Eugene Mymrin/Moment via Getty Images

Eugene Mymrin/Moment via Getty Images

Following my coverage on Trimble (NASDAQ:TRMB), which I recommended a buy rating due to my expectation that the business was set to ride on the digital transformation secular tailwind in its end markets, and as the transition to software and subscription continues, the business would also become a less cyclical business, this post is to provide an update on my thoughts on the business and stock. I am reiterating my buy recommendation, as I believe TRMB is going to see a recovery in earnings over the next few years if the catalysts that I identified play out as expected. When that happens, I also expect valuation to trade at a premium to the market price in the positive fundamental outlook.

It has been a full year since I wrote about TRMB, and in hindsight, my buy rating was not the right call as the stock went on to see continuous decline, dropping to as low as $39.57 at one point last November. However, I think the worst seems to be over as the fundamentals and outlook have improved.

Recapping the recent 4Q23 results, at the bottom line, TRMB reported an adj EPS of $0.63, touching the higher end of guidance ($0.55 to $0.63) and beating the consensus estimate of $0.60. Revenue was up 9% to $932 million, which came just a touch above the high end of guidance ($890-$930 million) and also beat the consensus estimate for $910 million. ARR also grew in similar directions, up 24% on a reported basis and 13% on an organic basis to $1.98 billion. Adj EBIT margin continues to show expansion, improving by 240bps vs. 4Q22 to 24.3% in 4Q23, which ended FY23 with 24.6% adj EBIT margin vs. FY22 of 22.9%. Guiding for FY24, management expects FY24 adj EPS of $2.60–2.80, revenue of $3.57–3.67 billion, and adj EBIT margin in the range of 24-25%. This set of guidelines implies ~2% growth in EPS, ~4.5% decline in revenue at the midpoint, and maintaining sustainability at the current level.

Own calculation

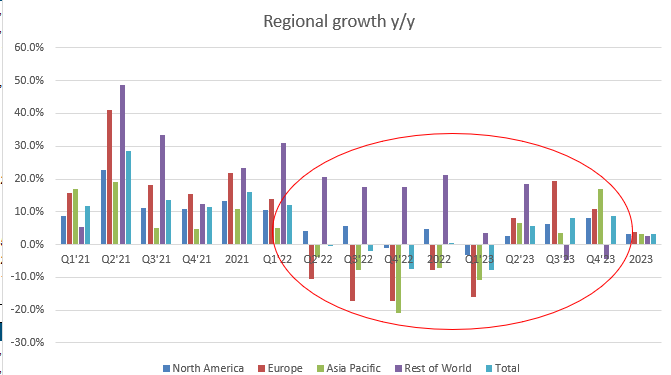

I believe management guidance is pointing to the start of a recovery cycle, which performance at underlying regions seems to be pointing to as well. Growth has recovered across all regions except the rest of the world from the softness seen in FY22. In 4Q23, North America (the largest region for TRMB) grew 8.2%, Europe grew 10.8%, and APAC grew 16.9%, while the rest of the world fell by 4.4%. The rest of the world's performance is relatively less meaningful, as it represents less than 10% of total revenue. When viewed from the end market perspective, it appears to me that demand is strong but held down by a couple of end markets that are largely dragged down by macro pressures rather than anything structural. TRMB continues to enjoy tailwinds in the construction end markets with AECO (architects, engineers, contractors, and owners). Organic ARR was up by ~20% in 4Q23. Notably, a large part of AECO booking growth is achieved through cross-selling, which now accounts for more than 25% of the annual contract value. This tells us two important things. First, the TRMB change in go-to-market strategy to adopt a more direct market approach has worked out very well, which is a plus for management’s ability to execute. Secondly, this also tells us that the underlying demand remains healthy (i.e., underlying customers are willing to adopt more products). Similar strength was seen in subsegments such as infrastructure, renewables, and data centers, which drove booking growth. Revenues from connected digital platforms also performed well, now representing ~15% of FY23 revenue. With the addition of more businesses like e-Builder and Cityworks, as well as the expansion of AECO initiatives to other regions, management anticipates this to reach approximately 35% by the beginning of 2024. Although this is below management guidance back during the investor day, it is still decent progress. As TRMB shifts towards it digital platform, it should open up more opportunities to cross-sell.

The few end markets that are dragging down TRMB performance due to the weak macroeconomic situation are residential construction and agriculture. For residential construction, the impact was particularly profound in Europe as mortgage rates and house prices remain high, causing demand to plummet. On this end, this is largely a macro problem rather than a TRMB-only problem. TRMB is not the only business that is being impacted by this. My view is that rates have to come down eventually, and the impact of rate increases has so far shown positive results with inflation coming down. While it might take some more time, the direction is positive for TRMB, which I expect to show up sometime in FY25. As for agriculture, it also suffered the same fate, where high commodity prices (as noted by management) continue to impact the sector. I am not an expert on commodities, but I think a key reason for the elevated commodity prices is the freight situation (note that this also impacts the TRMB transportation end market), led by the conflict in the Red Sea. That is outside of TRMB's ability to govern, but my bet is that it will be resolved soon, given the pressure from the US and its allies.

An upcoming catalyst that I expect to improve TRMB fundamentals and valuation is the joint venture [JV] between AGCO Corp. (AGCO) and TRMB. The proposed JV is to combine AGCO’s JCA Technologies assets with TRMB’s precision agriculture business (excluding its core GNSS IP). In the JV, AGCO will hold 85% of the interest, while TRMB will hold the remaining 15% and receive a cash consideration of $2 billion from AGCO. The transaction is expected to close in 1H24. I see this as a major win for TRMB, as it would be able to exit the hardware-centric precision agriculture business that is competing against the OEMs. With the partnership, TRMB effectively turned this negative situation into a less-risky-and-positive one, as it will be supplying core positioning services to AGCO. Also, the exit of this hardware business will also improve TRMB revenue mix to more recurring/software-based, which should also improve TRMB valuation multiple (the weaker hardware precision agriculture business is now a smaller portion of TRMB business).

Own calculation

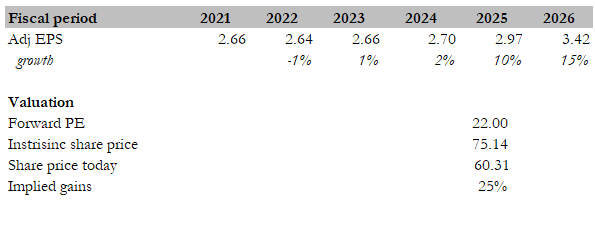

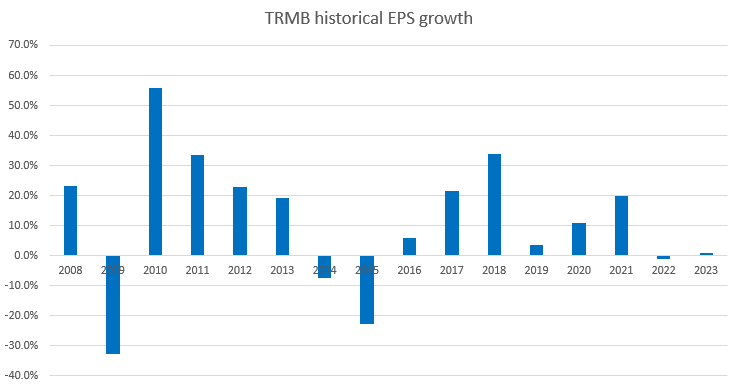

My target price for TRMB, based on my model, is $75 by the end of FY25. My model assumption is that adj EPS growth will follow a similar recovery pattern that TRMB has seen over the past 2 cycles (FY16-FY18 and FY19-FY21), growing 2% in FY24 (management guidance), 10% in FY25, and 15% in FY26. I believe there are three catalysts that will drive this performance. Firstly, the recovery of the global macroenvironment should lead to lower interest rates, thereby lowering mortgage rates, to drive a recovery in residential construction. Secondly, the resolution of conflict in the Red Sea should have an immediate impact on lowering commodity prices through lower freight costs, which should also relieve pressure on the TRMB transportation end market. Lastly, the successful execution of the JV with AGCO should better position TRMB for earnings growth as it positions itself away from competing with OEMs (instead, they are now riding on an OEM’s growth) and has a better revenue mix that should improve margins. As these three catalysts play out, TRMB should trade at a premium valuation to where it has historically traded (21x forward PE) as the business fundamentals turn positive for the near term.

Own calculation

Of the three catalysts, two are outside of TRMB control, which could get a lot worse than it is today. A key metric that is being observed by central banks is the inflation rate, and while it has come down in major regions, it has proven to be a lot stickier than expected. If it stays sticky and possibly re-inflects upwards again, it could lead to further rate hikes that are going to be extremely detrimental to TRMB end markets. Also, the conflict at the Red Sea has been going on longer than expected; if that conflict leads to a major war, it will put TRMB end markets under much more pressure.

I maintain my buy recommendation for TRMB, with the expectation that FY24 marks the beginning of a recovery for the company. Despite the stock's decline over the past year, recent positive developments, including solid 4Q23 results, indicate an improved outlook. While certain end markets, such as residential construction and agriculture, face challenges, I believe the recovery in global macroeconomy and the resolution of the Red Sea conflict will turn the situation around in these end markets. A key catalyst is the successful execution of the JV with AGCO, which should improve TRMB position in the value chain and its revenue mix.