Yong Chen/iStock via Getty Images

Yong Chen/iStock via Getty Images

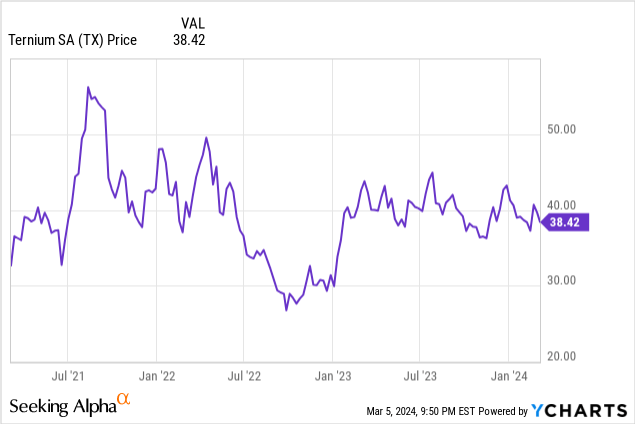

I turned bullish on Ternium S.A. ADR EACH REPR 10 ORD NPV (NYSE:TX) in 2019, when I argued the company’s investments in growth would start to pay off from 2021 on. Unfortunately the COVID pandemic delayed things, but the total return since my article in 2016 with a Buy rating exceeds 400%.

Seeking Alpha

I sold my position a while ago, but I am impressed with how this LatAm focused steel producer has been managed. The recent acquisition of Usiminas weighed on the 2023 income statement and will weigh on the cash flow result in the next few years as Ternium completes the necessary investments, but I think this acquisition will prove its value in the long term. This article is meant as an update to previous coverage. I'd like to recommend you to read my older articles to get a better idea of the company's business model and opportunities & challenges.

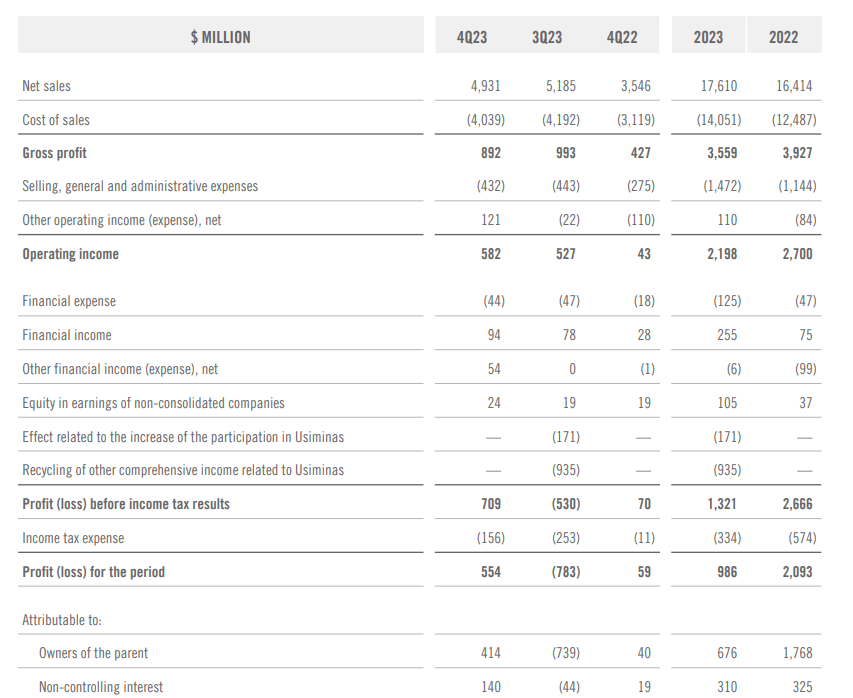

During the financial year 2023, Ternium reported a total revenue of $17.6B, thanks to a relatively strong performance in the second half of the year, as in excess of $10B of the full-year revenue was generated in the second semester.

Looking at the Q4 results, the gross profit did decrease by approximately 10% compared to the third quarter of the year, but the operating income increased to $582M due to XXXX. As the company further increased its net finance income (up to $50M in Q4 2023 coming from $29M in Q3 and $10M in Q4 2022), the pre-tax income came in at $709M. Substantially higher than the $530M pre-tax loss it recorded in the third quarter but that quarter included a $1.1B charge related to the Usiminas acquisition in July 2023. These expenses and items should be non-recurring (as it was related to the carrying value of the minority interest in Usiminas which had to be revalued based on the purchase price) going forward but have a substantial impact on the Q3 2023 and full-year 2023 results. Ternium is determined to improve the efficiency at Usiminas, and hopefully this will be reflected in an improved financial performance of Ternium as a whole.

Ternium Investor Relations

Looking at the Q4 results in particular, the net income on a consolidated level was $554M of which $414M was attributable to the common shareholders of Ternium. Considering there are 1.96 billion shares outstanding and one ADS represents 10 underlying shares, the Q4 EPS was $414M / 196M = $2.11 per share.

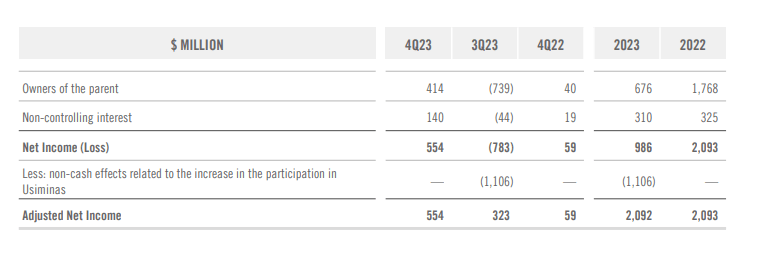

Looking at the full-year result, the $676M in net attributable income represents $3.45 per share. Purely based on that result the current share price which represents approximately 12 times the net income appears to be generous but let’s not forget the full-year results include the full impact of the $1.1B impairment charge related to Usiminas.

Ternium Investor Relations

Excluding that, the pre-tax income would likely have been $2.4B and the net income would have been $2.1B on a consolidated basis while the attributable net income would likely have been twice the $3.45 EPS recorded in 2023.

In the previous articles, I was very impressed with Ternium’s ability to generate a positive free cash flow, and that wasn’t any different in Q4 2023 or even the entire financial year.

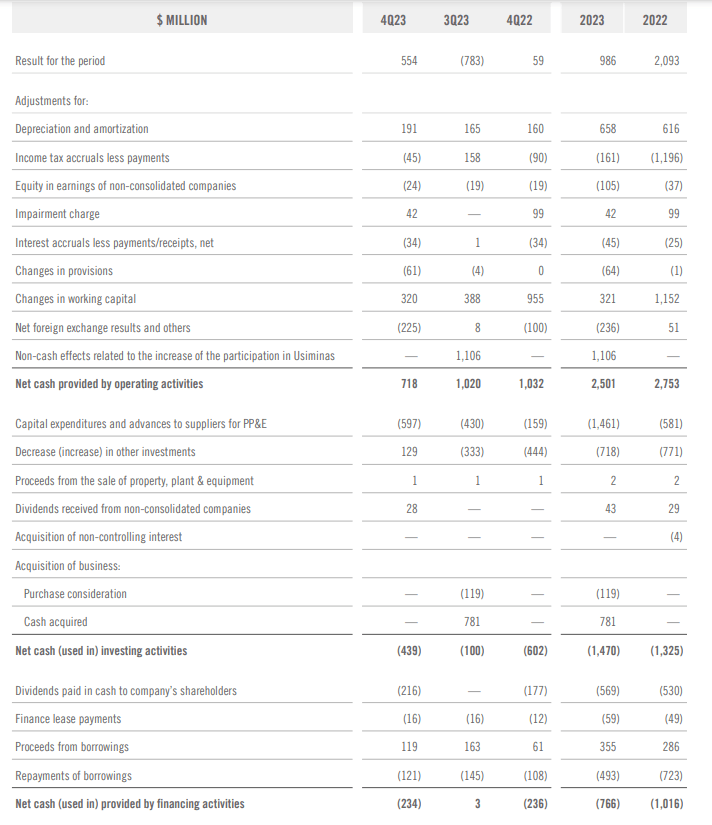

Looking at the fourth quarter, the company published a total operating cash flow of $718M which included a $320 change in working capital elements and a negative impact to the tune of $225M related to the FX changes. After also deducting the $16M in lease payments, the adjusted operating cash flow was $617M.

Ternium Investor Relations

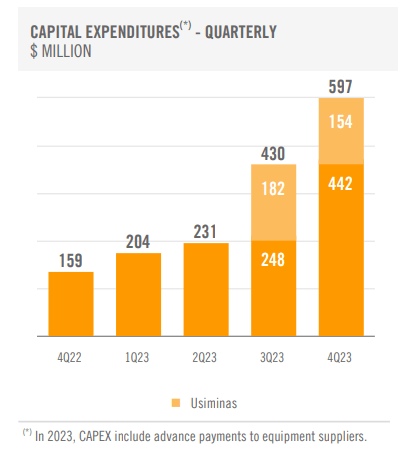

You’ll immediately see the total capex was $597M which means the company was barely cash flow positive. That being said, the last two quarters, the company has spent in excess of $330M on the Usiminas blast furnace relining while there were a bunch of other capital expenditures related to other growth prospects as well.

Ternium Investor Relations

The total capex will remain at an elevated level as Ternium is guiding for a capex of $1.8B this year, increasing to $2.5B as the Usiminas project will require approximately $1.5B in capital that year.

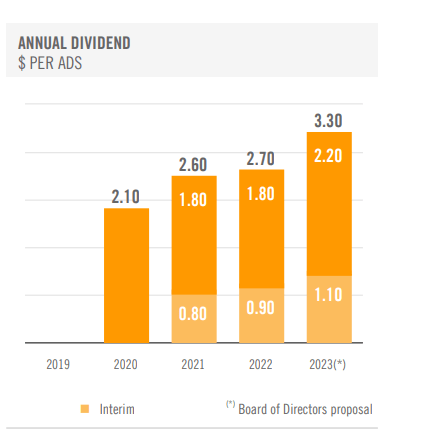

The company is proposing to pay a total dividend of $3.30 per ADS share and while that is fully backed by the underlying free cash flow, I am somewhat surprised the company isn’t putting a bit more money on the side to cover the capex-heavy years 2024 and 2025.

Ternium Investor Relations

Fortunately Ternium has a very healthy balance sheet. As of the end of 2023, Ternium had $1.85B in cash and $2.15B in gross debt for what seems to be $300M in net debt. However, the company also has other cash-like investments (deposits with a maturity of more than three months) on the balance sheet and it actually ended the year with $1.9B in net cash on the balance sheet. And that net cash position, in combination with the anticipated cash flows in 2024 and 2025, will go a long way to cover the total anticipated capital expenditures. Additionally, Ternium ended the year with a positive working capital position of in excess of $8B.

So although Ternium is facing high capex commitments in 2024 and 2025, the balance sheet is definitely able to handle that. Additionally, Ternium is relatively upbeat about the start of this year as it expects the Q1 2024 adjusted EBITDA to be higher than the Q4 EBITDA (which came in at $651M).

Despite the non-recurring items related to the acquisition of Usiminas, Ternium did very well in 2023 as the underlying net income and free cash flow remained very strong. The existing net cash position and the anticipated incoming cash flows should be sufficient to cover the anticipated capex, which means Ternium remains an interesting vehicle to gain exposure to the South American economies. The company ended the year with an enterprise value of approximately $5.6B (using the current share price) which means the stock is trading at just 2.75 times the 2023 adjusted EBITDA.

I sold my position in Ternium a while ago, but I’m positively surprised how well Ternium is performing and I am considering writing put options to establish a long position again.