shaunl

shaunl

Over the past year I've been rebalancing my dividend portfolio looking for additional stocks to potentially add. Besides BDCs and REITs which I own, I also look for reputable, well-known companies that consumers often use but don't necessarily think about when it comes to them paying dividends.

One company that comes to mind is Deere & Company (NYSE:DE), a business that has been around for quite some time and also pays a nice dividend. They have a long history of paying dividends but have faced some headwinds recently. Despite these, their cash flows remain strong. In this article we'll discuss these headwinds which, in my opinion, have also caused the stock to trade at a more attractive level currently.

For those unfamiliar with Deere & Company, or more commonly known as, John Deere, they are best known for their equipment used in construction, forestry, and agriculture. These include everything from tractors, gator utility vehicles, dump trucks, and large dozers.

This is similar to Caterpillar (CAT), which I covered back in November in an article you can read here. The two companies share some similarities although they do differ as CAT focuses on construction & heavy transport equipment, and Deere & Company focuses on farm & agricultural machinery. DE has been around for nearly two centuries developing innovative solutions to help customers become more productive.

In short, they provide machines and applications that help revolutionize the construction & agriculture industries. They operate in four segments and have more than 100 locations globally. Additionally, they have operations in Europe and Latin America with a portfolio consisting of 25 brands.

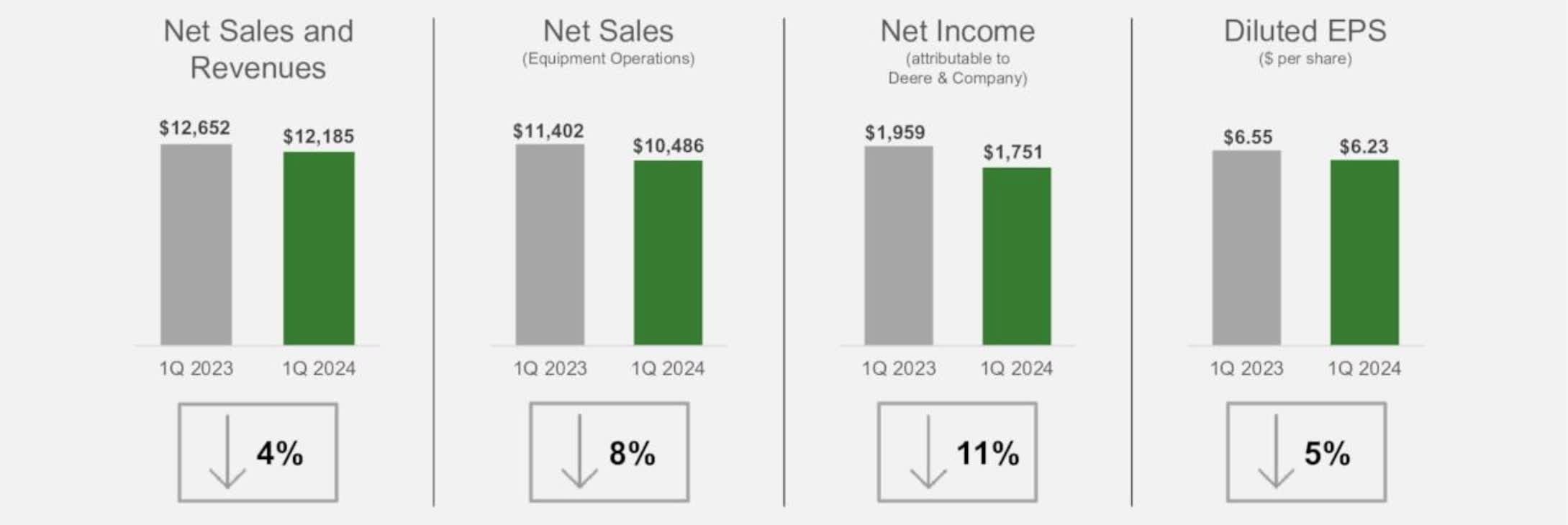

The current macro environment has proven to be tough for several high-quality companies and Deere & Company is no exception. During their Q1 earnings the company beat on both the top & bottom lines with EPS of $6.23 and revenue of $12.19 billion.

Despite the beat, net sales were down essentially across all segments. While revenue was up year-over-year from Q1 2023, EPS did decline by nearly 5% from $6.55 to $6.23. Net sales & revenues declined 9% overall.

DE investor presentation

As far as the four segments, net sales declined in all but construction & forestry where these were flat at $3.42 billion. Small agriculture sales were hit the hardest, down double-digits at 19% to $2.425 billion. Production & Precision sales and Equipment Operations sales were down 7% and 8% respectively.

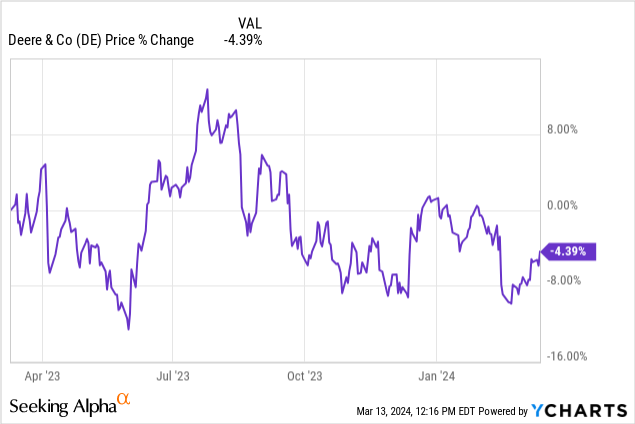

This is likely the cause of the stock being down over 4% over the past year. All sales were impacted by lower shipment volumes affecting their operating profits. And management expects 2024 sales to be down roughly 15%.

In Europe & Latin America specifically, industry sales are projected to be down in both. Higher interest rates have affected the company since their rapid rise causing higher SA&G and R&D expenses as well. The war in Ukraine and adverse weather has also affected financials for the company.

Despite the headwinds, the company's cash flows have remained robust, making the dividend safe. Net income and cash from operations are projected to be $7.5 billion - $7.75 billion and $7 billion - $7.5 billion respectively. CAPEX is expected to be roughly higher than last year's $1.5 billion at $1.9 billion. This is significantly lower than the $11.9 billion in operating cash flow the company brought in 2023.

The company also has been aggressively repurchasing shares, buying back $7.2 billion worth in 2023. And with their cash flows remaining strong, I expect this to continue going forward. In the past decade the company has decreased its share count roughly 20% from 375 million to 281 million shares outstanding at the end of Q1. This decreased from 299 million year-over-year, so the company has allocated its capital prudently, returning capital to shareholders in the form of dividend increases & buybacks.

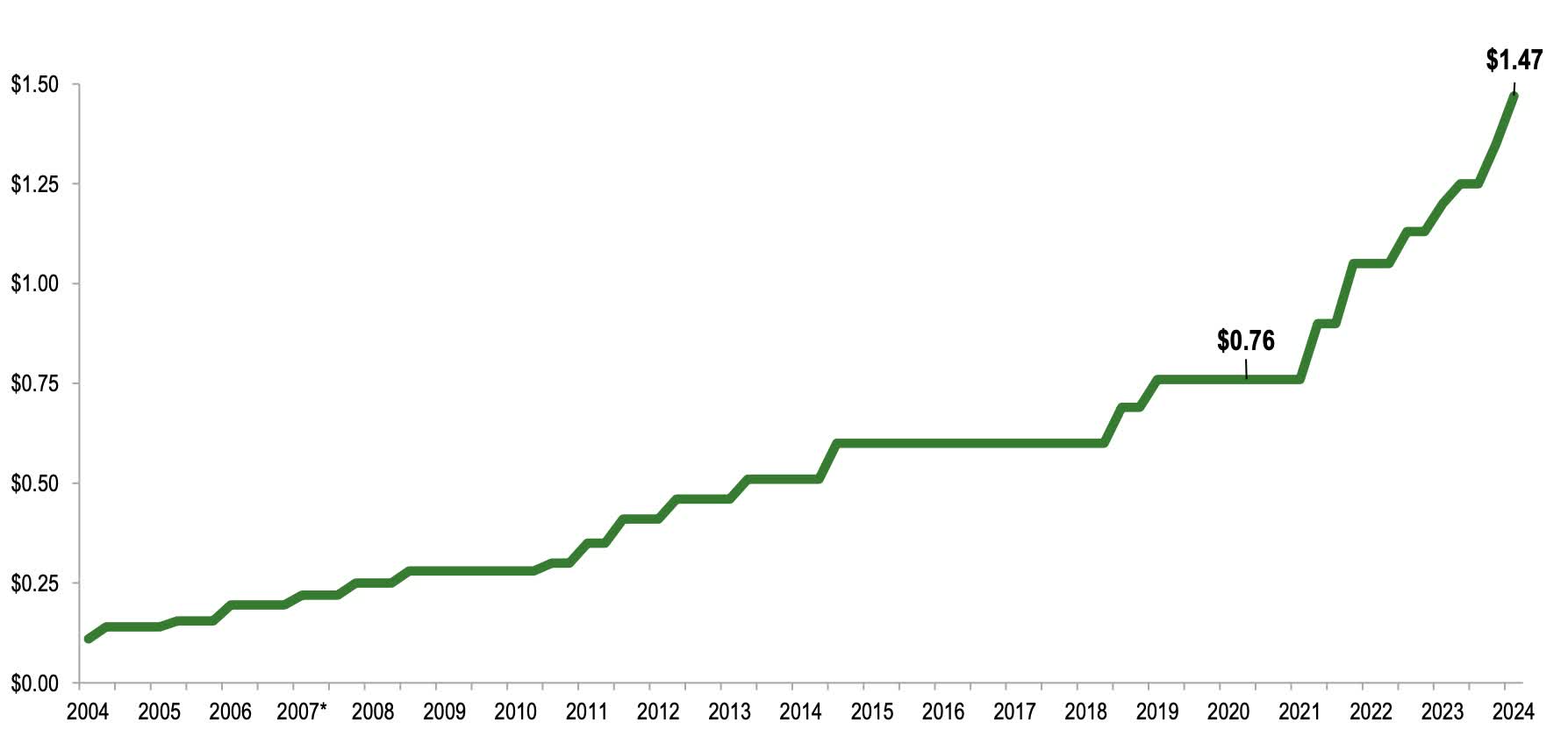

Using the current share count, DE needs roughly $440 million to cover the quarterly payout of $1.47. Using the company's projected cash flow, DE has ample room for further dividend increases for the foreseeable future and continue to maintain a very safe payout ratio of 25% - 35%.

This ensures DE can continue its long history of paying dividends with more than 30 years without a reduction. Since COVID when the company paused the dividend, they have grown it by more than 93% from $0.76 to current.

DE investor presentation

This is in comparison to peers AGCO Corporation (AGCO) and The Toro Company (TTC) who've grown their dividends more than 81% and roughly 44% respectively over the same period. And as seen by DE's strong cash flows, I see them continuing to reward shareholders with strong dividend growth.

Deere & Company sports an A-rated balance sheet which the company is committed to through its strong financials and capital allocation. However, the company's debt has increased significantly in the past few years as they've acquired 3 companies since 2022. Two of these came last year when DE acquired SparkAI and Smart Apply, Inc to accelerate the integration of smart technology into the company's products.

At the end of 2023 DE had a healthy cash balance of $5.1 billion, which increased year-over-year from roughly $4 billion in January 2022. Additionally, they do have quite of bit of debt due in 2024 with more than $17 billion, which also may be a reason investors may be skeptical, in turn causing the share price to decline. With high interest rates and uncertainty surrounding when they will be cut, companies with a lot of upcoming debt will face refinancing headwinds as they may have to refinance at much higher rates. This will also place downward pressures on cash flows going forward.

Currently, Deere & Company is trading closer to its 52-week low at less than $379 at the time of writing. Because of the headwinds discussed previously and the disappointing outlook, now may be a great buying opportunity for long-term dividend investors.

Furthermore, the company has a price target of $415, offering investors some nice upside. Their forward P/E of 13.61x is well-below their 5-year average and sector median further signaling the stock may be undervalued and a buy.

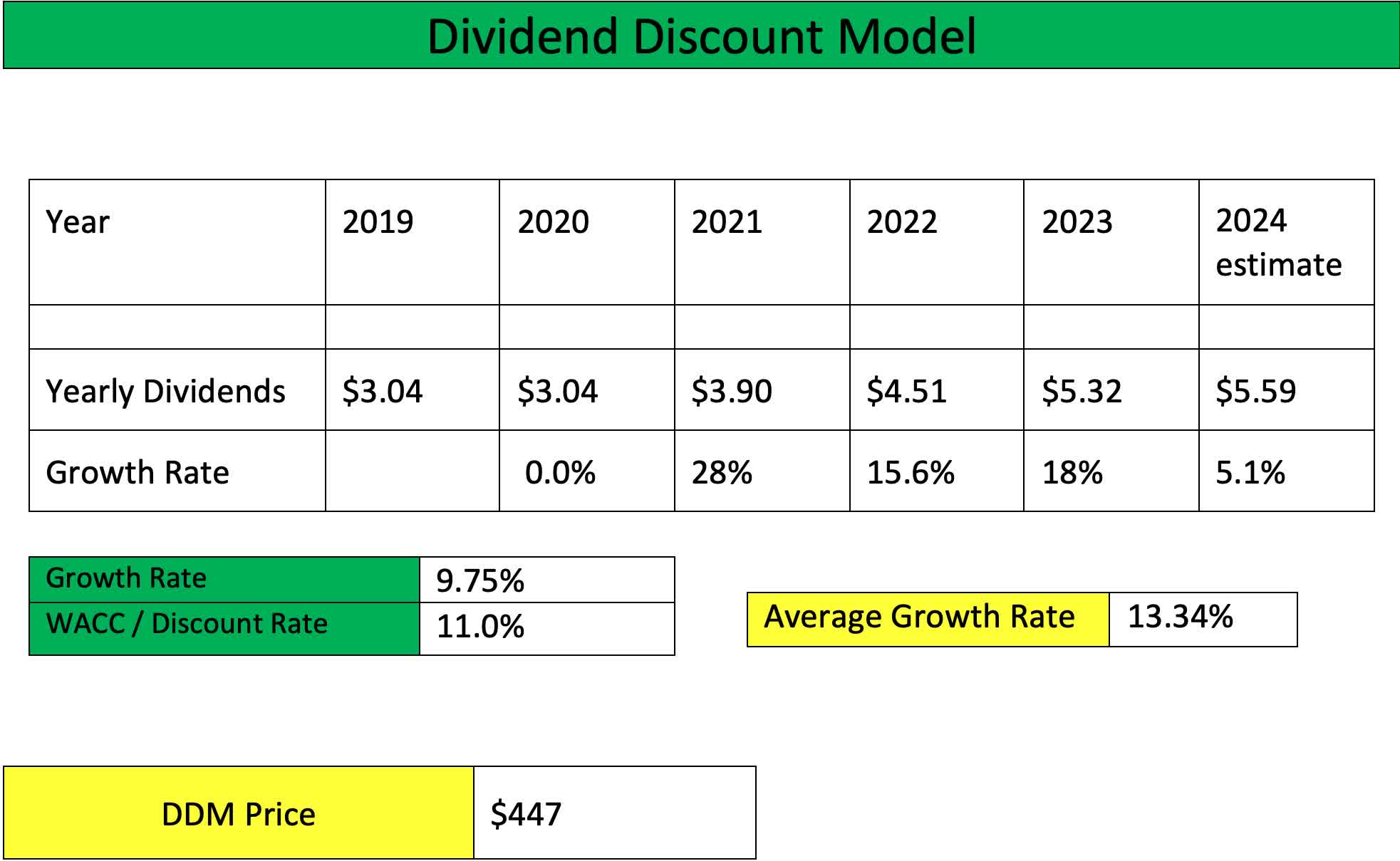

Using the dividend discount model, I have a price target higher than Wall Street's $418. DE has an 5-year average dividend growth rate of 13.34% and I use an expected growth rate of 9.75% to be conservative and manage expectations going forward. Still the stock offers massive upside from the current price.

Author DDM

Seeing as how the company has outperformed the S&P over the longer-term and is a high growth stock, I use a WACC of 11%, slightly above the 7% - 10% historical average for the index. In the short-term the company may continue to face headwinds but if rates are cut as expected, DE will likely outperform in the coming years.

As seen by the headwinds the company has faced over the past year with net sales down across all segments, this will likely continue to be a headwind and risk going forward. Furthermore, with the hotter-than-expected CPI report recently, rates could potentially rise further although I think it's unlikely but a small chance indeed.

If so, this will continue to place downward pressure on operating profit margins for the company, affecting their financials going forward. Higher rates & inflation will also continue to affect the price of goods & services and until this moderates, DE's share price will likely face volatility until the economy gets more clarity regarding interest rates and inflation.

Deere & Company is a high-quality company trading closer to its 52-week low, which presents long-term investors with a great opportunity to pick up a stock trading at an attractive price. And despite headwinds in 2023 and disappointing guidance from management, Deere & Company's cash flows and dividend safety remain strong.

With a conservative payout ratio and robust cash flows, this ensures the company has ample room to continue raising the dividend and returning cash to shareholders via buybacks. In lieu of what I view as short-term volatility, because of their upside potential and strong business model, I rate DE a buy.