ayo888

ayo888

One of the biggest dangers I see for investors today is to simply take things at face value. They assume the stock market will always be a safe place in the "long run" which brings to mind the famous phrase from 20th century economist John Maynard Keynes: In the long run, we're all dead. (If that's a bit disturbing, just sing the Eagles hit, "The Long Run" to yourself).

Another danger is not about what might happen, since predicting the future path of the stock market, while it gets headlines, should truly be a minor factor in an investor's process. Note that I said "predicting" the market. What I do think is extremely valuable (to me) over the decades managing money professionally is a simple, yet course-changing concept:

This article dives into one such approach that I have always had in the "toolbox", but which I thought would be a good one to present to Seeking Alpha's audience at this stage of the market cycle. It is something that can be used any time or even all the time, and with a ton of flexibility as to which securities are used to implement the strategy.

But what it all boils down to is this: by using pairs or sets of ETFs, some that aim to profit from up markets and others from down markets, using them in tandem, but using levered ETFs to play the "defense" to spend less capital, there's a differentiated way to navigate these strange modern markets.

Keep in mind that with leveraged ETFs, there are a host of risks that should be understood by investors before even considering them. But in this case, I am using them as essentially a replacement for put options on major stock indexes or index ETFs, since not all investors want to venture into using options. Inverse ETFs can lose most or all of their value (but heck, so did the Nasdaq about 20 years ago!). But in that sense they are similar to options, but do not have expiration dates like options do.

This article is primarily what I think investors should learn "right now" so that they have a better chance of staying solvent the next time the broad stock market does what it has done regularly over the long term: take away huge chunks of previous gains, and turn long-term investing into an unexpected emotional situation. That in turn increases the chances of making short-sighted decisions.

Modern markets are filled with so many innovative tools, investors can go much further than in past eras in, as I say, "shrinking the range of possible outcomes." In other words, while investors can hold their noses at the thought of deviating from an "own the market and sleep at night" approach (which I think is jaded by the old "recency effect" because we have not had an extended downturn in 15 years), some may feel as I do that it is not only possible to be a long-term, return seeking investor, but do so without leaving oneself vulnerable to life-altering drawdowns. That's risk management.

And while there are many ways to defend without stopping one's offensive approach, by trading off just a bit of upside potential, I think there are ways to deliver a smoother ride. In other words, a far less emotional one.

Inverse ETFs, put options, T-bill investments, CDs, true diversifiers (like gold used to be and Bitcoin claims to be) are all potential resources we can use to manage the risk of major loss, all while pointing northward, pursuing solid long-term returns from stock market investing. So the rest of this article will focus on a specific approach I have used over the years, especially in times of increasing market stress.

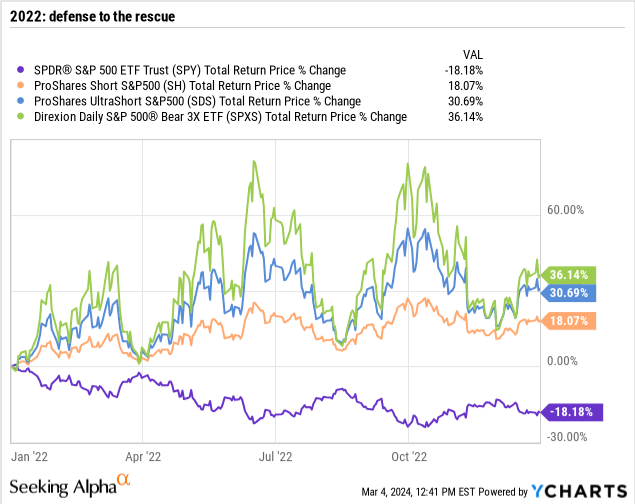

First, let's quickly visualize what my version of risk management is, by reminding about or introducing the concept of inverse ETFs. They come in a much wider variety than back when I started managing my first mutual fund back in August of 2008. That was quite an initiation! And other than the one in orange in the charts below, there was not much else to choose from, and even it had just enough liquidity to consider owning it for the fund I ran.

Fast forward to today, and inverse ETFs are much more mainstream. And while I lament the fact that the ones with the most leverage tend to get the most attention, I get it. And I use all three varieties shown: single inverse, 2X inverse and 3X inverse. And I consider inverse ETFs that target not only the S&P 500, but the Nasdaq 100, the Dow, small caps, China, bonds and even single securities.

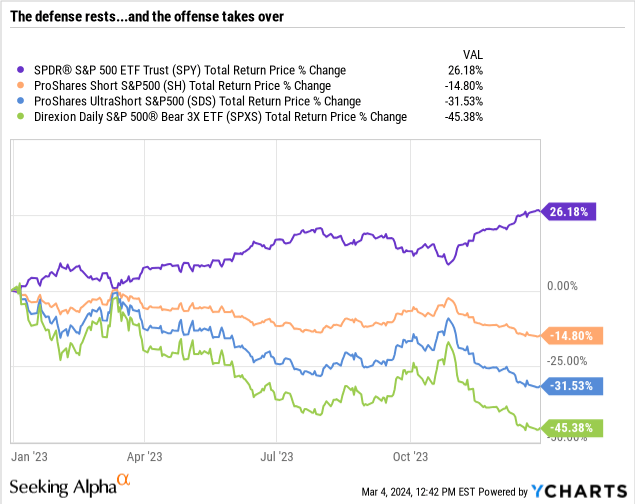

As shown below, 2022 was a good time to know how to manage risk. Frankly, so was 2023. Because it is ALWAYS a good time to know how to manage risk! Last year, risk management via inverse ETFs was a losing proposition for pretty much the entire year. However, these are absolutely not "buy and hold" securities.

If anything, I use them instead of put options on major indexes. The tradeoff: inverse ETFs typically require more capital than options to get the same level of "tail risk" protection against sudden adverse market events. But while options have limited life and you pay to have more time for them to pay off, the "cost of hedging" is more straightforward with inverse ETFs. They require less of that Greek alphabet stuff that a "meat and potatoes" risk manager like me needs to deal with.

With these, I know what I am getting and while there is always a risk they don't function properly (as with many ETFs and securities in general), I think there's enough tenure behind a lot of these to make me feel they are better put option surrogates than they were back in 2008, when a new mutual fund manager (yours truly) saw the S&P 500 drop 55% the first seven months I was in the hot seat. FYI, my fund was off about 16% and I told myself I'd never let a portfolio I managed fall that far, peak to trough, ever again if I could help it. So far, so good on that promise to myself.

Yet I do have concerns that investors young and old, new and experienced, don't have enough appreciation of the tools and the use cases for these vehicles. My late mother's favorite expression was "Better to have it and not need it than need it and not have it!" She was usually referring to bringing a raincoat to school on a cloudy day or something like that.

But I repeat it to myself frequently, relating to my broad approach of "playing offense and defense at the same time." Because the latter may not end up being used, but then again neither does that little container of extra gasoline folks keep in their vehicles, just in case they run out of gas and are nowhere near a gas station. And while some investors prefer to throw caution to the wind and not spend capital on hedging techniques, I do so regularly, in one form or another. I am willing to give up making slightly less than my neighbor in an up cycle, in order to still be in my home when that hypothetical neighbor is selling theirs to replace the liquidity they lost when a strong market finally did, well, what strong markets usually do eventually.

With that introduction or re-introduction to my brand of risk management from a conceptual level, here's a straightforward introduction to one of the approaches I incorporate at different points in the market cycle. Welcome to "ETF Arbitrage."

I just reviewed the fact that for the S&P 500, there are ETFs that can short it 1:1, 2:1 and 3:1. That's a lot of "shorting" power in my hands. Is it needed? Here's why I think it is.

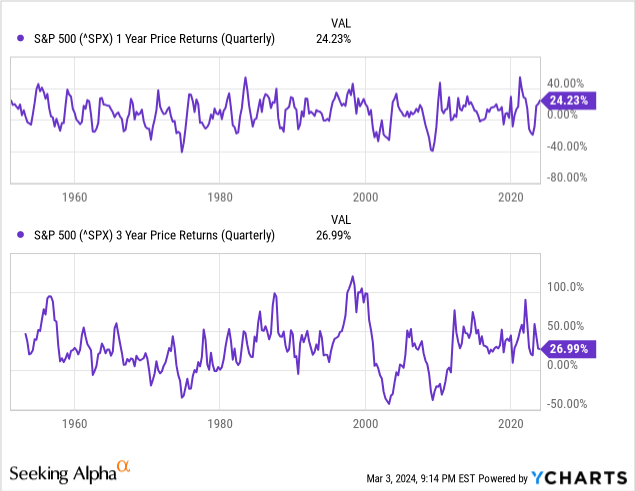

That chart below shows "rolling" 1-year and 3-year (cumulative) returns for the S&P 500 Index since it debuted during the 1950s. The top chart shows many 1-year time frames that produced losses of at least 20% and up to 40%. That should not surprise anyone, and "buy and hold" types are built (or should be) to simply blow off such events. After all, if one is really buy and hold, if they decide to "buy and hold... until something goes really wrong" then it is not a strategy at all. It is speculation, and too much risk-taking for my tastes.

I don't bring this up to try to frighten investors or to make a case for a deep bear market. I have no idea if and when we'll get one. But I do know that I am always ready for the start of a deep decline or a sudden drop in market prices that does not soon recover. That's what living through and investing through the 1987 crash, the dot-com bubble, the Great Recession, early 2020 and most of 2022 has made second-nature to me as an investor, and a key part of my process back when I managed other people's money, since they tended to be "stay wealthy" types, rather than "get wealthy" folks.

So, that 3-year rolling chart is important to me. Because many investors can look at the recent past and have a knee-jerk reaction that all dips can be bought. But as we see on the right 1/3 of the chart, we've seen the S&P 500 fall by nearly 50% cumulatively over three years not once, but twice, in only the past 23 years. That signals to me that investment management is nothing without risk management.

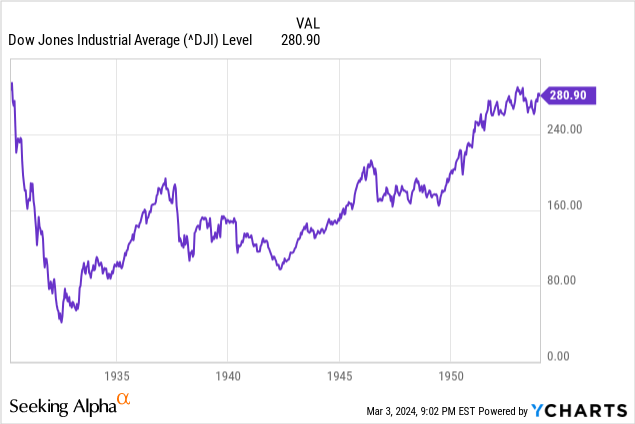

Here's the Dow Jones Industrial Average, albeit with some very ancient history. But again, just as I cannot have predicted a pandemic-induced bear market, I did assess at the time that risk was abnormally high. So it didn't take much of an excuse for markets to bail in 2020. That was a "flesh wound" with a quick recovery. This is 1930-1954!

And for those who know their market history, they will note that the peak level of the Dow at the far left of the chart is AFTER the Crash of 1929. So it doesn't even include that event. Do not get lulled into complacency. The stock market is a great place to make money over time, in a highly-liquid fashion. But to just "let it ride" is not my mantra, ever.

Here's what ETF Arbitrage is about, at a high level:

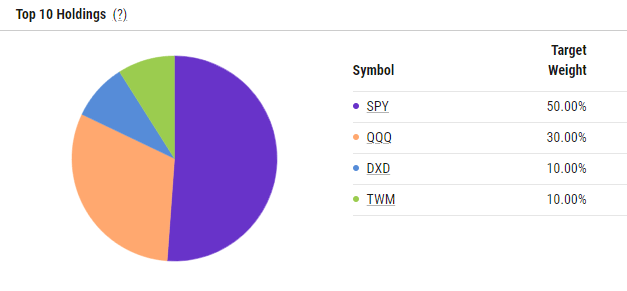

This takes some opinion-generation. To keep it simple, let's say that I'm looking at four major US stock market indexes and their associated long and inverse ETFs: S&P 500, Nasdaq 100, Dow Jones Industrials and Russell 2000 Small Cap. In this case, I've decided I am going to maintain an 80% combined allocation to the two markets of those four that I believe will do the best over the next six months. I chose the SPDR S&P 500 (SPY) and Invesco QQQ Trust (QQQ) in this instance.

The other 20% will be allocated between the two markets I think will perform the worst during that same period, in this case the Dow and the Russell 2000. Here is what this sample educational model I created looks like:

Ycharts

In this example, I'm using 2X levered ETFs for the "short markets, ProShares UltraShort Dow30 (DXD) and ProShares UltraShort Russell 2000 (TWM), so it can be assumed I would not hold them for years, maybe months or a few quarters, tops, due to what I noted earlier about the risks of those ETFs as longer-term holds when the market goes against them (i.e. up in this case). But for simplicity to show the concept, I'll leave them that way, with no rotation i.e. "active management" around that 4-ETF mix.

So, if the market performs uniformly, and all four market segments go up about the same, my 80% long and 20%x2=40% short should land my performance around 40% that of the stock market's over that time. But the idea of arbitrage is for those more frequent periods, which can last a long time, where certain segments outperform others. So, ETF arbitrage aims to exploit those differences in performance between market segments, but with an infinite amount of ways to structure and rotate the positions as one sees fit.

Remember that inverse ETFs, even the single inverse varieties, get less useful the longer the market goes up. That's why investors are told not to consider them to be more than 1-day holdings. In my own experience, I have used them for as long as the market is not rising consistently for an extended period of time.

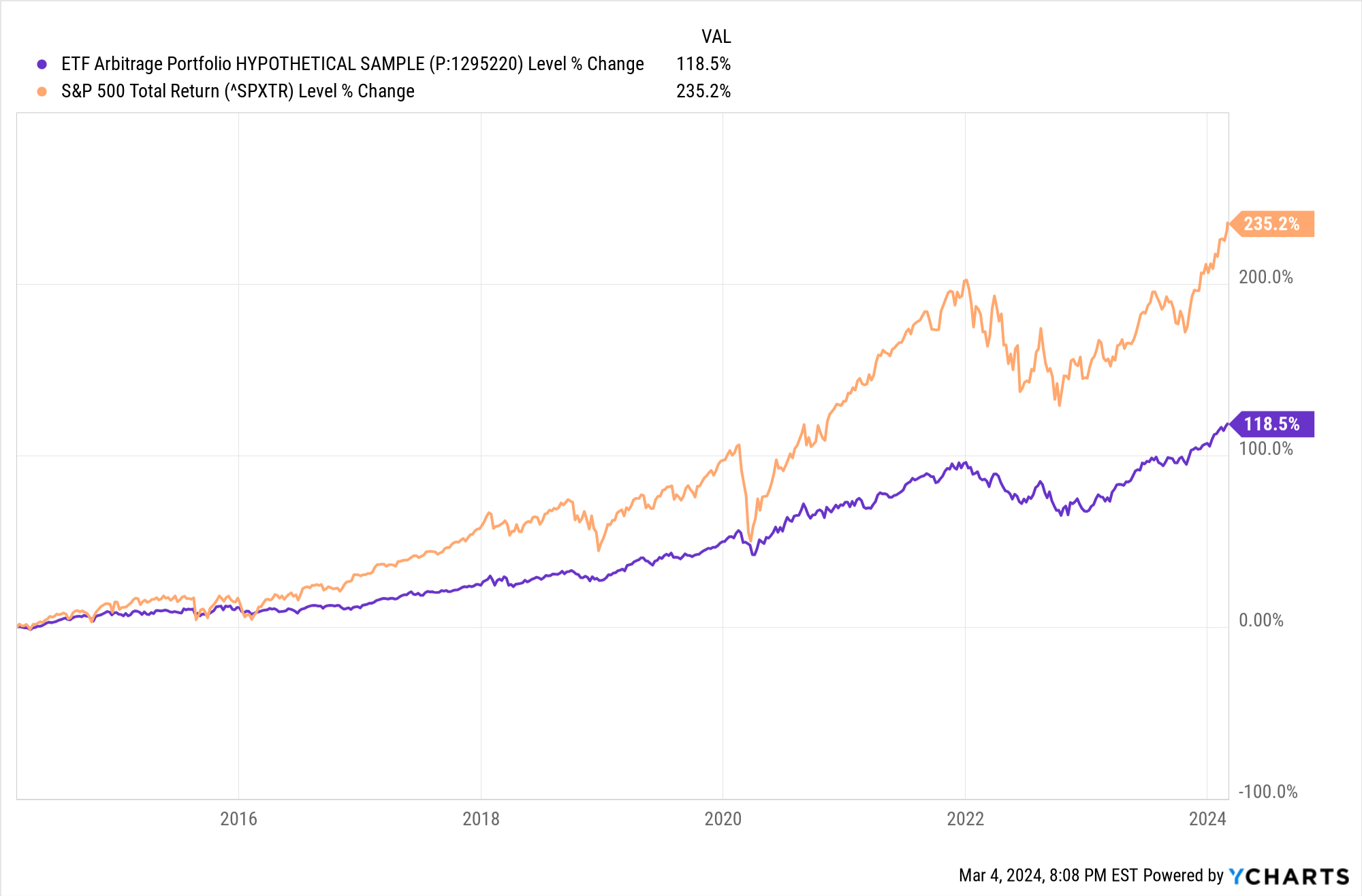

But that's what has generally happened the past 10 years. So the worst way to evaluate the effectiveness of ETF Arbitrage would be what I show below: a static asset mix, with no adjustments made, either to rotate among long and inverse, or among the four (in this case) market segments.

Ycharts

That said, as bad as the headwind was by allocating 20% to that pair of 2X inverse ETFs for a 10-year period when the S&P 500 more than tripled, this "slapped together" hypothetical sample ETF Arbitrage model portfolio STILL doubled in value over that time, for an annualized return of more than 7% per year. Also notice that in 2020, at the bottom of the 5-week, 33% SPY crash, the two growth lines were nearly even. You can clearly see the orange line (S&P 500 index) crashing, but the purple line representing the ETF Arbitrage sample barely budged, relatively speaking.

Again, this is longer than the expected holding period for those 2X inverse ETFs, but the point is this: The S&P 500 has taken investors on a wild ride since the start of 2022. It fell more than 20% and then came roaring back. Recent all time highs are nice, but all that really meant to me is that finally, the market ended two years of negative returns since 1/1/2022!

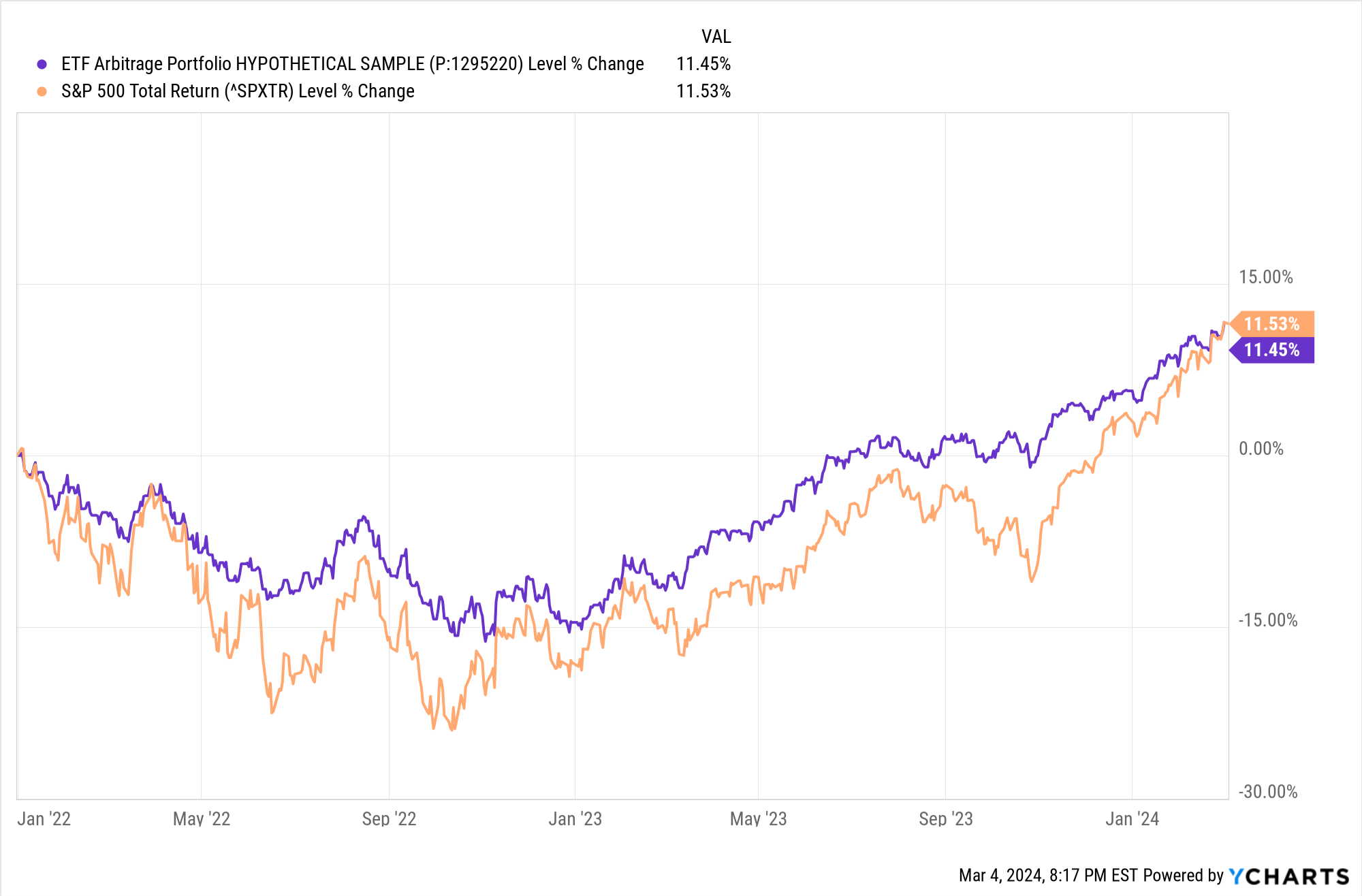

Ycharts

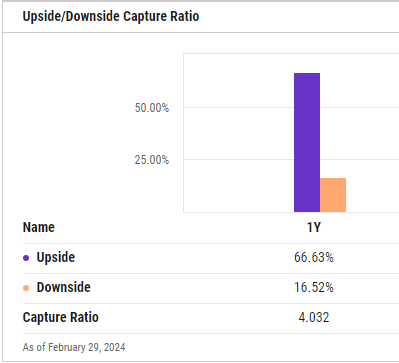

The ETF Arbitrage sample model here ended up in essentially the same place, but contained much of the downside risk. I pulled this one interesting snapshot from the data I ran. Below, it shows that over the past year, the S&P 500 gained 32% to the ETF Arbitrage model's 26%. That's not bad for a portfolio with a hedge and not active management as would normally be the case. But recall that even the past 12 months were a gyration up and down. The S&P 500 traded between 3,800 and the current level of over 5,100 during that period. But as shown below, the ETF Arbitrage model sample "captured" 2/3 of the up moves and only 16.5% of the down moves of the S&P 500.

Ycharts

I realize that this was not the "classic" article in that I did not end with a "buy this" or "sell this. My "rating" is a very strong BUY... on understanding the power of ETF Arbitrage, its extreme flexibility, the fact that it does not mean giving up on big returns, and that once an investor learns to think more like what this broad style of "offense and defense at the same time" aims to do, investing goes from forcing oneself to be a hopeful long-term investor to taking charge over setting boundaries for what is allowed to happen to a portfolio's value over time. In particular, reducing the financial and emotional cost of suffering through potential market washouts that don't reverse themselves as quickly as today's "buy the dip" investor has gotten way too used to seeing.

I have been strongly considering creating an ETF Arbitrage "tool" which investors can use to stress-test their own combinations of long and inverse ETFs to their heart's content, since I cannot possibly show even a fraction of the potential structures and rotational methodologies. Yes, in nearly 3,000 words, I've merely scratched the surface on the topic of ETF Arbitrage.

But I welcome feedback and interest on creating a tool, which I suspect I can embed in an upcoming article if demand for it is there.