Leon Neal

Leon Neal

My thesis is that Take-Two Interactive (NASDAQ:TTWO) will have considerable success with GTA VI and that this will cause short-term price returns worth holding the stock. However, it won't deliver exceptional alpha over the long term based on less popular titles comprising a large portion of the total gaming portfolio. I consider the stock fairly valued at this time, with a significant risk of overvaluation around the time of GTA VI being released and the year following this.

The financial expectations for GTA VI are incredibly high, reflecting the historical success of the GTA brand but also the high investment in its production. GTA VI's development costs are rumored to be between $1-2 billion, according to Game Pressure. Analyst Joost van Dreunen is predicting that the title will need to generate outsized sales to break even on these costs. Forecasts at this time suggest that the title could sell around 25 million copies over its launch period. However, this is optimistic, and it anticipates a 20% increase in console sales, forecasting 125 million PlayStation 5 and Xbox Series X/S units on the market by 2025. Revenue from the title should match the success of its predecessor, GTA V, which achieved $1 billion in revenue in just three days. He estimated that the game will find about 12-14 million buyers in the first 24 hours after release. To contrast this to GTA V, it sold 11.21 million copies in the first 24 hours of release.

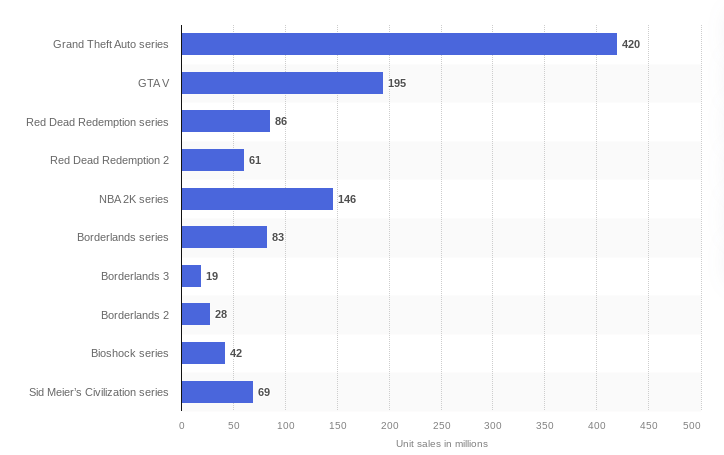

GTA V had a production cost of $265 million and has generated about $7.7 billion in revenue, selling around 185 million copies since 2013. That makes it one of the most successful video games in history.

Take-Two Interactive's portfolio of games includes major franchises like BioShock, Borderlands, Civilization, GTA, Mafia, Max Payne, NBA 2K, PGA Tour 2K, Red Dead, WWE 2K, and XCOM. GTA V is one of the most profitable and well-known in its portfolio, and GTA VI is expected to follow suit.

Despite a lowered FY25 bookings outlook, analysts remain bullish on TTWO. The firm revised its net bookings to $5.315 million for FY23, which is a 4% decrease from the previous guidance. The revision attributes shifts in release dates and variations in mobile advertising and NBA 2K24 sales. In FY25, bookings are expected to exceed $7 billion, down from $8 billion, but FY26 is expected to show YoY growth, in large part caused by GTA VI sales.

However, TTWO's recent earnings results are remarkably positive, with EPS GAAP actual results beating consensus estimates by $0.18. Additionally, the firm beat revenue estimates by $1.26 million. However, Q4 earnings, which come next, are expected to show an 87.09% YoY decrease in EPS normalized actual, according to Seeking Alpha.

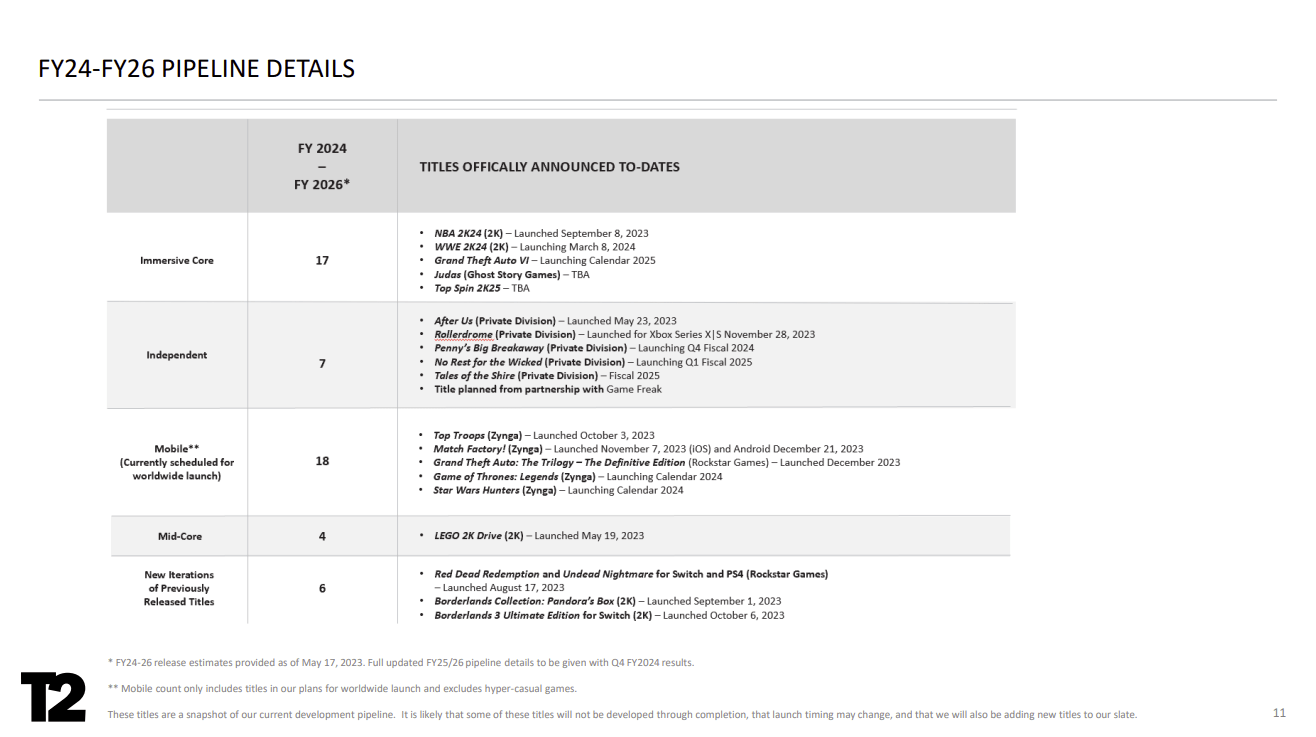

Consider also the pipeline for the next two years, which I believe shows outsized success to be had from GTA VI, with other titles generating significantly less popular anticipation. This contributes to my overall thesis that GTA VI is going to be immensely successful, but because this will be diluted by less popular projects, TTWO still doesn't look like a compelling investment. However, I think if Rockstar Games, the producer of GTA, Red Dead Redemption et al., were available as an individual investment, it would be the ideal exposure to have in the gaming industry.

Take-Two Interactive Q3 2024 Results

Take-Two Interactive All-Time Game Title Unit Sales Worldwide 2024 (Statista)

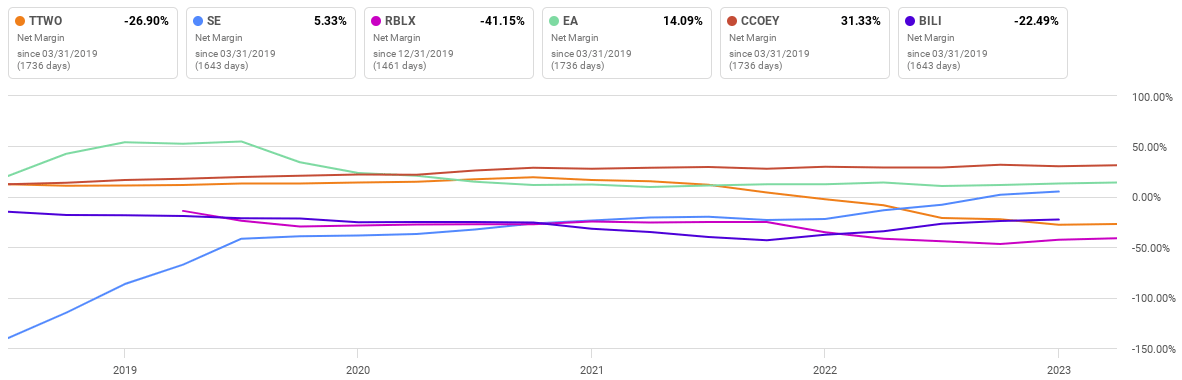

Most notably, at this time, TTWO's TTM net income margin is negative, at -26.9% as of the last report, significantly worse than the sector median of 3.45%. If we compare this to some of TTWO's similar-sized peers, we can see that it also ranks considerably poorly:

Seeking Alpha

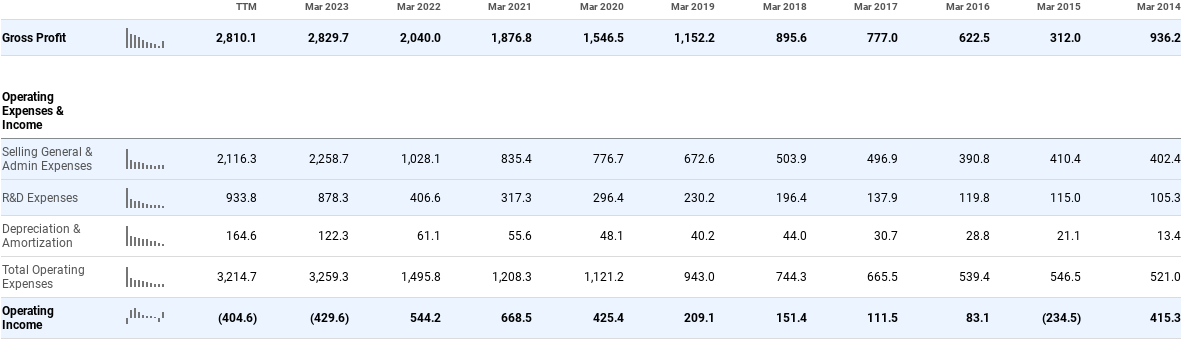

TTWO's operating loss at the moment is largely a result of higher SG&A expenses and R&D expenses:

Seeking Alpha

However, the firm notes in the Q3 earnings presentation:

We are currently working on a significant cost reduction program across our entire business to maximize our margins, while still investing for growth. These measures are incremental to, and even more robust than, our prior cost reduction program, and we aim to achieve greater operating leverage as we roll out our eagerly-awaited release schedule. - TTWO Q3 2024 Earnings Presentation

Take-Two also has a moderately stable balance sheet, which I estimate will allow the business to focus on profitability adequately moving forward. At this time, its equity-to-asset ratio is 0.57, and it has a debt-to-equity ratio of 0.41.

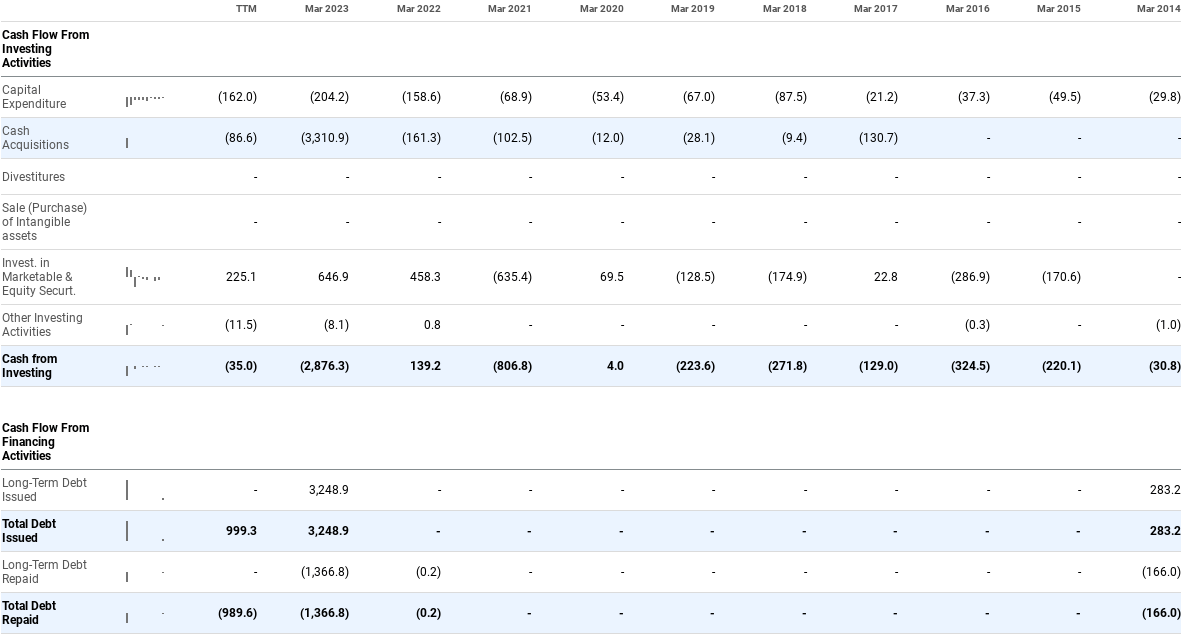

We can also see on the cash flow statement that a significant amount of debt was issued last year for a cash acquisition cost of $3,310.9 million. The company repaid $1,366.8 million of debt that year when it issued $3,248.9 million.

Seeking Alpha

For comparison in regards to financial health, EA (EA) has an equity-to-asset ratio of 0.55 and a debt-to-equity ratio of 0.26. Roblox (RBLX) has a much worse equity-to-asset ratio of 0.01 and a debt-to-equity ratio of 23.11. Sea (SE) has an equity-to-asset ratio of 0.36 and a debt-to-equity ratio of 0.71.

My analysis of the firm's financials, including its liabilities risk, indicates to me that the company shouldn't struggle to achieve relatively good long-term earnings and continued growth. However, it also isn't in an exceptional position either, and all things considered, I think the stock is a good rather than a great investment. Yet, in my opinion, the market has highly priced it at what I consider could become an overvaluation around the time GTA VI is released.

TTWO has a forward P/E non-GAAP ratio of 65.87 at the time of this writing, which is a 329.98% difference from the sector median of 15.32. Its forward price-to-cash-flow ratio is also 55.65, which is a 543.07% difference from the sector median of 8.65.

TTWO also needs to be put into perspective with other firms of similar size to get a fuller idea of its relative valuation:

Based on these figures, TTWO looks to be selling at an undeniable premium compared to the wider video game industry. Also, consider a much more favorable valuation from another compelling gaming company called Nintendo (OTCPK:NTDOY), with a forward P/E GAAP ratio of just 6.

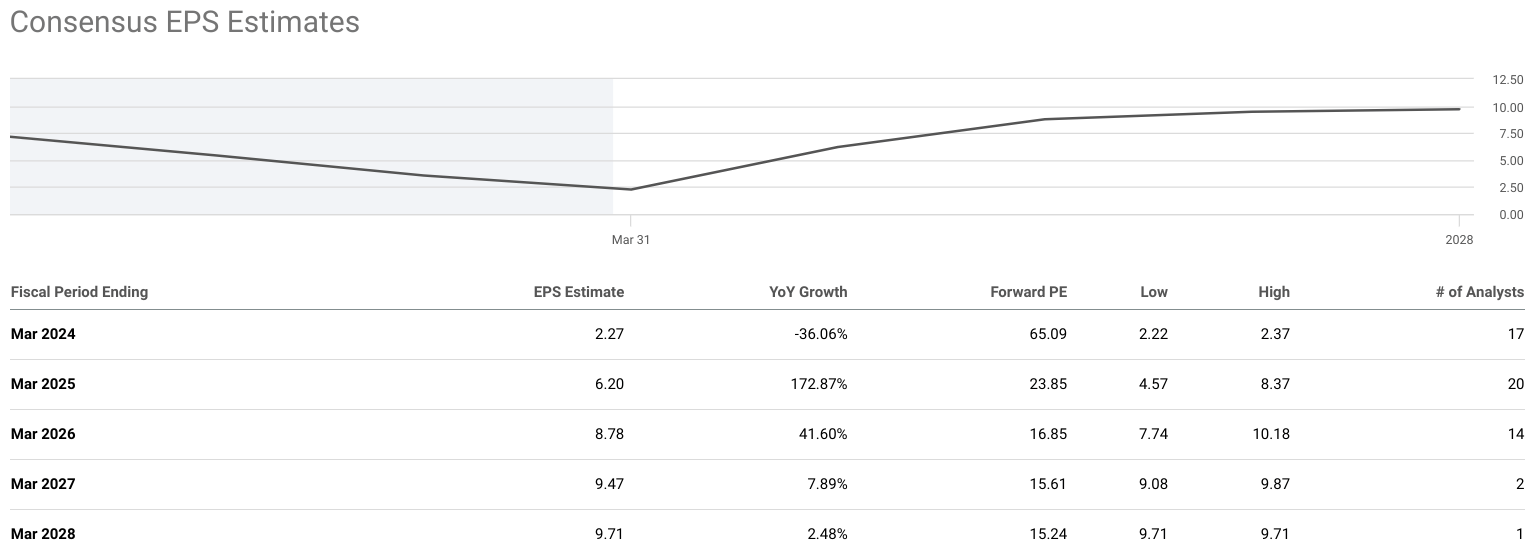

Considering future earnings estimates on consensus by analysts aggregated by Seeking Alpha, TTWO is likely to go through high earnings growth as a result of the GTA VI release in 2025, with considerable growth in 2026, too. However, following this, the firm is expected to have lower, more reasonable growth. I believe that the share price will see a significant overvaluation at the time of release but will experience downside volatility following this. As an investor focusing on 10+ year investment periods, I do not think this is the best allocation for my portfolio due to the lack of consistency in high growth amongst other Take-Two titles that can be attributed to GTA.

Seeking Alpha

To summarise, because of the upcoming GTA VI release, I believe the stock could be considered fairly valued at this time, with a significant risk of overvaluation to come based on short vs. long-term earnings prospects.

There is, of course, a risk that GTA VI is not as popular as anticipated. However, I see this as unlikely, considering initial data on its trailer viewership. The first trailer for GTA VI was the most viewed video game reveal on YouTube in 24 hours, accumulating 90,421,491 views. It also became the most viewed YouTube video in 24 hours (non-music), surpassing Mr. Beast.

More real is the risk that the company won't cut the right games or divisions from its portfolio to focus more intently on popular titles like those often developed by Rockstar, the NBA 2K Series, and Borderlands. Therefore, I consider a moderate risk in how management develops its portfolio strategy, and I believe it would benefit from a leaner set of games focusing on popularity and profitability. The downside of not doing this could result in an average stock to own long-term rather than a great one.

My thesis concludes that TTWO is a good stock to own at the moment, and it should see high levels of price return in the next two years from the GTA VI release. However, I think investors would be wise to consider the long-term prospects of the stock and how the market will react to a potential overvaluation around GTA VI that could then correct following slower earnings growth from a less compelling total games portfolio. As a long-term investor focusing on 10+ year holding periods, my analyst rating for TTWO stock is a Hold.