janiecbros

janiecbros

Twist Bioscience Corporation (NASDAQ:TWST) is a promising bet on DNA applications with synthetic DNA, DNA products, and Next-Generation Sequencing [NGS] tools for researchers in several industries. TWST's IP has applications in health care, materials and chemicals, agriculture, and academic research. The company's Express Genes service effectively expanded TWST’s customer base, and as a result, its Q1 2024 report came in above management’s guidance. Yet, despite all these positives, my valuation analysis suggests TWST’s stock price already reflects this potential, trading at a relatively inflated valuation. This tempers my optimism on the stock itself. Hence, I rate it a “hold,” but I consider TWST a great buy on dip for opportunistic investors.

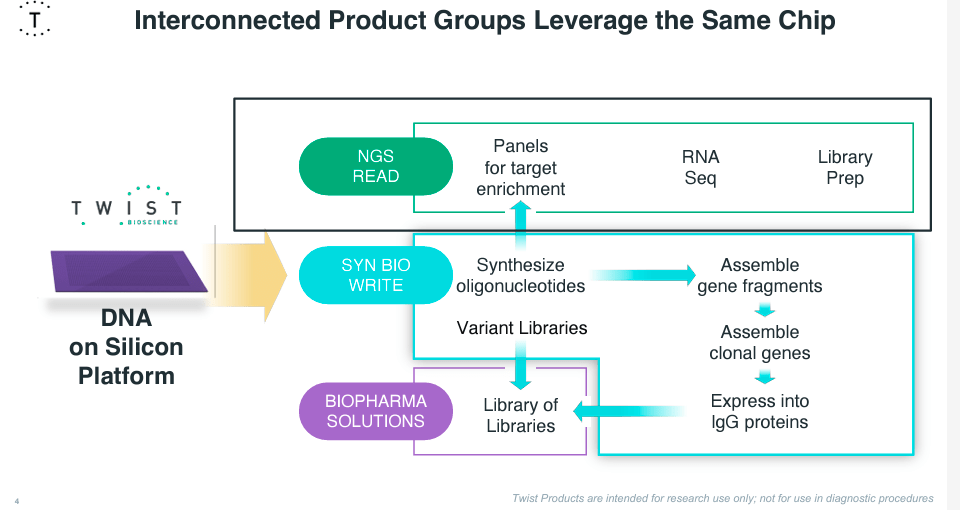

Twist Bioscience specializes in synthetic biology, delivering artificial DNA, DNA products, and NGS systems and tools. The company was founded in 2013 and is based in South San Francisco, California. TWST's platform automates and industrializes synthetic biology with a new method to produce artificial DNA by writing its information on a silicon chip, reducing production times and costs. You can think of TWST as a company that leverages its proprietary platform to manufacture synthetic DNA, which can later be used in various applications and can be mostly broken down into 1) Syn Bio Write, 2) NGS Read, 3) Biopharma Solutions, and 4) DNA Data Storage. As of the latest quarterly data, these segments represented 37.5%, 55.2%, and 7.3%, respectively, as DNA Data Storage isn’t generating revenues yet.

The company’s revenue-generating segments are promising already. Still, I believe TWST's DNA Synthesis Platform might have the highest potential yet, as it uses DNA synthesis to overcome DNA obtainment limitations. This effectively escalates DNA production and reduces costs. Moreover, this platform’s technology applies techniques from semiconductor production to improve efficiency at a lower price.

Source: 2024 AGBT Investor Dinner Presentation - February 2024.

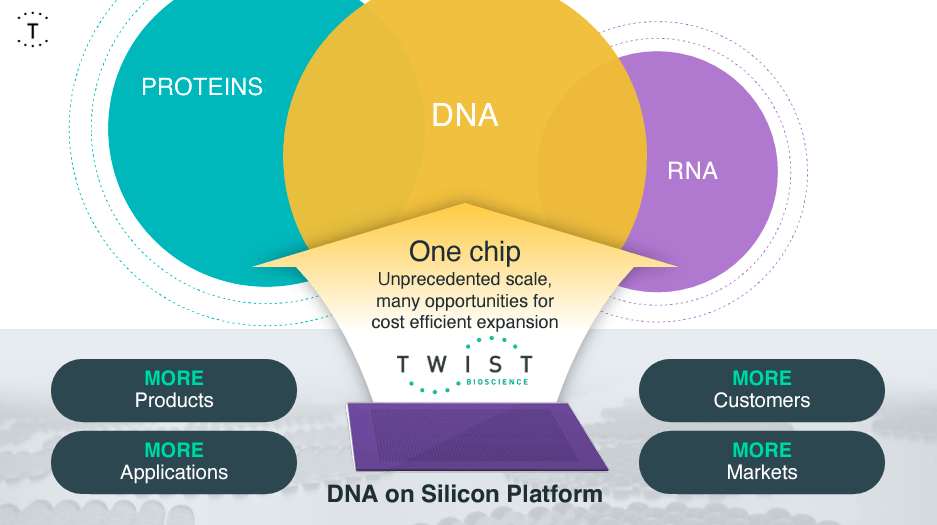

TWST’s platform uses silicon to create arrays of synthetic DNA to process up to millions of DNA sequences in parallel with high fidelity. As a result of automating this process, artificial DNA has become accessible, fulfilling the needs of researchers who require precise, large-scale DNA production. Such DNA production is key for various applications like therapeutics and drug discovery, test diagnostics, bio-based chemicals, engineering crops, and, as previously mentioned, potentially even digital storage for large amounts of data. Essentially, TWST's products can be used as tools for researchers in several biotechnology fields to manipulate genetic material. I believe it’s a game-changing technology still in its early stages.

Furthermore, TWST applies its technology to deliver a range of developments, including synthetic genes designed according to specifications, clone genes that are copies of precise DNA sequences, gene fragments for portions of DNA to be used for applications like gene or enzyme construction, and oligo pools for CRISPR gene editing, or Next-Generation Sequencing libraries. The company also has a service called Express Genes for the fast delivery of artificial genes. The NGS tools and systems for preparing library kits and sequencing panels for fast DNA and RNA synthesis are also important contributions. These applications further demonstrate the flexibility and wide potential that TWST’s IP has, which I think should reasonably add optionality to its valuation.

It’s also worth noting that TWST's Q1 2024 report once again came in above guidance, which is usually a positive sign for a company. The latest quarterly filing showed revenue growth and hit a new record of $71.5 million. TWST’s orders rose to $77 million, increasing its customer base, mostly attributed to the ongoing trend of clients adopting TWST’s new technologies in segments like synthetic genes, oligo pools, DNA libraries, and NGS.

Additionally, these revenues are highly profitable, with over 40% gross margins, which shows pricing power. Still, it’s worth noting that TWST is not yet profitable, but its EBIT margins have consistently improved. I noticed that TWST’s operating expenses are relatively stable, around $50 million for the last few quarters, and haven’t increased alongside its growing revenues. This is why EBIT margins are continually improving QoQ, and I think there’s a reasonable path towards profitability as long as this trend continues.

Source: 2024 AGBT Investor Dinner Presentation - February 2024.

Lastly, the company’s Express Genes service expanded, capturing more researchers as customers. This was mostly because of TWST’s five-day shipping turnaround for larger DNA preparations of up to 1 milligram. Interestingly, these developments occurred while slightly curtailing R&D expenses, tilting the company’s efforts towards commercializing its IP.

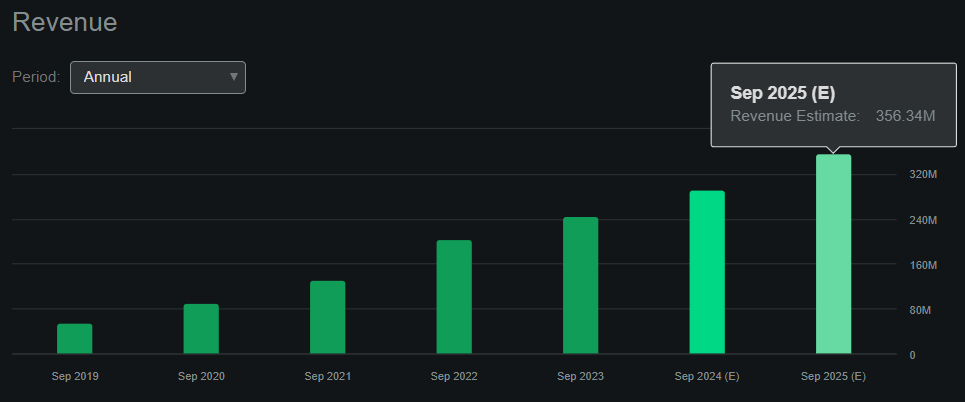

From a valuation perspective, TWST is not a microcap biotech worth a few hundred million dollars in market cap hoping for FDA approval. TWST is slightly more mature than that, with consistently growing revenues and a respectable market cap of about $2.0 billion. However, if we annualize the latest quarterly revenues, TWST’s current revenue run rate is approximately $286.0 million annually. That would imply a high P/S ratio 7.06, notably higher than the sector’s median P/S multiple of 2.06. Even Seeking Alpha’s dashboard revenue forecasts for TWST in 2025 imply a valuation premium. By 2025, the company is projected to generate about $356.34 million in yearly revenues, which means a forward P/S multiple of 5.67. This multiple is still considerably higher than its peers, so TWST trades at a premium.

Source: Seeking Alpha.

Nevertheless, TWST’s liquidity seems safe, with $311.1 million in cash, cash equivalents, and short-term investments. Furthermore, TWST's CEO expressed the company’s focus on revenue growth and financial discipline to achieve profitability and sustainable success. So, I think TWST is currently pivoting into a monetization phase, caring about its financial sustainability over the long run. This is promising, and if we annualize its most recent quarterly cash burn rate, TWST does appear healthy for now. I estimate TWST’s quarterly cash burn to be about $24.5 million by adding up its cash flow from operations and CAPEX. This would mean TWST burns through $98.0 million annually, implying a cash runway of roughly 3.2 years. However, since TWST’s revenues should continue growing and its focus is on cost management at this stage, I’d argue that this is a conservative estimate.

Source: TWST’s Fiscal 2024 1Q Financial Results.

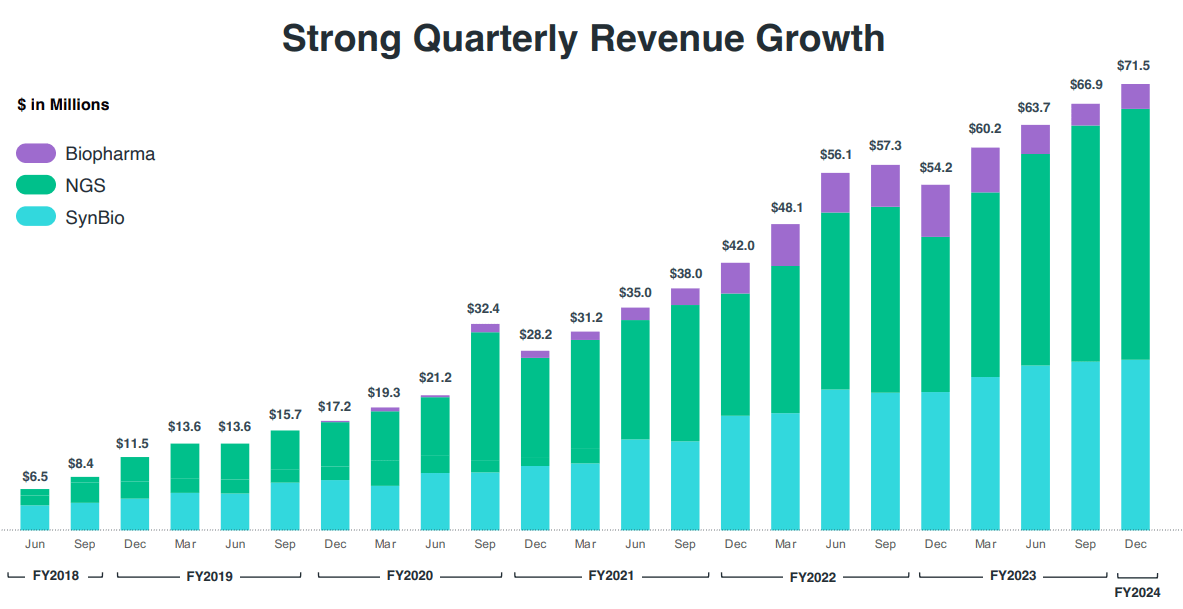

As you can see in the image above, the company has had an impressive growth rate since 2018. Using the figures from that chart, I estimated a CAGR of about 54.7% since June 2018. This is, without a doubt, explosive growth and shows that TWST undoubtedly deserves a growth premium. This is particularly true after you consider that DNA data storage isn’t even being monetized at this stage, and that could potentially be a game changer down the road. After all, DNA storage could be much more cost-efficient for certain types of data that don’t require frequent read-and-write operations. For instance, long-term data storage would greatly benefit from DNA’s denser and more durable properties than traditional cloud storage.

So, putting it all together, TWST is a promising biotech company with impressive top-line growth that trades at a relatively elevated valuation multiple. This makes me lean towards a more neutral assessment of the company, as I’m incredibly bullish on the underlying tech and business fundamentals. Yet, simultaneously, my optimism is tempered by the already inflated valuation. This leads me to a “hold” rating, but I lean on the bullish side. But for now, I think this is a “buy on dips” stock rather than a “great buy” at this time.

Moreover, I’ve identified a few caveats that further detract from the “buy” rating on TWST. First, I believe that the recent efforts to cut costs and focus on a path toward profitability are commendable from a financial perspective but may risk the company’s long-term prospects. Synthetic biology and DNA applications remain a rapidly evolving field, and without constant R&D expenditures, there’s a real risk that TWST’s IP portfolio might become outdated relatively quickly. Also, while DNA applications are promising, other competing narratives might attract more investor capital if TWST’s tech becomes stale or meaningful progress halts. Hence, this company might not be ideally suited to look for profitability just yet. Instead, it may be better to focus on finding a patent to achieve a lasting business moat.

Potential competing narratives. (Source: StartUs Insights.)

However, today, I concede that TWST’s platform, particularly regarding DNA synthesis, is almost without a match. TWST leverages this to offer a wide range of applications, from healthcare to agriculture, at lower costs and higher speeds, making it more scalable. Given that the company’s business is centered around synthetic biology, we estimate its current market size to be around $11.4 billion (Markets and Markets, 2022). Moreover, the source also reported a sector-wide CAGR of 25.6% until 2027, below TWST’s realized CAGR since 2018. This could imply that TWST’s growth rate will likely decline, trending towards the sector’s CAGR. However, the flip side of that argument is that TWST’s above-average CAGR corroborates its strong value proposition with its customers. We don’t know at this time, so it’s a risk that new investors would take on if they invest at these levels.

Overall, TWST is one of the most promising biotech stocks I’ve researched. It’s monetizing its platform and has consistently grown revenues at an impressive CAGR for several years. Moreover, I think there’s still much untapped potential in its IP, especially in DNA Data Storage. This alternative data storage method could become a game changer for certain storage needs. Also, TWST’s balance sheet seems solid, and its cash runway also appears safe. Yet, at the same time, it’s undeniable that the stock is already trading at a high valuation multiple. This tempers my enthusiasm for the stock, not the business itself or its technology. Hence, I rate TWST a “hold,” but I still consider it a great buy on dips.