dra_schwartz/iStock via Getty Images

dra_schwartz/iStock via Getty Images

Cytek Biosciences (NASDAQ:CTKB) is a leading cellular analysis instrument maker, with a primary focus on industry-leading Aurora flow cytometry platform. The flow cytometry field is mature with the lab instrument manufacturers holding significant market share, but Cytek has built a leading position thanks to offering the highest number of fluorescent detectors. This leads to deeper insights using a full spectrum of fluorescence. This niche leadership has allowed Cytek to develop a strong financial profile despite the early-stage nature of the business. In fact, the company flirts with profitability most quarters and a long operating runway is what separates them from other innovative new peers. I believe as Cytek matures by increasing their installed base and recurring reagent/consumable revenues, investors will be rewarded with above-market returns.

Despite a downturn in the broader healthcare and biotech market, Cytek has kept revenue growth above 15% for all but one quarter since IPO almost three years ago. The reason for this is that Cytek is not selling equipment to translational companies, but instead to well-funded academic and research organizations as the Cytek platforms are on the leading edge of modern research. However, with time the opportunity in the commercial space will grow as research is completed, adding visibility to Cytek’s outlook. As the interest-rate environment equalizes over the coming months, I expect healthcare investment to increase again across all sectors. This undoubtedly will sustain revenue growth for Cytek, and a more stable environment can lead to continued margin improvement. Therefore, I believe 2023 and 2024 are the bear years for Cytek performance, and investors should take advantage of this relative bottom.

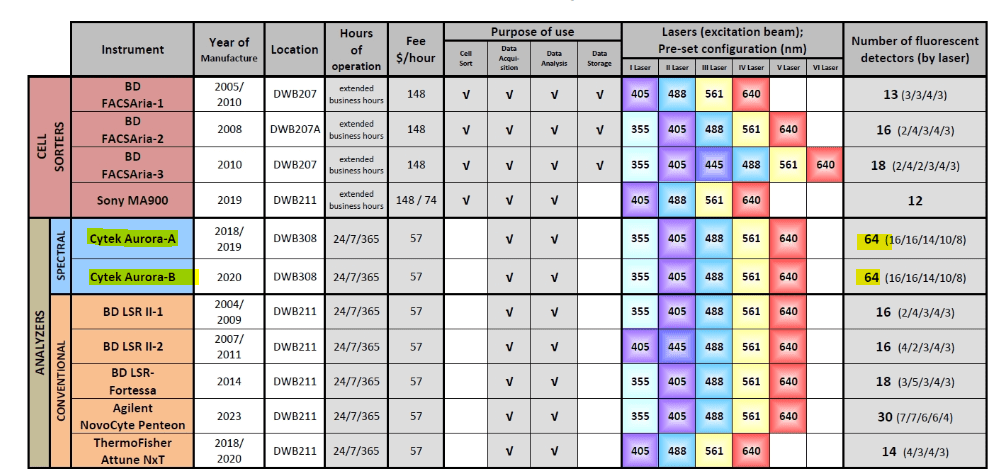

A comparison of flow cytometry tools in the Rockefeller Uni FC Resource Center lab. (Rockefeller University)

Cytek remains one of the best performing new entrants to the lab equipment market for a few select reasons. Firstly, there is a clear technological advantage as margins and growth are above peers. I include a comparison to the closest peers later in the article. Of note, the expensive phase of building out manufacturing and sales teams is nearly complete, and this lowers expenses moving forward. Also, the ecosystem is broadening and Cytek’s entrenched position will lead to translational opportunities in the clinical and biopharma space. An example is the success of PerkinElmer, now Revvity’s (RVTY), assay specialties such as DELFIA, Alpha38, and BRET2 which all have done well to increase profitability.

Currently, Cytek is facing margin headwinds, but during bull periods both EBITDA and net income generation has been significant. However, the field will remain cyclical for some time as investments in new technologies come and go. Thankfully, the realm of spatial biology is new and untapped, allowing a range of competitors to be successful. It will be important for Cytek to rein in the losses moving forward, as technological success can really only be measured through financial performance in this IP sensitive industry. What I find most important though, is the fact that margins have declined less than other innovator peers, but significant investments in R&D and new product lines continue. As an example, new tools for cell sorting and automated reagent cocktail preparation open up competitive advantages and market expansion opportunities.

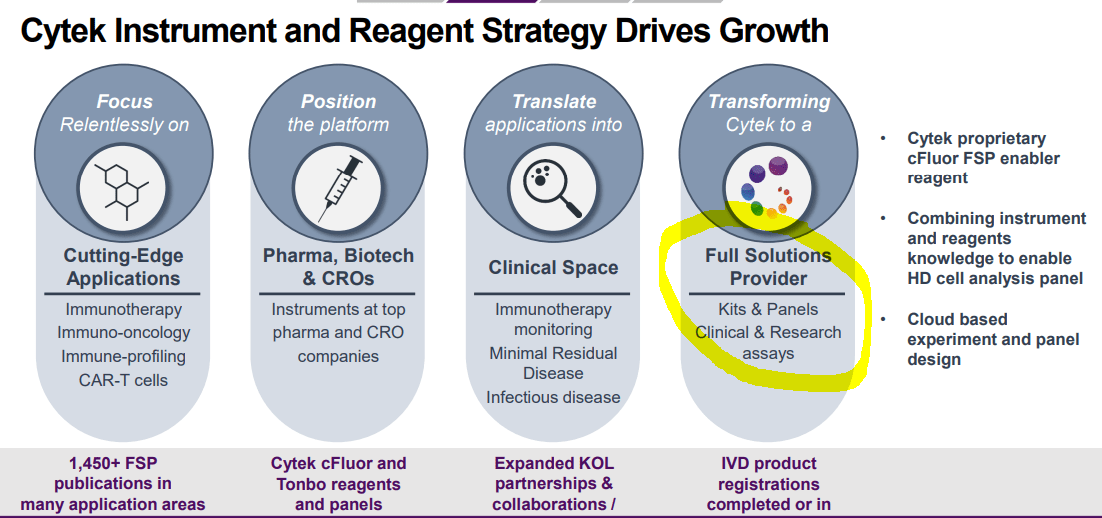

Cytek Investor Presentation

Cytek has a small group of peers that are useful for comparative analysis. Classified into two subsets, mature and innovators, each subset highlights where Cytek came from, and where they are going. Firstly, there is a select group of single cell and spatial biology innovators who are small in size, but operating at a loss. With Cytek now operating on a loss on a TTM basis, it is clear that the business environment is difficult despite advanced instruments. The largest peer is 10x genomics, a company on the boundary of next generation sequencing and single cell analysis. However, the company is an investor darling and generated significant amounts of cash during its IPO in 2019. This, and their leading platform, led to swift revenue growth and a high valuation, but losses remain extensive.

Standard BioTools and Akoya are both unique players in the mass cytometry and spatial phenomics space, respectively. Unfortunately, both are short of operational runway despite niche instrument offerings. The data clearly shows that Cytek offers a superior outlook with higher profit margins preventing cash burn, and a long runway to offset competition. The opportunity is also reflected in the valuations, as the short-runway and heavily indebted peers are swiftly falling in value. Even 10x Genomics has fallen 80% from highs in 2021, despite the higher P/S. When considering these points, it is clear Cytek is superior from a financial standpoint, but the valuation remains uncertain. Therefore, the positive sentiment in my prior analysis of Cytek remains.

Company | Cash ($M) | Debt ($M) | Quarterly Net Income (Loss $M TTM/4) | Runway (quarters) | P/S (TTM) |

Cytek Biosciences | 299 | 17 | (3) | 100 | 4.8 |

10x Genomics (TXG) | 418 | 102 | (64) | 6.5 | 6.8 |

Standard BioTools (LAB) | 155 | 102 | (19) | 8.2 | 1.9 |

Akoya (AKYA) | 60 | 75 | (16) | 3.75 | 2.3 |

A comparison with mature peers of reagents leader Bio-techne and advanced instrument provider Tecan Group ( will provide further valuation insights, particularly in Cytek’s future. Firstly, Tecan’s focus on value-added solutions such as automation and multi-mode analysis at a profitable level show where Cytek’s instrument platform can end up with time as economies of scale emerge. Then, as Cytek increases the sale of reagents and other consumables, Bio-techne showcases how even higher profits can be earned on top of instrument sales. But again, valuation data is mixed as Cytek is valued higher than the more similar Tecan.

The main benefit of the current valuation, however, is that Cytek is growing revenue far faster, above 20%, compared with Tecan’s 10% annualized long-term rate (and Bio-Techne’s 12.5% rate). I believe investors will benefit immensely if the financials improve towards these peers. Then, do not forget the opportunity to be acquired by a giant such as Thermo Fisher (TMO) or Danaher (DHR) is an additional shareholder catalyst that is of high potential* with the success of the platform.

* Do note that acquisition may or may not be influenced by a settlement with Becton, Dickinson (BDX) in 2021.

Company | 5 Year EBITDA Margin (%) | 5 Year Net Income Margin (%) | P/S (TTM) |

Cytek | 2.3 | 1.4 | 4.8 |

Bio-Techne (TECH) | 30 | 22 | 9.9 |

Tecan Group (OTCPK:TCHBF) | 17.5 | 11 | 4.1 |

Despite shares failing to gain traction in the 2023/24 stock market climb, Cytek remains financially superior to other small-sized innovative peers. There is also plenty of data from larger, but still innovative players that highlight the future opportunity that Cytek can grow into. As a long-term investor, I believe that Cytek has much in store in the years to come. However, I do not know when the industry will begin investing into innovation/R&D. In particular, the high interest rates have damaged the ability of pre-revenue companies to earn sufficient funding, and current economic data continues to highlight a strong economy that requires high rates for longer.

While I believe in taking advantage of the momentary weakness by investing on a recurring basis, a financial indicator risk-averse investors can look for is a return to net income profitability on a TTM basis. When this comes, I expect that the R&D investment landscape is far healthier than today and a new bull market will be just beginning.

Thanks for reading. Feel free to share your thoughts below.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.