Yauhen Akulich

Yauhen Akulich

All financial numbers in this article are in Canadian dollars unless noted otherwise.

I don't like this market environment. As I have written in many prior articles, the risk/reward is poor. Valuations are lofty, and sentiment is very bullish.

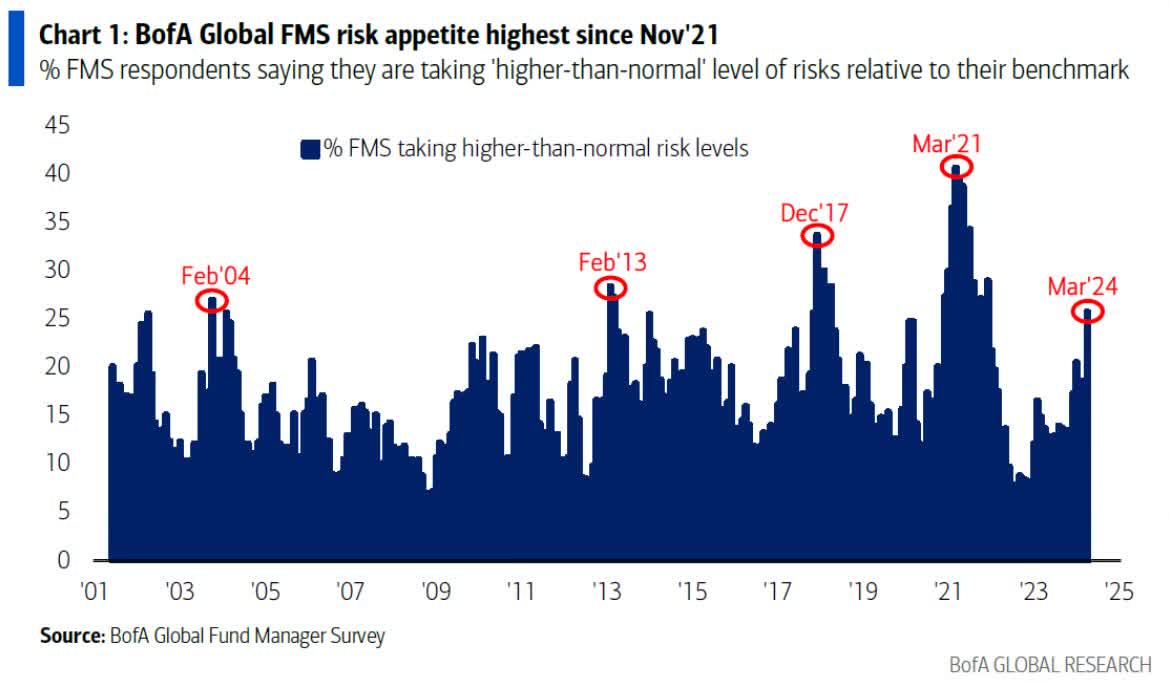

Looking at the latest Bank of America (BAC) numbers, we see that the number of fund managers who are taking "higher-than-normal" levels of risks has reached a number that tends to be unfavorable for the risk/reward.

Bank of America

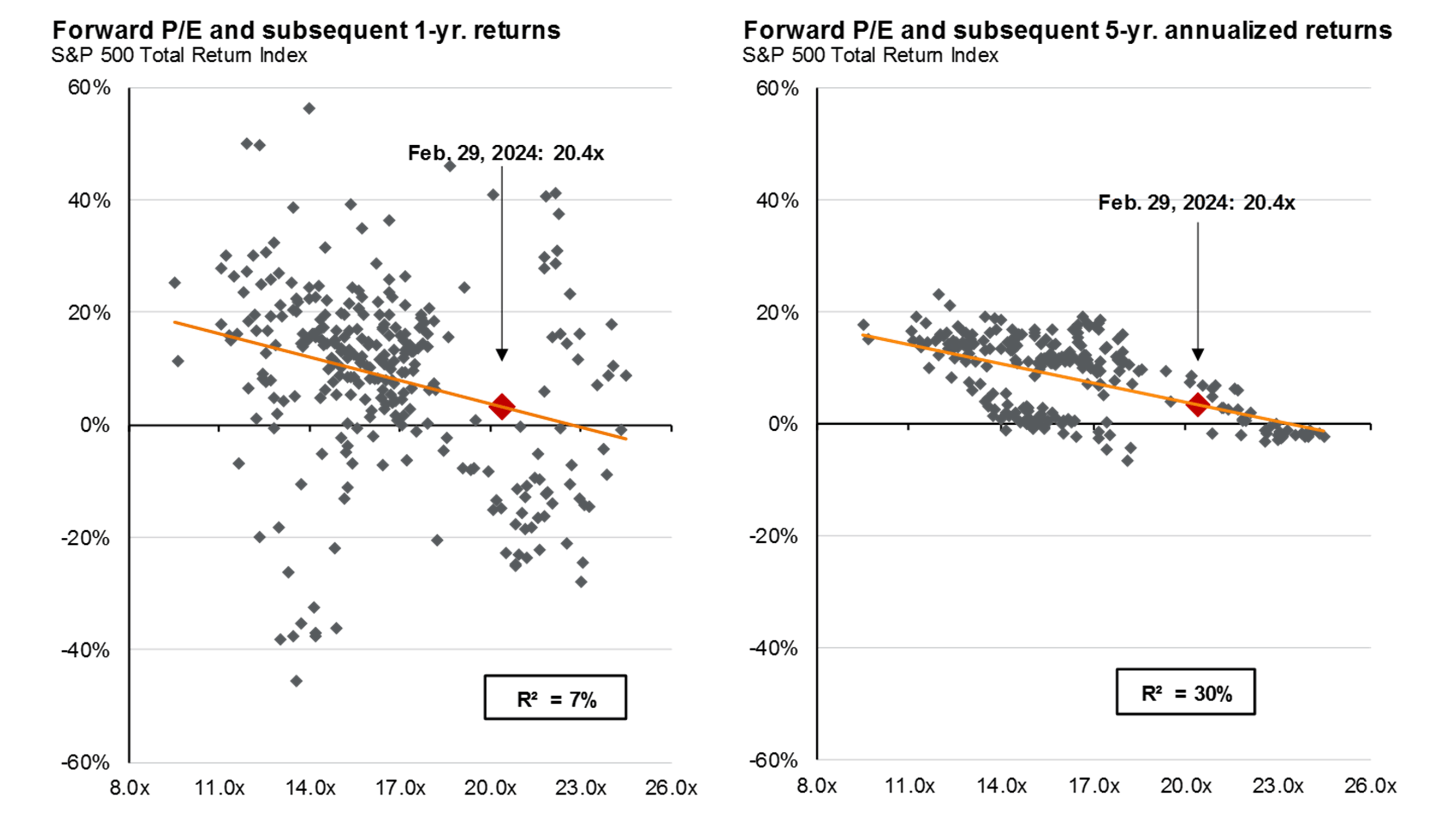

The chart below shows that going into this month, the market's valuation of more than 20x earnings indicated a high likelihood of subdued returns over the next five years.

Usually, when markets are this "expensive," we are looking at less than 5% annual returns going forward.

JPMorgan

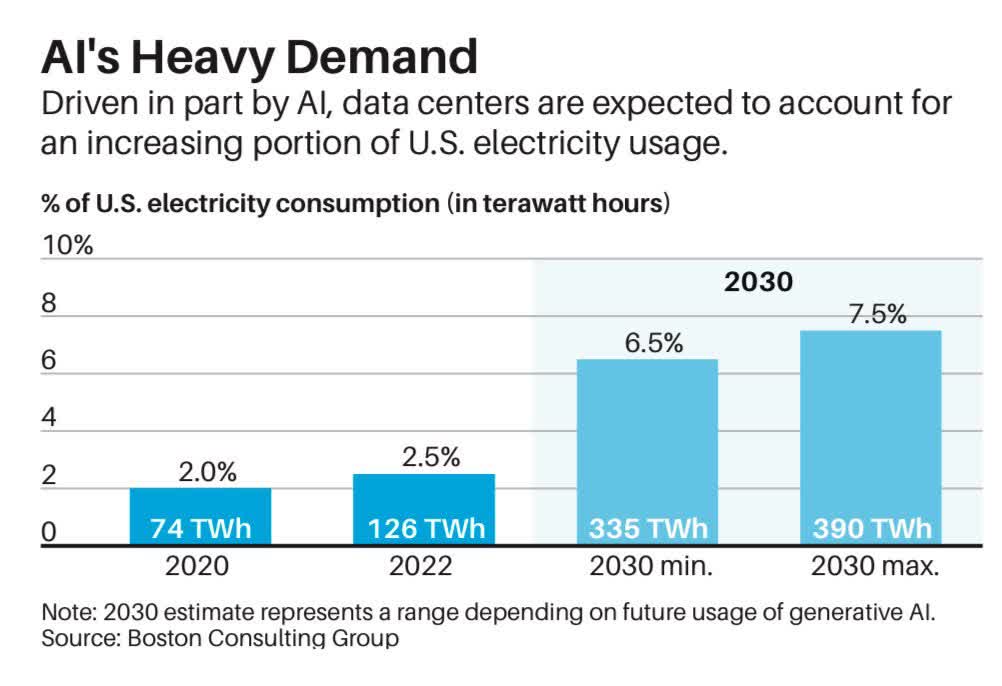

This has caused me to return to a company I have covered in the past. A company that not only benefits from long-term global natural gas demand growth but also accelerating energy demand caused by secular trends like artificial intelligence ("AI").

Looking at the data below, we see that the impact of AI on electricity demand could rise to at least 6.5% by 2030!

In 2022, that number was 2.5%, indicating an addition of at least 209 terawatt hours.

Boston Consulting Group

This is bullish for natural gas.

“Electricity demand is experiencing three times faster growth per year this decade than what we’ve seen in previous decades, driven by the increase in electric vehicles and emergence of new, large-load data centers,” Williams President and CEO Alan Armstrong told analysts this month.

“This is a major shift for our country, and it’s a major shift for the natural gas market to be able to keep up with this,” he said. “We are projecting that data center loads will be up to 30 gigawatts by 2030.” - Williams Companies

The star of this article is TC Energy (NYSE:TRP), a company that does not produce natural gas. However, it transports fossil fuels using one of the biggest networks in North America.

My most recent article on the stock was written on November 8, 2023, when I went with the title "TC Energy Stock: 7.4% Dividend Yield, This Is A Fascinating Income Play."

Since then, New York-listed shares have returned 13.5%.

In this article, I'll revisit my bull case and explain why this 7%-yielding stock remains one of my favorite income plays in the midstream industry.

So, let's dive into the details!

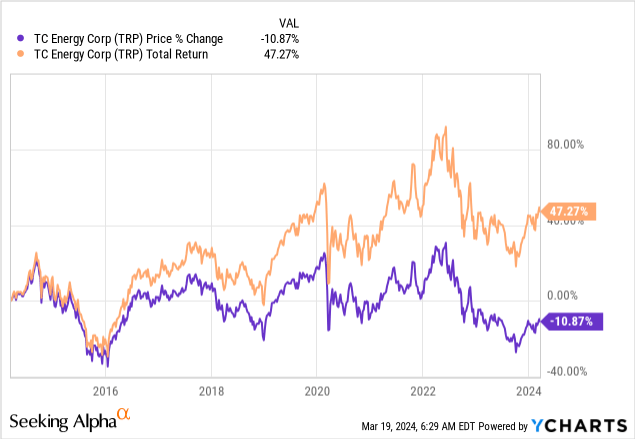

Over the past ten years, New York-listed TRP shares have fallen by 11%. That's a horrible performance. Including dividends, the total return rises to 47%. That's better, yet nothing to write home about.

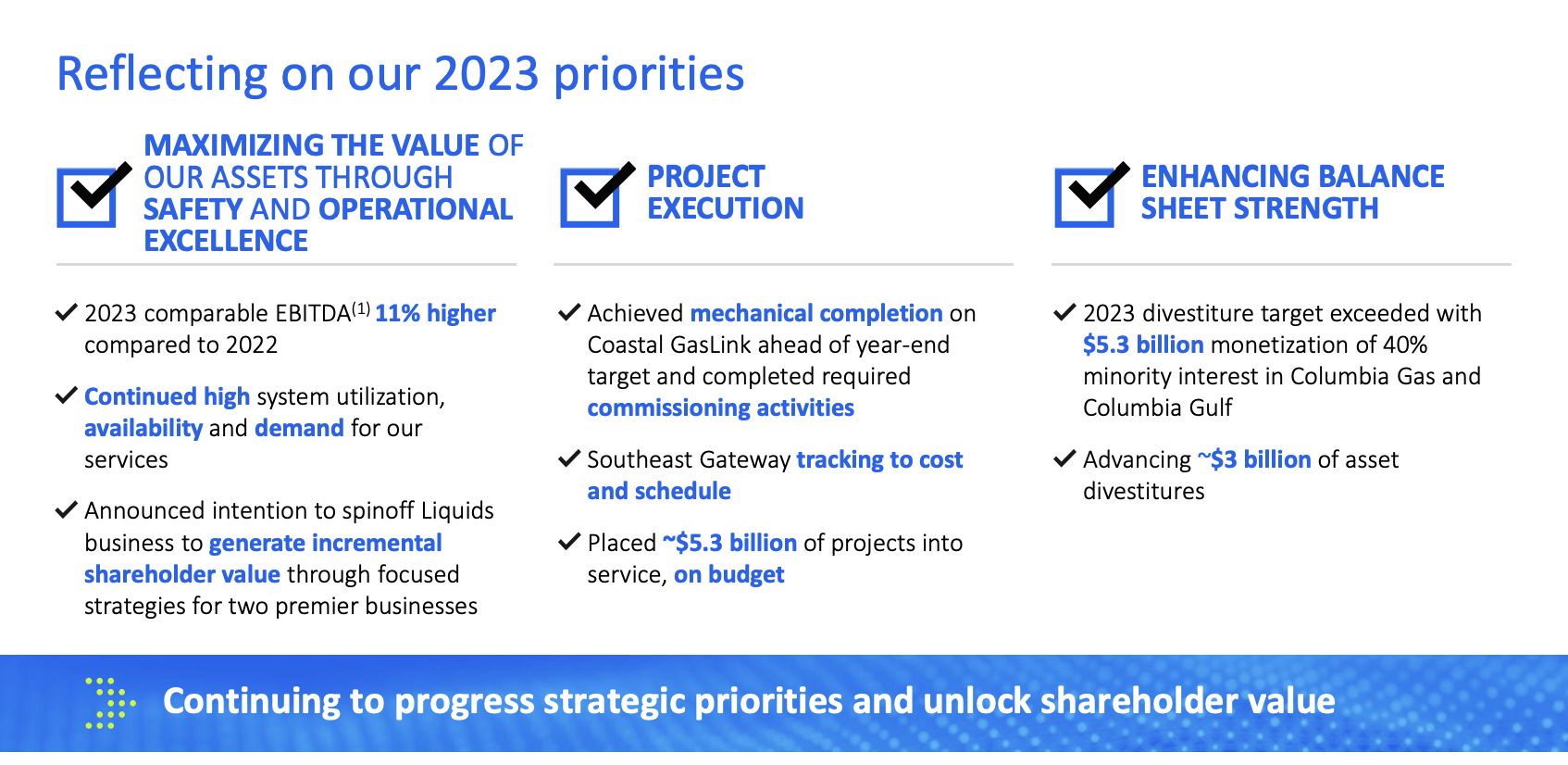

The good news is that the company is seeing improvements, as its stock price is gaining upside momentum, fueled by spin-off news and improving fundamentals.

For example, last year, the company had a record year, as it grew comparable EBITDA by 11%.

TC Energy Corporation

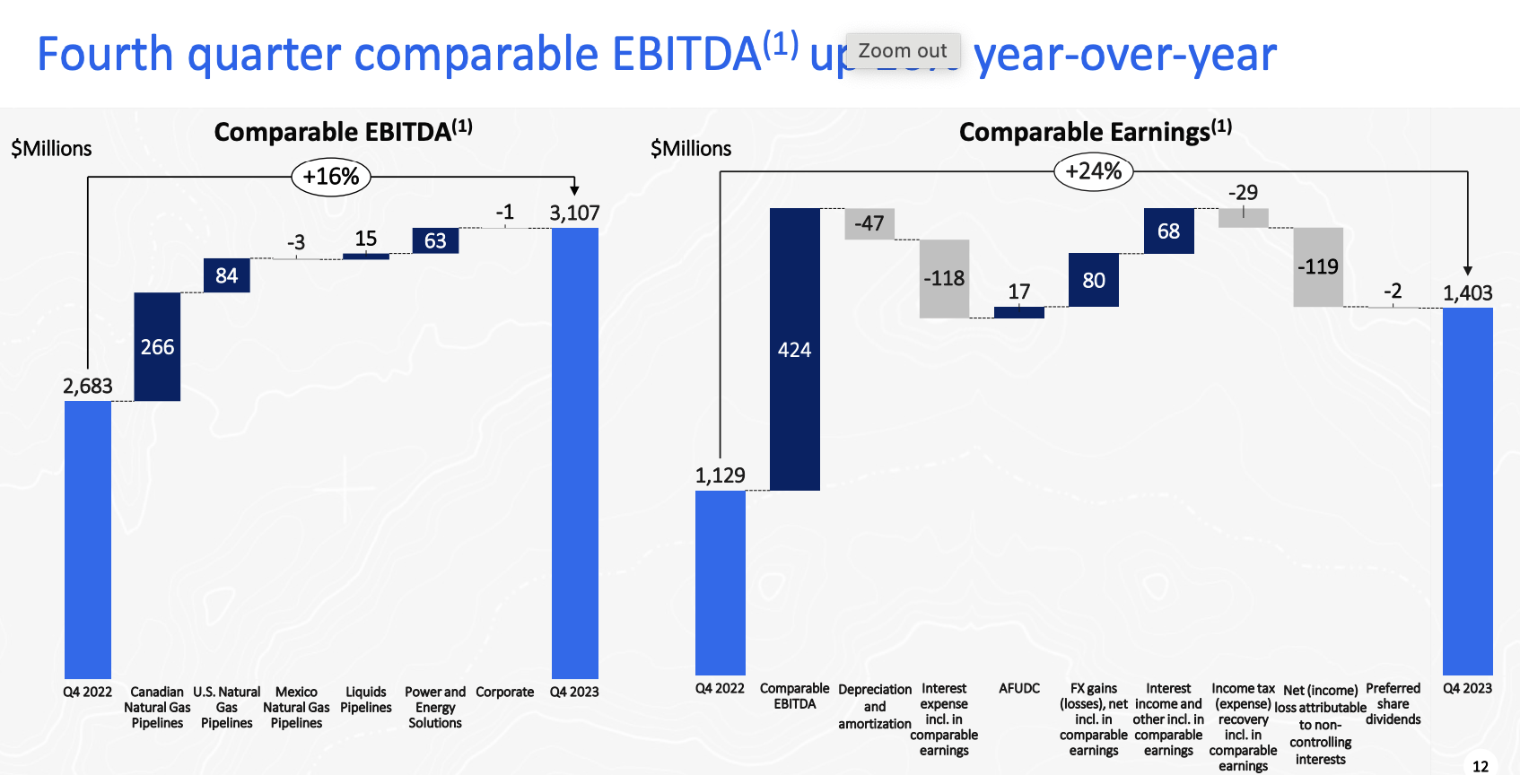

In the fourth quarter, comparable EBITDA increased by 16%. This was primarily attributed to its Canadian natural gas pipeline business.

TC Energy Corporation

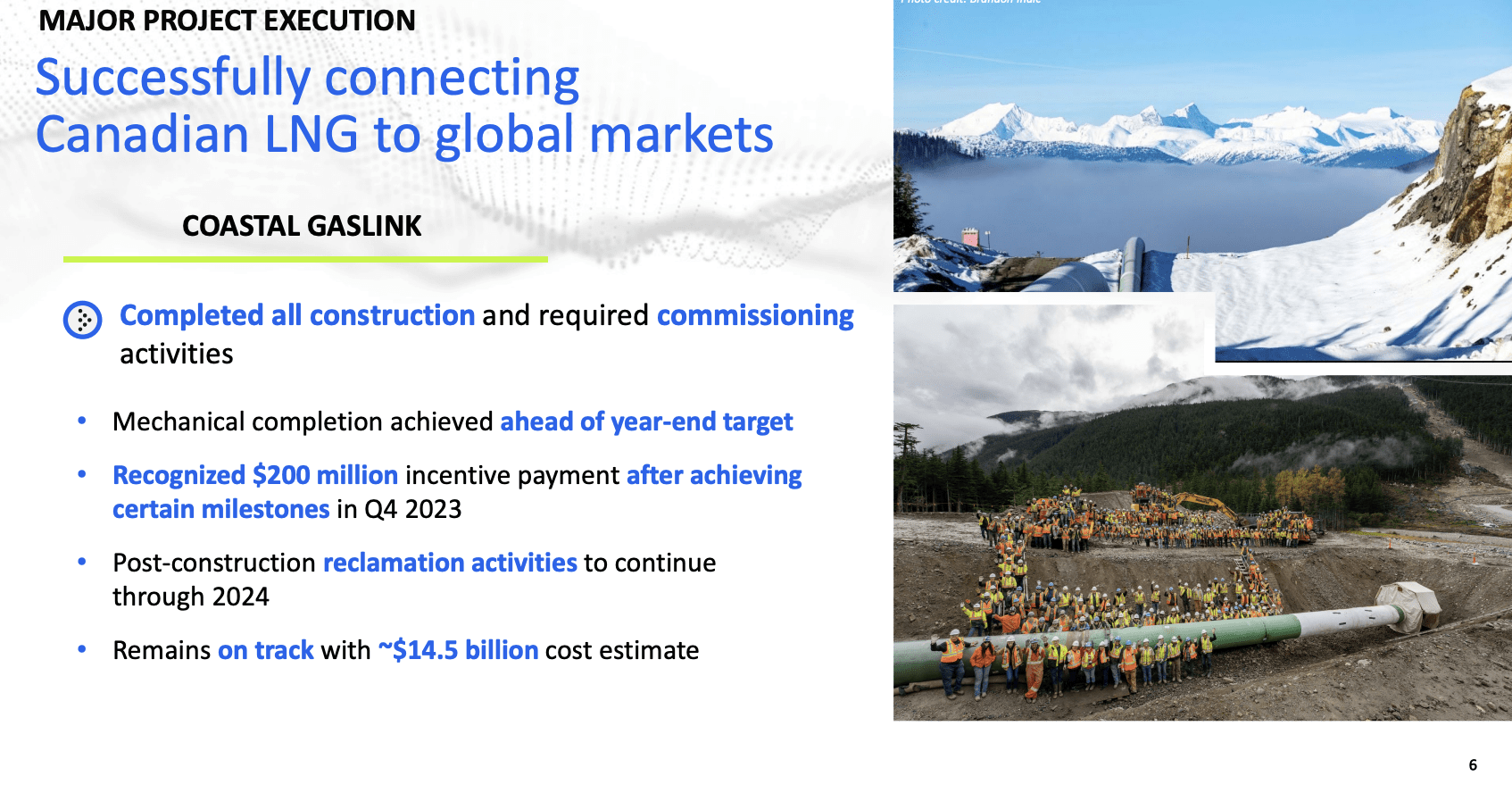

Moreover, while the company saw a $200 million tailwind from an incentive payment related to the Coastal GasLink projects, it still achieved 8% comparable EBITDA growth adjusted for that payment.

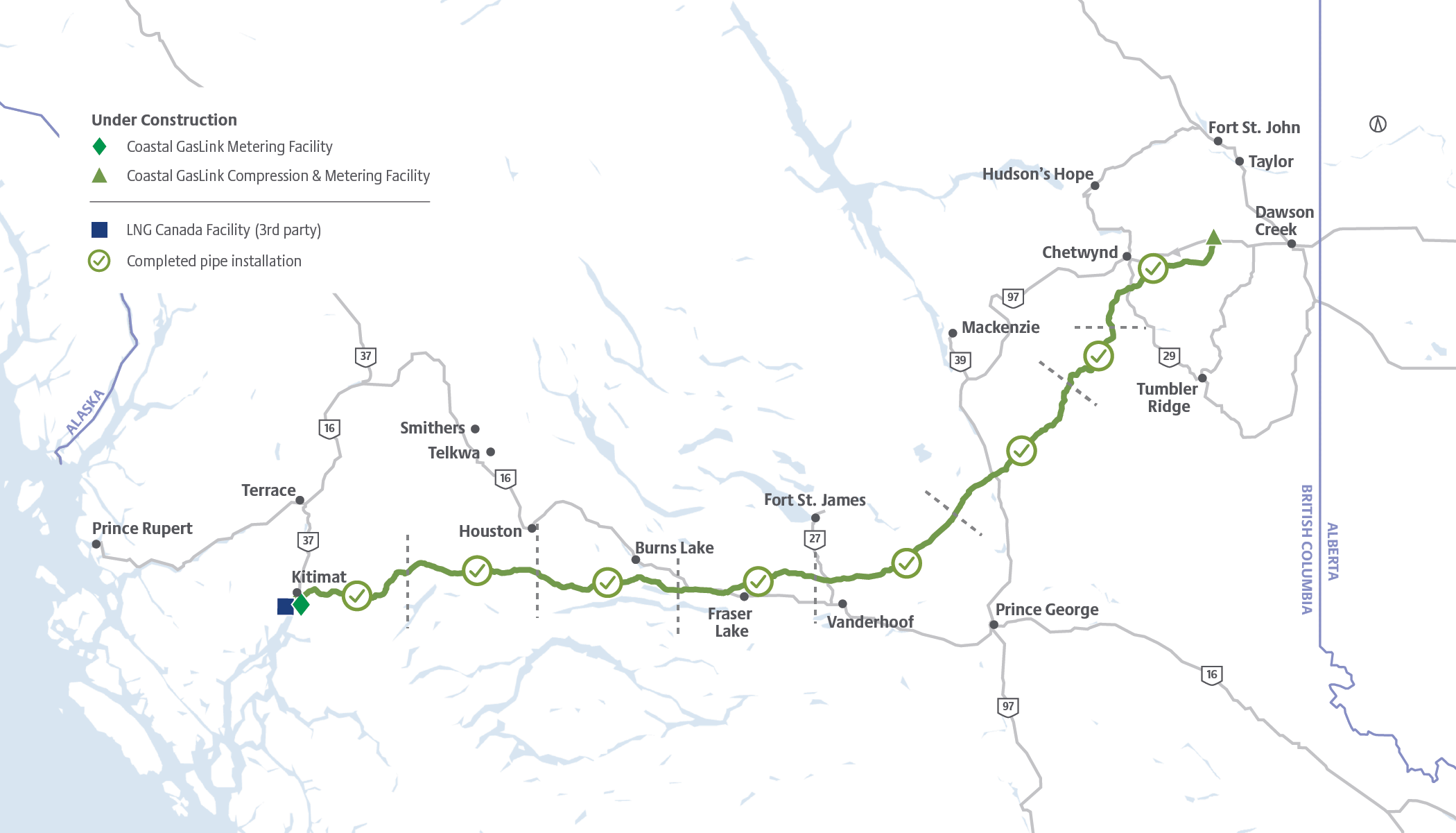

The Coastal GasLink project is one of Canada's most challenging pipeline projects, as it connects Canadian natural gas producers to export markets that serve Asian demand.

Coastal GasLink

It's a very important project in North America's push to become increasingly important in the global liquid natural gas ("LNG") market. Canada, which has massive natural gas reserves, is in a great spot to serve overseas demand.

This mega project completed all construction and required commissioning activities and is on track to stay within the latest $14.5 billion cost estimate.

TC Energy Corporation

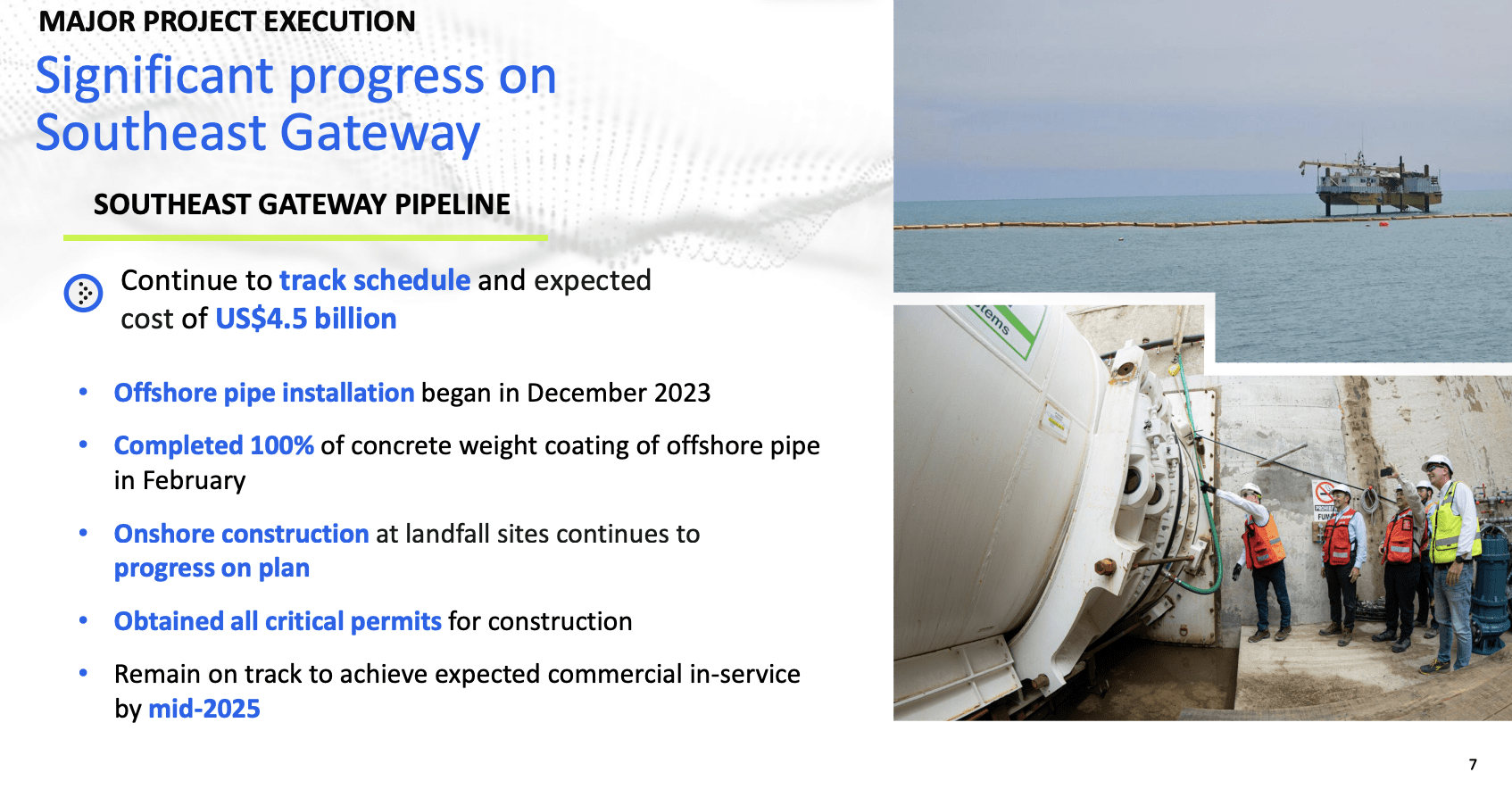

Further south, the company made progress on the Southeast Gateway project.

This is a project with Mexico's Federal Electricity Commission and consists of the construction of a natural gas marine pipeline connecting the supply from Tuxpan, Veracruz, to delivery points in Coatzacoalcos, Veracruz, and Paraíso, Tabasco.

According to TC Energy, the project remains on schedule and within the expected cost of $4.5 billion.

TC Energy Corporation

Going back to the performance of its existing assets, the aforementioned record EBITDA numbers were provided by record volumes and improving demand for services.

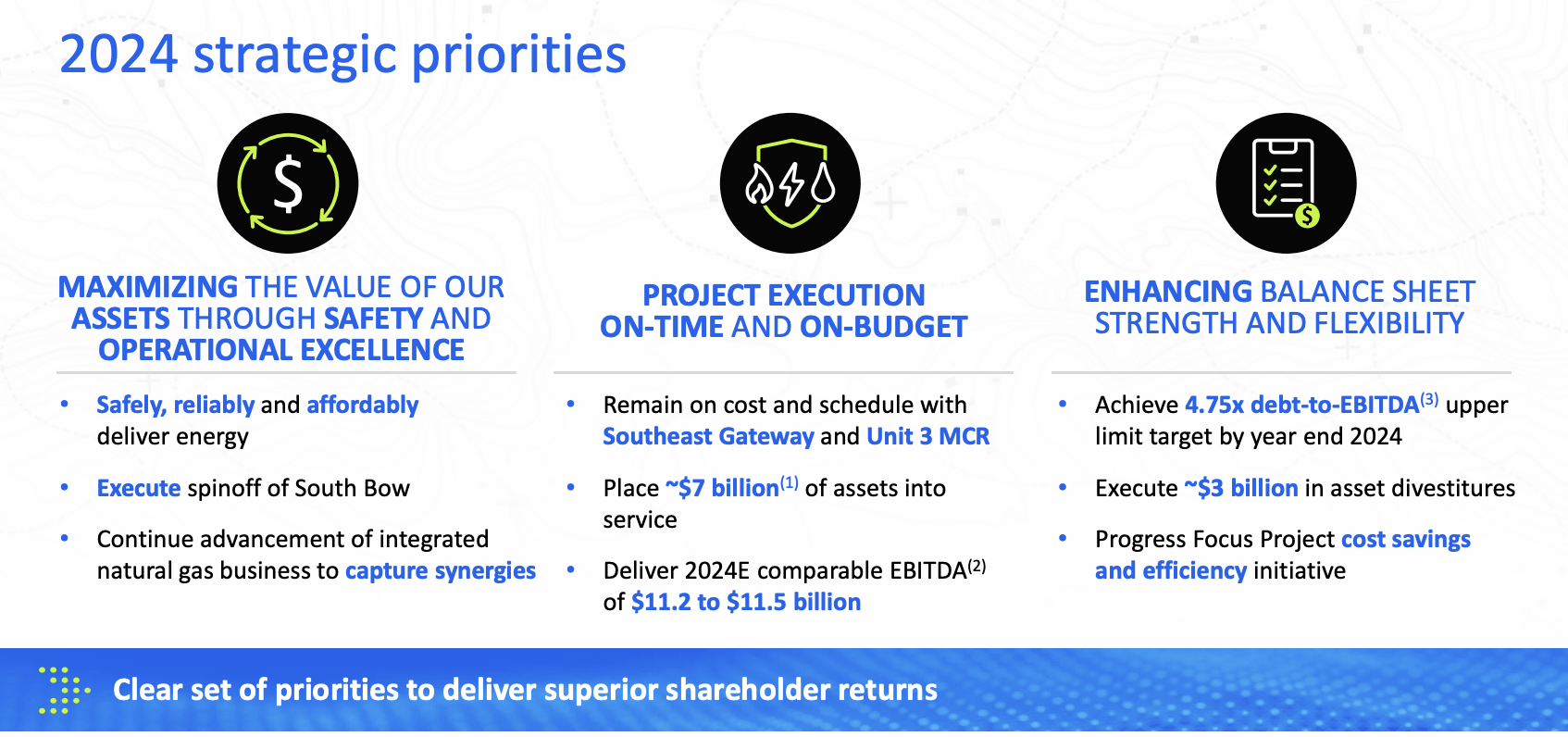

Before I elaborate on its financial improvements, I need to mention that the company is working on a spin-off. I mentioned this in my prior article as well.

Essentially, TC Energy is progressing with plans to spin off its liquids pipeline business into a standalone company. This would make TC Energy a natural gas midstream player.

The spin-off will be called South Bow. In Mid-2024, shareholders will vote on these spin-off plans.

TC Energy Corporation

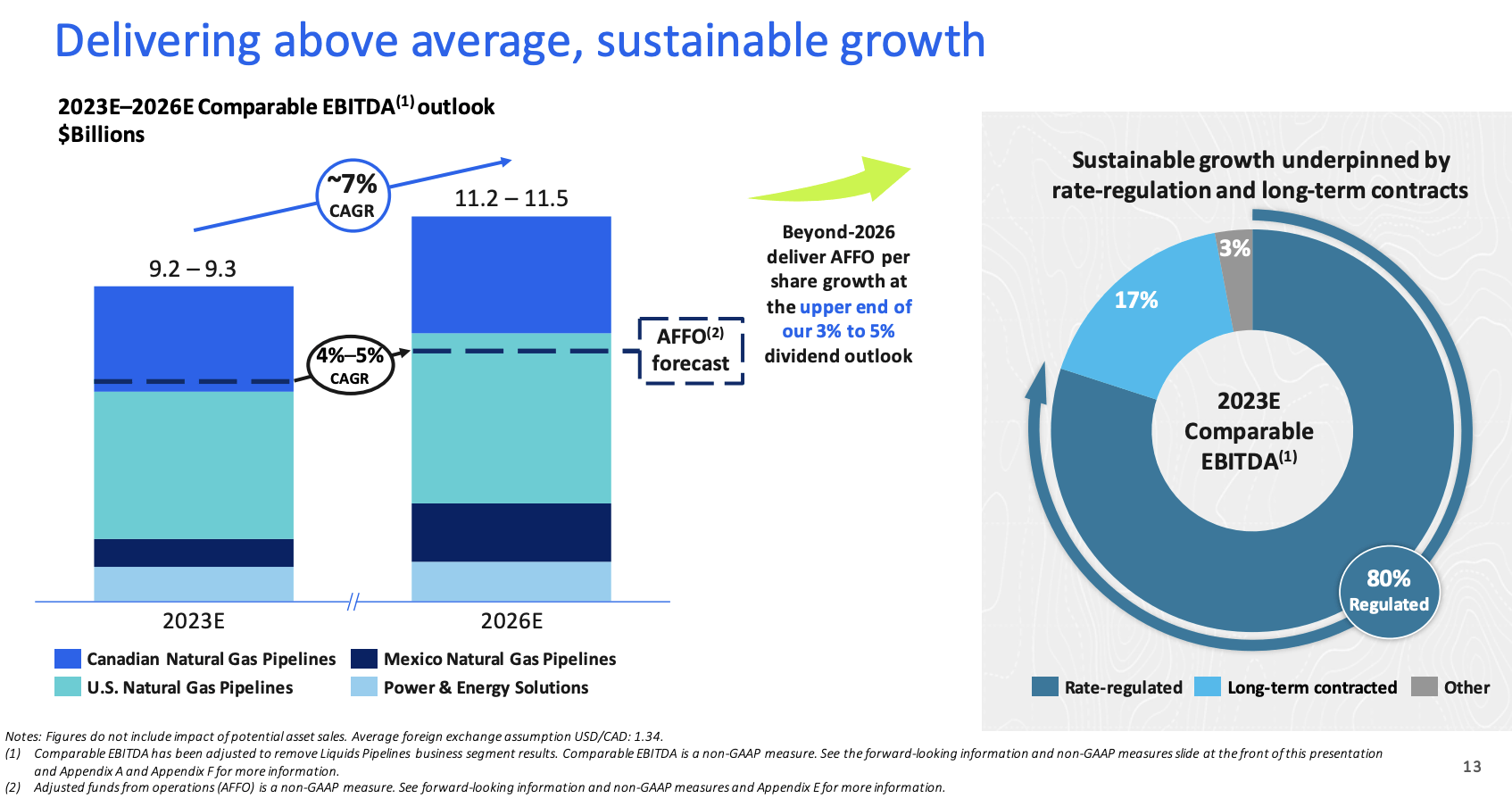

After spinning off South Bow, which is targeting long-term annual dividend growth of 2-3%, TC Energy will be a highly focused natural gas giant.

Elevated long-term growth is expected to be provided by a healthy mix of income from various regions and 80% regulated "utility-like" income. 97% of total growth is coming from regulated and long-term contracted operations, which adds a lot of safety.

TC Energy Corporation

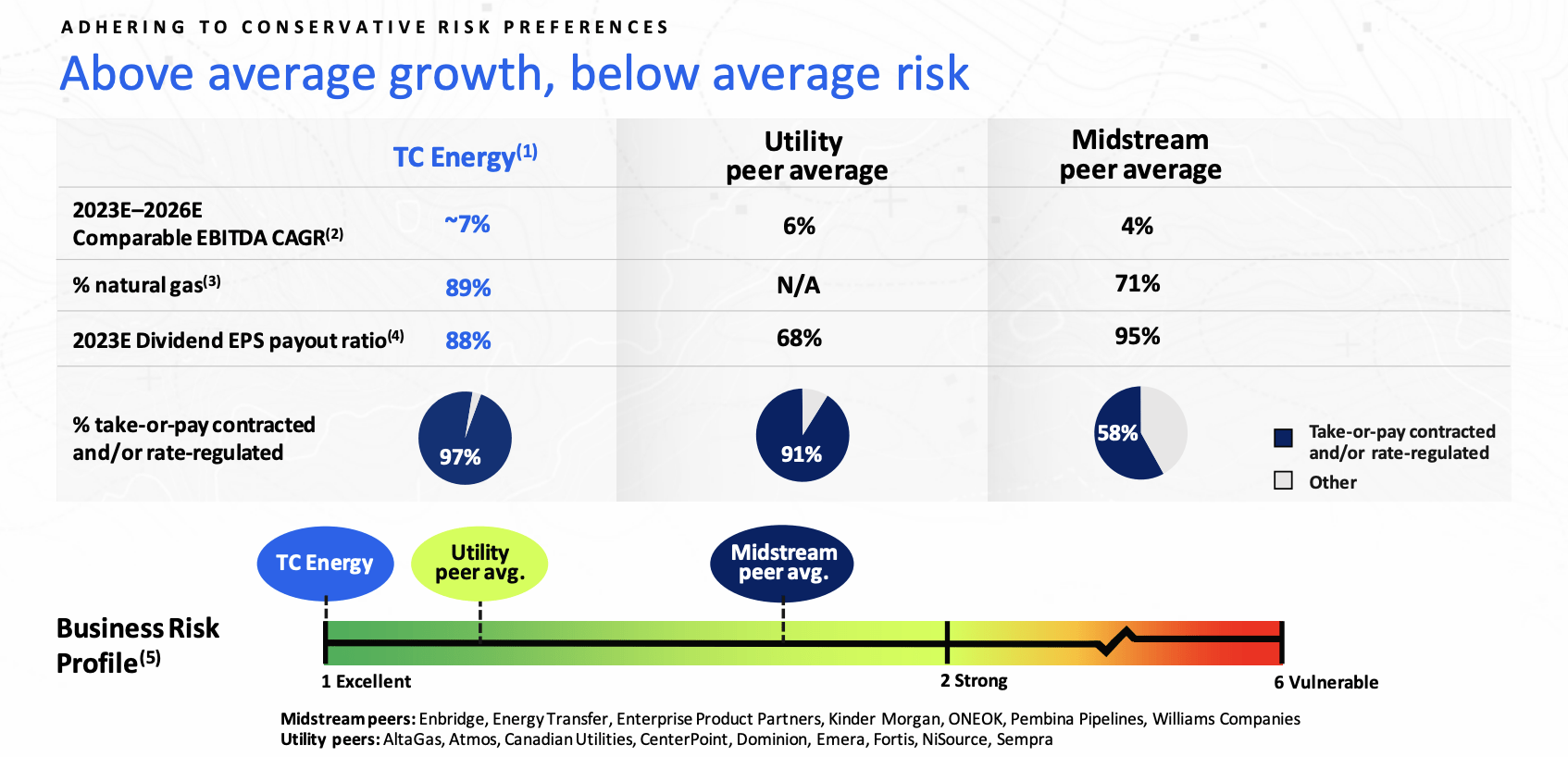

After the potential spin-off, the company is in a good spot to outperform both utilities and midstream companies when it comes to annual EBITDA growth, generate more of its income from natural gas, and have a greater take-or-pay/contracted share of its total income.

This provides it with a highly favorable risk profile.

TC Energy Corporation

In fact, the company's financials have been extremely resilient over the past two decades.

Although midstream operators are subject to throughput risks, they have limited pricing risk, which is why the company was able to grow EBITDA even when oil prices imploded in 2015 and when the pandemic hit in 2020.

After all, companies like TC Energy transport energy. They do not produce it.

TC Energy Corporation

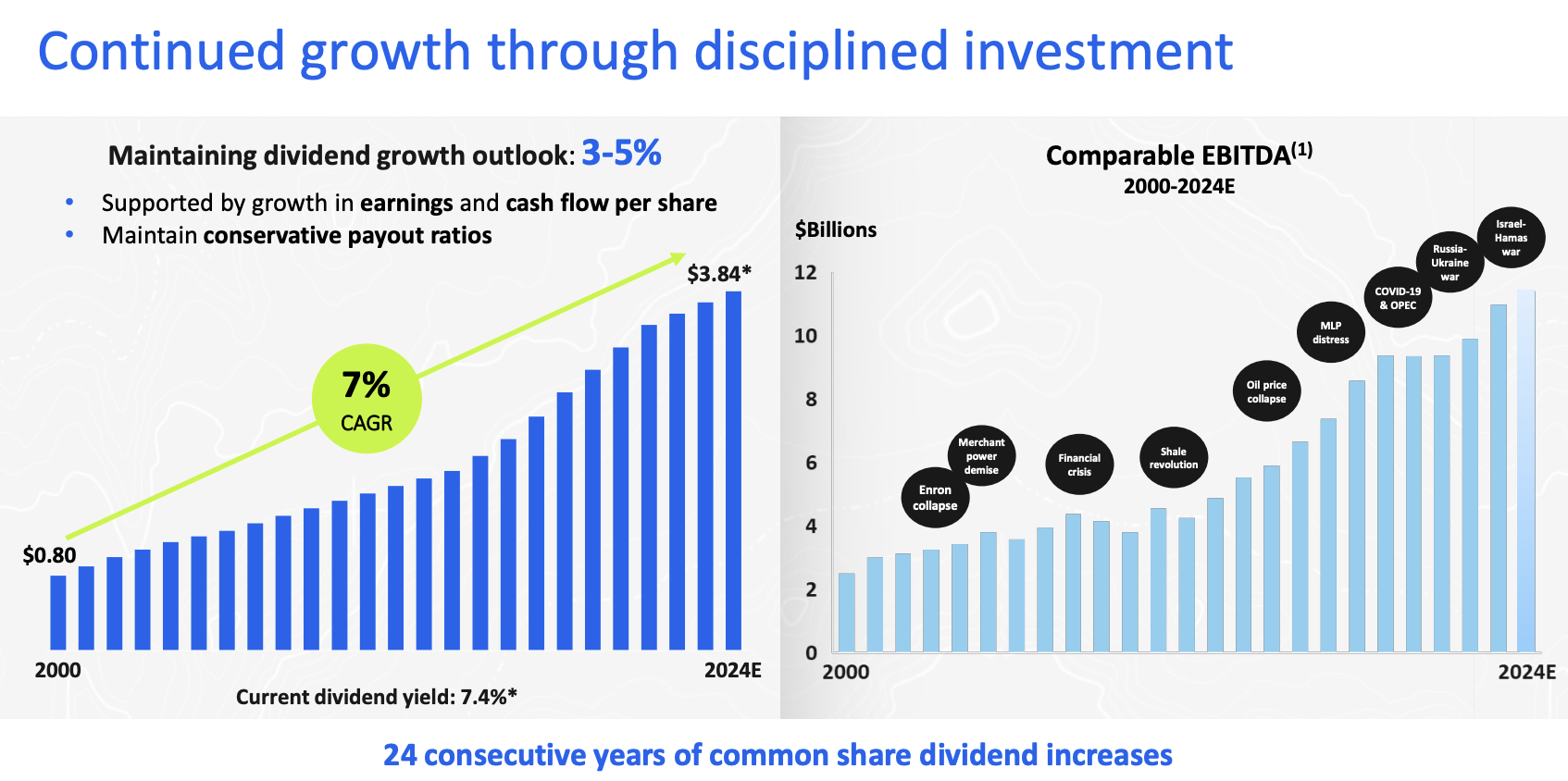

This also came with dividend stability.

As we can see above, the company's dividend has been hiked for 24 consecutive years. Going back to 2000, the dividend CAGR was 7%.

On February 16, the company hiked its dividend by 3.2% to $0.96. That's $3.84 per year and 7.0% of its stock price (the current yield).

Please be aware that the dividend is paid in Canadian dollars. In other words, while dividend growth may be consistent, non-Canadian owners are still subject to currency fluctuations.

As I already briefly mentioned, the dividend is expected to see 3-5% long-term annual growth.

Furthermore, the dividend is increasingly protected by healthy financials.

Moreover, a big part of debt reduction is the sale of assets. In 2023, the company exceeded its divestiture targets with the $5.3 billion monetization of 40% minority interest in Columbia Gas and Columbia Gulf.

It is now advancing roughly $3 billion of asset divestitures.

[...] our first priority is to achieve a minimum of $3 billion of divestitures and to do that by the end of the year. And while we're not going to undertake fire sales, if we see reasonable value today, we will transact on it. - TRP 4Q23 Earnings Call

The company also reaffirmed its 2024 EBITDA guidance between $11.2 billion to $11.5 billion.

TC Energy Corporation

So, what about its valuation?

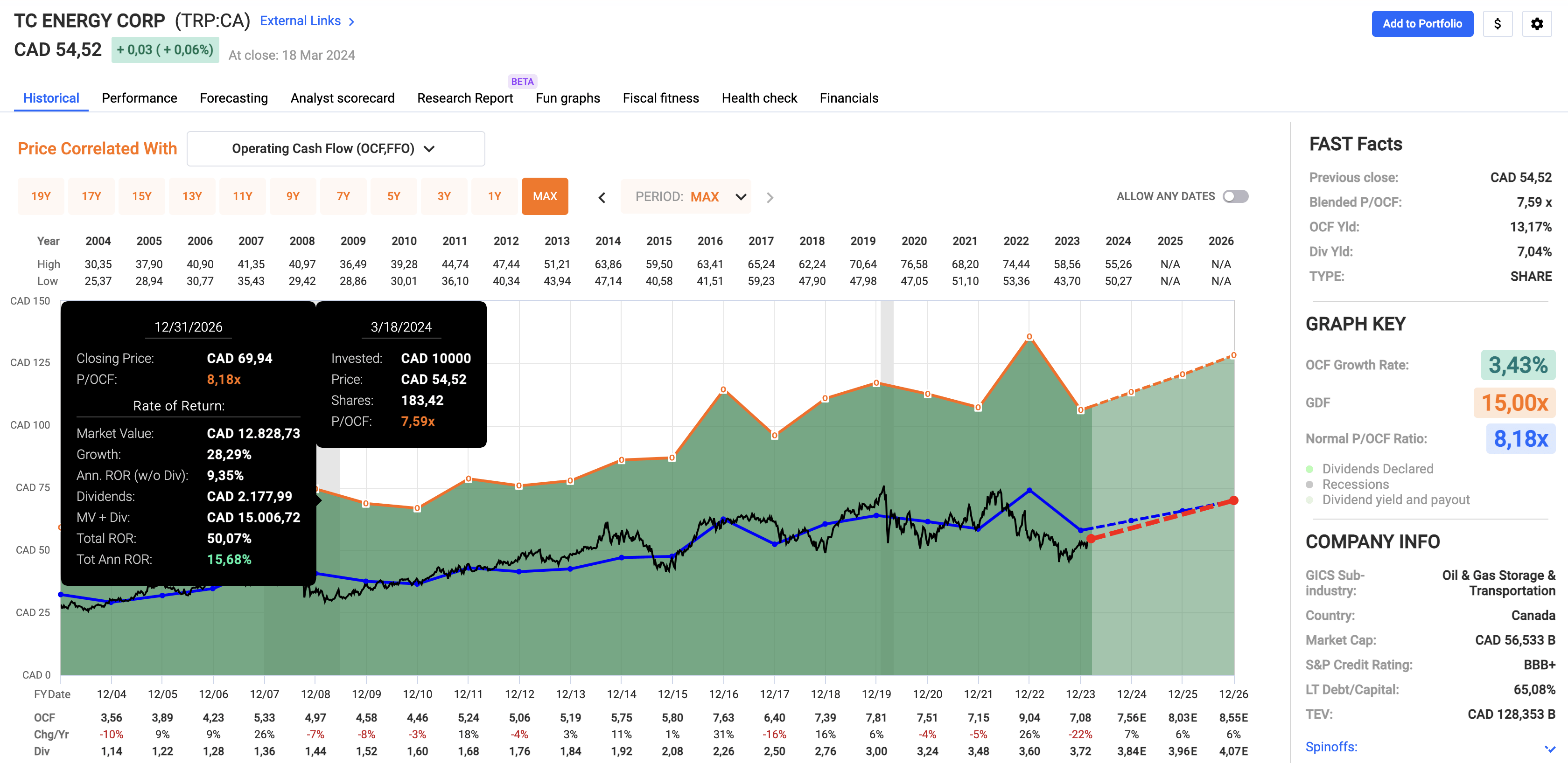

TCP is trading at a blended P/OCF (operating cash flow) ratio of 7.6x. That's below its long-term normalized P/OCF ratio of 8.2x.

This year, per-share OCF is expected to grow by 7%, potentially followed by 6% growth in both 2025 and 2026.

FAST Graphs

Combining 2026E per-share OCF estimates of $8.55 with an 8.2x OCF multiple, we get a "fair" price target of $70. That's 28% above the current price.

If we include the 7% yield, the company has an implied annual return of 14-15% through 2026.

However, this is subject to uncertainties, including economic growth, the company's success in selling assets, completing existing projects, and the interest environment, which impacts lending costs and investors' willingness to take risks.

If I didn't have so much energy exposure already, I would likely be a buyer of TRP, as I have started to really like the company since last year.

In a market where future returns are likely to be subdued, TC Energy stands out as a compelling income play.

With a strong dividend track record and a focus on resilient, contracted midstream operations, TRP offers stability and potential for long-term growth.

Meanwhile, the company's spin-off plans and commitment to debt reduction further enhance its value proposition.

Despite uncertainties, including economic factors like interest rate developments, TRP's attractive valuation and solid fundamentals make it an attractive opportunity for income-focused investors.

Pros:

Cons: