Vertigo3d

Vertigo3d

Trade Desk (NASDAQ:TTD) is an ad-tech platform that has outperformed the S&P 500 and Nasdaq 100 YTD. With the stock up 18% YTD, I believe that there is further upside ahead. The company reported its Q4 FY23 earnings report, where revenue and Adjusted EBITDA grew by 23% and 15%, respectively.

Looking forward, I believe that the company sits at the intersection of key secular growth drivers in segments such as Connected TV (CTV), audio, and retail media, where it enables its clients to build targeted campaigns on its platform to drive superior returns on ad spend. The company has also invested in developing Unified ID 2.0 (UID2) that addresses the need for precision targeting and measuring, while complying with privacy norms. It continues to see growing adoption of UID2, where brands are seeing marked improvements in campaign performance compared to their traditional methods. At the same time, the company continues to build capabilities in its AI-enabled Kokai platform to better support their customers through the ad buying process. With Adjusted EBITDA margins consistently above the 40’s range over the last 3 years, I believe that the stock is currently undervalued, with a potential upside of 20% from its current levels. As a result, I will rate the stock a “buy”.

Trade Desk is a cloud-based ad-buying platform that helps ad buyers such as brands and advertising agencies create, execute, measure, and optimize targeted ad campaigns across ad formats and channels that include Connected TV (CTV), display, and audio, among others.

The digital advertising market is a growing part of the total advertising market, and demand for CTV is rapidly evolving as a secular extension of the digital ad market. Trade Desk’s platform is uniquely positioned to help advertisers run targeted advertising campaigns and optimize campaign performance using synchronized data streams across devices to provide a holistic view of their target audience, thus enabling them to maximize return on advertising spend.

The company obtains its digital advertising inventory from 140 integrated ad exchanges, publishers, and supply-side platforms. It primarily generates revenue by charging its clients a platform fee based on the percentage of gross spend on the platform.

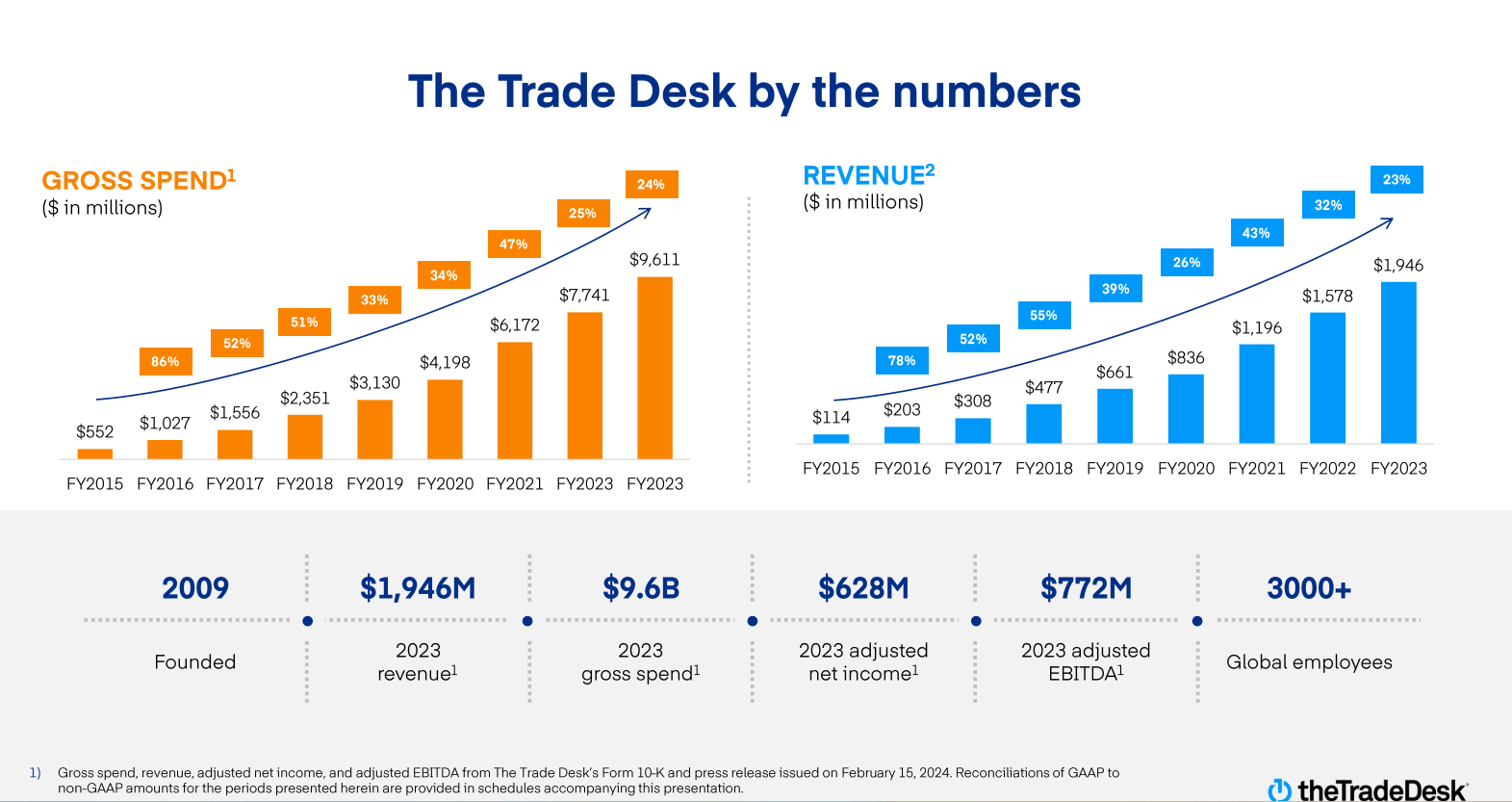

The company reported its Q4 FY23 earnings, with spend on the platform growing 24% YoY to $10B. So far, the company has championed through a complex macroeconomic environment as well as a rough period in the digital ad market caused by cookie deprecation, increased regulatory focus, macroeconomic volatility, and the rapidly changing TV landscape. Revenue in Q4 increased 23% YoY to $606M. For the full year FY23, revenue grew 26% YoY to $1.95B.

Q4 FY23 Earnings Slides: Trade Desk's growing spend and revenue growth

There are a number of factors that are playing in favor of Trade Desk’s growth trajectory.

Secular trend of the shift towards CTV: The management believes that CTV has a huge opportunity, as there is a higher imperative for brands to prove return on ad spend, while CTV content owners increasingly realize how ad-viewing free subscriptions are more valuable than higher-priced ad-free subscriptions. Over the last 2 years, 25% of US streaming subscribers have canceled at least 3 subscriptions, according to Jeff Green, CEO of Trade Desk. With a growing pressure on CTV content owners to expand relevant ad programs, I believe Trade Desk is well positioned to enable brands and advertising agencies to build targeted campaigns with a broad reach of 90M+ households across 120M+ CTV devices. During the earnings call, Laura Schenkein, CFO of Trade Desk, said that CTV is the fastest-growing channel globally and, as of Q4, represents a mid-40’s percentage share of total revenue.

2024 will be a big year for Audio: The management believes that Trade Desk could be in the early innings of programmatic advertising growth in audio, similar to how it had positioned with CTV years ago, as digital audio benefits from a logged-in authenticated user base that is deeply engaged.

The evolving landscape of identity amidst third-party cookie deprecation: Considering that the fastest growing channels that include CTV and digital audio don’t rely on cookies, Trade Desk’s management believes that it stands to benefit from Google’s (NASDAQ:GOOG) recent decision to accelerate the deprecation of third-party cookies. In an environment where advertisers need to reach their audiences with precision and relevance, I am impressed by the company’s innovation pipeline, where it developed UID2, an open-source identify framework that operates by transforming email addresses or phone numbers into an encrypted advertising identifier, which is then shared with advertisers and publishers to enable targeted campaigns without relying on third-party cookies.

During the earnings call, Jeff Green detailed one of the success stories with Unilever (NYSE:UL), where they leveraged UID2 to target relevant audiences as opposed to their traditional targeting methods. This saw a marked improvement across key areas of measurement that include click-through rates, brand awareness, and cost per completed view.

At the same time, the company continues to advance its AI-enabled Kokai platform, which leverages predictive algorithmic tools to process vast data sets and make recommendations and optimizations of the ad purchase process, such as ad impression relevance scoring, budget optimization, measuring, and forecasting. With positive feedback across 1000 clients internationally, I believe that the company’s investments to integrate AI into its platform will further advance advertiser performance, leading to deeper adoption and spend on the platform.

Meanwhile, Trade Desk continues to capture market share in Retail Media, where it enables advertisers to combine first-party data with retail data to better attribute marketing campaign activities and how they impact consumer behavior at different stages in the purchase funnel, so that they can be more precise with their campaign activities. Plus, the company is now seeing international growth outpacing US revenue growth for four quarters in a row, although US revenue still contributes 88% of total revenue. With growing adoption of CTV outside of the US, I believe we can expect tailwinds from international expansion to boost the company’s top line over the coming years.

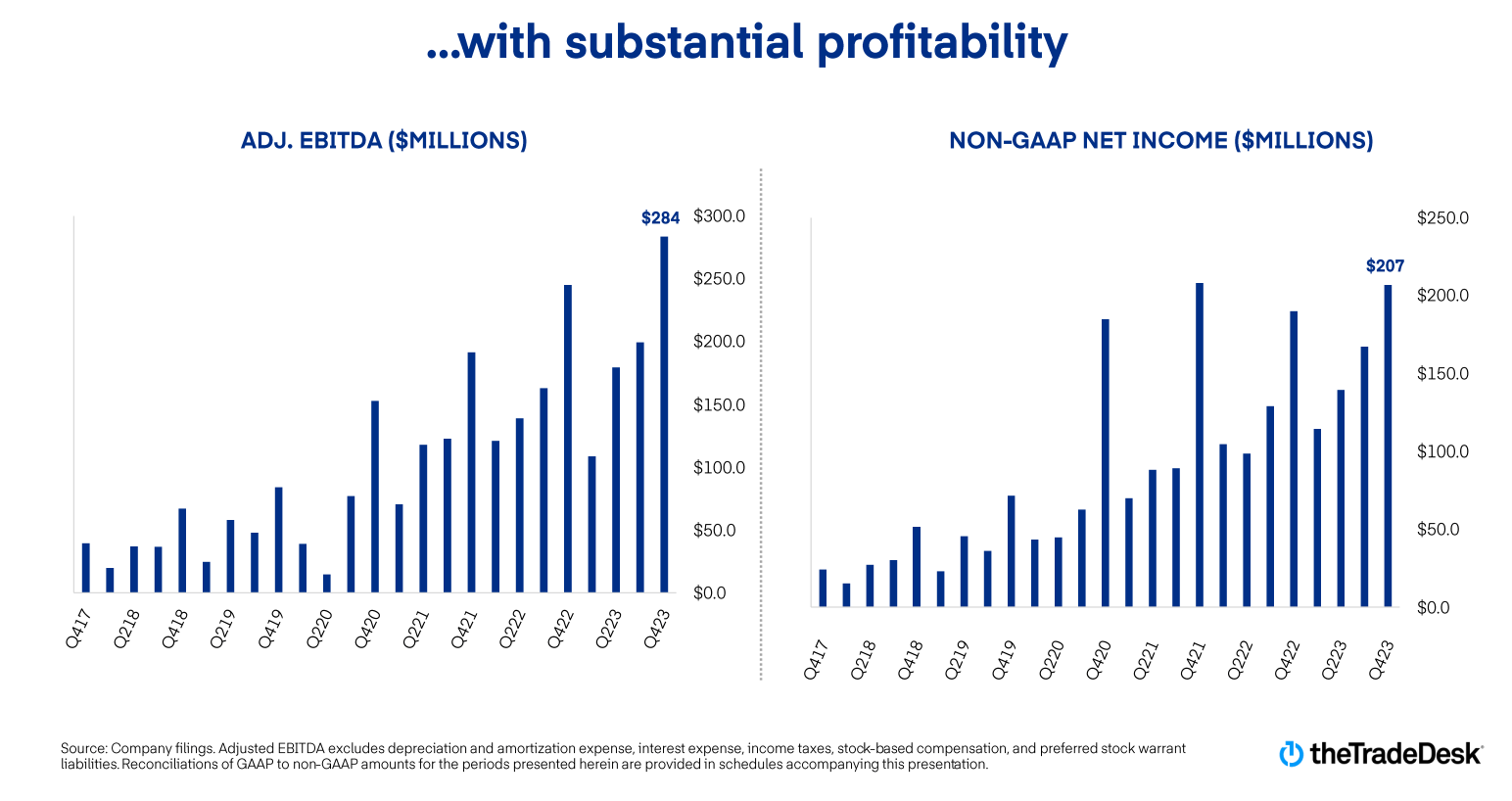

Shifting gears to profitability, the company generated $284M in Adjusted EBITDA in Q4, up 16% YoY, representing a margin of 47%. For the full year FY23, the company generated $772M in Adjusted EBITDA. Over the last 3 years, the company has consistently maintained its Adjusted EBITDA margins above the 40’s range, which I believe indicates growing operating leverage, which is ultimately allowing the company to make strategic investments to continue to grow and capture market share in the digital advertising space.

Q4 FY23 Earnings Slides: Trade Desk's growing profitability

Looking forward to Q1 FY24, the company expects revenue to grow 25% YoY to $478M. In my view, this demonstrates the strength of the underlying secular drivers that the company has positioned itself to spearhead growth in, while continuing to invest in its product roadmap to enable advertisers to stay ahead of the curve, especially when it comes to regulation. At the same time, the company is expecting an adjusted EBITDA of $130M, up 19% YoY, with a margin of 27%, a drop sequentially from the prior quarter.

The ad-buying industry is ripe with cutthroat competition. This is also a rapidly evolving space with the potential to reach new markets and devices very quickly. The scale of competition and pace of target market evolution require Trade Desk to maintain a rigorous framework of innovation. In the scope of target market evolution, CTV is one market extension that Trade Desk is currently benefiting from, as I have pointed out earlier, since it has innovated and moved quickly in this space. If the company fails to maintain its pace of innovation, it can quickly lose market share, especially when competitors have already announced intentions to contest for market share in this space. AppLovin Corp. (NASDAQ:APP) announced that they were already in the early stages of testing and rolling out their CTV offering.

On a broader level, 2024 will mark the year when third-party cookies are finally deprecated. Since Trade Desk is in the space of digital advertising and a previous phase of its business model relied on cookies, there is still some uncertainty around the cookie deprecation this year and its full impact on the ad business. But it has already moved early on to address the issue by launching UID2 during the pandemic, which has eased a lot of the uncertainty around the impact of cookie deprecation on its business. In fact, Trade Desk’s CEO recently authored an opinion to illustrate how the company’s UID2 framework continues to support its ad business. I believe that Trade Desk is well positioned to ride through 2024 despite the changing advertising landscape and competition.

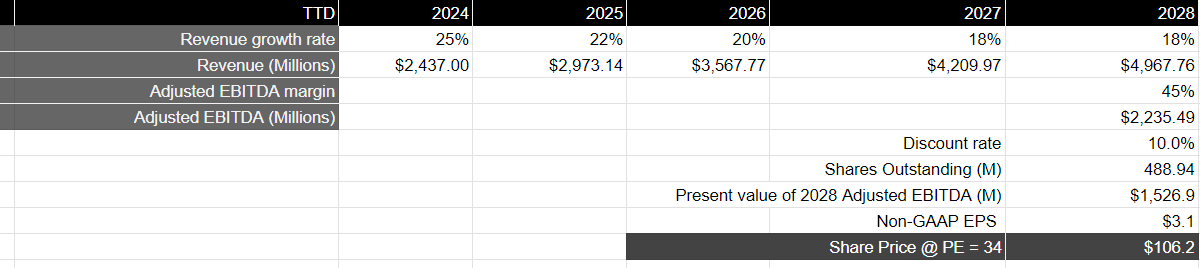

Assuming that Trade Desk grows 25% in FY24, slightly higher than mid-point consensus estimates, followed by growth in the low 20’s range until FY26, then growing in the high teens thereafter until FY28, the company should be able to generate close to $5B in revenue by FY28. I believe this is achievable as the company continues to drive penetration in the growing digital advertising space, in segments such as CTV, audio, and retail, while continuing to innovate its platform by building AI capabilities to drive superior outcomes for their clients. Meanwhile, assuming that the company is able to maintain its Adjusted EBITDA margin of around 45% through FY28, it should generate approximately $2.2B in Adjusted EBITDA, which translates to a present value of $1.5B in FY28 when discounted at 10%.

Taking the S&P 500 as a proxy, where its companies have grown their earnings on average by 8% over a 10-year period with a price-to-earnings ratio of 15–18, I believe that Trade Desk should trade at least twice the S&P 500 multiple at around 34. This would translate to a price target of $106, which represents an upside of 20% from its current levels.

Author's Valuation Model

Trade Desk is sitting at the intersection of key secular trends and a great product. As the company continues to spearhead revenue growth, I believe it will be able to keep up the momentum as it continues to unlock opportunities in CTV, audio, and retail while also expanding internationally. I also like the company’s commitment to profitability, which I believe is enabling it to drive key investments in Kokai and UID2, thus strengthening its competitive position. Taking into account both the “good” and the "bad," I believe the stock is a “buy” with an upside of at least 20% from its current levels.