izusek

izusek

Dividend growth investors are interested in seeing a company's dividend grow over time. Rather than searching for high yields, they focus on consistently growing dividends. A growing dividend will ensure the income continues growing even when the investor begins to withdraw the distributions. Of course, since a company pays dividends out of earnings, rising dividends also means rising profits, which in turn creates share price appreciation as a byproduct.

Most dividend growth investors are familiar with the rule of 72. The rule is as follows: 72 divided by a growth rate equals the time it takes to double something.

For example, if your portfolio grows at 10% per year, it will double every 7.2 years (72/10). This rule applies to dividend growth as well.

Using the rule of 72, a company with a 2% yield today and a 10% dividend growth rate would double the dividend in 7.2 years. This would create a yield on cost (YOC) to an investor of 4%. Give it another 7.2 years, and the YOC jumps to 8%. Give it a holding time of 21.6 years, and the investor's YOC is now a whopping 16%! This compounding is the magic of dividend growth investing. Of course, maintaining that 10% growth rate is the key.

Since I became a dividend growth investor in 2009, dividend safety has been pounded into my head as the most important thing. At one point, investing in companies with less than 20 years of dividend growth was almost blasphemous. They were just too risky. To be fair, we were coming out of a severe recession and dividends had been cut left and right.

However, the longer I do this, the more I realize that as a dividend growth investor focused on high-quality companies, dividend cuts are not the main risk to my portfolio or my goals. Over the years, I have seen the occasional cut, yet my income quickly bounces back. However, to meet my goals, I need dividend growth of 7% without reinvesting dividends. Maintaining this dividend growth is the real threat to meeting my objectives.

All too often, I have purchased a company based on its past dividend growth performance, only to see it slow once it's in my portfolio. I see others who like to chase dividend growth, dumping a company with a slight increase for one with a better one. While swapping an underperformer for one with better dividend growth can be productive, it can also be a losing game.

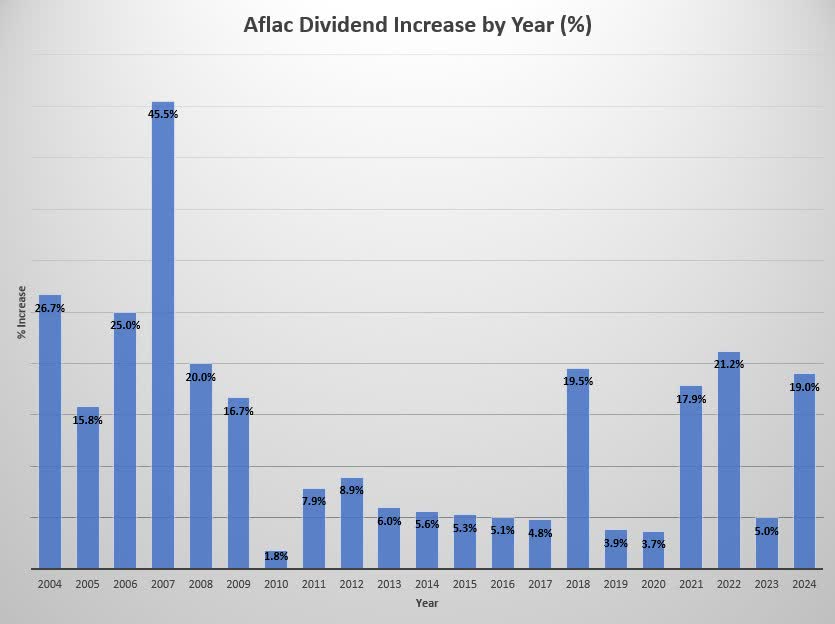

Many of the best dividend growth companies can have "lumpy" increases. Aflac (AFL) is a prime example of a company that has lumpy increases. In both 2021 and 2022, the company had nearly 20% dividend increases. However, last year's was just 4.5%. This is typical for the company, which has a 5-year dividend growth rate of 10% and a 10-year of 9%. The table below shows the lumpiness of the increases.

Wyo Investments

An investor chasing dividend growth would surely be disappointed with the 2023 increase. By the same token, an investor dumping Aflac after 2019's 3.7% raise missed the huge gains. By the way, the increase announced in February was another whopper at 19%!

Dividend increases happen for two reasons: Increasing earnings or expanding the payout ratio. Only dividend increases from earnings are sustainable in the long run. (Technically, there is a third, by borrowing, but this is an unsustainable practice.)

Because earnings are the ultimate driver in dividend growth, it seems logical to just invest in the companies with the highest projected earnings growth. Of course, if investing was that easy, we could put all our money in the one company with the highest estimate every year and crush the market. Unfortunately, earnings projections constantly change, and once you get beyond a year or two, they are "mostly" meaningless. And, of course, sentiment trumps fundamentals in the short run.

I don't mean to say that earnings projections have no value, but their use is minimal for the buy-and-hold investor looking at holding periods of twenty-plus years.

The payout ratio, the other factor in dividend growth, is a little more helpful in looking at a company's future dividend growth prospects. Companies that have grown the dividend by expanding the payout ratio will, at some point, have to slow the dividend growth to match earnings.

It's well known that, over time, many companies slow the dividend growth rate. Just compare the 5- and 10-year dividend growth rates; in most cases, the ten-year rate is higher. This slowing often occurs because many companies initiate a dividend at a very low payout ratio and slowly increase it, allowing them to grow the dividend faster than earnings. However, eventually, dividend growth needs to begin to match earnings.

Earnings growth is the ultimate factor in dividend growth rates. However, until a company reaches its maximum sustainable payout ratio, the potential to grow the dividend outside of earnings exists. In theory, a company with no debt and no capital requirements could have a payout ratio of 100%, and the dividend growth would always match the earnings growth. Of course, companies retain earnings to fund growth, R&D, capital costs, and debt servicing. The degree for each company depends on the business.

For the last couple of years, I have looked at a company's change in payout ratio to help determine its suitability for investment. However, I had always done this somewhat subjectively, simply estimating from charts. While this is perfectly suitable for evaluating a single investment, I wanted a more empirical method for comparing large data sets.

The method I settled on was using the earnings growth divided by the dividend growth, or, as I refer to it, the dividend growth coverage ratio or just DG coverage ratio. These numbers are easily attainable, and the calculation is simple. A result greater than one means the dividend growth is well covered, and a result less than one implies the dividend growth will likely need to slow in the future. At some point, dividend growth cannot exceed earnings growth.

However, because most companies initiate dividends well below their maximum sustainable payout ratio, the dividend growth coverage ratio works with the payout ratio to help determine how long the company will be able to grow the dividend faster than earnings.

While there is a limit to how high a payout ratio can go, it's safe to say that a company with a 0.85 DG coverage ratio and a 20% payout ratio can likely maintain the dividend growth rate for many years, while a company with the same DG coverage ratio and a 50% payout ratio will have many fewer years before the dividend growth rate needs to slow to match earnings.

While we can't know the future earnings growth, a company with a low payout and high DG coverage ratio can grow dividends faster than earnings for an extended time. Conversely, we know that companies with higher payout ratios and low coverage ratios are unlikely to grow the dividend faster than earnings for long periods.

Visa (V) has a 5-year dividend growth coverage ratio of 0.75 and a payout ratio of about 21%. The DG coverage ratio of 0.75 means that only 75% of the dividend growth was funded by earnings growth. As a low capital-intensive business, they could likely grow the dividend payout ratio to around 70% and still be comfortable. Even if Visa's future earnings growth rate falls considerably, it will likely be able to give 10% dividend increases for many, many years.

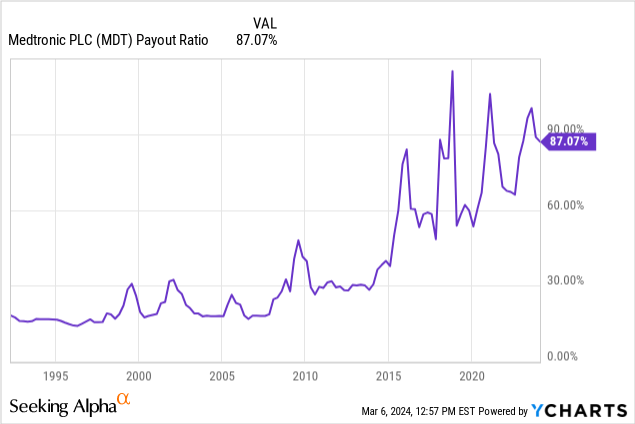

By most metrics, Medtronic (MDT) has a very safe dividend. However, its ability to grow the dividend at its past rates is questionable. The company has a 5-year dividend growth rate of over 7% and a 10-year of nearly 10%. However, earnings have not covered the dividend growth.

The dividend growth coverage rate is zero (actually slightly negative) for the last five years! This means the dividend has grown entirely by expanding the payout ratio. The 10-year isn't much better at 0.31. At an adjusted earnings payout ratio of 50%, it's unlikely to expect dividend growth to do much more than match earnings in the future. The expanding payout ratio is shown in the chart below.

The coverage ratio isn't helpful for companies with long-standing dividend policies to payout out a certain percentage of earnings or cash flow, such as Paychex (PAYX) or Altria (MO). The dividend growth of these companies will always match earnings, mainly because they are close to their maximum sustainable payout ratios.

Some companies make sudden changes in their dividend policies, making the dividend coverage ratio look worse. Examples in recent years include Broadcom (AVGO) and Tractor Supply Company (TSCO). TSCO consistently paid out around 25% of adjusted earnings until they gave a massive 75% dividend increase in 2022. The enormous increase jumped the payout ratio to closer to 40%. While their 5-year dividend growth coverage ratio sits at 0.71, the ratio skews lower due to a change in dividend policy.

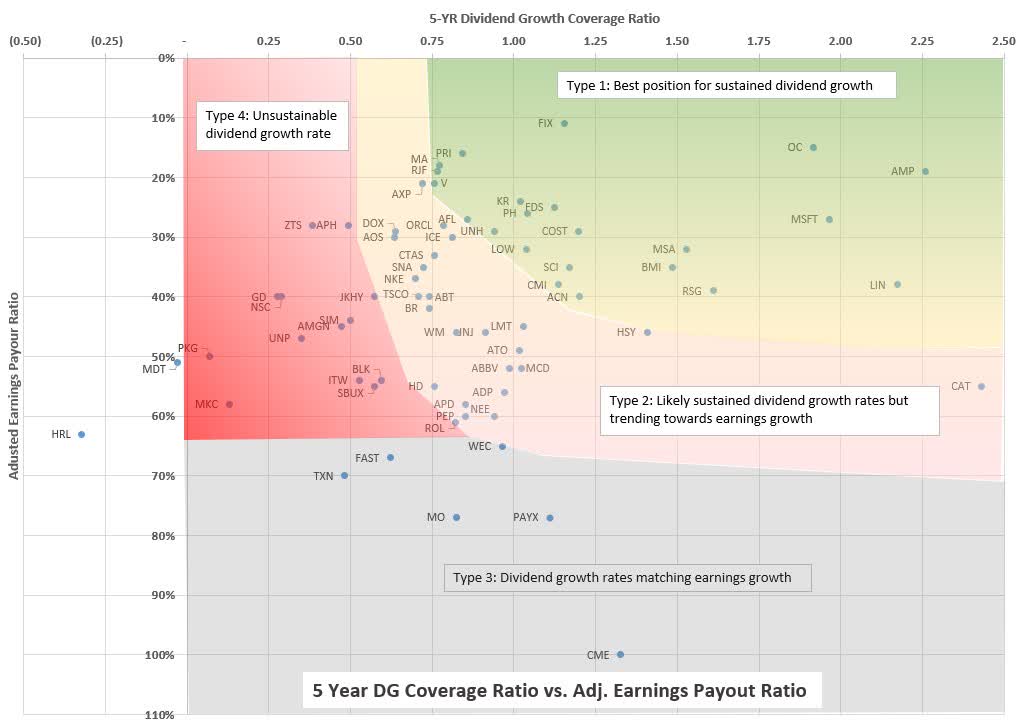

There are two cases where this is particularly useful: Fast dividend-growing companies with low yields and evaluating dividend growth all-stars of the past.

Below is a chart plotting 5-year dividend growth payout ratios against adjusted earnings payout ratios. I've identified approximate quadrants that I watch. Companies I consider Type 3 or Type 4 require extra consideration before investing, especially if an investor is using past dividend growth rates as a consideration. While the Type 1 companies have the best likelihood for sustained dividend growth rates.

Wyo Investments

While there is no way to know for certain how companies will perform in the future, companies with higher payout ratios that have not covered dividend growth with earnings are likely to have slower dividend growth in the future.

While earnings are the ultimate driver of dividend growth, companies that have managed their dividend growth well in the past are likely to do so in the future.

Ok, that's eleven, but it doesn't seem fair to separate Visa and Mastercard. Additionally, it should be mentioned that CAT is highly cyclical, so its payout ratios fluctuate significantly. However, the company is by far the best at managing its dividend through the cycles.

Additionally, there are a few companies with fast-growing dividends that may need to slow the dividend growth going forward, maybe not immediately, but I wouldn't expect the next five years of dividend growth to match the last. These include Amphenol (APH), and Zoetis (ZTS).

The dividend coverage ratio is just one metric that I consider when evaluating a company. While earnings growth ultimately drives dividend growth, the coverage ratio allows an investor to consider whether a company has artificially inflated its past dividend growth rates.

It might seem a trivial metric, but when looking at a twenty-year-plus holding period, any variable an investor can remove is a benefit. Using the dividend growth coverage ratio, coupled with the payout ratio, can be a valuable tool in evaluating future dividend growth prospects.

It's all about needing the dividend growth to justify the low starting yield for fast-growing companies. While for low-payout, fast-dividend-growth companies, future earnings will always play a significant role, it's essential to consider the current payout ratio and the coverage ratio to determine if there is a factor of safety in the earnings.

For higher-yielding companies that have seen outsized dividend growth rates, it's about avoiding ones that have grown the dividend significantly by expanding the payout ratio. It's about understanding where the past dividend growth came from and how indicative it is of what the future holds.