporation (NYSE:TYG) is a closed-end fund, or CEF, that focuses specifically on investing in midstream companies and other energy infrastructure companies, such as utilities and certain renewable energy companies. This is overall a very good place to be right now, as rising energy prices across the spectrum are driving the demand for greater production of energy. This means that additional infrastructure will be needed to get the energy supplies from the oil fields or other producing locations to homes, businesses, and other end-users.

Thus, there are certainly some reasons to believe that the companies in which this fund invests could be on the verge of a massive growth spurt. The fact that many energy infrastructure companies also have stable and sustainable cash flows coupled with high dividend yields is something that is likely to appeal to investors in this fund. The Tortoise Energy Infrastructure Corporation, for its part, has a 9.83% yield at the current price so it is certainly no slouch when it comes to yield.

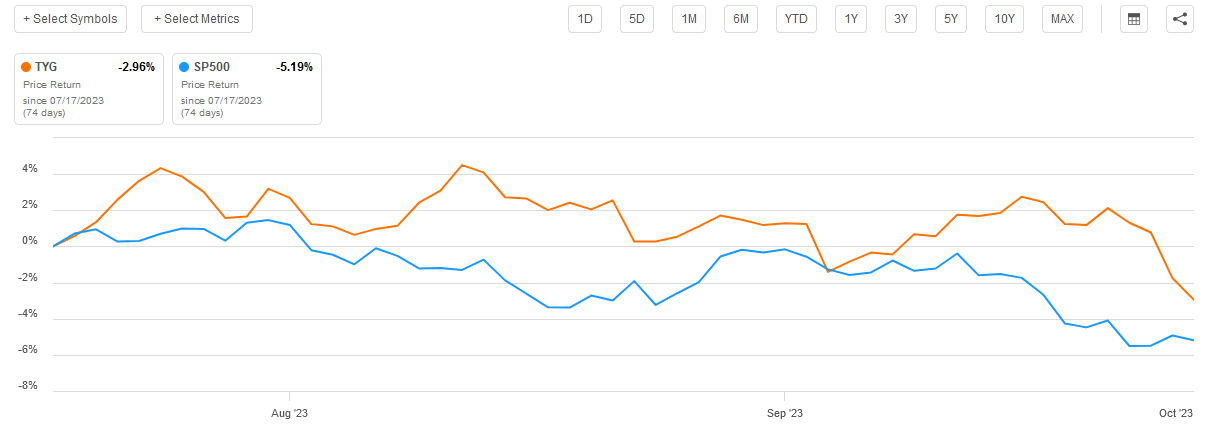

We last discussed this fund back in the middle of July. The fund has not delivered the best price performance since that time, but it did manage to beat the S&P 500 Index (SP500):

Seeking Alpha

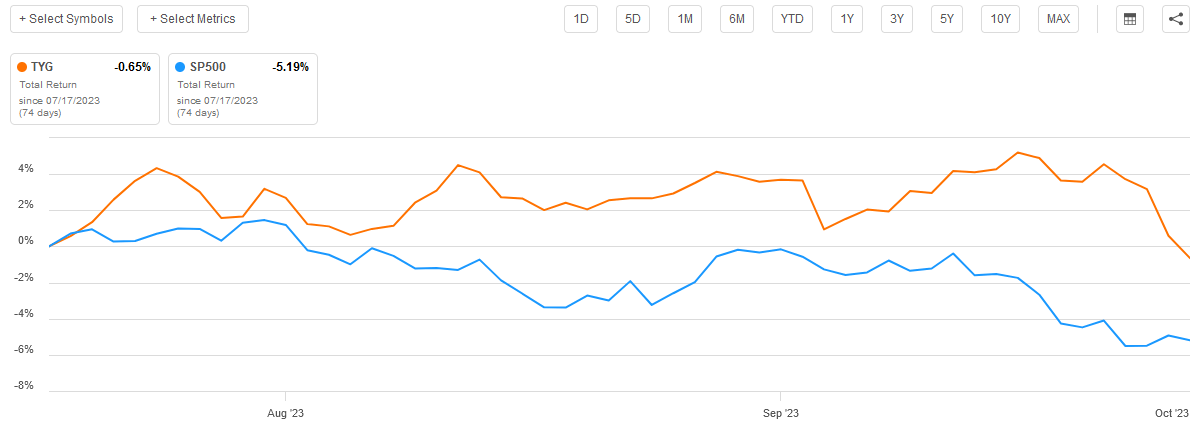

However, this fund delivers the majority of its returns through the distributions that it pays out, not price appreciation. Thus, we cannot simply watch the stock price to see how we are doing with a fund like this. Once the distribution is added in, we can see that investors in this fund have been relatively flat since the time that my previous article on this fund was published. That is not a particularly impressive performance, but it was still much better than the S&P 500 Index managed to deliver over the same time period:

Seeking Alpha

As a few months have passed since mid-July, it is a good idea to revisit our thesis for investing in this fund. After all, several things can change in two months, and we want to see how the fund has been adapting to these changes and if our original thesis still makes sense. Therefore, let us investigate and determine if investing in this fund still makes sense today.

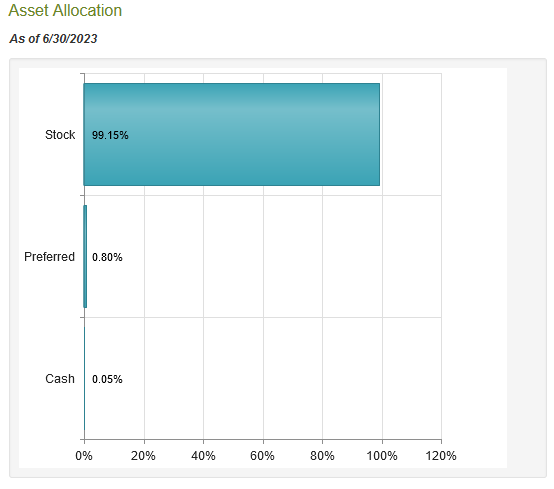

According to the fund's webpage, Tortoise Energy Infrastructure Corporation has the primary objective of providing its investors with a high level of total return. This makes sense since, as we saw in the previous article, this fund is primarily invested in common equities. This is still the case today, as 99.15% of the fund's assets are invested in equity alongside small allocations to both preferred securities and cash:

CEF Connect

As I pointed out in the previous article:

The reason why the fund's investment objective makes sense in this respect is that common equity is by its nature a total return vehicle. After all, investors typically purchase common equity in order to generate income through dividends and distributions paid by the issuing company. They also want to benefit from capital appreciation as the issuing company grows and prospers with the passage of time. As the fund is almost completely invested in these securities, it makes sense that this is the objective that it would be targeting.

The balance between capital appreciation and direct payments to investors as a source of total returns is different between different stocks and industries. For example, growth companies will frequently not pay out any dividends to their investors. Berkshire Hathaway (BRK.B), Alphabet (GOOG) (GOOGL), and Tesla (TSLA), for example, do not pay dividends yet have still been able to deliver acceptable returns to investors over time. In fact, this trait of offering no or minimal dividends is pervasive throughout the American economy as evidenced by the S&P 500 Index (SPY) only yielding 1.52% as of the time of writing. That is actually a negative real yield given the current inflation rate, which stands as evidence that most companies and investors consider dividends to be an afterthought.

It is a bit different with energy infrastructure companies, especially pipeline operators and other midstream firms. We can see this simply by looking at some of the indices that track the sectors containing these companies:

Index | Current Yield |

Alerian MLP Index (AMLP) | 7.87% |

U.S. Utilities Index (IDU) | 2.99% |

S&P Global Utilities Index (JXI) | 3.69% |

All of these are clearly much higher than the S&P 500 Index, although curiously both of the utilities indices do still have a negative real yield. However, we can still see that these companies have a much stronger focus on returning cash to the shareholders in the form of a regular dividend than companies in many other sectors. This comes from the fact that most energy infrastructure companies have low growth rates and as such are highly unlikely to deliver the growth that the market expects from companies in other sectors. As such, their stock prices do not appreciate very rapidly so they typically pay out a substantial portion of their cash flows to the investors in order to provide an acceptable investment return.

Tortoise Energy Infrastructure Corporation invests primarily in the companies that would be included in these indices, so we can expect that the fund will receive a significant amount of dividend and distribution income from its holdings. Indeed, the fund's own website suggests that this is the case:

TortoiseEcofin

Thus, the basic strategy is for the fund to collect large amounts of income from these companies and pay that out to the investors along with the limited capital gains that it manages to earn along the way. This is the sort of thing that should generally appeal to most investors, particularly given the overall stability that most energy infrastructure companies have.

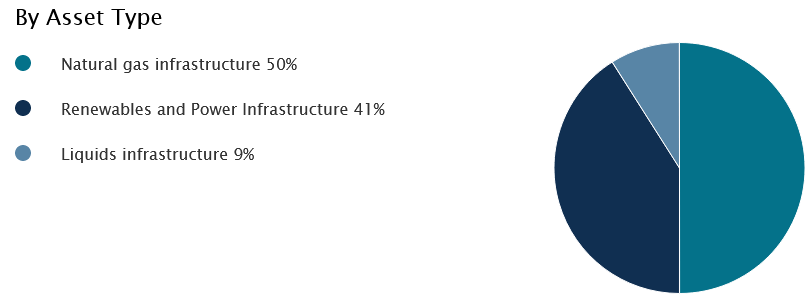

Frequently, energy infrastructure funds will be very heavily focused on midstream companies and pipeline operators. This one appears to have a somewhat more balanced approach, as about half of its assets are invested in natural gas-focused midstream companies alongside a very similar allocation to renewable energy and utility plays:

TortoiseEcofin

This is a pretty good balance for people who want to play the energy transition theme that politicians, activists, and the media have been screaming about over the past several years. As I have pointed out in the past, natural gas is going to be critical for any energy transition due to the unreliability of wind and solar power. After all, wind power does not work if the air is not moving. Solar power does not work at night and is not particularly effective on cloudy days.

Thus, something else is needed to ensure that the electric grid continues to function in the way that we have all become accustomed to over the years. As of right now, batteries are other energy storage technologies are woefully inadequate for that task, so utilities have generally opted to supplement renewable energy facilities with natural gas turbines. Natural gas burns much cleaner than other fossil fuels and it is reliable enough to ensure that the electric grid continues to function even when the renewable energy plants are not producing sufficient electricity.

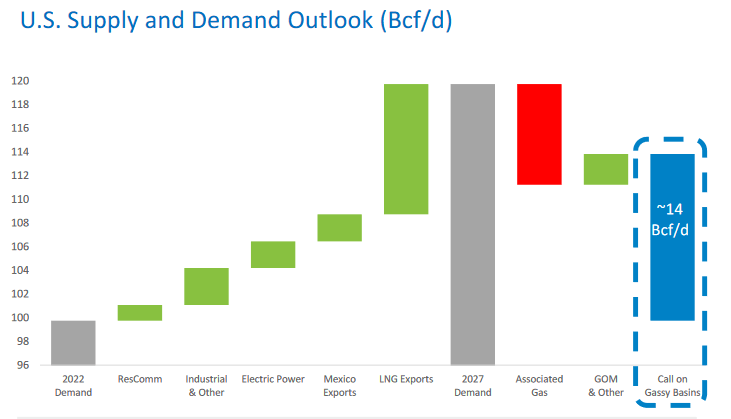

This use of natural gas as a supplement to renewable energy is driving demand growth in the United States and around the world. As we can see here, the American demand for natural gas is expected to increase by twenty billion cubic feet per day by 2027:

Range Resources

A sizable portion of this growth comes from the export sector, which is primarily exports to Mexico and Asia. The United States is also expected to be increasing its exports to Europe due to the reduction in the natural gas supply from Russia. In the case of both Asia and Europe, natural gas will need to be converted into liquefied natural gas, which as we can see is the largest single driver of demand growth domestically. These two regions primarily want natural gas for electric generation purposes, so that part of the thesis still holds true.

The natural gas pipeline operators in this fund will be the beneficiaries of this natural gas demand growth. After all, these are the companies that will transport the natural gas from the fields where it is produced (primarily the Marcellus, Permian Basin, and Haynesville Shale) to liquefaction plants and utility companies. As I pointed out in numerous previous articles, the cash flows of pipeline operators directly correlate with the volume of resources that are transported so this trend should result in growth for the companies that this fund invests in. As many pipeline operators raise their dividends or distributions as cash flow increases, we can anticipate that this will result in income growth for the fund itself.

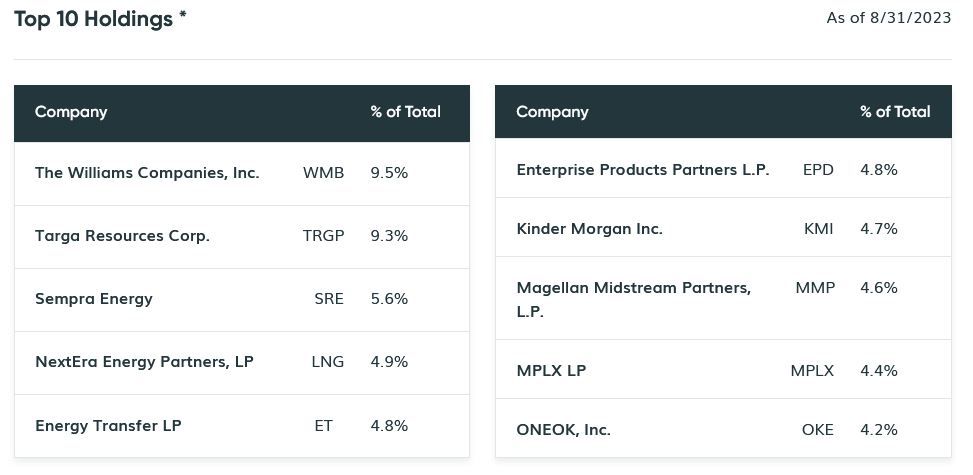

As regular readers are no doubt well aware, I have devoted a considerable amount of time and effort over the years to discussing energy infrastructure companies both here at Energy Profits in Dividends and on the main Seeking Alpha site. As such, the largest positions in the fund should be familiar to most readers. Here they are:

TortoiseEcofin

I have discussed every single company on this list several times over the past year or two, so they should all be reasonably familiar. For the most part, the fund seems to have selected a good cross-section of companies for its portfolio as most of these are among the best companies in the industry. I will admit though that it seems a bit strange that the fund is invested in both Magellan Midstream Partners (MMP) and ONEOK (OKE) during the run-up to the impending merger between those two companies. It will probably have to sell off some of its position in the combined company following the merger or that will easily be one of the biggest positions in the fund. This merger was consummated last week, so the fund has almost certainly had to address this situation by now. However, as of October 2, 2023, the most recent information that the fund sponsor has released about the portfolio is dated August 31, 2023, so we can only speculate about how the fund's portfolio looks today.

There were two significant changes since the last time that we discussed this fund's portfolio. These are that DTE Energy Company (DTE) and Clearway Energy (CWEN) were both removed from the largest positions list. In their place, we see Magellan Midstream Partners and ONEOK. This suggests that the fund may have been speculating on the merger, which actually did work out pretty well for Magellan Midstream Partners' investors due to the substantial premium that ONEOK offered.

In addition to these two major changes, the weighting of several of the fund's assets has changed, but there are a lot of reasons why this could have happened that do not necessarily mean that the fund was actively attempting to change its weightings. However, the fund does have a fairly high 73.84% annual turnover, so it is definitely engaging in some active trading activity. This is a higher annual turnover than many other equity closed-end funds possess, which could prove to be an issue with investors who are concerned about the fund's expenses. After all, the higher the fund's expenses, the more difficult it is for management to earn satisfactory returns.

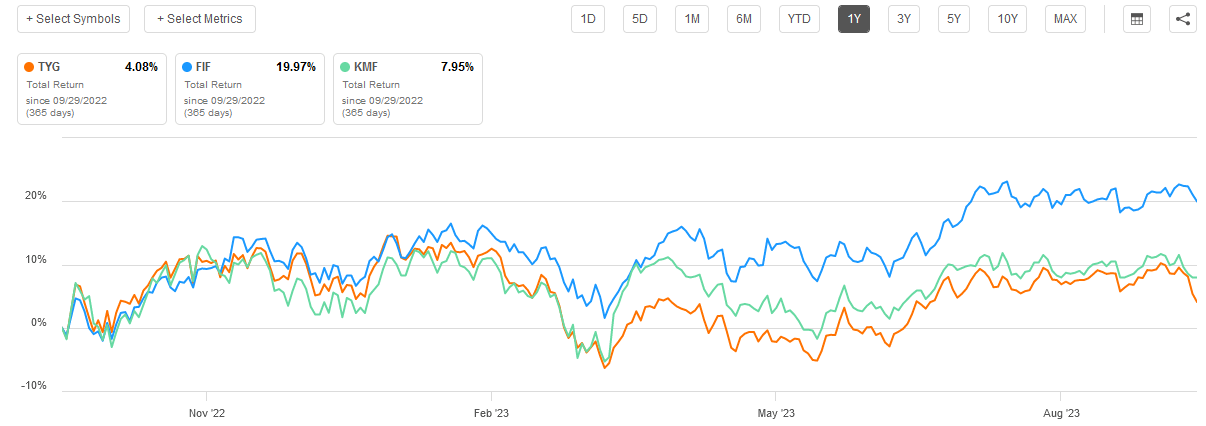

That could be a potential issue here. Tortoise Energy Infrastructure has underperformed some of its peers in the energy infrastructure space. As we can see here, this was the worst-performing fund out of a few others that focus on investing in energy infrastructure companies over the past year:

Seeking Alpha

The First Trust Energy Infrastructure Fund (FIF) completely dominated this one in terms of total return over the period. The Kayne Anderson NextGen Energy & Infrastructure Fund (KMF) likewise beat Tortoise's offering, although not by nearly as much. However, it is a very different story if we go out to the three-year period:

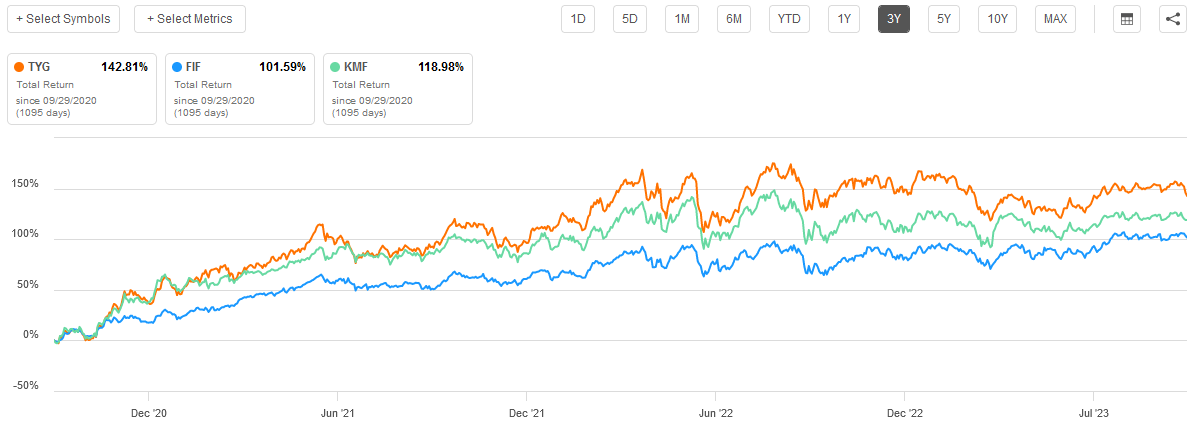

Seeking Alpha

Here, we see that Tortoise Energy Infrastructure Corporation has actually outperformed both of the other closed-end funds by quite a lot. This could have something to do with the fund's holdings. Tortoise Energy Infrastructure has a higher allocation to renewable energy than either of the other two funds, which are somewhat more heavily weighted to traditional midstream firms. Renewable energy companies have substantially underperformed traditional midstream over the past year, despite the help that they have been getting from the Federal Government's Inflation Reduction Act. This is partly due to the rising cost of materials and fossil fuel energy that are needed to construct renewable energy facilities. However, renewable energy companies dominated traditional energy back in 2020 and 2021 when low interest rates and a great deal of investor euphoria resulted in a tremendous amount of money chasing those companies.

However, another major contributing factor to the performance difference over the past three years is that Tortoise was much more aggressive about raising its distributions once the energy sector started to recover from the COVID-19 pandemic in late 2020. As such, investors in this fund would have realized a much larger distribution payment for much of 2021, boosting its total return overall.

The best option then might be for investors to hold Tortoise Energy Infrastructure alongside something like one of the First Trust energy infrastructure funds in order to get the best of both worlds. However, its underperformance over the past twelve months is still a point of concern. This is especially true since rising energy prices right now are benefiting traditional fossil fuel companies and hurting renewable energy ones.

As is the case with most closed-end funds, Tortoise Energy Infrastructure Corporation employs leverage as a means of boosting its total return and the effective yield of its portfolio. I explained how this works in my previous article on this fund:

In short, the fund is borrowing money and using that borrowed money to purchase common equities of midstream and renewable companies. As long as the purchased assets deliver a higher total return than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case. However, it is important to note that this strategy is not as effective today with interest rates at 6% as it was two years ago when rates were at 0%.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. Thus, we want to ensure that the fund is not using too much leverage since that would expose us to too much risk. I generally do not like to see a fund's leverage exceed a third as a percentage of assets for that reason.

As of the time of writing, Tortoise Energy Infrastructure Corporation has levered assets comprising 23.11% of its portfolio. This is quite a bit less than the 26.39% of the portfolio that the fund had the last time that we discussed it. This is probably a good thing, as it represents a reduction in risk for the fund's shareholders. However, most midstream partnerships and many corporations actually have yields higher than the borrowing rate and are delivering gains in the otherwise weak market. Thus, the reduction in leverage is not as big of a deal as it would be for many other funds. It is certainly not a bad thing though and overall this fund is striking a very reasonable balance between risk and reward. We should not have to worry about its leverage right now.

As mentioned earlier in this article, one of the biggest reasons why people buy energy infrastructure companies is because of the high yields that these companies typically possess. This is particularly true with midstream companies, which are one of the few things that have a higher yield than an ordinary money market fund right now, as well as being one of the only asset classes with positive real yields. These companies comprise a bit more than half of this fund, as we saw earlier in this article.

Thus, the fund is probably collecting a respectable yield from its portfolio, especially when the effects of leverage are added. Its basic business model is to collect all of the distributions and dividends that it receives from the assets in its portfolio and pay them out to shareholders, net of the fund's own expenses. We might expect that this would result in the fund having an attractive yield itself.

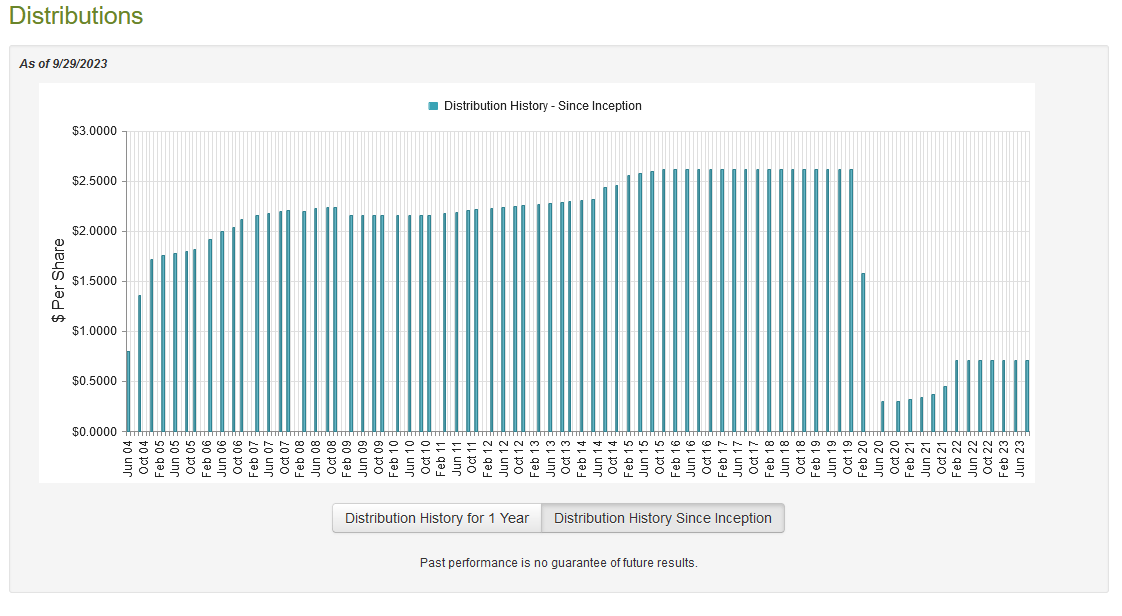

This is certainly the case, as Tortoise Energy Infrastructure Corporation currently pays a quarterly distribution of $0.71 per share ($2.84 per share annually), which gives the fund a 9.83% yield at the current price. This is a very respectable and attractive yield that easily competes with any other energy infrastructure fund in the market. Unfortunately, the fund has not been very consistent with respect to its distribution over the years:

CEF Connect

As we can see here, the fund had a pretty good track record until the coronavirus lockdowns during the spring of 2020. While it did cut just before the lockdowns occurred, there was generally a growing wave of fear even back in January of that year and demand for gasoline and other crude oil products was starting to waver even then. Fortunately, the fund has made some efforts to restore its distribution and raise it as the energy sector has recovered, but it still remains far below the level that the fund had prior to the pandemic.

As I have pointed out before though, the fund's past is not necessarily the most important thing for buyers today. After all, anyone who purchases shares of the fund today will receive the current distribution at the current yield and will not be negatively impacted by the events that occurred in the fund's past. As such, the most important thing for our purposes right now is to determine how well the fund can sustain its current distribution.

Fortunately, we do have a very recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on May 31, 2023. This is a much more recent report than the one that we had available to us the last time that we discussed this fund. That is certainly a positive thing as the energy sector in general was weaker during the first half of this year than it was during 2022. This report should give us a good idea of how well the fund handled that particular market environment, which could be insightful with respect to its ability to sustain its distribution. After all, if the fund managed to earn enough to sustain its distribution during that period, then it probably will not have too much trouble sustaining it going forward.

During the six-month period, Tortoise Energy Infrastructure Corporation received $13,235,185 in dividends and distributions along with $261,997 in interest from the investments in its portfolio. However, a sizable portion of the dividends and distributions came from master limited partnerships, so are not considered to be income for tax purposes. This gives the fund a total investment income of $8,511,566 during the period. The fund paid its expenses out of this amount, which left it with $2,275,338 available for shareholders. As might be expected, that was not nearly enough to cover the distributions that were paid out. During the six-month period, the fund paid out a total of $16,090,742 in distributions to its shareholders. At first glance, this is almost certainly going to be concerning as the fund clearly did not have sufficient net investment income to cover the distributions.

However, the fund has other methods through which it can obtain the money that it needs to cover the distribution. For example, it might be able to generate capital gains that could be paid out to the investors. In addition, the fund did receive $4,989,010 in distributions from master limited partnerships that were not included in net investment income due to rules around taxation of partnership income. This still represents money coming into the fund, though. Fortunately, the fund did enjoy some success in this area during the period. The fund reported net realized gains of $22,361,867 but this was offset by $74,841,900 net unrealized losses. Overall, the fund's net assets declined by $66,295,437 after accounting for all inflows and outflows during the period. This is certainly concerning, however, the fund's net realized gains plus its net investment income were sufficient to cover the distribution.

The big concern here is that the fund's net assets declined over the trailing eighteen-month period. This is much worse than most other closed-end funds that focus on energy infrastructure as the overwhelming majority of them have managed to grow their net assets over the period. The reason for this is probably this fund's heavy weighting towards renewable energy, which as already mentioned, underperformed midstream fairly significantly since the start of 2022. The losses from this part of its portfolio could have offset some of the gains from its midstream investments.

As of September 29, 2023 (the most recent date for which data is currently available), Tortoise Energy Infrastructure Corporation has a net asset value of $33.65 per share but the shares only trade for $28.53 each. This gives the fund's shares a 15.22% discount on net asset value at the current price. This is a massive discount that is relatively in line with the 15.39% discount that the shares have averaged over the past month. Overall, the current price seems like a good entry price to pick up the fund.

In conclusion, Tortoise Energy Infrastructure Corporation does have some things to offer, but I do not rate it as highly as its peers right now. In particular, there are reasons to expect that traditional energy will outperform renewable energy for a while and this fund is not as weighted to traditional energy as some of its peers. This has driven the fund's underperformance over the past year. However, there is a chance that things could change, so a case could be made for buying this one and another fund that is more midstream-heavy. The fund's impressive 9.83% current yield appears sustainable and the shares are currently trading at a massive discount so there is definitely a case to be made for it, though.