SOPA Images/LightRocket via Getty Images

SOPA Images/LightRocket via Getty Images

trivago (NASDAQ:TRVG) is a German company that operates in an extremely competitive market; it does not have a particular competitive advantage and has lost market share over time, however, the company has more cash than debt and having a non-capital intensive business, it is nevertheless able to generate a positive FCF.

This is not a very good premise for an investment thesis if one embraces the principles of "modern value investing," which recommend investing in companies with exceptional businesses and competitive advantages that can endure over time. In my view, trivago could meet the prerequisites of Benjamin Graham's value investing and fall into what Warren Buffett calls "cigar butt"; companies with businesses that are unexciting but cheap enough to offer short to medium term earnings opportunities.

Personally, when I invest in a company I do so with the intention of ideally holding it forever. trivago in my opinion does not have the necessary characteristics for this type of strategy, but it might be a stock to watch for those with a more "traditional" approach to value investing.

trivago is a global accommodation search platform, founded in 2005 by three university classmates, Rolf Schromgens, Peter Vinnemeier, and Stephan Stubner (who left the company in 2006 and was replaced by Malte Siewert). In 2013 Expedia Group bought 63% of the company's shares, increasing its stake slightly in 2016 by purchasing the shares of some employees who had exercised their stock options. Today Expedia Group holds 61% of the class B shares (which entitle the holder to 10 votes per share), and has an absolute majority in the company.

trivago is a search and comparison product, and users do not book directly on this platform, but are redirected to the site of the company that posted the ad on trivago. trivago's business model is therefore centered on referral; advertisers participate in the marketplace by forwarding CPC bids (cost-per-click) for each user click on each hotel ad.

With this model, trivago cashes in regardless of whether the user completes the booking or not. However, in 2020 they also introduced a CPA (cost-per-acquisition) based model, in which case the advertisers pay trivago a percentage of the booking revenue.

Once you understand how trivago generates revenue, it is immediate to understand that traffic volume is one of the most important performance indicators. The more people who visit trivago's platform, the greater the number of clicks on ads and the more interest advertisers have in advertising on the platform.

Who is interested in advertising on trivago? The main advertisers on the platform are OTAs (Online Travel Agency), hotel chains or independent hotels, and alternative accommodation providers. trivago's main customers are Booking Holdings (43% of revenue in FY23, 49% in FY22) and Expedia Group (36% in FY23, 33% in FY22). Interestingly, trivago's main customers are also its competitors and owners (in the case of Expedia). Moreover, among the companies that are part of Expedia Group, we also find Hotels.com, a large customer of trivago and a direct competitor (it is not an OTA but a comparison site exactly like trivago). Needless to further emphasize the hilarity of this situation.

For completeness, it is useful to point out that trivago also generates revenue through other b2b services, such as white label services, data product offerings, and subscription fees for the trivago Business Studio PRO Package. The weight of these services on total revenue is practically insignificant, in fact, in 2023, "other revenue" accounted for about 1.72% of revenue (2.53% in FY22).

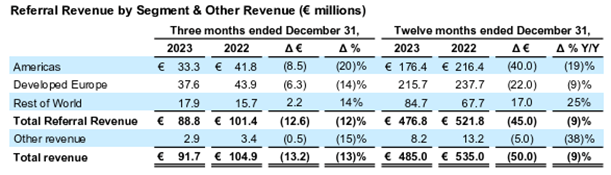

In terms of Referral Revenue, on the other hand, trivago divides this revenue into three geographic areas: Americas, Developed Europe, and Rest of World.

Q4 FY23

The Americas segment accounted for 37% of referral revenue (41.5% in FY22) and decreased by 19% in 2023, due to lower traffic volumes due to increased competition in performance marketing channels, softer bidding dynamics on the platform compared to the previous year. These same reasons also led to a 9% reduction in revenue in the Developed Europe segment, which accounts for about 45% of referral revenue. Rest of World was the only segment that grew (+25% yoy), driven by higher traffic volumes in Japan and Turkey and an increase in travel demand fueled by greater investment in marketing; a reduction in traffic volumes in Central Eastern Europe slowed the segment's performance.

Q4 FY23

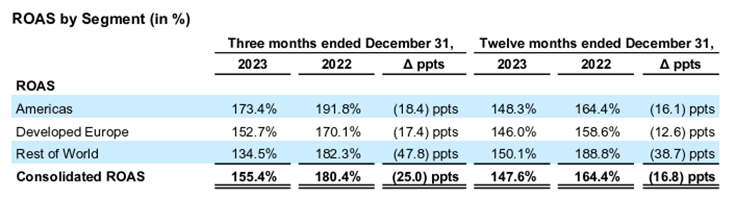

Selling and marketing expenses are the main category of expenditures, in 2023 they were 71% of revenue (64% in 2022), trivago manages to generate sufficient traffic only inorganically therefore incurs high expenditures in marketing, both brand awareness and performance marketing, buying travel and hotel-related keywords from search engines. ROAS is consequently a key indicator for judging the company's performance, and it has deteriorated significantly in the past year due to higher expenses that generated less revenue than in 2022.

Marketing is an extremely critical aspect of trivago's business model and on which depends not only the ability to generate satisfactory margins but also the revenue generation itself. In particular, in performance marketing it suffers extreme competition from larger companies with larger budgets that are interested in the same keywords. Expedia and Booking in addition to being major clients but also competitors (direct or otherwise), compete with trivago in ranking in the top positions on search engines. Being companies with larger advertising budgets than the one available to trivago inevitably increase the cost of traffic acquisition and also reduce the visibility of the platform. This in my opinion makes it extremely risky to invest with a long term view in trivago (10+ years), having no competitive advantage, the business of this company is in the hands of the big players in the industry who, having greater economies of scale, are able to achieve better positioning.

trivago's current strategy is to relaunch its brand in order to make a profitable return to long-term growth. In mid-December they launched globally a new advertising campaign with a new logo and a "refreshed visual identity." These brand awareness campaigns clearly take time to actually translate into sales, for 2024 they are in fact expecting higher marketing expenditures but stable operating expenses (outside advertising spend) compared to 2023.

We continue to believe that, as we increase our brand marketing efforts throughout 2024 and in the coming years as part of our multi-year strategy, this will have a long-term positive impact on the volume of direct traffic to our platform. As we re-invest our profits into our marketing strategy to fuel revenue growth in the medium-term, we continue to expect Adjusted EBITDA2 to be close to breakeven for 2024.

Source: Q4 FY23

TIKR

Compared to 2016, trivago's revenue decreased by about 35.7%, and is less than half of the 1 billion euro peak reached in 2017. This decline is mainly due to a decrease in spending on marketing, in fact, in 2017 the latter amounted to about 947 million euros compared to 345.6 million in 2023. As mentioned in the previous paragraph, trivago generates virtually all of its traffic inorganically, if spending on marketing increases, sales should tend to increase as well, and vice versa.

2016-2023 (TIKR)

On a positive note, in the same time frame the company has become more efficient and managed to optimize its expenses. From having a negative operating margin in 2017 of -2%, in 2023 with less than half of the revenue this was 8.2%, generating an operating income of almost 40 million euros.

In FY20-22-23, the company's net income was heavily negative due to substantial impairments on goodwill and intangible assets of 208 million, 185 million, and 196 million euros, respectively. In 2023, the Developed Europe and Americas segments suffered an impairment of 95.5 million and 86.5 million euros, respectively, due to adjustments made on the profitability outlook after the announcement of the new strategy geared toward long-term growth, which includes increased spending on brand awareness. Currently, trivago's goodwill is zero and there are only 76 million euros of intangible assets in the balance sheet.

A very positive aspect of trivago is its excellent financial condition, which inevitably limits downside risk. In fact, trivago has about 127 million in cash and short term investments and only 110 million in total liabilities, of which about 30 million are Accounts Payable and Accrued Expenses, more than covered by about 60 million in total receivables and prepaid expenses. It has no financial liabilities but only 38.4 million in capital leases and 26.5 million in non-current deferred tax liabilities. Moreover, given the company's ability to generate positive cash flows in recent years, I believe that the condition of this balance sheet greatly reduces the risk of catastrophic losses.

2019-2023 (TIKR)

It is also necessary to mention that in 2023 the company paid a substantial special dividend of 184 million euros, which clearly significantly reduced cash resources compared to 2022 and caused the share price to plummet.

trivago's current market capitalization is about $185 million (about 171 million euros) and it has an Enterprise Value around $90 million (about 83 million euros). If one compares the EV with the 2023 FCF, the yield is about 29%, a very attractive yield for which, however, some valid justifications can be found:

TIKR

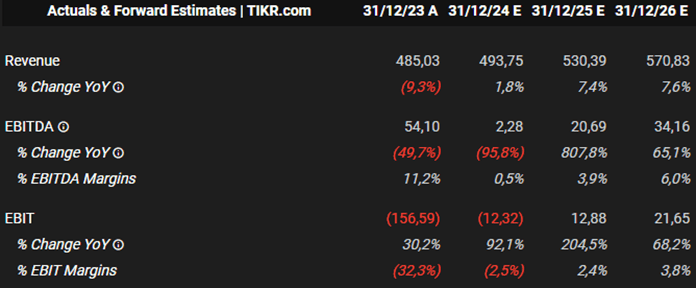

Should the new strategy be successful, how much could trivago be able to achieve in terms of EBIT? For 2024 given the high expenses in marketing expected, the company said it would reach EBITDA breakeven, this would result in a slightly negative EBIT (in 2023 D&A was about 4.5 million euros). The operating margin in 2023 was 8.2 percent (12 percent in 2022 and 2.8 percent in 2021), if we apply this margin to analysts' projected 2026 revenue, trivago could achieve an operating margin of about 47 million euros, which would result in a forward P/EBIT of less than 4 and a forward EV/EBIT of 1.9. Given the increase in marketing expenses as a percentage of revenue, however, I consider this scenario overly optimistic. Analysts predict an EBIT margin of 3.8 percent, much closer to that achieved in 2021. In this case the forward P/EBIT would be around 8 while an EV/EBIT of 4.

For a company with no competitive advantage and not so clear growth potential, a P/EBIT multiple between 8 and 10 might be right. Should management be able to demonstrate to the market that it can invest the cash generated by the business with satisfactory returns, and perhaps initiate stable distribution policies (dividends or buybacks), a lot of value could be unlocked, and the market might pay more attention to multiples based on EV rather than market capitalization. In this case, an EV/EBIT multiple of 4 would be very low, and could well be between 8 and 10. For comparison, consider that Expedia's current EV/EBIT multiple is just over 12, however, since trivago is a company with a lower competitive advantage the multiple should clearly be lower.

The current valuation thus seems attractive, considering also that analysts' expectations (especially in terms of margins) are not that high, trivago might be a company to watch if you have a Benjamin Graham approach.

The success of any investment in trivago depends solely on management's ability to execute the new strategy. Should it be successful in increasing user traffic and achieving satisfactory margins, the multiples could expand significantly. Otherwise, the company could simply burn through the cash it currently has on its balance sheet or it could grow but not profitably, as happened in the 2016-2018 period, destroying shareholder value.

Lacking a strong and lasting competitive advantage, trivago's worst enemy is time. While it may be able to achieve good results in the short term as a result of a successful advertising campaign, the absence of a competitive advantage and the presence of much larger and better-known players makes the company's long-term future extremely uncertain in my opinion.

The "investment thesis" strategy I have presented in this article is different from the one I personally prefer as a long-term investor. It is much more like the "first" value investing, the one that looked for cheap companies without taking into consideration the qualitative characteristics of the business. Perhaps the current price of trivago is not yet low enough to consider it a "cigar butt," but I believe it is low enough to offer at least satisfactory returns. The very good balance sheet and the ability with which the company can choose to become very profitable, decreasing expenses in brand awareness (clearly at the expense of turnover), makes the risk of significant capital losses limited.

The results of the first quarter of FY24 and management's comments on the execution of the new strategy will be key to understanding whether the company is on the right track for long-term growth.