jiefeng jiang

jiefeng jiang

Tower Semiconductor (NASDAQ:TSEM) recently reported its FY23 financial results, so I wanted to look back at how the company progressed over the last year and comment on the outlook going forward. It’s been a tough year for many companies in the semiconductor sector, including TSEM, however, many analysts are seeing improvements in demand across the board for many different sectors and the declines in revenues seem to have bottomed. The company is still trading at a decent discount; therefore, I am sticking with a buy rating, and I am hopeful for a decent recovery going forward.

As of Q4 ’23, the company had around $1.2B in cash and short-term investments, against $172m in long-term debt. So, the company is still very healthy liquidity-wise, and on par with many other semiconductor companies, as these tend to have great balance sheets, in terms of low outstanding debt and a lot of cash on hand.

The current ratio is somewhere around 6, so it is safe to say the company is at no risk of insolvency and has no liquidity problems, which should be very attractive to many investors. So, let’s check how the company’s other metrics developed over the last year.

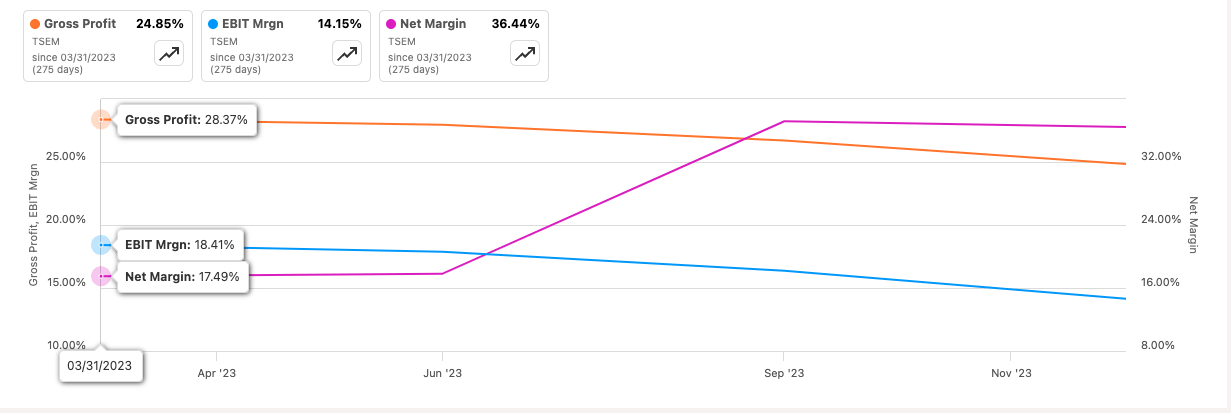

In terms of margins, we can see that over the last year, the company has lost quite a bit of efficiency and profitability, as margins decreased across the board, except for net margins, which saw a one-time boost due to the company receiving the merger contract termination fee from Intel (INTC), so net margins will come back down to below where they have been because we can see EBIT and gross margins have declined slightly. Q4 net margins came in at around 15%.

Margins (SA)

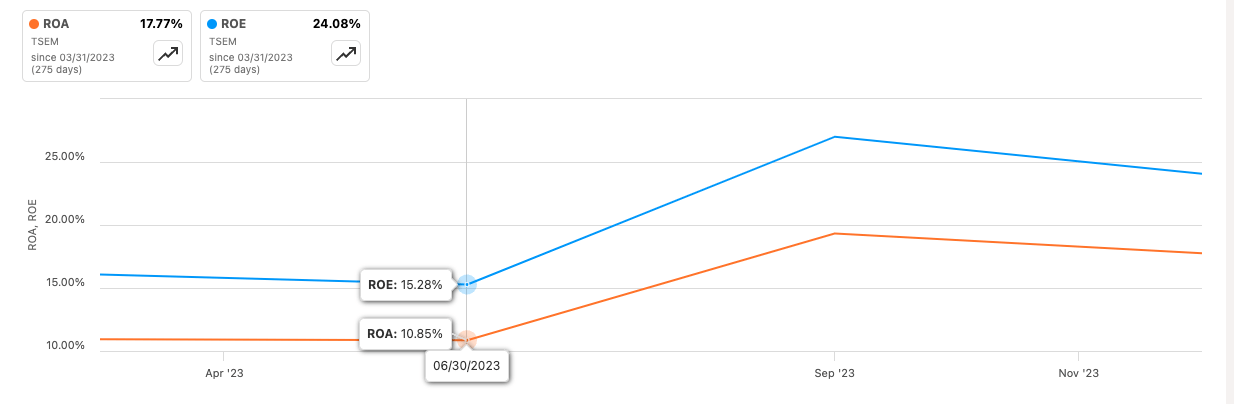

Continuing with efficiency and profitability, the company’s ROE and ROA have also come up due to the same termination fee, so I am anticipating these to come down quite a bit in the later quarters on a trailing twelve-month basis, as we can see already in the latest quarter. Even so, if these return to around Q2 numbers, they are still very decent returns and well higher than what I am looking for: ROA of 5% and ROE of 10%, so it is still good.

ROA and ROE (SA)

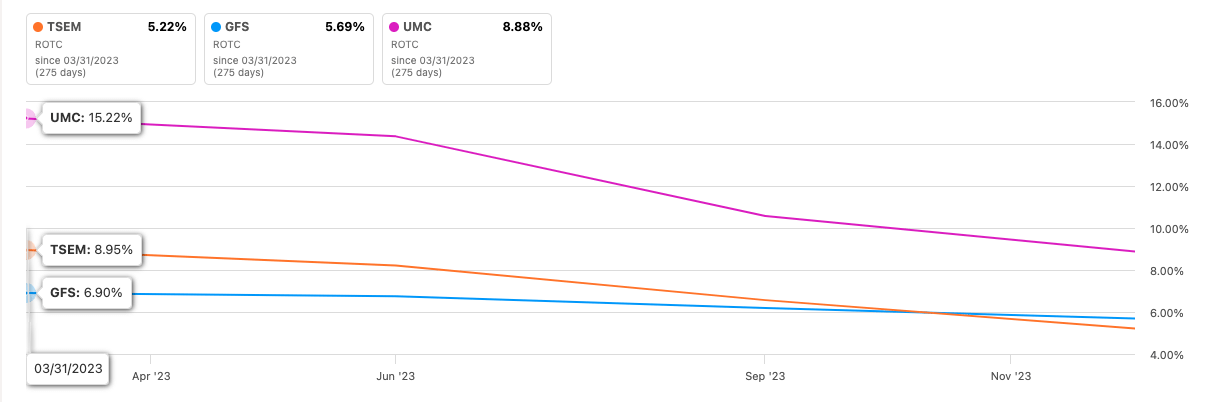

In terms of competitive edge, the company’s ROTC against some of the peers mentioned in their 20-F filing, we can see that over the last year, the company struggled to maintain its efficiency. ROTC has been on a downtrend. The positive here is that the two competitors in the image also saw their competitive edge come considerably down, and it makes sense. The semiconductor industry had a tough time for a while. The negative sentiment persisted and only looks to improve going forward, but we are still not too sure.

ROTC vs Peers (SA)

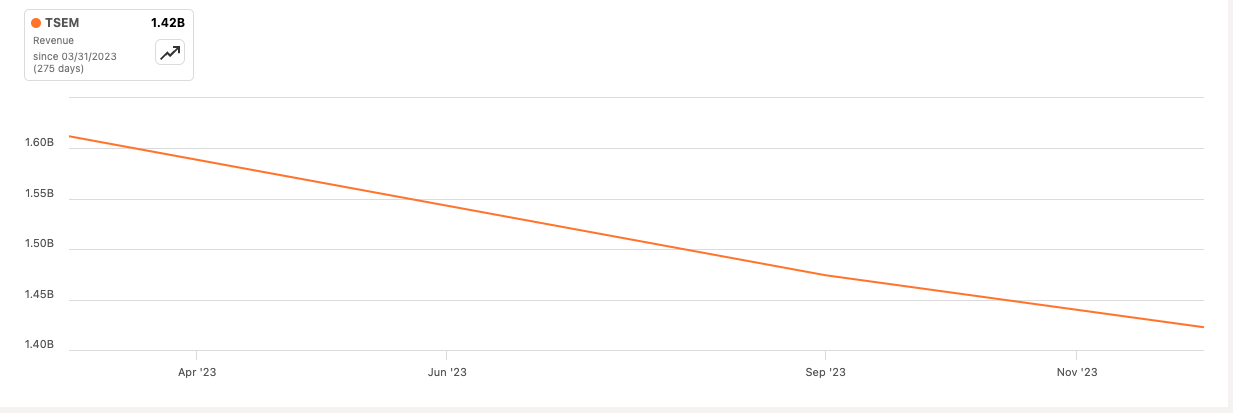

In terms of revenue, it is exhibiting the same downward trend as all other metrics (excluding the effects of the termination fee). Q/q revenue declines were quite large, ranging from -16.2% to -12.78% in Q4, which seems that the declines are slowing down, but the company’s revenues were affected quite massively over the last year.

Revenue (SA)

Overall, we can see the company had quite a rough time in 2023. Many companies in related sectors experienced a similar fate, but given the company’s financial position and cyclicality turning positive, I would expect all these metrics to pick back up going forward, unless the macroeconomic environment turns for the worst yet again.

Q4 non-GAAP EPS came in at $0.55, which beat estimates by 3 cents, while revenues came in at $352m, which beat estimates by around $2m. Revenue decline improved, as I alluded earlier, to around -12.7%, up from around -16% in the previous quarter comparison. The management is guiding even further improvements in revenue numbers next quarter. A range of -5% to +5%, so we can see the environment is starting to improve dramatically, and we may have seen the bottom a couple of quarters ago. The demand is picking back up, and the management is positive about what's coming next, citing “As we transition into 2024, there are clearer indicators of market recovery. We are realizing renewed demand across several of our key market segments.”

I already mentioned the latest margins above, so I will skip that here and just say that the numbers have been improving, and with the market slowdown in 2023, I believe the company did rather well, and will certainly come out on top given its strong balance sheet and liquidity.

Firstly, I would like to see the company improve its efficiency and profitability by looking internally, and I am glad that is exactly what the management looks to be doing in the future. The management said that they are actively looking to “optimize operations through consolidation of their 6-inch activities into 8-inch operations.” Furthermore, to improve the company’s efficiency and profitability, the company will phase out some lower-margin products in their 6-inch offerings. The margins have come considerably down in just one year, so I do like the fact that the management is going to prioritize this, but it will take a few quarters to see the effects of these efforts.

In terms of revenues, the mobile segment is experiencing a rebound, after what was around 2 years of straight declines in demand, many analysts are suggesting the market to grow at around 4% in 2024, and achieve around 2.6% through 2027. This doesn’t sound like much, but it is a good start, and eventually, the growth should surpass pre-pandemic levels. The management said that the facility in Italy met their initial targets, and they are planning a ramp-up throughout 2024, to meet increasing demand.

In terms of automotive, the adoption of EVs has slowed down in 2023, so that didn’t help the company’s top line. However, the outlook for vehicles looks to recover and will start to approach pre-pandemic norms in 2024, eased by the chip shortages. The adoption of EVs will recover, as more and more countries start to offer more incentives and eventually, these vehicles will become less of a burden to manufacture and will cost on par with ICE vehicles. I don’t see much adoption happening in first-generation EVs that we currently have because it is not very economical, but the next iterations will be much more capital-friendly and this will impact the company’s revenues, as the demand for their components will be picking up once again.

And I feel I have to mention the buzzword of 2023 and so far in 2024, AI may play a decent role for the company, but we can’t judge how much it will contribute to the overall top-line growth, but I’m sure it is not going to hurt. AI is going to be used in many different sectors, like automotive and mobile, so further applications of AI in these markets, will certainly drive the company’s revenue potential. As the management said, “We see additional AI and mobile AR, and VR applications having the potential to drive a stronger handset refresh market over the next several years to further benefit our RF business.”

I looked back at the last DCF model that I made for the company, and I didn’t see much to change, except for the risk-free rate, which changed only slightly, I also updated the financials up to the end of 2023. The assumptions were already quite conservative in the model, so I’m ok with them going forward, as I do believe that the company will see a decent recovery in its revenue growth and margins will improve also. In my model, I went with a reduction in margins and subsequent recovery over the next decade to the margins seen at the end of 2023, so no further improvement is assumed, to keep it safe. I am, however, updating my final intrinsic value to around $45 a share, which implies the company still trades at a decent discount to its fair value.

Intrinsic Value (Author)

The risks, in my opinion, are minimal going forward, but that doesn’t mean that it’s not in our best interest to cover them. Overall, semiconductor sector might not recover as many analysts predict, and we may continue to see further declines in demand for the products, which will continue to weigh down on the company’s top line and its share price potential will not be reached. I am a little worried about the frothy valuations of some semiconductor companies recently, which are bolstering the whole market. Just look at how the markets reacted to a good Nvidia (NVDA) report just last week, sending many semiconductor companies up in sympathy, like AMD (AMD), even though it reported weak numbers, the company went up 10% in sympathy, or Super Micro Computer (SMCI) becoming a meme stock, went up 35% on the day. All three major indices went considerably up on the day also, so I would be a little cautious.

Any further escalation in Israel may send the shares further down, even though the company is not materially affected by the conflict. That doesn’t matter to investors/traders who will look for any excuse to trade on the news. So, be vigilant of any further news on that front and be sure you can stomach the volatility. I think the company’s financials are strong enough that you shouldn’t worry about such short-term noise and hold strong until the share price eventually recovers as investors recognize the company’s potential or the thesis has changed dramatically, at which point, consider selling.

It may look like the company didn’t do very well in 2023, but the fact that many companies experienced the same, tells me that the company itself will be just fine, and with any further recovery in the macroeconomic conditions and the sentiment in the semiconductor sector improving, TSEM will start to grow once again as the demand for their products ramps up and further improvements in operations internally will lead to better profitability and efficiency overall, which should unlock the company’s true value even if revenue growth doesn’t improve. Therefore, I am reiterating my buy rating, and I am looking forward to what’s in store for the sector and the company this year, which I think will be much better than last year, but we can’t predict that.