JulPo

JulPo

Since I published my initiation report in June 2023, Trane Technologies' (NYSE:TT) stock price has surged by more than 56%. I pointed out their strong growth driven by decarbonization and electrification, as well as robust pricing power. They delivered 8.7% organic revenue growth and 21.4% adjusted operating profit growth in FY23. I admire their structural growth and reiterate the 'Strong Buy' rating with a one-year price target of $339 per share.

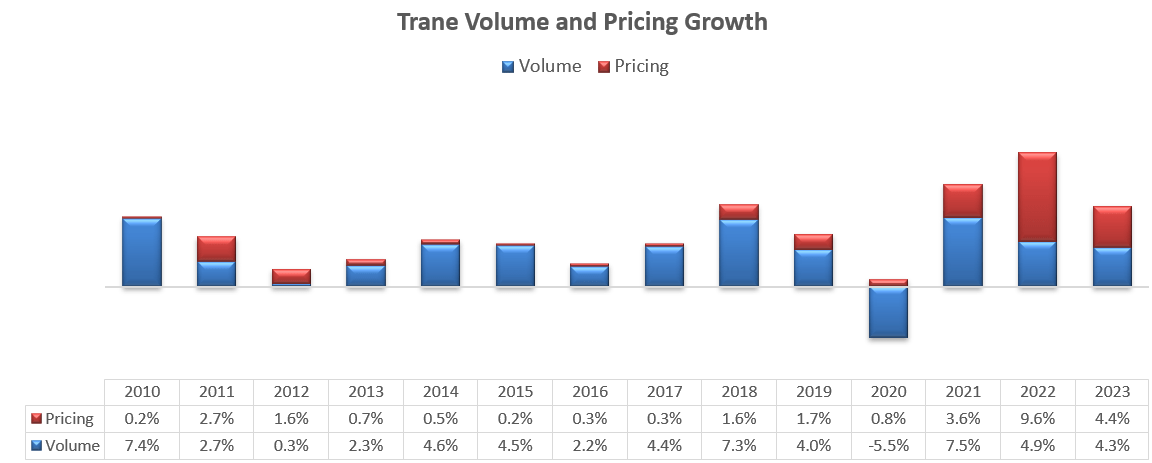

Trane delivered 8.7% organic revenue growth in FY23, comprising 4.4% pricing growth and 4.3% volume growth. As depicted in the chart below, Trane has been delivering strong organic growth over the past two years.

Trane Technologies 10Ks

The strong commercial HVAC growth has been a primary growth driver for the company in my view, and I expect the growth momentum to persist in the future for the following reasons.

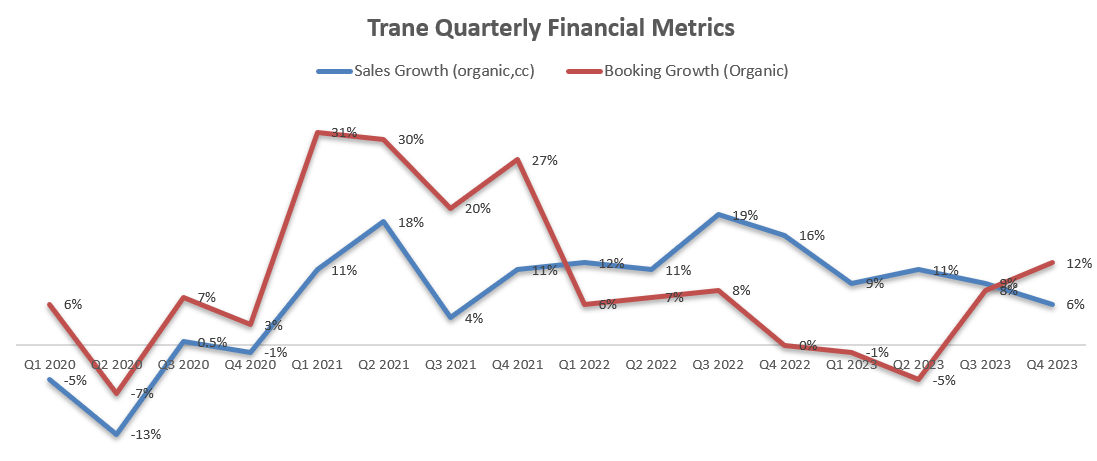

As disclosed in their Q4 FY23 earnings call, their backlog in commercial HVAC was up $700 million in FY23, and their backlog has nearly tripled over the past three years. The company is witnessing a strong pipeline of applied HVAC projects. Historically, Trane could convert the backlog into the actual revenue in 6-12 months. The chart below examines the relationship between organic booking growth and organic revenue growth, and there is quite clear that booking growth is a leading indicator for their revenue growth. As such, the strong backlog could potentially convert into real revenue growth over the next few quarters in my view.

Trane Technologies quarterly results

In addition, according to IEA report, energy efficiency delivers the second largest contribution to bringing down CO2 emissions over the next decade, and many energy efficiency measures in industry, buildings, appliances and transport are ready to be put into effect now. High-efficiency HVAC systems have the potential to reduce the energy consumption in buildings/factories.

In March 2024, The Securities and Exchange Commission (SEC) adopted rules to enhance and standardize climate-related disclosure for listed companies. I think the requirement of climate-related disclosure could compel listed companies to pay more attention to their energy consumptions, water usage, and other related KPIs. According to Schneider Electric, buildings account for 37% of the world's annual CO2 emissions. Therefore, in my view, enterprises have incentives to upgrade their low-efficiency HVAC systems to newer applied systems, which can reduce energy bills and improve ESG. As such, the strong growth in commercial HVAC is more likely to sustain in the near future.

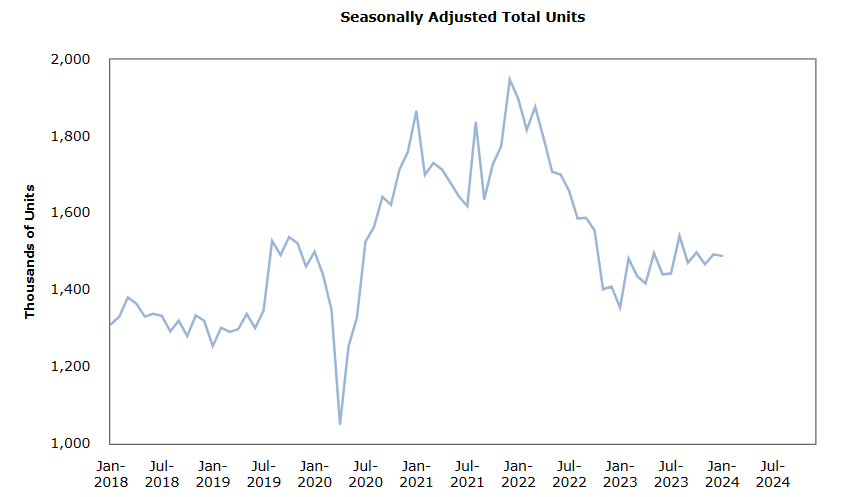

As highlighted in my initiation report, Trane's residential business is impacted by the current high-interest rate and subdued residential housing market. In Q4 FY23, Trane's residential business experienced negative YoY growth ((amount not disclosed)), while they are witnessing the market continuing to normalize. Their management expressed confidence that the market would return to a GDP plus type of growth for the long-term.

The current high-interest rate has indeed placed tremendous pressure on housing starts. The chart below illustrates the seasonally adjusted total units of new residential constructions in the U.S. market. The residential market has been quite weak since late-2022 caused by the rising interest rates.

U.S. Census Bureau

However, when the Fed starts to cut the rate, the housing market should be able to recover, in my opinion. Having said that, residential market only represents 20% of Trane's total revenue, as such, the financial impact is quite limited.

The management anticipates transport refrigeration market moving into a moderate down cycle in the near future. Interestingly, the transport refrigeration business was up 20% in the first half of FY23, then went down 20% in the back half of the year. Their management expects the business to decline in FY24 as the market enters the down cycle.

2/3 of Trane's transport refrigeration revenues come from trailers, trucks and auxiliary power unit (APU), and 1/3 come from marine/bus/rail/air and aftermarket. Kuehne + Nagel (OTCPK:KHNGF), one of the largest road logistic companies in the world, experienced -15% revenue growth in their road logistics business in Q4 FY23, and -11% for the full year. For the full year, the volume declined by 6% and pricing dropped by another 5%. These figures indicate that the overall logistic market faced significant challenges in Q4. Given the decline in both volume and pricing, it seems unlikely that logistic companies will expand their capital expenditures on trucks, in my view. Therefore, Trane's transport refrigeration could encounter growth challenges in FY24. In addition, Trane calculated that the transportation market in the North America will decline by 12% on a weighted-average basis, based on ACT's forecast data. Having said that, the business represents around 15% of group revenue; again, the overall impact should be quite limited in my view.

Trane delivered 6% organic revenue growth and 12% organic booking growth in Q4 FY23. Due to the strong margin expansion, their adjusted operating profits grew by 23% YoY, and EPS was up 19% YoY.

There are several reasons for their notable margin expansion.

As mentioned in my initiation report, Trane exhibits super strong pricing power over their customers. In Q4 FY23, Trane's American segment delivered 4% volume growth and 3% pricing growth. The strong pricing growth is expanding the company's gross margin. Furthermore, Trane has been expanding their service business over the past few years, especially for the applied HVAC products. The service business carries much higher margin than the group level, as disclosed over the earnings call. As such, the growth of their service business would expand their operating margin over time.

The last factor is their volume growth, which would generate tremendous operating leverage for the company. A sustainable volume growth would benefit the company's utilization rate, contributing to margin expansion as well.

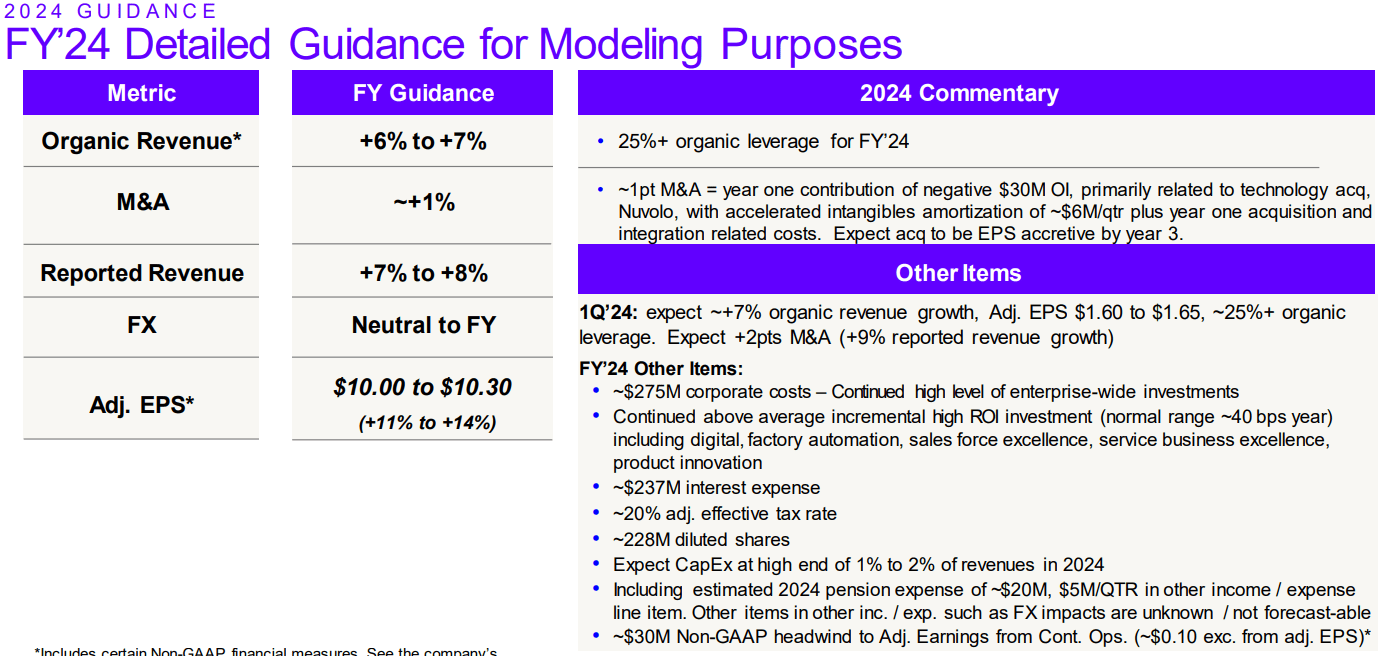

For FY24, the company is guiding 6%-7% organic revenue growth, 1% M&A growth, and 11%-14% adjusted EPS growth, as depicted in the slide below.

Trane Technologies Investor Presentation

Grand View Research forecasts that the global HVAC market will grow at a CAGR of 7.4% from 2024 to 2030, driven by rising need for cost-effective and energy-efficient cooling and heating applications in the industrial and commercial sectors. Just considering the market growth, Trane's revenue guidance appears to be quite conservative, in my view.

Over the earnings call, Trane has made it clear that pricing would continue to be their growth driver in the near future. Assuming 3.5% pricing growth, Trane only needs to grow their volume by approximately 4% to achieve their full-year guidance. Over the past three years, Trane delivered an average volume growth of 5.6%; therefore, their full-year guidance appears to be quite conservative, in my opinion.

In the DCF model, I assume 8% organic revenue growth, comprising 5% volume growth and 3% pricing growth. The growth assumption is slightly higher than the long-term forecast provided by Grand View Research mentioned previously, as Trane's strong commercial HVAC portfolio could potentially outperform the overall market growth. In addition, the volume and pricing growth assumptions are aligned with their historical average over the past three years. M&A is expected to contribute 1% to the topline growth in the model, aligning with their M&A track record.

Their margin expansion is driven by pricing initiatives as well as operating leverage. I estimate their operating expenses will grow by 8.5% YoY, leading to 40-60bps margin expansion annually.

In FY23, Trane generated $2.089 billion of FCF, returning $684 million in dividends and $669 million in shares repurchase, a quite generous capital allocation strategy in my view. Due to their shares repurchase, the number of common shares outstanding was reduced by 2% in FY23. The company has committed to the shares repurchase in FY24, and I estimate the total number of shares outstanding will be reduced by another 2% in FY24.

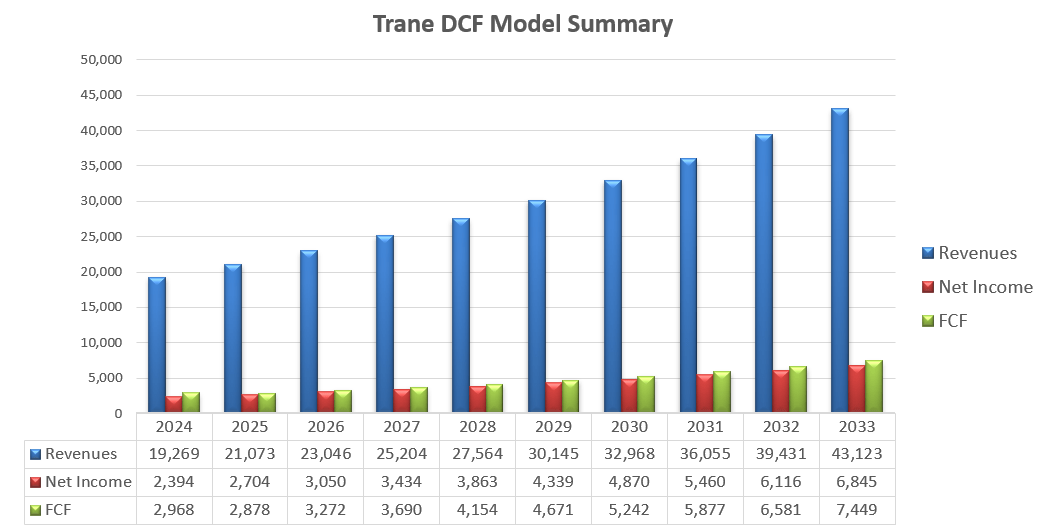

Trane Technologies DCF - Author's Calculation

With these parameters, I calculate the free cash flow from the equity (FCFE) for the next ten years by adjusting net income with depreciation/amortization, change in working capital and net borrowings, as illustrated in the table below.

Trane Technologies DCF - Author's Calculation

The 24-month beta is 1.19 according to (SA), risk-free rate is 4.32% using U.S. 10-year treasury yield, and market premium is 5% in the model. Thus, the cost of equity is estimated to be 10.265%. The total equity value is estimated to be $75.8 billion after discounting all the future FCFE. As such, their one-year target price to be $339 per share, as per my estimate.

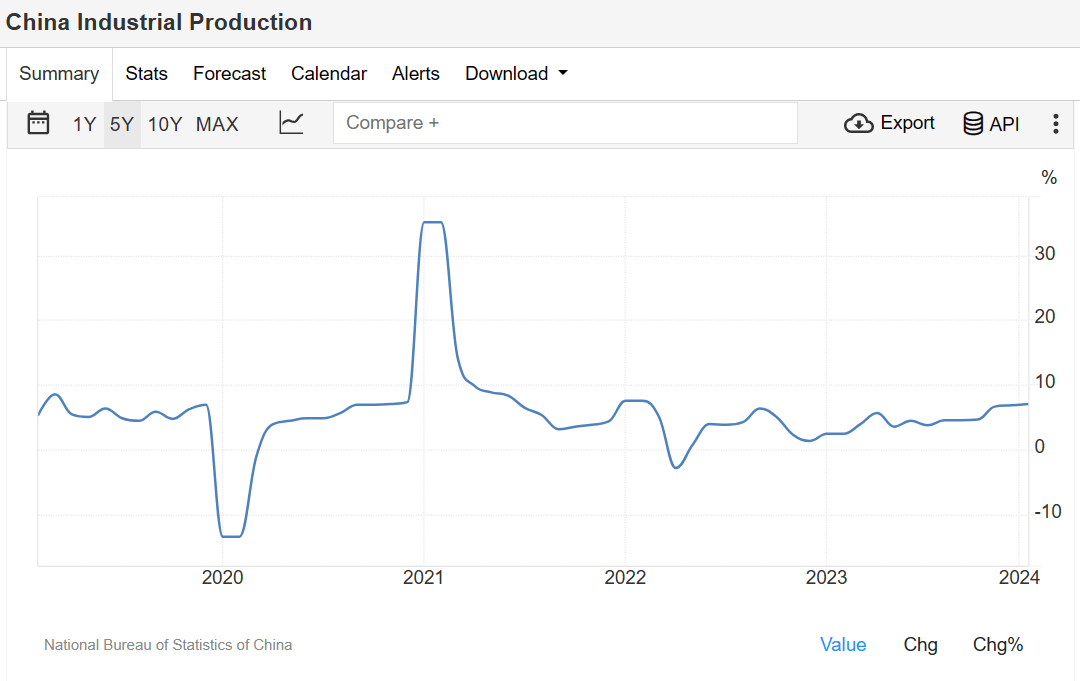

In FY23, their China bookings were down LSD due to the weak economy and subdued industrial productions in the local market. Their China revenue declined MSD year-over-year as a result. Asian Pacific represents around 8.2% of group revenue, and I estimate China accounts for LSD percentage of total revenue. I don't expect Chinese economy to recover in the near term, as their local economy is currently suffering from weak property market and poor stock equity market.

China Industrial Production has shown considerable weak the emergence of the pandemic in 2022, as depicted in the chart below. Trane is selling applied HVAC solutions in China for manufacturing facilities and buildings. Therefore, the slowdown in industrial activities would hamper Trane's growth prospects in China.

Trading Economics

Therefore, China should continue to be a headwind for Trane in FY24, in my view. While Trane expects their commercial HVAC growth to persist, there are some weak spots such as office end-market. The HVAC in office market was quite weak in FY23, and their management anticipates the softness continuing into FY24.

As pointed out in my previous article, I define a 'Boring' investment as steady business growth regardless of macro conditions. Trane Technologies is one of my long-term 'Boring' investments, as they consistently deliver superior organic revenue and free cash flow growth. Their growth is driven by the mega trend of energy efficiency and global decarbonization. I reiterate the 'Strong Buy' rating with a one-year price target of $339 per share.