Extreme Media

Extreme Media

I desire no future that will break the ties of the past." - George Eliot

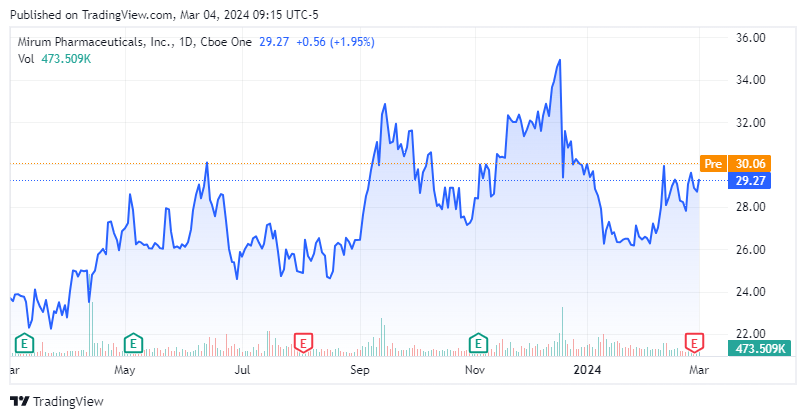

Today, we peek back in on Mirum Pharmaceuticals, Inc. (NASDAQ:MIRM) since our last article on this intriguing biopharma concern in April 2023. The company delivered better-than-expected Q4 results last week. In addition, losses are projected to drop dramatically as sales growth clocks in around 70% for the fiscal 2024 year. An updated analysis of Mirum Pharmaceuticals follows below.

Seeking Alpha

Mirum Pharmaceuticals' headquarters is in Foster City, CA, just outside of San Francisco. This commercial stage biopharma is focused on the development of novel therapies for debilitating rare and orphan diseases. The stock trades for around $30.00 a share and sports an approximate market capitalization of $1.35 billion.

February Company Presentation

The company's primary growth driver is an oral solution called Livmarli which was FDA approved in 2021 for the treatment of cholestatic pruritus for Alagille syndrome [ALGS] patients. The compound was approved in Europe for the same indication late in 2022. ALGS is a rare genetic disorder that affects one to every 30,000 to 40,000 people born in the United States.

February Company Presentation

Livmarli should also get approval to treat cholestatic pruritus in patients with progressive familial intrahepatic cholestasis [PFIC] later this month. This will add 20% to 25% to its potential approved target market. Mirum was also developing Livmarli to treat biliary atresia, but a Phase 2 trial failed to meet its endpoints late in 2023.

Elsewhere in the company's pipeline and product portfolio, Mirum has Cholbam which was approved in 2015 for some very rare forms of bile acid synthesis disorders that affect less than 2,500 people in the United States per year. In October, the company announced positive Phase 3 trial results from a study 'RESTORE' evaluating its compound Chenodal to treat cerebrotendinous xanthomatosis, or CTX. Management plans to file a New Drug Application or NDA for this indication sometime in the first half of this year. Chenodal is already approved for treatment of radiolucent stones in the gallbladder. Mirum Pharmaceuticals acquired both of these compounds from Travere Therapeutics (TVTX) last summer for $210 million upfront, as well as roughly $235 million in potential sales milestones.

February Company Presentation

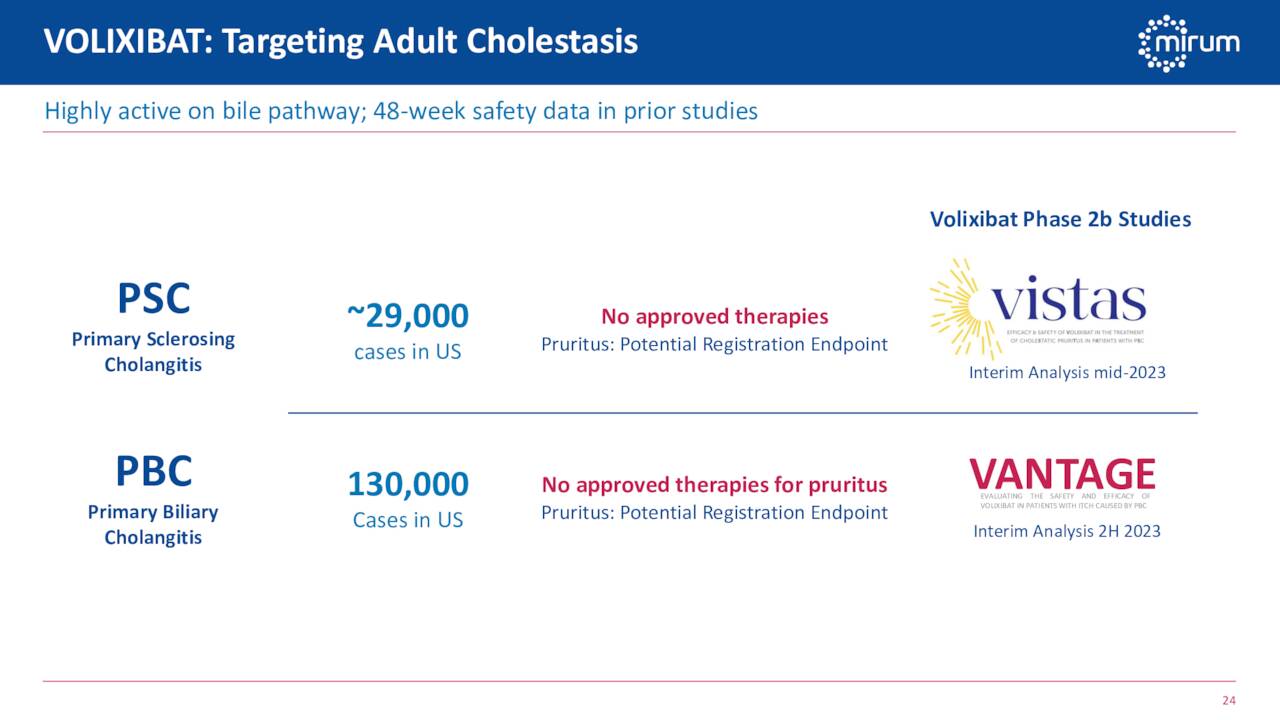

Finally, the company is developing a candidate called Volixibat as a potential treatment for Adult Cholestasis. Interim data from two studies (VISTAS, VANTAGE) targeting primary sclerosing cholangitis [PSC] and primary biliary cholangitis [PBC]. Dose selection interim data from both of these studies should be out in the first half of the year. Both studies continue to enroll patients, as both have the goal of supporting registration.

January 2023 Company Presentation

Mirum Pharmaceuticals posted its Q4 numbers on February 28th. Mirum delivered $69.6 million worth of revenues during the quarter. $28.1 million came from the recently acquired Cholbam and Chenodal franchises. $41.4 million was from Livmarli. $31.4 million of this came from the U.S., which represented 63% year-over-year growth. Overseas demand continues to see 'strong uptake' according to management, but quarter-to-quarter sales have much more variability.

Management provided initial FY2024 sales guidance for $310 million to $320 million, which would roughly be a 70% increase over FY2023's revenues.

Since fourth quarter results hit the wires last week, H.C. Wainwright ($58 price target), Leerink Partners, JMP Securities ($69 price target) and Robert W. Baird ($34 price target) have reissued Buy ratings on the stock. Late in October, Cantor Fitzgerald started MIRM as a new Buy with a $50 price target, as it sees the company eventually reaching $1 billion in peak sales.

Approximately 18% of the outstanding float in the shares is currently held short, and insiders hold just over two percent of the stock. So far in 2024, several insiders have sold just under $600,000 worth of equity collectively. The company ended the fiscal 2023 year with a bit over $285 million of cash and marketable securities on its balance sheet. The company has not filed its full-year 10-K year for FY2023 but did list $306 million in convertible notes on its third quarter 10-Q.

Mirum Pharmaceuticals lost $3.94 a share in FY2023 as sales soared to just over $196 million. The current analyst firm consensus sees losses falling to just less than a buck a share in FY2024 as revenues rise to $315 million. The project profits of nearly a dollar a share in FY2025 on better than 35% sales growth.

February Company Presentation

The company has several key milestones before the first half of this year is over, which are nicely summarized above. Mirum is seeing considerable sales traction from Livmarli and is projected to become profitable in FY2025. The stock trades at just over three times FY2025E revenues, which is more than reasonably valued. A key reason the stock remains comfortably below most analyst firm price targets. Given its wholly-owned portfolio, MIRM would also make a logical buyout target for a larger concern.

Therefore, I will continue to maintain my core stake in MIRM as the company is advancing its pipeline and delivering solid revenue growth and its longer-term future seems bright.

It is difficult to live in the present, pointless to live in the future and impossible to live in the past." - Frank Herbert