pastorscott/iStock via Getty Images

pastorscott/iStock via Getty Images

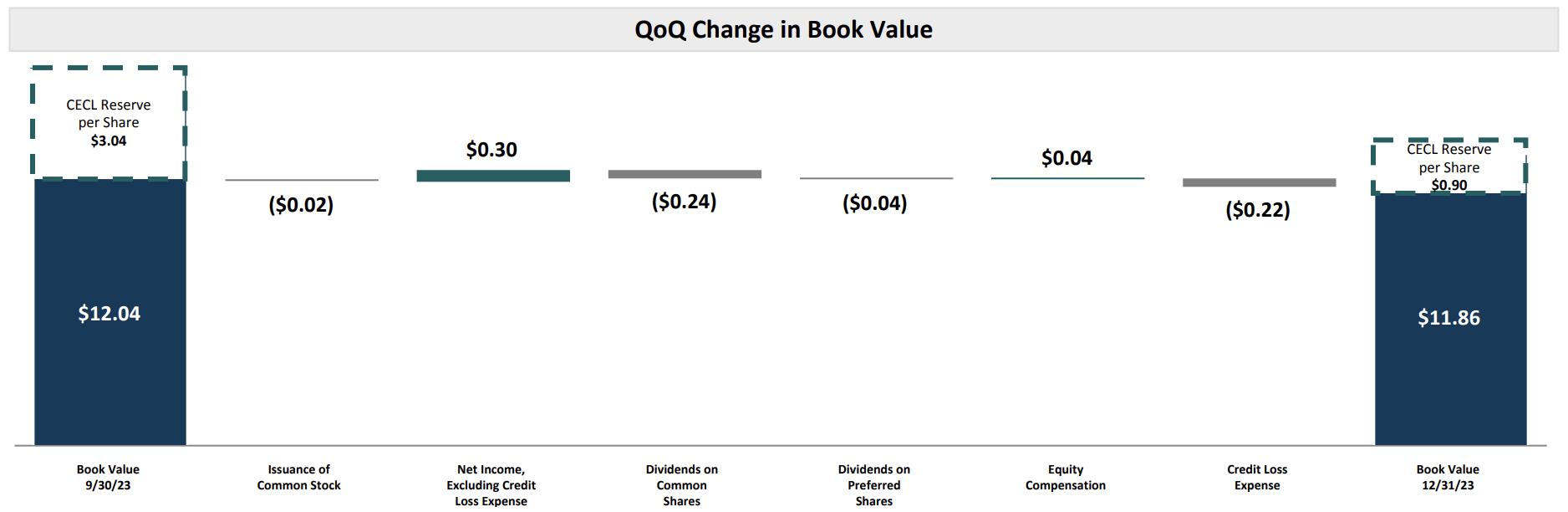

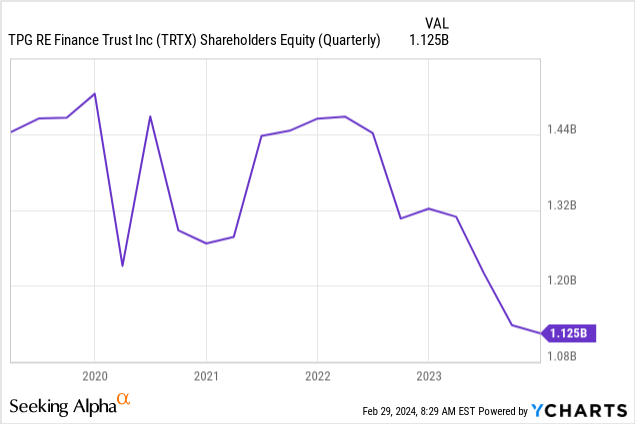

TPG RE Finance Trust, Inc. (NYSE:TRTX) common shares have rallied heavily recently on the back of fiscal 2023 fourth quarter earnings that highlighted at just how deep of a discount the mortgage real estate investment trust ("mREIT") was trading. When I last covered the ticker, this was a 46% difference from its book value per share, with the commons dipping since that article. Hence, even though fourth quarter earnings saw book value per share dip by 18 cents, the discount had widened on commercial real estate fears and reduced expectations of base interest rate cuts going into 2024.

TPG RE Finance Trust Fiscal 2023 Fourth Quarter Supplemental

TRTX is currently trading at a 40% discount to book value per share of $11.86 at the end of its fourth quarter and last declared a $0.24 per share cash dividend for an annualized 13.6% dividend yield on the commons. The commons still command a hold rating, but the Series C preferreds shares (NYSE:TRTX.PR.C) offer a healthy return profile in which I've taken a significant position in recent weeks. These are a possibly potent way to play possible Fed rate cuts later this year, but critically are currently undervalued against the core risk faced by TRTX.

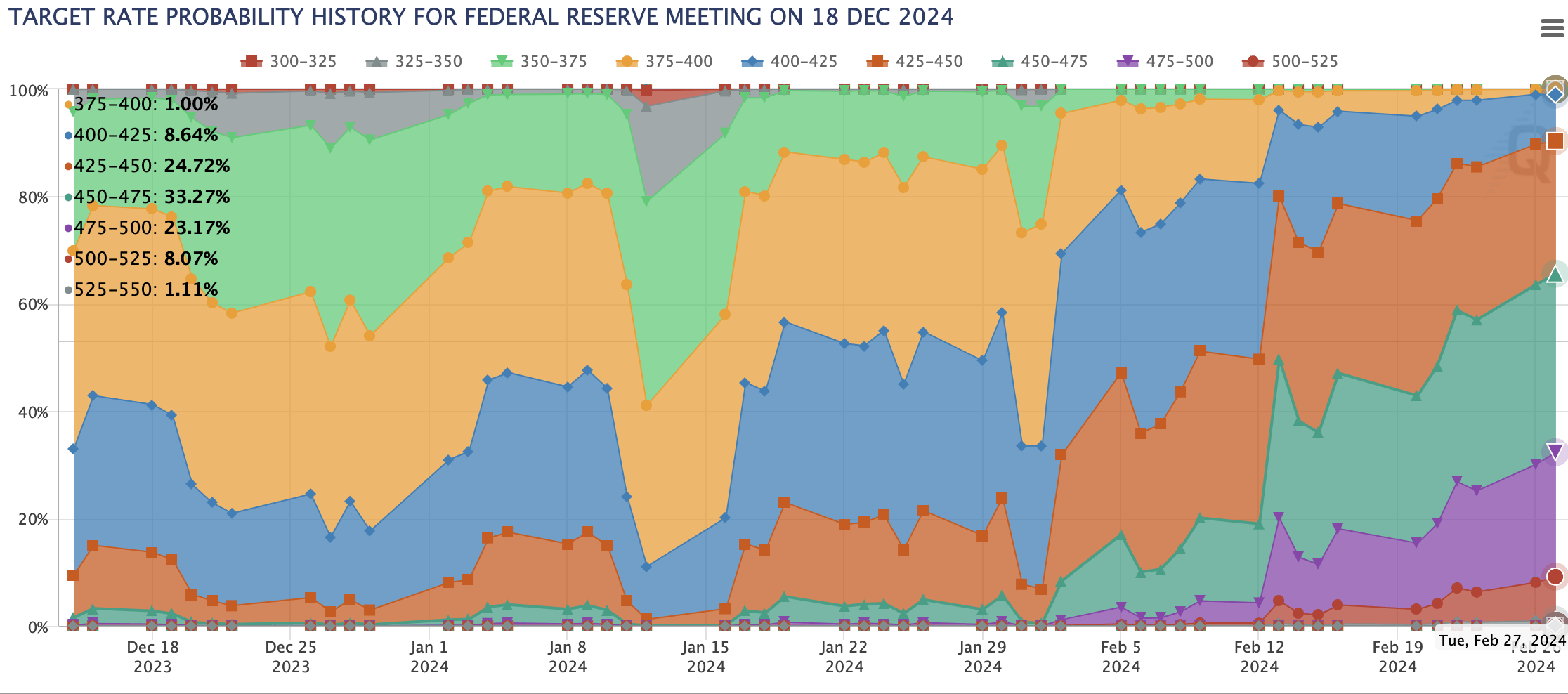

CME FedWatch Tool

JPMorgan Chase's (JPM) Jamie Dimon recently came out to state that the fears around CRE are being overblown, with most players likely going to muddle through the disruption posed by the Fed to the asset class. This hinges on the U.S. not falling into a recession, with the market currently pricing in a 70% to 80% probability of a soft landing even as the odds of aggressive rate cuts get pared back with the market now expecting 75 basis points of cuts to exit 2024, down from 150 at the start of the year.

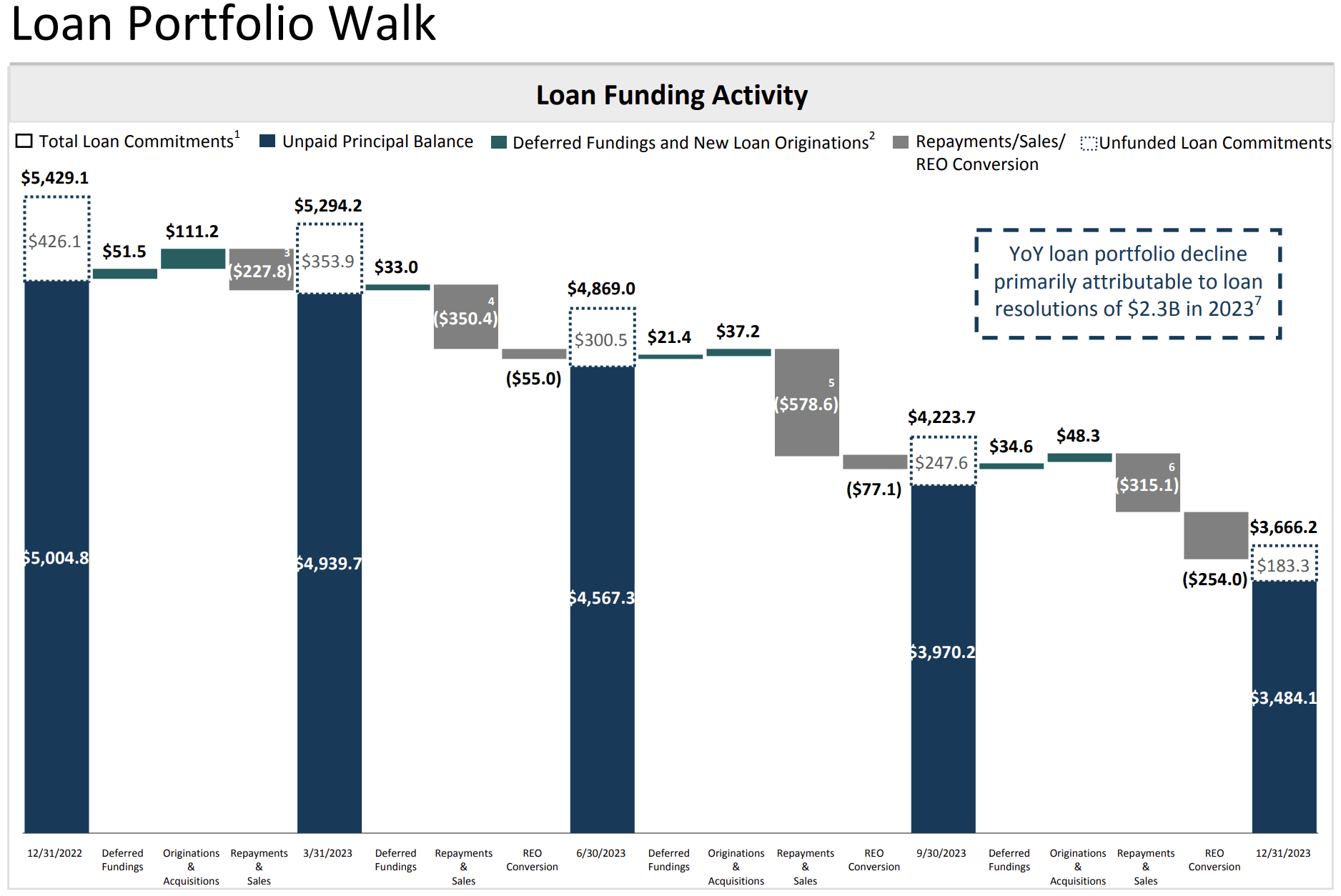

TRTX's loan portfolio was valued at $3.67 billion at the end of its fourth quarter following $315 million in loan repayments and sales versus originations of $48.3 million and deferred fundings of $34.6 million. The mREIT spent 2023 deleveraging with full repayments for 2023 at $711.6 million running far ahead of investments of $229.4 million. Partial loan repayments meant repayments came in at $907.0 million for 2023.

TPG RE Finance Trust Fiscal 2023 Fourth Quarter Supplemental

However, some parts of this decline have been driven by realized losses on loans. TRTX sold two loans during the quarter for aggregate losses of $78.2 million. This included an office loan with a $84.7 million unpaid principal balance offloaded for $29 million and a dramatic 66% discount for a loss on sale of $55.8 million. It also included a multifamily loan with an unpaid principal balance of $127.3 million.

TPG RE Finance Trust Fiscal 2023 Fourth Quarter Supplemental

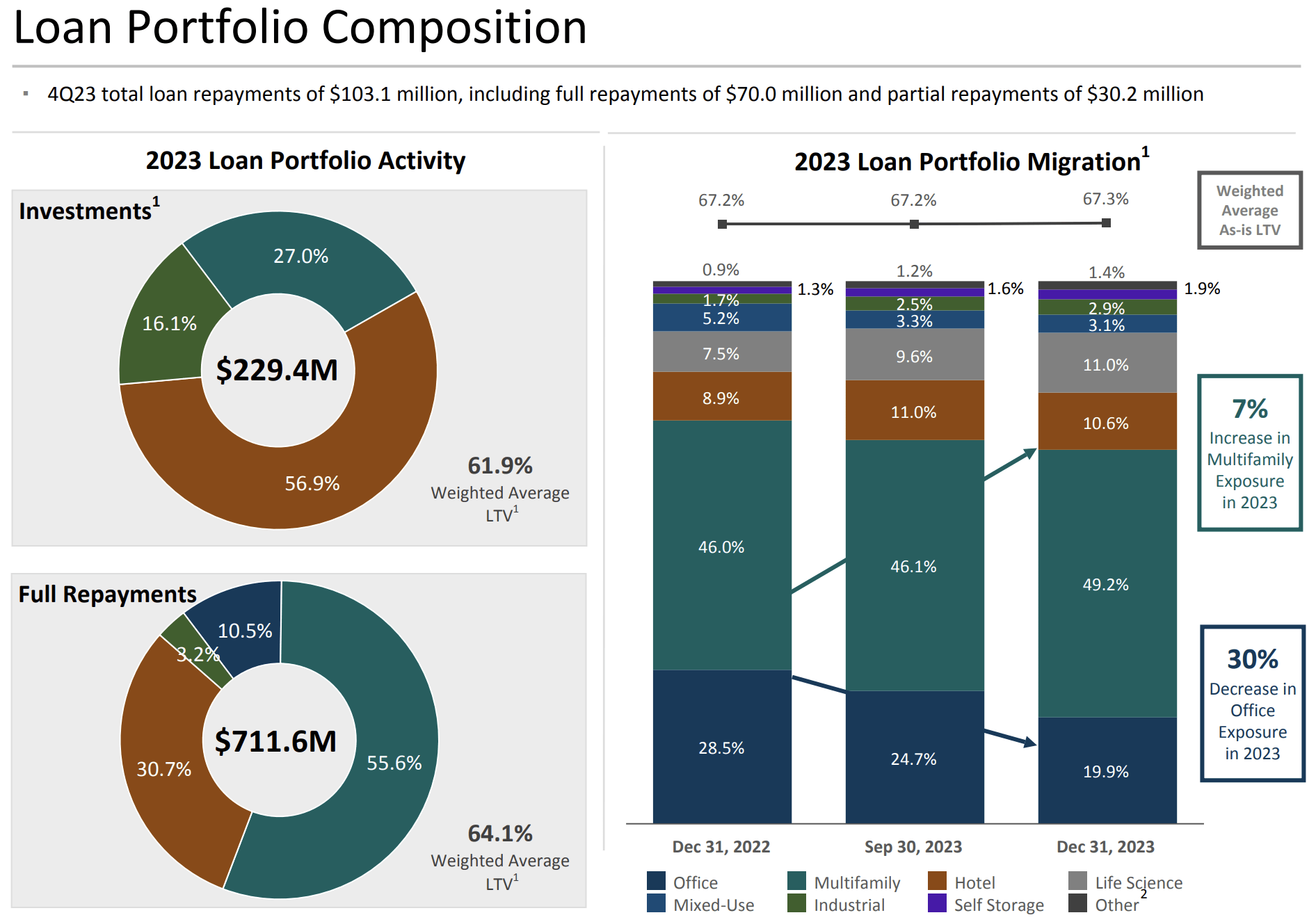

Hence, while TRTX's portfolio has seen its allocation to office properties drop from 28.5% at the start of 2023 to just under 20% at the end of the fourth quarter, this has come at the cost of sustained realized losses. The dip in book value of the mREIT reflects this seemingly controlled but still unattractive dip in shareholders' equity. This looks to be stabilizing.

This continued fall in TRTX's portfolio poses risks around the mREIT's ability to sustain its common share dividends, it has set the backstop for materially safer preferred payments. TRTX is fully amidst a structural shift of its portfolio away from office loans. The mREIT's CECL reserve at the end of the fourth quarter was $69.8 million, a dip from $214.6 million at the start of 2023 against losses of $189.9 million in credit loss expenses, around $2.44 per share, realized through the year.

QuantumOnline

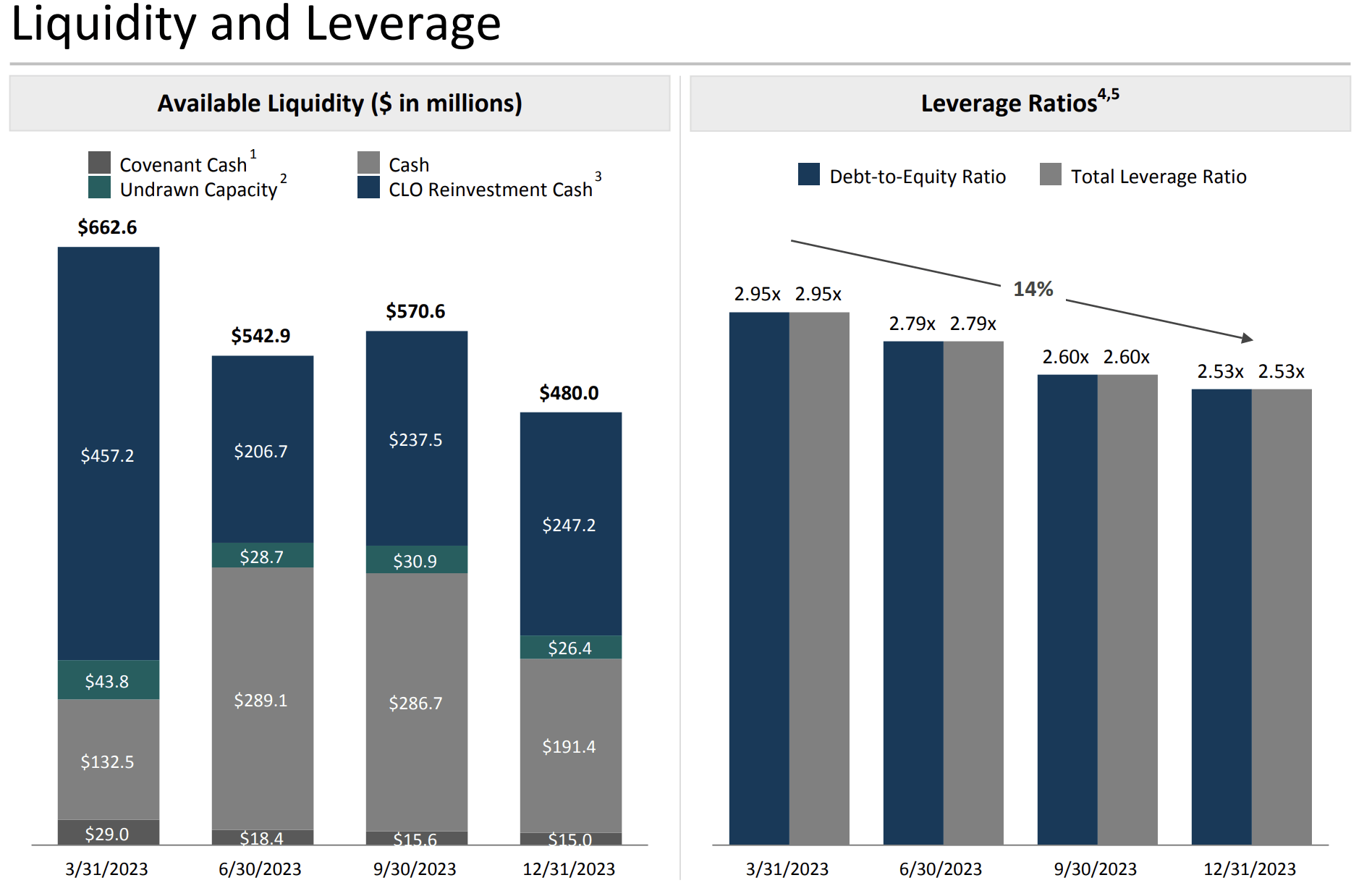

The preferreds are currently trading hands for $16.40 per share, a roughly 34% discount to their liquidation value of $25 per share or for 66 cents on the dollar. Further, the $1.5625 annual coupon means a 9.5% yield on cost. These two factors have come against a portfolio that is set to soon reach an inflection with CECL reserves at new lows and the mREIT's leverage profile having seen a sustained reduction with multifamily exposure increasing and the Fed set to cut rate to provide a boost to preferreds due to the positive duration effect. The mREIT's debt-to-equity ratio came in at 2.53x at the end of the fourth quarter, a 14% dip from 2.95x at the end of its 2023 first quarter.

TPG RE Finance Trust Fiscal 2023 Fourth Quarter Supplemental

The higher concentration of multifamily properties should place TRTX on a fundamentally safer path with the mREIT generating a 3 cents per share GAAP net income during the fourth quarter. Distributable earnings were negative at $2.05 per share. Not enough to cover to common share dividend, raising the specter of a dividend cut on the common. Hence, the TPG RE Finance Trust, Inc. preferreds form a materially safer redoubt against TRTX's lack of common dividend coverage but a still healthy liquidity balance and lower office exposure.