bugto/Moment via Getty Images

bugto/Moment via Getty Images

Global growth trends for 2024 are already on the rise. Improved macro data out of the U.S. and Europe have led to forecasters rethinking this year’s rate of worldwide economic expansion. That’s generally a boon to cyclical companies that depend on high demand for oil and other commodities. But with a normalizing oil and transport market, there is the risk that profits in the tanker and marine exhaust markets may retreat. Still, renewed geopolitical tensions in the Middle East add a twist to this volatile niche of the Energy sector.

I reiterate my hold rating on TORM plc (NASDAQ:TRMD). The valuation appears fair to me, while the technicals are mixed. In my previous analysis, I gave a bit too much credence to the chart, looking too far past its solid valuation in Q3 2023.

Goldman Sachs

According to Seeking Alpha, TRMD operates as a shipping company, and it engages in the transportation of refined oil products and crude oil worldwide. It operates in two operating segments, Tanker and Marine Exhaust. The company transports gasoline, jet fuel, naphtha, and gas oil, as well as dirty petroleum products, such as fuel oil. It also engages in developing and producing advanced and green marine equipment.

The $3.1 billion market cap Oil and Gas Storage and Transportation stock features high volatility. Data from Option Research & Technology Services (ORATS) shows that share-price implied volatility is above 45% with Q4 earnings unconfirmed to take place on March 7, according to Seeking Alpha. Analysts currently forecast $1.94 of operating EPS, compared to $1.80 reported in the same period a year ago.

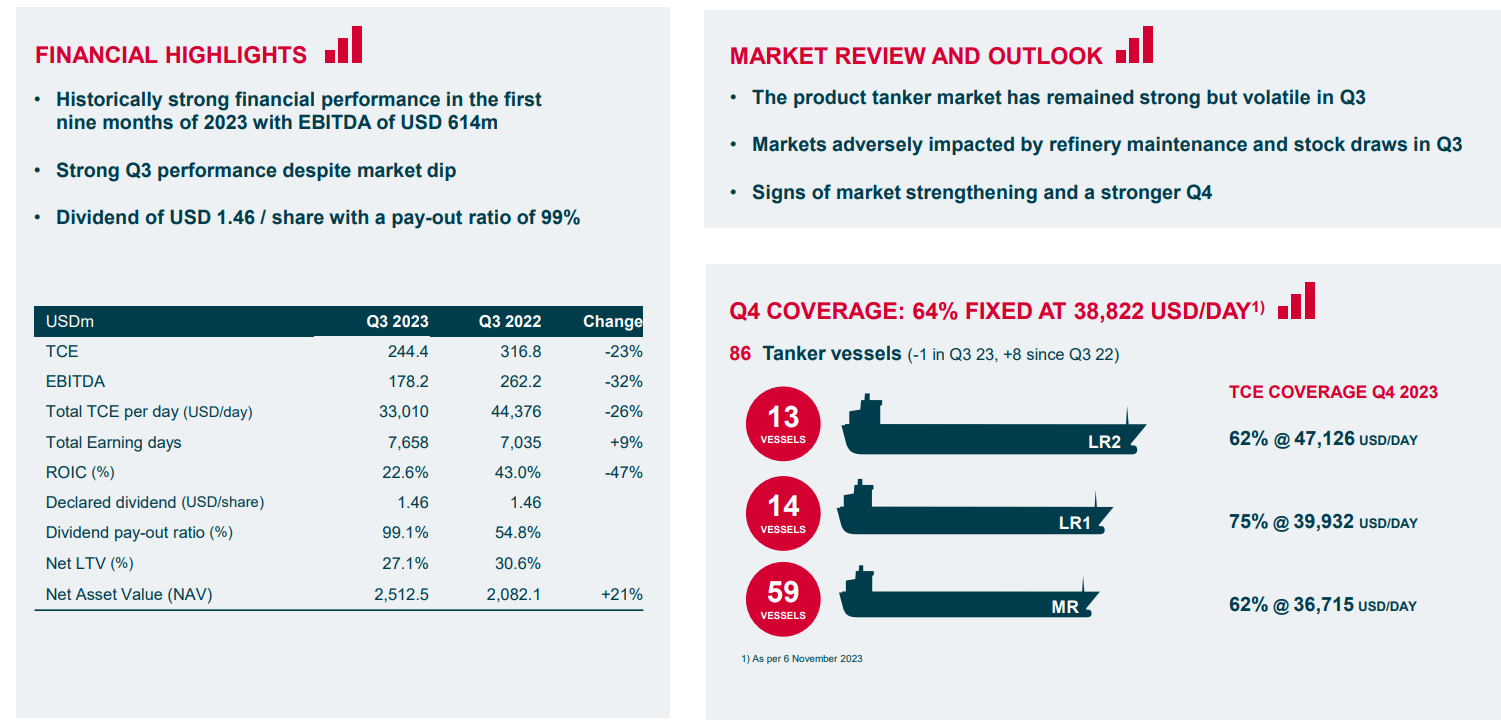

Last go-round, TRMD reported a solid quarter despite tougher industry conditions. Time Charter Equivalent (TCE) revenue verified at $244.4, a 23% decrease from $317 million earned in Q3 2022 while its return on invested capital plunged from 43% to just 22.6%. The management team remained committed to paying out a high dividend – the payout ratio was 99% - I would like to see improved earnings metrics so that free cash flow sustains in the years ahead. Overall, its net asset value rose 21% to $2.513 billion. On the call, TORM cited a more volatile third-quarter operating environment with refinery maintenance and stock draws impacting results, though management was optimistic about a better Q4.

TORM IR

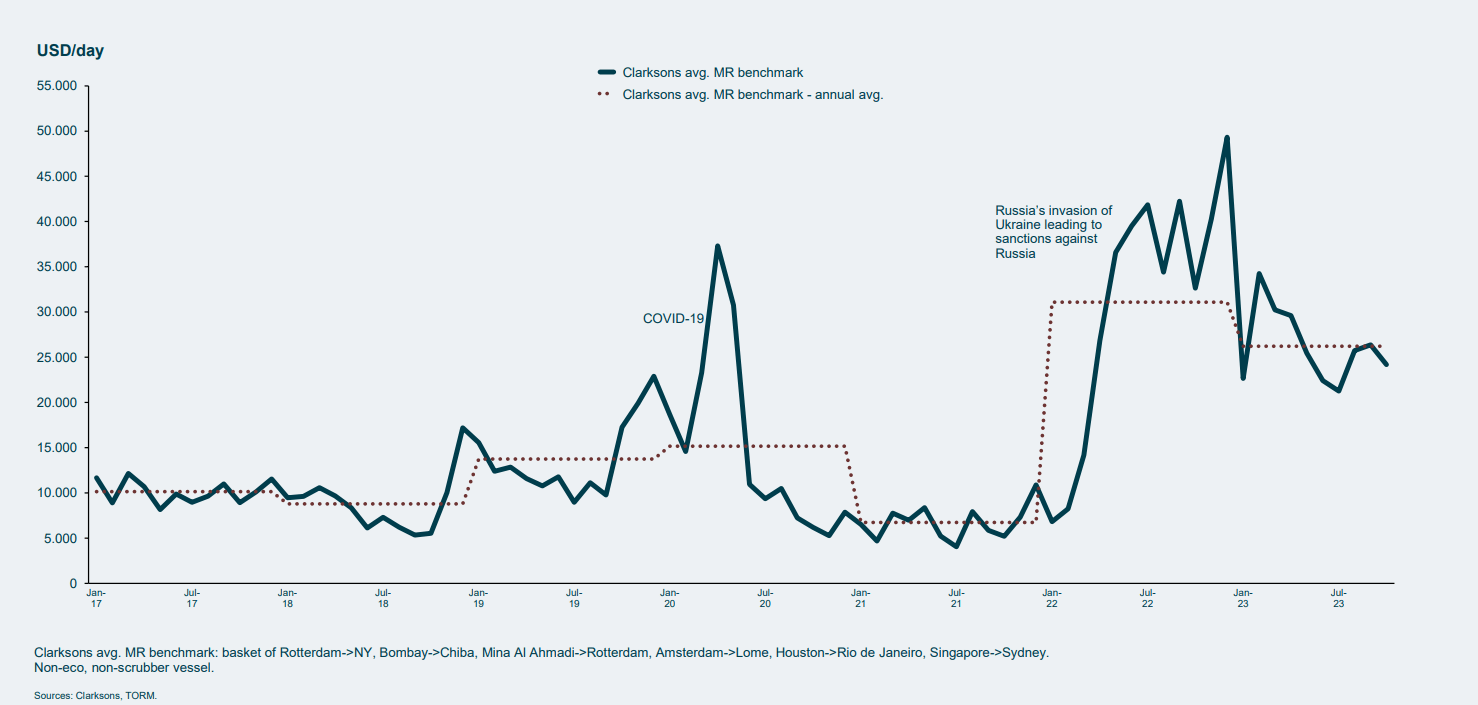

Geopolitical tensions indeed resulted in much higher tanker rates through 2022 and the first portion of last year, but key industry benchmark rates are normalizing, though still at elevated levels. The rates are high enough, in fact, that TORM’s Board of Directors approved a dividend of $1.46 per share based on a strong balance sheet – the payout came from operating cash flow, too. Moreover, the company has been active in optimizing its fleet, acquiring 10 vessels and divesting 4 in the first nine months of last year, which should help support EPS growth in the years ahead, though the revenue outlook is currently unappealing according to the consensus forecast.

But the firm expects continued support for the product tanker market, with positive demand and supply drivers, trade recalibration benefits, and refinery dislocation. A key risk is how interest rates evolve as TORM acquires new vessels through financing, though there was confidence that its current leverage level is appropriate. Of course, ebbs in the global macro growth trajectory are also important to monitor.

TORM IR

On valuation, analysts see $7.37 of operating EPS this year, with its top-line dropping from $1.37 billion in 2023 to perhaps just $1.0 billion in the out year as the industry reverts from an abnormally strong period. If we assume $5.50 of normalized EPS and apply a 7 forward P/E, then the stock should be in the mid to high $30s, not far from where it trades today, and a slight increase from my previous analysis given the decent quarterly results. Bear in mind that TORM has historically traded at just a 5.5 forward non-GAAP earnings multiple.

Seeking Alpha

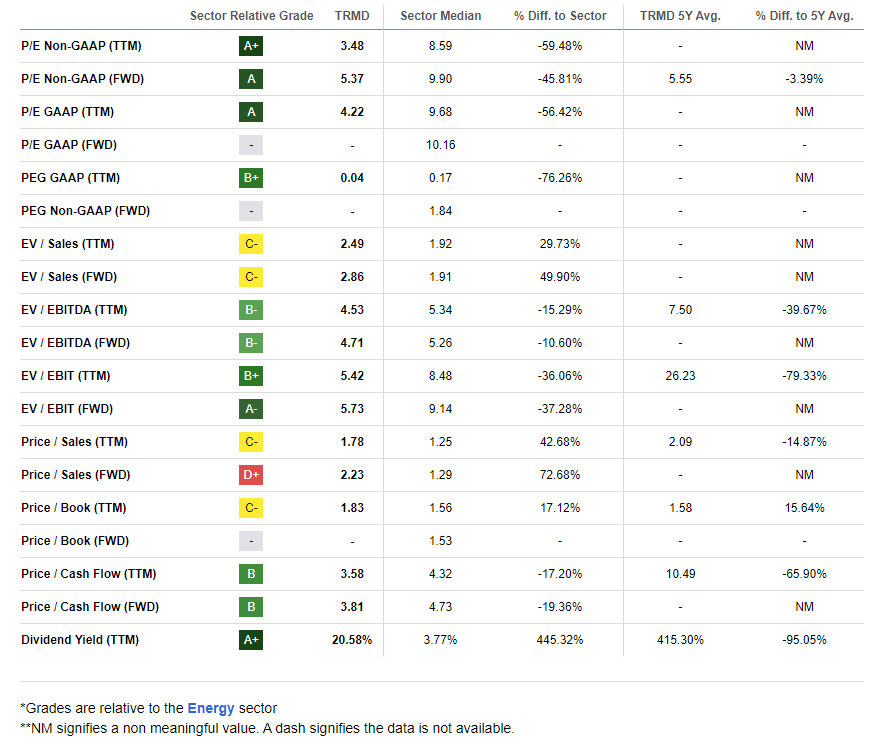

Compared to its peers, TRMD features an attractive valuation grade, though I would note that some of its primary competitors have mid-single digit P/Es, so low valuations are to be expected. Still, the company has been on a solid growth trajectory, but I have questions about how sustainable recent per-share profits have been. The company earned $1.64 in operating EPS pre-pandemic (2019), for perspective.

Current free cash flow per share is very high at $5.87 on a trailing basis while share-price momentum has greatly improved, though I will note key price points that could give the bulls fits later in the article. I also took a look at Seeking Alpha’s new seasonality tool, and it shows a very bullish stretch on the horizon from February through May that near-term investors should weigh. Finally, EPS revisions appear to be poor, but there has been just a single EPS downgrade in the last three months, so take that with a grain of salt.

Seeking Alpha

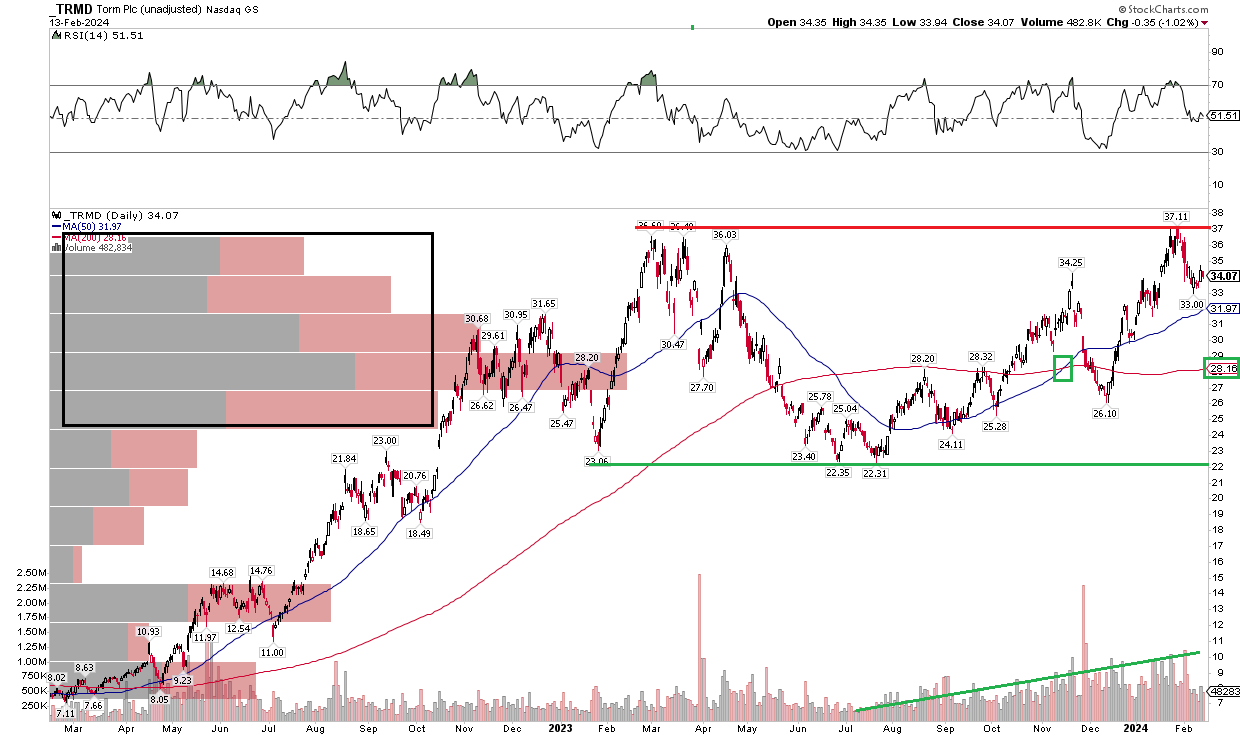

With a neutral valuation, solid current earnings and free cash flow, along with positive seasonal trends, TRMD’s chart may take a breather after a stellar advance. Notice in the graph below that shares approached their previous all-time high from 2023 around the $37 mark. A pullback is currently underway, though the trend is clearly higher from the $22 double-bottom low notched in June and July last year. Moreover, there was a bullish golden cross pattern in which the shorter-term 50-day moving average rose above the longer-term 200dma last November. While shares dipped in December, no major damage was done, and volume was strong as TRMD surged 40% to its recent peak. Still, the 200dma is flat in its slope, and shares have not yet broken out to new highs.

If we do see a breakout, however, then I project an upside measured move price objective to $52 based on the $15 consolidate range the stock is currently in ($37 at the high, $22 at the low, added on top of the $37 all-time high). So, as we approach May earnings, be on the lookout for this possible strong move. Until it breaks out technically, shares are a hold.

Overall, TRMD continues to consolidate under its highs, but a bullish technical rally could be in the works above $37.

Stockcharts.com

I reiterate my hold rating on TORM plc. Shares now appear near fair value, while the chart asserts that a significant gain could be in play if we see a continued high-volume price advance through $37.