ATU Images/The Image Bank via Getty Images

ATU Images/The Image Bank via Getty Images

Co-produced by Austin Rogers

The US economy as a whole might not be in recession, but it is certainly experiencing a "rolling recession" affecting specific industries.

One of the most obvious sectors of the economy that is suffering its own mini-recession is the housing market.

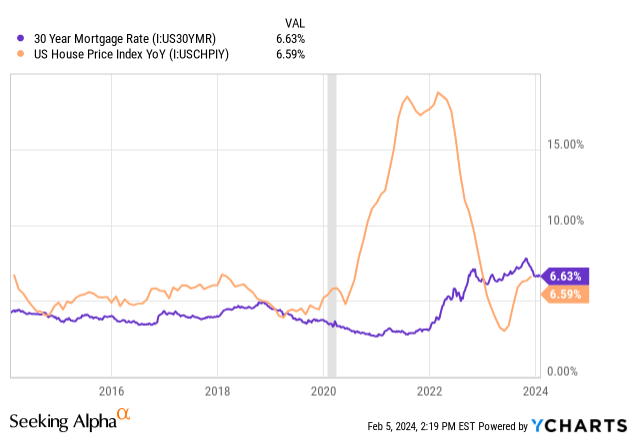

The ultra-low mortgage rates of 2020-2021 fueled a homebuying frenzy, especially among Millennials who are entering their prime single-family home years. Home prices soared, cooling only briefly as mortgage rate spiked to a 25-year high in 2023.

Today, home prices continue to rise as inventory of homes on the market is low and mortgage rates have receded a bit. No existing homeowner is eager to give up their current mortgage rate of 3-4% to move to another house that would have a 6.5%+ mortgage rate.

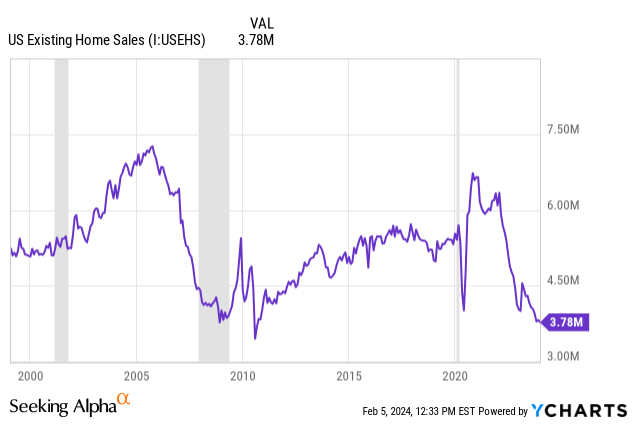

Hence we find that sales of existing homes (by far the largest part of the home sales market) has plunged to Great Financial Crisis-era lows.

It would not be too much of an exaggeration to call the US housing market "frozen."

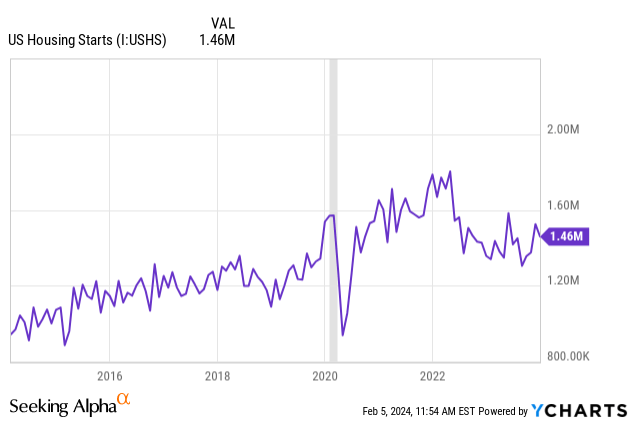

At the same time, US housing starts, which includes both single-family and multi-family housing, have dropped from their elevated post-pandemic levels and now hover below their pre-COVID trendline.

Thus, while home prices continue to hold up, the various industries that serve the housing market and thrive on home sales and construction are suffering their own mini-recession.

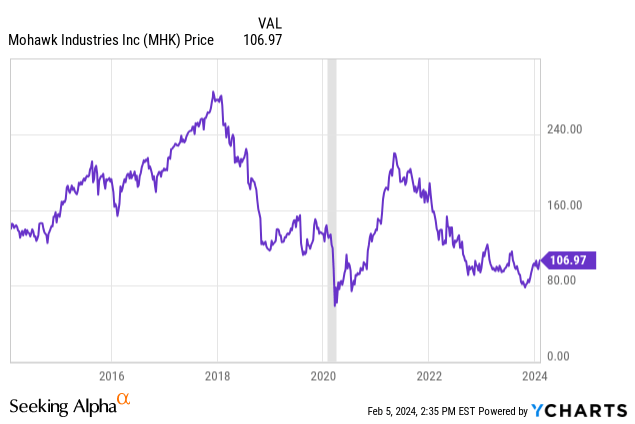

Take, for example, Mohawk Industries (MHK), a producer of various kinds of flooring, mainly for residential use. After its stock price surged during the go-go days of homebuying in 2021, it has since slumped back to COVID-era levels.

But Mohawk isn't one of the cyclical stocks we are covering in this article.

Instead, we want to take a look at two other, currently high-yielding cyclical companies that are being punished right now from the housing market recession. These two companies have excellent long-term track records of performance, boast leading market shares in their respective product lines, and enjoy long histories of paying dividends without cuts.

These two companies are Whirlpool (WHR) and Leggett & Platt (LEG).

Are the impressive dividend records of WHR and LEG at risk of coming to an end during the current housing market mini-recession?

Let's explore.

WHR is a leading American producer of household appliances, both large and small. They make refrigerators, oven/stoves, dishwashers, microwaves, laundry machines, and certain smaller appliances through their KitchenAid and InSinkErator brands.

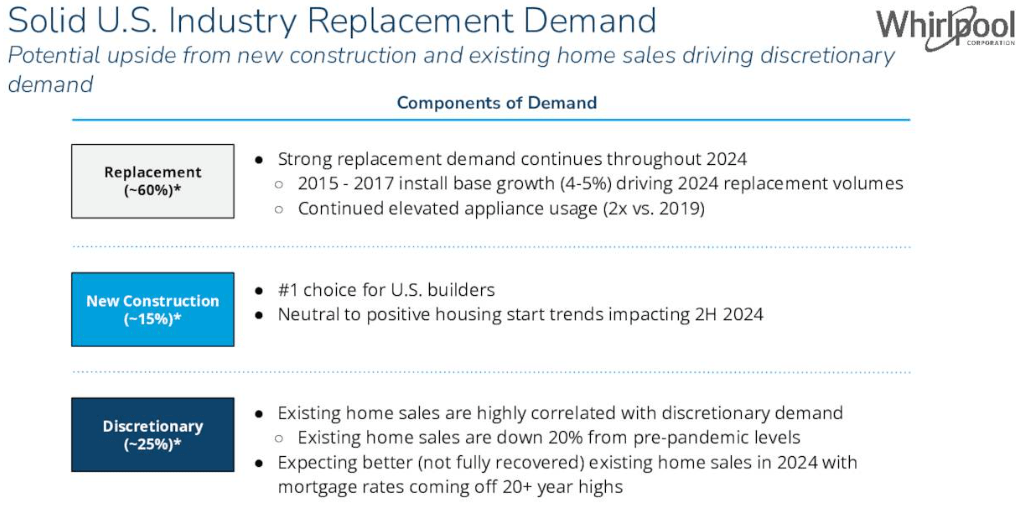

Historically, about half of WHR's sales are tied to home sales, with the other half being replacements. WHR boasts the #1 market position in appliances for new build homes, which obviously means more new home construction is good for WHR's business.

Currently, however, replacements account for around 60% of sales because of the drop in home sales.

WHR Q4 2023 Presentation

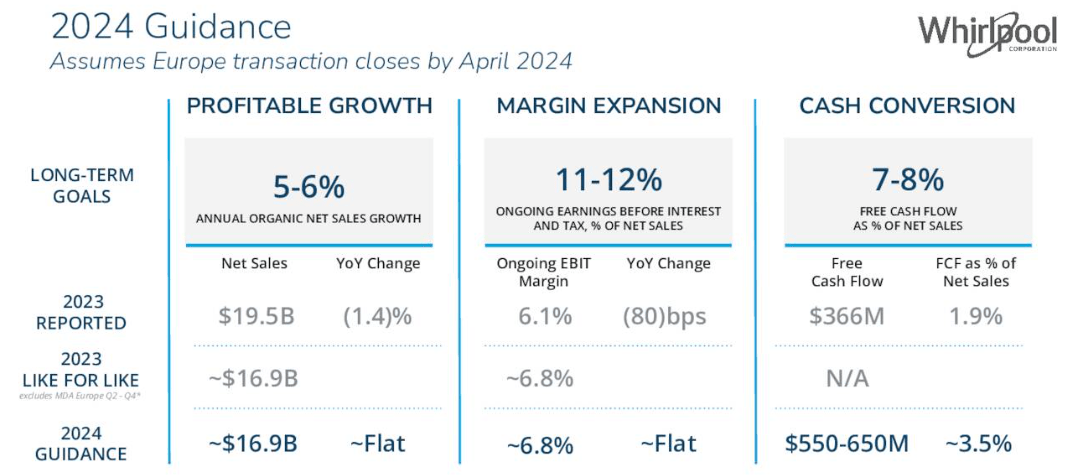

In 2023, sales came in roughly flat YoY, and while margins improved, free cash flow and FCF conversion dropped. Compared to WHR's long-term FCF conversion target of 7-8%, WHR generated a mere 1.9% FCF conversion in 2023, and 2024's metric is expected to improve only to ~3.5%.

Compared to 2023's $366 million in FCF, WHR has guided for a rebound in FCF in 2024 to $550-650 million against flat sales. This should be driven almost entirely by cost cuts -- $300-400 million worth of cost cuts, to be exact.

WHR Q4 2023 Presentation

This is an important metric to watch, because in 2023, WHR's ~$400 million dividend was not covered by FCF. Hopefully FCF will bounce back in 2024 to a sufficient degree to cover the dividend, deleverage, and perhaps also fund some share buybacks.

WHR's performance and dividend safety this year depends a lot on the direction of the housing market. If home sales volume makes a comeback this year and there is a rise in new homes getting built, then WHR should enjoy a nice rebound. If the housing market continues to languish with minimal home sales for most of the year, WHR's performance would likely continue to languish with it.

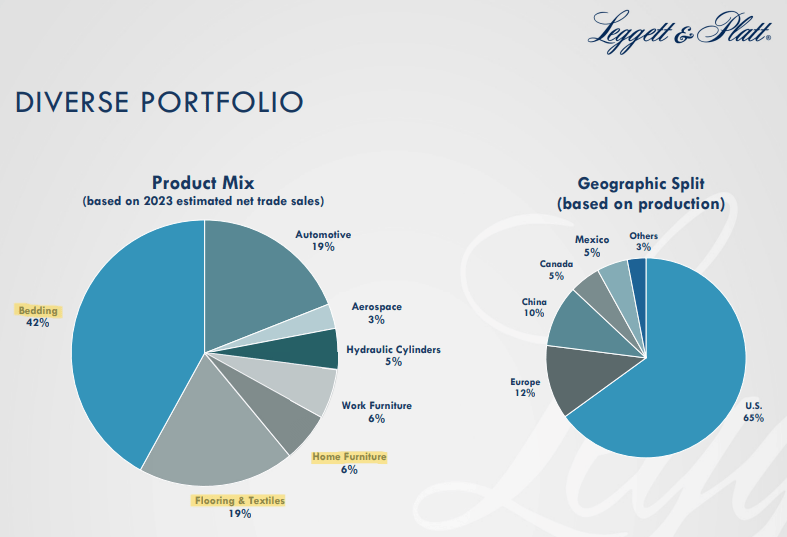

Meanwhile, LEG is a business-to-business industrial company that is not customer-facing. They produce intermediate components of bedding, flooring, furniture, and certain automotive and aerospace products. Roughly 2/3rds of LEG's products are directly or indirectly tied to the housing market and home sales.

LEG November Presentation

The biggest catalyst for buying new mattresses or furniture, after all, is moving into a new home. With fewer home sales, fewer people are moving into new homes.

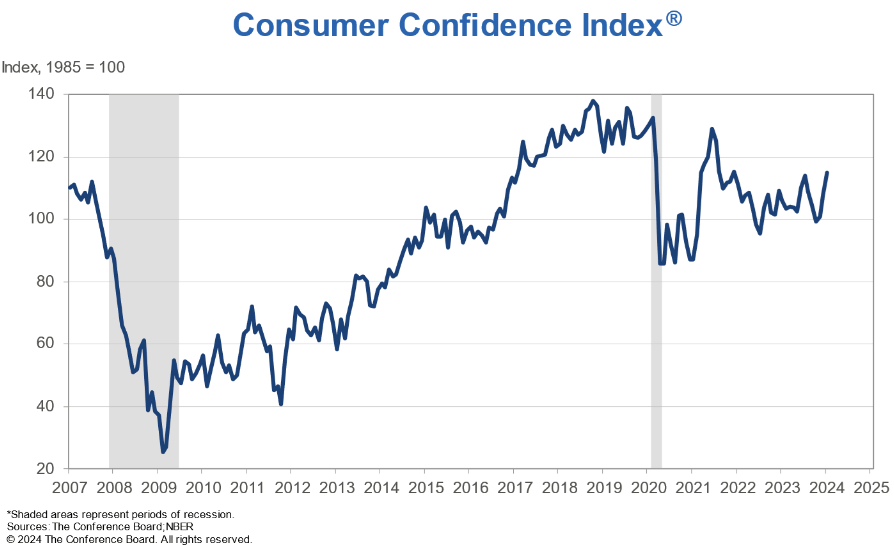

Of course, consumer confidence plays a big role in LEG's sales as well, because many if not most bed and furniture sales are to replace existing products. While consumer confidence took a bit hit during the pandemic and then again during the inflationary surge, confidence rebounded significantly in January.

The Conference Board

At the end of the day, bedding, furniture, and to some extent flooring are discretionary products that can be deferred for an indefinite period until consumers feel ready to spend money on them.

LEG has suffered in recent years not only from a downturn in home turnover but also from receding consumer desire to engage in those big-ticket discretionary product purchases.

While we do not have Q4 2023's earnings report yet as of this writing, LEG did have to lower guidance for 2023 sales and earnings in its Q3 earnings report because of weaker than expected sales volume.

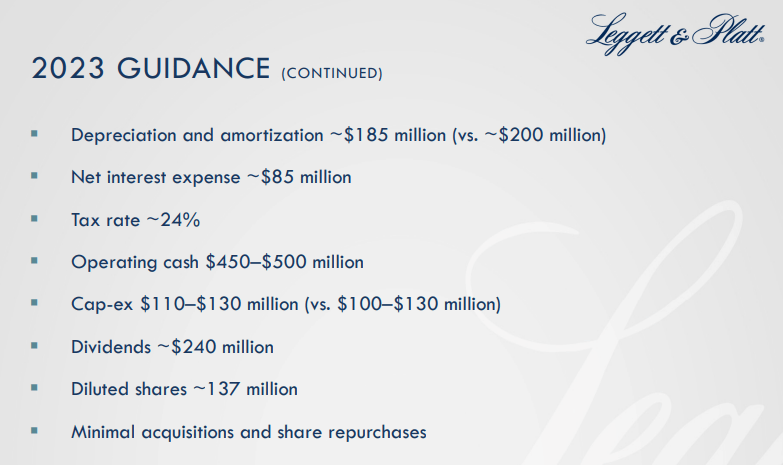

Even so, at the time, LEG still expected to generate free cash flow of $320-390 million, which would be more than sufficient to cover the ~$240 million annual dividend.

LEG November Presentation

Could LEG's performance outlook have eroded even more since then?

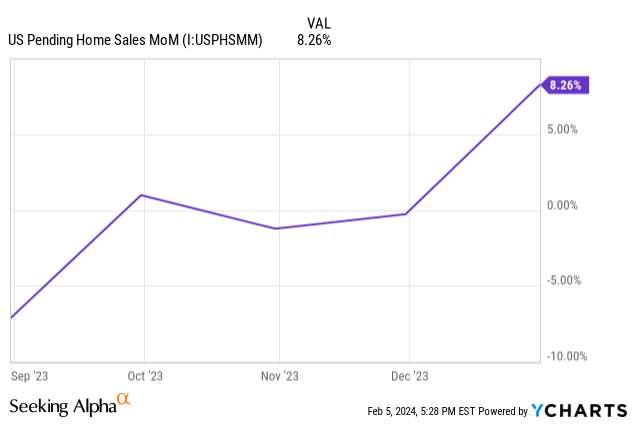

It's possible, but we doubt it. After all, as previously stated, consumer confidence has ticked up since then, and pending home sales have likewise risen over the last 3- and 6-month periods.

If this trend of more home sales continues into 2024, then LEG should be on the path to recovery this year just like WHR.

Assisting in this recovery path is a recently announced "restructuring"/cost-cutting plan that should see LEG generate an additional $40-50 million annualized by consolidating both its real estate footprint and its workforce.

The analysts' estimate of revenue and earnings rebounds for bedding and furniture companies like Tempur Sealy (TPX) and Haverty Furniture (HVT) in 2024 is encouraging, even if preliminary at this time.

There is always uncertainty in the markets, but when it comes to these two cyclical stocks leveraged to the housing market, this year brings with it an elevated level of uncertainty. A lot depends on what happens with the housing market and consumer confidence.

That said, there are some reasons to believe it is unlikely that either WHR or LEG will cut their dividends this year.

First, both have very impressive dividend records.

While WHR is not a dividend aristocrat because it has had to pause its dividend growth for a few periods of time (including the last few years), the company has also paid uninterrupted, steady or increasing dividends every year for the last 68 years.

On the Q4 conference call, WHR's management made clear their intention to pay the same dividend in 2024 as they did in 2023.

Meanwhile, LEG is a dividend king, having raised its dividend over the last 50+ consecutive years. Management have indicated their intention to preserve and extend that record.

Second, both companies have strong cash generation abilities even in the midst of the presently difficult environment. WHR expects to generate more than enough FCF to cover its dividend in 2024, and LEG expected to do so for 2023 as of the last report.

Third, both companies have some liquidity providing the flexibility needed to sustain the dividend for a quarter or two if and when FCF doesn't cover it completely.

WHR ended 2024 with $1.6 billion in cash, while LEG ended Q3 2023 with about $274 million in cash along with a $1.2 billion credit revolver with little drawn on it.

This year will undoubtedly be a difficult one for industries that rely on a smoothly functioning housing market. Uncertainty about the performance of WHR and LEG is higher than normal in 2024.

That said, the Federal Reserve has still forecast the likelihood of cutting rates sometime this year. This should help push mortgage rates down, which in turn should give a boost to home sales volume. WHR and LEG should indirectly benefit from that.

We are cautiously optimistic about the prospects of both these blue-chip cyclical names. Although we acknowledge the possibility of dividend cuts this year, we think it is more likely that we will see a recovery this year for both companies and that their dividends will remain intact.

For those who would like to own either or both of these cyclical dividend payers, we think right now may be the best time in the cycle to buy.