MarsBars

MarsBars

Those who have been through the dot com bubble and crash may be keen to see parallels between that and the current Al-frenzy that's gripped the market today, in which some investors are chasing growth at any cost. As such, it's probably a good idea to stay level-headed and focused on one's own investment objectives rather than give into FOMO and overpay for some stocks at nosebleed valuations, as those who have been through these cycles know how they usually end.

That's why I continue to see value in REITs, especially in this current market, where income stocks are clearly out of favor. This brings me to Terreno Realty (NYSE:TRNO), which I last covered in October last year, noting its undervaluation and in-demand properties.

It appears that the market has agreed with my thesis, as the stock has given investors a 19% total return since then, nearly matching the 20% rise in the S&P 500 (SPY) over the same timeframe. In this article, I revisit the stock with key updates around its business fundamentals and valuation, and discuss whether if TRNO remains a good buy at present, so let's get started!

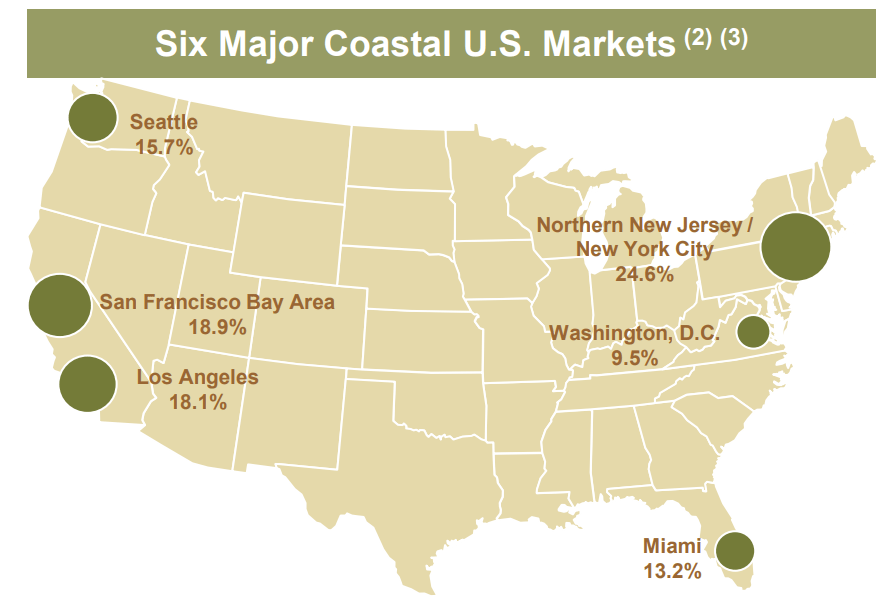

Terreno Realty is a moat-worthy U.S. Industrial REIT with presence in 6 major coastal markets, which are Seattle, SF Bay Area, Los Angeles, NYC Region, Washington D.C. and Miami. At present, it has 259 buildings covering 16 million square feet.

Investor Presentation

What makes Terreno an appealing company is its strong operating dynamics due to its presence in supply-constrained markets with no speculative development nor complex joint ventures, with focus on acquiring properties at a discount to replacement cost, giving TRNO a margin of safety.

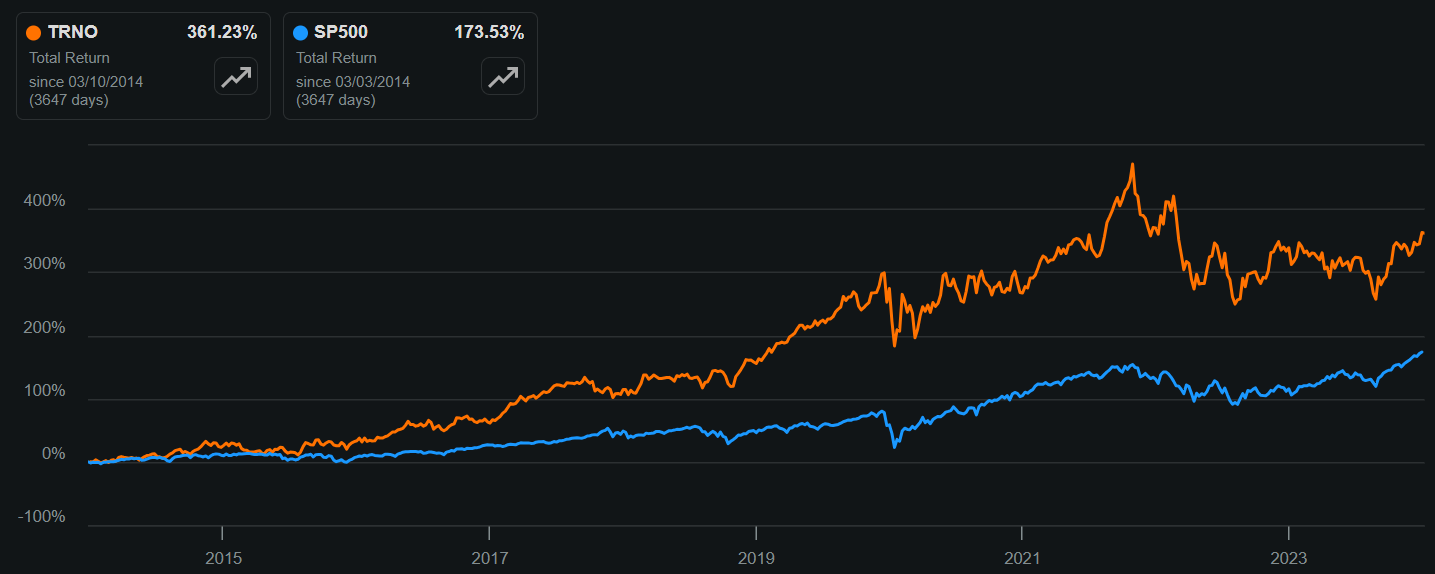

Moreover, its assets make for mission-critical last-mile distribution in strong demand centers with high population densities with high volume distributions points. The quality of TRNO's properties is reflected by average annual 11.3% cash same-store NOI growth since IPO, and TRNO has realized positive returns on 33 sold properties since IPO at a 12.9% unleveraged annual internal rate of return. As shown below, TRNO has delivered a 361% total return over the past decade, far surpassing the 174% of the S&P 500 (SPY)

TRNO vs. SPY 10-Yr Total Return (Seeking Alpha)

TRNO posted its Q4 results on February 7th, with key takeaways that continued strong demand for its properties as reflected by cash rental growth and occupancy that's remained high. This is reflected by the blended cash rental spread of 47.5% during Q4 on new and renewal leases. Tenant retention was also strong at 75.6%, and portfolio occupancy at the end of Q4 remained high at 98.5%, which is 20 basis points higher on a sequential quarter-on-quarter basis and just 10 bps below where it was in the prior year period.

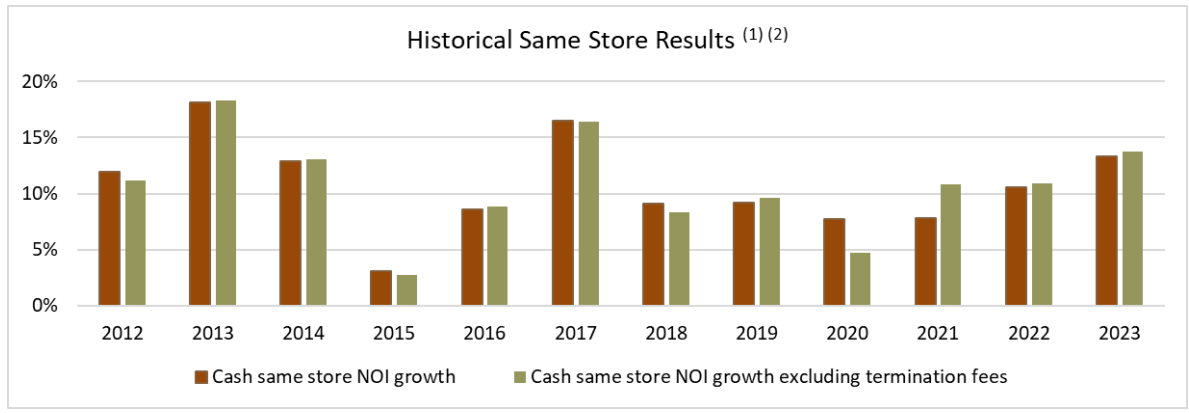

This continues TRNO's track record of growth in recent years. As shown below, TRNO's Cash SSNOI (same-store NOI) growth has been in the high single-digit to double-digits since 2016, with growth accelerating since the start of the pandemic in 2020. For the full-year 2023, TRNO's SSNOI and SSNOI excluding termination fees were 13.3% and 13.7%, respectively.

Investor Presentation

Looking ahead, I would expect for TRNO to pursue accretive growth opportunities, as it raised $315 million in equity capital during 2023, with around half of that ($158 million) coming from equity raised in the fourth quarter. TRNO could also be raising equity capital in the current quarter, since the share price currently trades at around a P/FFO of 27x, equating to a 3.7% cost of equity capital. This compares favorably to TRNO's acquisitions over the past year, which have trended at or above 5%.

Over the next few quarters, I would look for whether if TRNO is able to maintain acquisition cap rates at 5% or above stabilized yields, which would be a signal that management is able to continue to source properties at attractive cap rates. In addition, I would look for value-add opportunities stemming from roof-top solar, as it represents another monetization avenue for TRNO's industrial properties. This represents an incremental growth opportunity for TRNO, as noted by management in the recent earnings presentation:

[We] entered agreements to host rooftop solar projects in our Washington, D.C., Los Angeles, and Northern New Jersey/New York markets. The Company expects a portion of these projects to become operational starting in 2024 as part of Terreno Realty Corporation’s sustainability goal of rooftop solar on at least 5% of total rooftop area by year-end 2024, up from 1% today

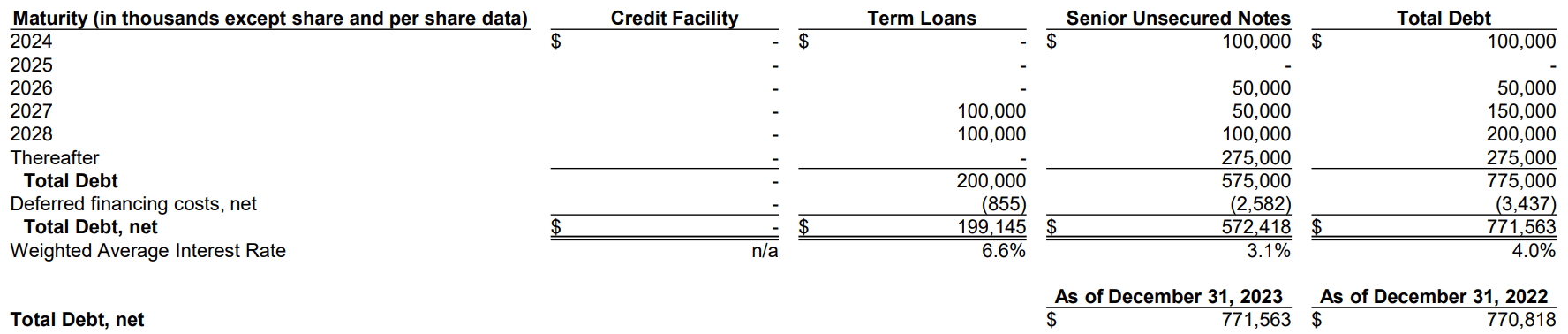

Meanwhile, TRNO is supported by one of the strongest balance sheets among REITs, with a net debt to EBITDA ratio of just 2.6x, sitting well below the 6.0x level generally considered to be safe by ratings agencies, and below 3.6x from the end of 2022. TRNO also has very high interest and fixed charge coverage ratios of 9.1x and 6.8x, respectively and has plenty of liquidity with $165 million in cash on hand and $400 million in undrawn capacity on its revolving credit facility.

TRNO's high liquidity goes a long way in covering its debt maturities, with just $100 million in debt maturing this year and no debt maturities in 2025, as shown below.

Investor Presentation

Risks to TRNO include potential for an economic slowdown, which could reduce tenant demand and cash spreads on new and renewal leases. In addition, TRNO's high exposure to coastal markets makes it vulnerable to geopolitical tensions as it relates to tariffs on imports, which could reduce international shipping traffic into coastal port cities and result in lower demand. Moreover, increased competition for properties from the likes of Prologis (PLD) or Rexford Industrial (REXR) could result in cap rate compression and lower external growth potential for TRNO.

Importantly for income investors, TRNO currently pays a 2.8% dividend yield that's covered by a 77% payout ratio. It also comes with 10 years of consecutive growth and a 5-year dividend CAGR of 18.5%.

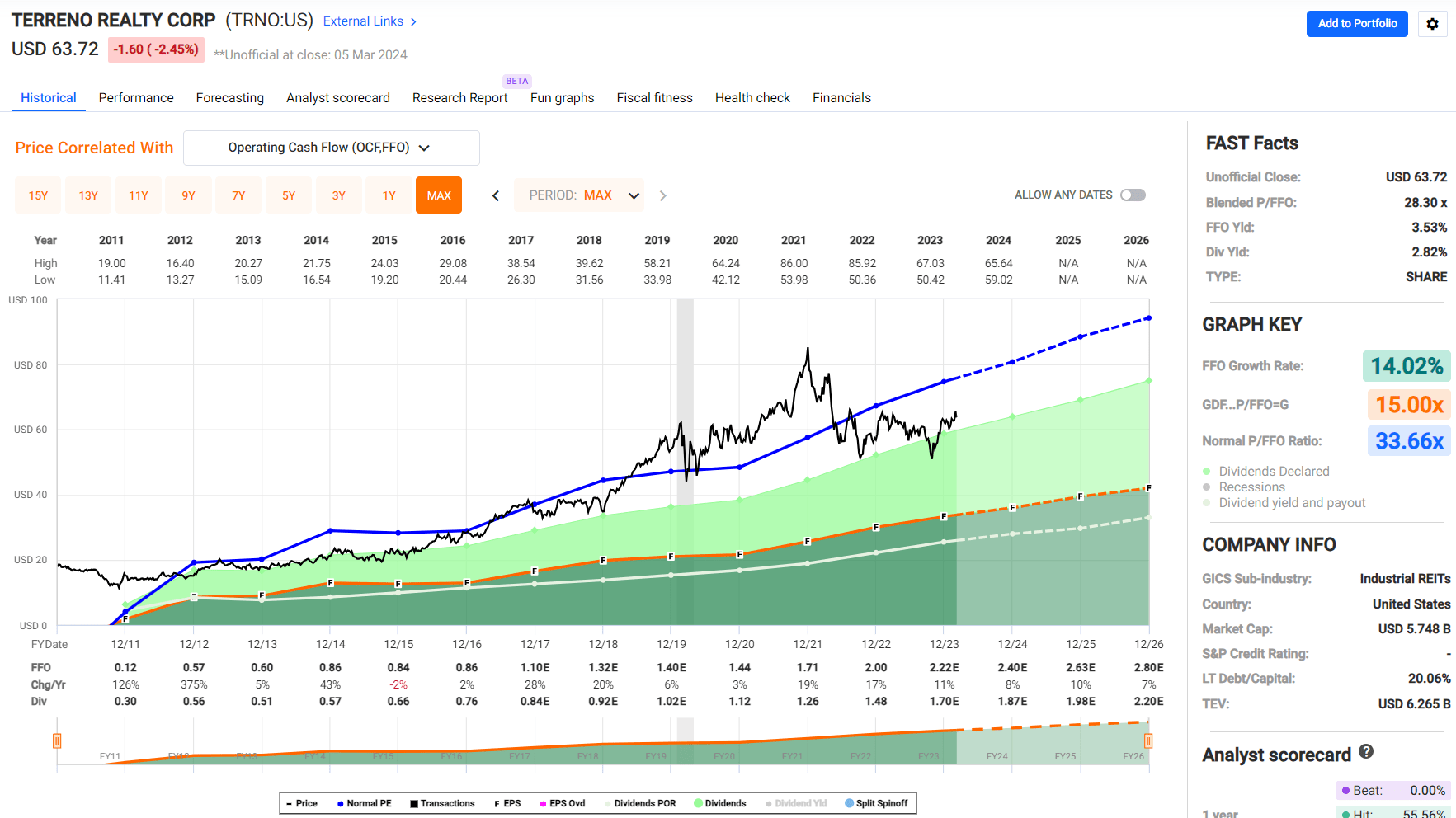

Turning to valuation, TRNO is admittedly no longer the bargain that it was when I last visited the stock at the current price of $63.72 with a forward P/FFO of 26.6. However, it does still trade at a discount to its normal P/FFO of 33.7, as shown below.

FAST Graphs

Nonetheless, I view TRNO as being more than fully valued at its current price, with the expectation that it can achieve an FFO/share growth rate in the 10% range, which matches the growth rate it achieved last year and with support from continued expectations of favorable cash lease spreads this year. At this growth rate, I would be more interested in TRNO at a P/FFO in the 20-24x range.

By comparison, TRNO is also pricier than its other high-quality counterparts Prologis and Rexford, which currently carry forward P/FFOs of 24.1x and 22.0x, respectively. These peers also carry a strong presence in supply constrained Tier 1 markets and have forward FFO/share growth estimates by analysts that are the same or higher than that of TRNO.

Overall, I believe that TRNO represents a solid candidate for long-term investment in the industrial real estate space, with its high-quality portfolio and strong balance sheet. It continues to see impressive cash rental spreads and same-store NOI growth, as well as incremental value-add opportunities. However, at its current valuation, there may be better opportunities to invest in other industrial REITs with similar growth prospects and presence in supply constrained markets. As such, investors may want to wait for a more attractive entry point before considering TRNO, and I'm downgrading TRNO from a 'Buy' to 'Hold' based on valuation.